Reports

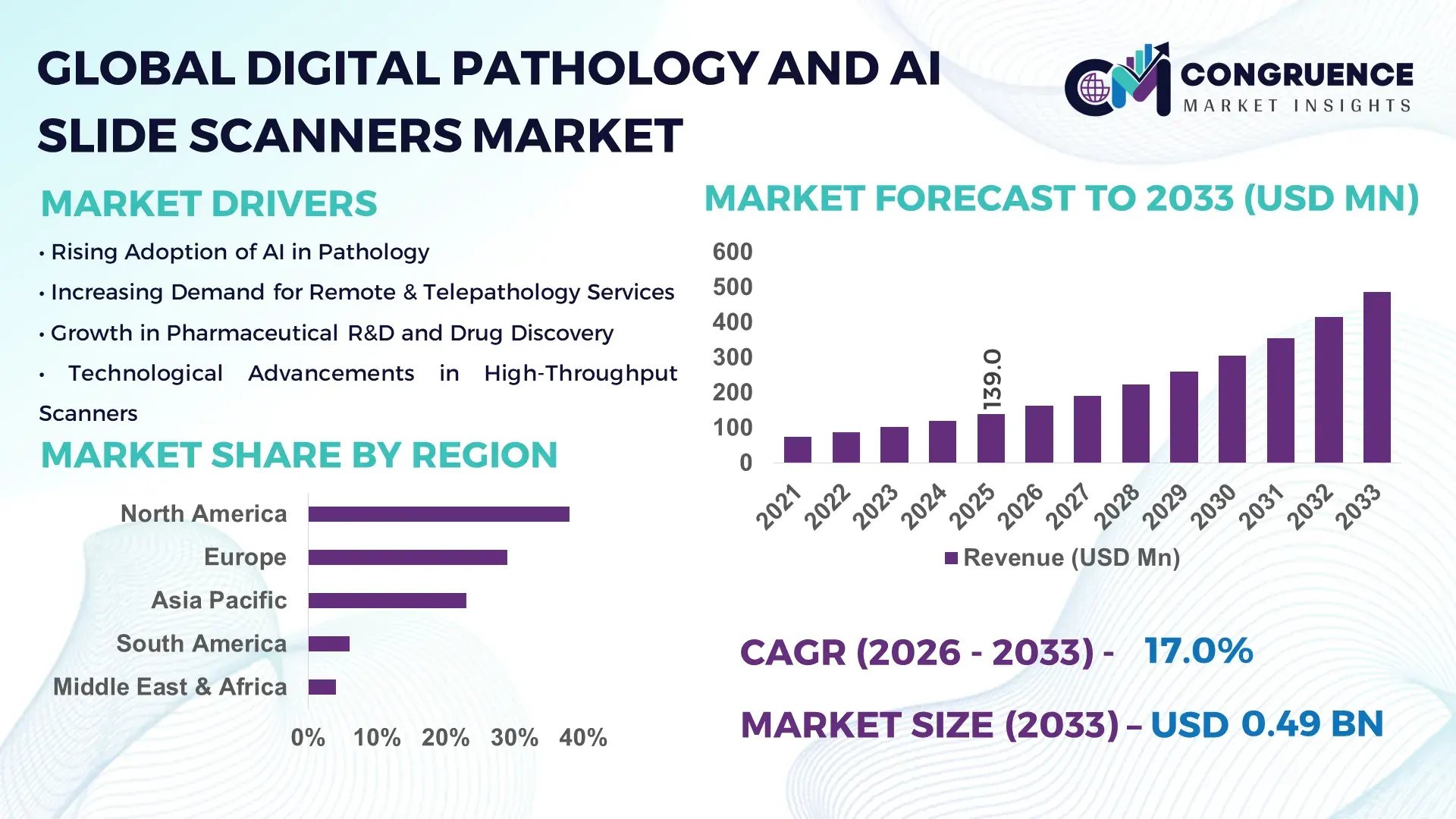

The Global Digital Pathology and AI Slide Scanners Market was valued at USD 139.0 Million in 2025 and is anticipated to reach a value of USD 486.4 Million by 2033, expanding at a CAGR of 16.95% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is supported by accelerating adoption of AI-assisted diagnostics, rising digital transformation across pathology laboratories, and increasing demand for faster, standardized clinical workflows.

