Reports

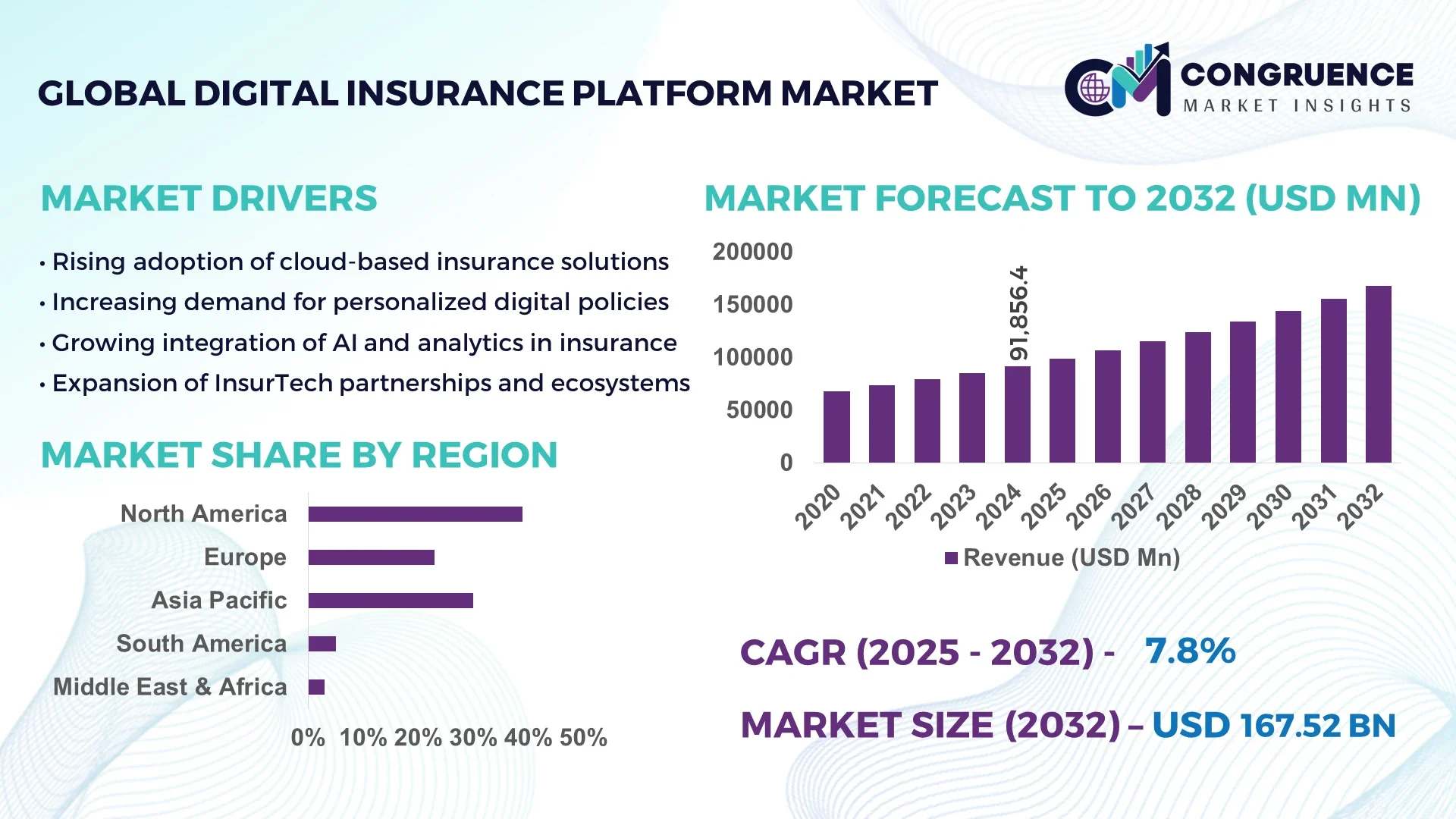

The Global Digital Insurance Platform Market was valued at USD 91856.38 Million in 2024 and is anticipated to reach a value of USD 167517.2 Million by 2032 expanding at a CAGR of 7.8%% between 2025 and 2032.

In China, production capacity has surged with digital insurers like Yuanbao leveraging over 4,000 AI models to power dynamic policy pricing and personalized coverage, while traditional players such as China Life reported net profit growth and high solvency ratios, reflecting substantial investment in technological advancement and industry applications.

Within the Digital Insurance Platform Market, key industry sectors include platform/software—accounting for nearly three-quarters of the market in 2024—and services poised for accelerated growth through 2030. Cloud deployments dominate, capturing over 63% of the market, while hybrid models are rapidly gaining traction. Recent technological innovations include embedded insurance partnerships and generative-AI pilots reshaping distribution and underwriting economics, alongside migration away from legacy tools toward fully integrated ecosystems. Regulatory mandates, economic modernization, and environmental resilience are pressing insurers to modernize systems, monetize data, and address compliance imperatives. Regional consumption patterns reveal North America as a fast adopter, while Asia-Pacific shows rapid growth. Emerging trends suggest a future shaped by generative AI, embedded insurance, and hybrid deployments, enabling scalable, data-driven operations tailored to decision-makers and industry professionals.