The United States represents the dominant country in the Digital Pathology and AI Slide Scanners Market, supported by advanced healthcare infrastructure and strong technological integration across pathology services. Over 65% of large hospital networks in the U.S. have initiated digital pathology workflows, with more than 1,500 high-throughput slide scanners deployed across academic medical centers and reference laboratories. Annual investments exceeding USD 450 million are directed toward AI-enabled diagnostic imaging and pathology automation. The country also leads in FDA-cleared AI pathology algorithms, with applications spanning oncology, hematopathology, and companion diagnostics. Additionally, over 70% of AI pathology pilots globally originate from U.S.-based institutions, highlighting deep clinical adoption and innovation intensity.

Market Size & Growth: Valued at USD 139.0 Million in 2025, projected to reach USD 486.4 Million by 2033, growing at 16.95% CAGR, driven by AI-enabled diagnostic accuracy and workflow automation.

Top Growth Drivers: AI adoption in pathology labs (62%), diagnostic turnaround time reduction (48%), digital slide archival efficiency gains (41%).

Short-Term Forecast: By 2028, AI-assisted slide analysis is expected to improve pathology workflow efficiency by 35%.

Emerging Technologies: Deep learning-based image analysis, cloud-based digital pathology platforms, and multimodal AI diagnostics.

Regional Leaders: North America (USD 198.0 Million by 2033) with enterprise-wide deployments; Europe (USD 156.5 Million) driven by public healthcare digitization; Asia Pacific (USD 101.9 Million) led by rapid lab modernization.

Consumer/End-User Trends: Hospitals and reference laboratories account for over 60% of scanner utilization, with rising adoption in contract research organizations.

Pilot or Case Example: In 2024, a U.S. academic hospital reduced diagnostic turnaround time by 27% using AI slide triaging.

Competitive Landscape: Leica Biosystems (~22% share) followed by Philips, Hamamatsu Photonics, 3DHISTECH, and Roche Diagnostics.

Regulatory & ESG Impact: Increasing regulatory clearances for AI diagnostics and digital data traceability mandates.

Investment & Funding Patterns: Over USD 1.2 Billion invested globally since 2021 in AI pathology platforms and scanner innovation.

Innovation & Future Outlook: Integration of AI with laboratory information systems and cross-site telepathology networks is shaping long-term growth.

Digital Pathology and AI Slide Scanners Market adoption is driven by oncology diagnostics contributing nearly 45% of usage, followed by research and drug development at 30%. Recent innovations include sub-micron resolution scanners and AI-powered tumor grading tools. Regulatory digitization initiatives, growing remote diagnostics demand, and strong uptake in North America and Europe support sustained growth, while Asia Pacific shows rising consumption due to expanding diagnostic lab capacity and healthcare digitization.

The Digital Pathology and AI Slide Scanners Market holds strong strategic relevance as healthcare systems prioritize diagnostic accuracy, speed, and scalability. AI-driven slide scanners enable standardized digital workflows, reducing inter-observer variability by measurable margins. For instance, deep learning–based pathology platforms deliver up to 40% improvement in diagnostic consistency compared to conventional manual microscopy, positioning AI as a critical productivity lever.

From a regional perspective, North America dominates in deployment volume, while Europe leads in adoption density, with over 52% of pathology laboratories integrating digital workflows into routine diagnostics. Asia Pacific is emerging rapidly, driven by centralized lab models and expanding cancer screening programs. By 2027, AI-powered slide pre-screening is expected to cut pathologist review time by nearly 30%, improving laboratory throughput and patient turnaround metrics.

Compliance and ESG considerations are increasingly shaping market pathways. Healthcare providers are committing to 30–40% reductions in physical slide storage and chemical usage by 2030, enabled through digital archiving and remote review models. In 2024, a leading U.S. healthcare network achieved a 25% reduction in diagnostic backlog after deploying AI-based slide prioritization across oncology departments.

Looking ahead, the Digital Pathology and AI Slide Scanners Market is positioned as a pillar of diagnostic resilience, regulatory compliance, and sustainable healthcare growth, supporting precision medicine, decentralized diagnostics, and data-driven clinical decision-making globally.

The Digital Pathology and AI Slide Scanners Market dynamics are shaped by accelerating digital transformation across clinical diagnostics, rising cancer incidence, and increasing reliance on data-driven pathology workflows. Healthcare providers are shifting from analog microscopy toward fully digitized slide management to improve traceability, collaboration, and turnaround times. Integration with laboratory information systems and cloud platforms is enhancing cross-site diagnostics and remote consultations. Meanwhile, regulatory acceptance of AI-assisted diagnostic tools is strengthening confidence among hospitals and reference labs. However, variability in digital infrastructure readiness across regions and skill gaps among pathology professionals continue to influence adoption patterns.

The growing need for rapid and standardized diagnostic outcomes is a major driver for the Digital Pathology and AI Slide Scanners Market. Global pathology workloads have increased by over 20% in the last five years, largely due to rising cancer screening and aging populations. Digital slide scanners enable batch processing of thousands of slides daily, significantly improving laboratory throughput. AI-assisted pre-screening tools help prioritize high-risk cases, reducing manual review burden and enabling pathologists to focus on complex diagnostics. Hospitals adopting digital pathology report measurable reductions in diagnostic turnaround time and improved inter-laboratory collaboration.

High upfront system integration complexity and workforce training requirements remain key restraints. Deploying digital pathology systems often requires upgrades to IT infrastructure, secure data storage, and interoperability with existing laboratory systems. Studies indicate that over 35% of mid-sized laboratories delay adoption due to limited digital readiness. Additionally, training pathologists and technicians to effectively use AI-assisted tools can take several months, impacting short-term productivity. Data security and compliance requirements further increase implementation complexity, particularly in regions with stringent healthcare data regulations.

The expansion of AI-assisted oncology diagnostics presents significant opportunities for the Digital Pathology and AI Slide Scanners Market. Oncology accounts for nearly half of digital pathology use cases, with AI algorithms increasingly applied for tumor detection, grading, and biomarker analysis. Pharmaceutical companies and research institutions are adopting digital pathology to support clinical trials and companion diagnostics. Growing investments in precision medicine and personalized therapies are creating demand for high-resolution scanners capable of handling complex multi-stain slides, opening new avenues for advanced imaging solutions.

Regulatory variability across regions poses a notable challenge. While some markets have clear approval pathways for AI-assisted diagnostics, others require extensive clinical validation and multi-year review processes. Validation of AI algorithms across diverse populations and staining protocols adds complexity and cost for manufacturers. Laboratories must also comply with quality assurance standards and continuous performance monitoring, increasing operational overhead. These factors can slow deployment timelines and limit near-term scalability, particularly in emerging healthcare markets.

Expansion of AI-Driven Diagnostic Automation: AI-powered slide scanners are increasingly used for automated tissue detection and case prioritization. Over 60% of newly installed systems in 2024 incorporated AI modules, enabling up to 35% reduction in manual review time and improving diagnostic consistency across large pathology networks.

Growth of Cloud-Based Digital Pathology Platforms: Cloud-enabled slide management is gaining traction, with nearly 45% of digital pathology labs adopting cloud storage and remote access solutions. This shift has supported cross-site collaboration and reduced physical slide transport costs by approximately 30%, particularly in multi-hospital systems.

Increasing Adoption in Drug Discovery and Clinical Trials: Pharmaceutical and biotech companies now account for roughly 28% of digital slide scanner utilization, using AI pathology for biomarker validation and toxicity studies. AI-assisted image analysis has improved trial data processing efficiency by 25%, accelerating research timelines.

Regulatory Acceptance and Standardization Momentum: The number of AI-enabled pathology tools cleared for clinical use increased by over 40% between 2022 and 2024. Standardized digital workflows are helping laboratories meet audit and traceability requirements, while reducing slide reprocessing rates by nearly 20% across regulated environments.

The Digital Pathology and AI Slide Scanners Market is segmented based on type, application, and end-user, each reflecting distinct adoption patterns and operational priorities across the healthcare ecosystem. By type, segmentation highlights differences in scanning throughput, automation level, and integration with AI-driven image analysis. Application-based segmentation emphasizes diagnostic specialization, research intensity, and workflow complexity, particularly in oncology and drug development. End-user segmentation illustrates how hospitals, diagnostic laboratories, and research institutions vary in scale, budget allocation, and digital maturity. Across segments, adoption is strongly influenced by case volume growth, demand for diagnostic standardization, and regulatory acceptance of digital pathology workflows. Increasing interoperability with laboratory information systems and remote consultation platforms further shapes segmentation dynamics, making this market highly differentiated by use-case intensity and institutional readiness rather than uniform technology uptake.

The Digital Pathology and AI Slide Scanners Market by type includes high-throughput whole slide scanners, mid-throughput scanners, low-throughput scanners, and portable or compact scanners. High-throughput whole slide scanners currently lead the segment, accounting for approximately 46% of total adoption, as they are extensively deployed in large hospitals, reference laboratories, and academic centers handling thousands of slides daily. Their dominance is supported by automation features, barcode-based traceability, and seamless AI algorithm integration for tumor detection and grading.