Artificial intelligence is redefining the Digital Insurance Platform Market by enhancing underwriting speed, claims processing accuracy, and personalized customer engagement. In 2025, 76 percent of U.S. insurers have already integrated generative AI into business functions such as claims processing, customer service, and distribution, accelerating enterprise-wide adoption. Many firms are pivoting from experimentation to full-scale deployment. AI enables automation of broker management, risk assessment, and customer touchpoints—translating into streamlined workflows, reduced processing times, and improved customer satisfaction. Insurers expanding technology budgets are directing the bulk of investments toward AI, signaling that Digital Insurance Platform Market strategies are increasingly AI-centric.

Small language models (SLMs) optimized for insurance-specific use cases are improving accuracy in pricing and personalized offerings, enabling carriers to deliver smarter, faster, and more intuitive services. Generative AI is central to modernization, powering product innovation and operational efficiency across the value chain. The result is enhanced policy agility, tailored risk solutions, and scalable deployment of digital platforms that elevate decision-maker confidence and performance.

“In May 2025, Zurich Insurance Group launched a new AI-powered customer relationship management platform that, by following a “three-click rule,” reduced service times by over 70 percent through centralized policy data and AI-driven product recommendations.” This concrete AI deployment within the Digital Insurance Platform Market demonstrates measurable operational improvement and strategic innovation.

The Digital Insurance Platform Market is experiencing rapid transformation driven by technology integration, regulatory modernization, and evolving customer expectations. Insurers are moving from legacy systems to agile, AI-enabled digital platforms that enhance underwriting, claims management, and customer service. Cloud deployment and embedded insurance solutions are accelerating adoption across both developed and emerging regions. Strategic partnerships between insurtech firms and established insurers are reshaping the ecosystem, while regulatory emphasis on compliance, transparency, and data security adds another layer of influence. With rising consumer demand for personalized and on-demand policies, the Digital Insurance Platform Market is set to expand through continuous innovation, operational agility, and digital-first strategies tailored for industry professionals.

The growing integration of AI and automation into the Digital Insurance Platform Market is significantly enhancing operational efficiency and customer experiences. Automated claims settlement has reduced processing times by nearly 60% in some insurers, enabling quicker resolution and improving customer trust. AI-driven chatbots are managing millions of policyholder queries annually, minimizing human intervention while ensuring 24/7 service availability. Predictive analytics is increasingly being applied to risk assessment and fraud detection, which strengthens underwriting accuracy and reduces losses. The impact of AI is evident across value chains as insurers utilize machine learning models for real-time data processing, resulting in scalable digital platforms that align with evolving customer expectations and improve profitability.

The Digital Insurance Platform Market faces restraints due to stringent and constantly evolving regulatory frameworks across different regions. Compliance with data protection laws, cybersecurity requirements, and insurance-specific regulations demands significant investment and technical expertise. For example, GDPR in Europe and similar frameworks in Asia-Pacific have increased compliance costs for insurers deploying cloud-based platforms. Additionally, maintaining transparency in AI-driven underwriting decisions remains a regulatory challenge, as oversight authorities demand explainability and fairness in automated processes. These legal and compliance burdens often delay innovation, increase implementation timelines, and raise operational costs, thereby restraining the pace of market expansion.

The rise of embedded insurance presents a compelling opportunity within the Digital Insurance Platform Market. Embedded models, integrated seamlessly into consumer ecosystems such as retail, e-commerce, and mobility services, are forecast to account for a growing proportion of digital policies in the coming years. Personalized insurance, supported by AI-powered insights, is enabling insurers to design coverage tailored to individual lifestyles, health conditions, and financial needs. With connected devices and IoT adoption expanding globally, insurers can access real-time data to create highly customized offerings. These innovations allow for higher customer retention, increased market penetration, and greater adaptability to consumer demand, positioning digital platforms as key enablers of next-generation insurance solutions.

Despite its potential, the Digital Insurance Platform Market is challenged by high initial implementation costs and the complexity of integrating new systems with existing legacy infrastructure. Migrating millions of policies and customer data into cloud-based platforms requires robust investment in cybersecurity, advanced analytics, and workforce training. Smaller insurers often face financial strain in adopting large-scale digital systems, leading to slower modernization. Furthermore, integration with third-party applications, regulatory tools, and AI models introduces technical complexities that can disrupt business continuity if not managed effectively. These challenges slow down digital transformation initiatives and create barriers for insurers seeking to achieve agility and competitiveness in a fast-evolving market.

• Acceleration of Cloud-Native Deployments: Cloud-native infrastructure is gaining traction in the Digital Insurance Platform Market as insurers prioritize flexibility and scalability. By 2025, over 65% of global insurers are expected to operate core functions such as claims management and policy administration on cloud-based platforms. This transition reduces operational costs, enables seamless integration with partner ecosystems, and enhances real-time analytics capabilities. Hybrid cloud adoption is also rising, providing insurers with greater control over sensitive data while maintaining the agility of digital transformation.

• Growth of Embedded Insurance Partnerships: Embedded insurance is reshaping product distribution models within the Digital Insurance Platform Market. In 