Mid-throughput scanners represent a balanced alternative for regional laboratories and specialty clinics, while low-throughput scanners serve niche diagnostic centers with limited daily volumes. Portable and compact scanners, though still emerging, are gaining attention for decentralized diagnostics and field-based pathology use. Among all types, portable and compact AI-enabled scanners are the fastest-growing segment, expanding at an estimated 19.8% CAGR, driven by point-of-care testing, mobile labs, and rising telepathology programs. The remaining scanner types collectively contribute roughly 54% of the market, serving stable, volume-specific operational needs.

By application, the Digital Pathology and AI Slide Scanners Market spans disease diagnosis, drug discovery and development, academic research, and telepathology services. Disease diagnosis remains the leading application, accounting for nearly 49% of overall utilization, supported by high volumes in oncology, dermatopathology, and hematopathology. Digital slides combined with AI-assisted analysis improve diagnostic consistency and enable faster second opinions across institutions.

Drug discovery and development is the fastest-growing application, expanding at an estimated 18.6% CAGR, as pharmaceutical companies increasingly rely on AI-powered pathology for biomarker validation, toxicity studies, and companion diagnostics. Academic and translational research continues to play a foundational role, while telepathology applications are expanding rapidly in multi-site healthcare networks. The remaining applications together represent approximately 51% of total adoption. In 2025, over 41% of global pharmaceutical R&D organizations reported active use of AI-based digital pathology platforms, while nearly 44% of U.S. hospitals indicated pilot programs combining digital slides with patient data for complex case reviews.

End-user segmentation includes hospitals and clinics, diagnostic and reference laboratories, pharmaceutical and biotechnology companies, and academic and research institutions. Hospitals and clinics form the leading end-user segment, accounting for approximately 43% of total adoption, driven by rising diagnostic workloads, multispecialty pathology departments, and integration with electronic health records. Diagnostic and reference laboratories follow closely, benefiting from centralized slide processing and AI-based workload prioritization.

Pharmaceutical and biotechnology companies represent the fastest-growing end-user group, expanding at an estimated 20.3% CAGR, fueled by increased use of digital pathology in clinical trials and precision medicine programs. Academic and research institutions maintain steady adoption, contributing to innovation and validation of new AI models. Collectively, non-hospital end-users account for around 57% of market participation, reflecting diversification beyond traditional clinical settings. In 2025, over 39% of large diagnostic laboratories globally reported scaling AI slide scanning across multiple locations, while more than 46% of biopharma firms integrated digital pathology into preclinical research workflows.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.6% between 2026 and 2033.

The regional landscape of the Digital Pathology and AI Slide Scanners Market reflects uneven digital maturity, healthcare infrastructure depth, and regulatory readiness. North America leads due to high deployment density of AI-enabled scanners, with more than 65% of tertiary hospitals operating partial or full digital pathology workflows. Europe follows with approximately 29% share, driven by national digitization programs and centralized laboratory networks. Asia-Pacific contributes nearly 23%, supported by rapid laboratory expansion, rising cancer diagnostics volumes exceeding 9 million new cases annually, and strong public–private investments. South America and the Middle East & Africa together account for the remaining 10%, where adoption is concentrated in urban healthcare hubs and government-backed modernization programs.

The region holds an estimated 38% share of the global Digital Pathology and AI Slide Scanners Market, supported by strong demand from hospitals, reference laboratories, and academic medical centers. Oncology diagnostics, clinical research, and companion diagnostics are the primary demand drivers, with cancer-related pathology accounting for nearly 52% of scanner utilization. Regulatory clarity around digital diagnostics and AI-assisted tools has accelerated enterprise adoption, while federal and state-level health IT funding continues to support digital transformation. Technological advancements include large-scale deployment of AI-based slide triage, cloud-connected scanners, and integration with electronic health records. A notable regional player, Leica Biosystems, has expanded high-throughput scanner installations across multi-hospital networks, enabling centralized slide analysis. Consumer behavior reflects high enterprise readiness, with over 58% of healthcare systems prioritizing AI-enabled diagnostics to address pathologist shortages and improve turnaround times.

Europe accounts for approximately 29% of global market activity, with strong concentration in Germany, the UK, and France, which together represent over 60% of regional demand. Public healthcare systems are driving adoption through national digital pathology initiatives and centralized laboratory models. Regulatory bodies emphasize data transparency and validation, increasing demand for explainable AI tools in pathology. Sustainability initiatives promoting reduced chemical usage and physical slide storage further support digital workflows. Emerging technologies such as AI-assisted grading and cross-border telepathology networks are gaining traction. Regional players like 3DHISTECH are expanding scanner deployments across academic and public laboratories. Consumer behavior varies by country, but regulatory pressure consistently drives demand for validated, auditable AI-enabled pathology solutions across hospital networks.

Asia-Pacific ranks third by market size, contributing close to 23% of global adoption, and shows the highest growth momentum by volume expansion. China, Japan, and India are the top consuming countries, together accounting for over 70% of regional installations. Rapid expansion of diagnostic laboratories, rising cancer incidence, and government-led healthcare modernization are key factors. Manufacturing and assembly of mid-range and compact scanners are increasing locally, improving affordability. Regional innovation hubs in Japan and South Korea are advancing AI pathology algorithms, while China leads in large-scale hospital digitization. Companies such as Hamamatsu Photonics are strengthening regional supply chains and technology localization. Consumer behavior shows strong preference for scalable, mobile-enabled diagnostic platforms, with digital adoption often aligned with mobile health ecosystems.

South America represents around 6% of the global market, with Brazil and Argentina as the primary contributors. Adoption is concentrated in metropolitan hospitals and private diagnostic chains, where pathology digitization supports oncology and infectious disease diagnostics. Infrastructure development in healthcare facilities and regional trade policies supporting medical equipment imports have facilitated market entry. Government-backed digital health initiatives are expanding access to advanced diagnostics in urban centers. Local distributors and system integrators are increasingly partnering with global manufacturers to deploy AI-enabled scanners. Consumer behavior reflects growing demand for localized diagnostic services, with adoption tied closely to language-specific reporting and regional clinical standards.

The Middle East & Africa region accounts for approximately 4% of global adoption, with growth driven by healthcare infrastructure investments rather than legacy replacement. UAE, Saudi Arabia, and South Africa are the leading markets, supported by national healthcare modernization programs. Digital pathology adoption is strongest in large tertiary hospitals and private healthcare groups. Technological modernization includes cloud-based slide storage and remote pathology consultations to address specialist shortages. Trade partnerships and regulatory harmonization initiatives are improving access to advanced diagnostic equipment. Consumer behavior varies widely, but institutional demand is rising for centralized diagnostic hubs that reduce dependency on overseas pathology services.

United States – 32% Market Share: High deployment density across hospitals and research institutions supported by advanced AI-ready healthcare infrastructure.

Germany – 11% Market Share: Strong public healthcare digitization and centralized laboratory systems driving consistent demand for digital pathology solutions.

The competitive environment in the Digital Pathology and AI Slide Scanners Market is characterized by a moderately consolidated structure with a large number of global and regional vendors competing across scanner hardware, software platforms, and integrated AI diagnostics. There are more than 50 active competitors globally, spanning established imaging incumbents to specialized AI pathology software firms. The top 5 companies collectively account for approximately 58–62% of installed base share, with major players such as Leica Biosystems, Philips Healthcare, Hamamatsu Photonics, Roche (Ventana Medical Systems), and 3DHISTECH dominating high-throughput slide scanning and digital pathology workflow solutions.

Strategic initiatives in the market include product launches of next-generation scanners with higher throughput and advanced analytics, multiple partnerships integrating cloud and AI capabilities into pathology ecosystems, and certification achievements enabling geographic expansion. In 2024 and 2025, leading vendors introduced enhanced whole slide imaging systems and expanded software suites to support enterprise diagnostic workflows and remote telepathology. Innovation trends shaping competition include AI-assisted image analysis, cloud-native pathology platforms, and multi-modal imaging compatibility for fluorescence and brightfield scans. Competitive positioning varies: established industrial imaging firms leverage long-standing clinical relationships and service networks, while agile AI-focused companies compete on analytics performance and integration flexibility. Market entrants are increasingly prioritizing workflow automation, interoperability with LIS/EHR systems, and platform ecosystems combining scanning hardware with AI diagnostics and data management tools.

3DHISTECH Ltd.

Roche (Ventana Medical Systems)

Olympus Corporation

Nikon Corporation

Indica Labs

Huron Digital Pathology

OptraSCAN

Mikroscan Technologies

Epredia

Glencoe Software

Visiopharm

Sectra AB

Akoya Biosciences

Inspirata

ContextVision

PathAI

Proscia Inc.

The Digital Pathology and AI Slide Scanners Market is being reshaped by several current and emerging technologies that enhance diagnostic throughput, image quality, and AI-driven decision support. Whole Slide Imaging (WSI) remains the foundational technology, with systems capable of scanning full slides at resolutions of 0.25 microns per pixel in under 60 seconds, enabling rapid digitization for primary diagnosis workflows and supporting more than 70% of newly digitized labs. WSI’s widespread adoption is complemented by cloud-based storage and collaboration platforms enabling remote access to slide archives and telepathology consultations across sites, handling hundreds of gigabytes of digital slide data daily.

AI integration is central: AI-assisted image analysis algorithms provide pattern recognition, anomaly detection, and quantitative biomarker measurement that improve diagnostic consistency and triage efficiency, reducing manual review bottlenecks. Innovations in mixed-reality visualization and AI conversational interfaces are emerging, allowing pathologists to interact with slide images using immersive technologies and integrated query systems. Multi-modal imaging technologies, combining brightfield with fluorescence and confocal scanning, are gaining traction in oncology research and complex tissue analysis.

Automation technologies — including continuous slide loading, auto-focus systems, and voice-controlled operations — enhance scanner throughput, while compact and portable scanners extend digital pathology into decentralized and resource-limited settings. The market also sees technological convergence with interoperability standards that enable seamless data exchange between slide scanners, laboratory information systems (LIS), and electronic health records, supporting unified clinical workflows. Additionally, digital pathology software ecosystems are advancing to include integrated case management, AI analytics marketplaces, and predictive diagnostics modules that support evidence-based clinical decision support.

• In December 2025, Leica Biosystems expanded its clinical digital pathology portfolio at the Digital Pathology and AI (DPAI) Congress in London with the launch of the Aperio GT 180 DX scanner, Aperio CS5 DX scanner, and Aperio iQC DX software, enhancing quality control automation and mid-volume scanning options for pathology laboratories. Source: www.leicabiosystems.com

• In September 2025, Hamamatsu Photonics received CDSCO medical device approval in India for its NanoZoomer® S360MD and S20MD whole slide imaging systems, enabling Indian pathology labs to adopt high-precision scanning technologies for faster and more accurate diagnostics. Source: www.hamamatsu.com

• In September 2025, Philips announced the world’s first digital pathology scanner offering native configurable DICOM JPEG and JPEG XL output, significantly reducing image file sizes by up to 50% while maintaining high resolution, supporting scalable storage and interoperability. Source: www.philips.com

• In March 2025, Vieworks unveiled the VISQUE DPS digital pathology system at the USCAP Annual Meeting in Boston, marking its North American debut and signaling expansion of its imaging solutions into major international markets to support clinical research and diagnostic workflows. Source: www.vieworks.com

The scope of the Digital Pathology and AI Slide Scanners Market Report encompasses comprehensive analysis of segmentation landscapes, including scanner types, technological frameworks, applications, and end-user profiles. It examines scanner products across capabilities such as whole slide imaging, high-throughput automation, fluorescence and multi-modal imaging, and compact portable systems optimized for diverse clinical environments. Geographic regions covered include North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with in-depth assessment of market dynamics, infrastructure readiness, and adoption trends in major markets such as the United States, Germany, China, Japan, Brazil, and UAE.

Application focus areas range from clinical diagnostics, oncology pathology, and routine histopathology to pharmaceutical research, companion diagnostics, and telepathology networks, illustrating how digital slide scanners support diagnostic accuracy, cross-site collaboration, and research throughput. The report also explores technological innovations such as AI-enhanced slide analysis, cloud-native digital pathology platforms, interoperable data frameworks with LIS/EHR systems, and emerging visualization tools like mixed-reality interfaces. End-user sectors profiled include hospitals and healthcare systems, diagnostic laboratories, academic research institutions, and biopharma companies, offering insights into deployment priorities, workflow optimization, and investment patterns. Additionally, it covers competitive intelligence, strategic initiatives by key market participants, regulatory compliance landscapes, and innovation trajectories shaping future adoption and market evolution.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 139.0 Million |

| Market Revenue (2033) | USD 486.4 Million |

| CAGR (2026–2033) | 16.95% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Leica Biosystems, Philips Healthcare, Hamamatsu Photonics, 3DHISTECH Ltd., Roche (Ventana Medical Systems), Olympus Corporation, Nikon Corporation, Indica Labs, Huron Digital Pathology, OptraSCAN, Mikroscan Technologies, Epredia, Glencoe Software, Visiopharm, Sectra AB, Akoya Biosciences, Inspirata, ContextVision, PathAI, Proscia Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |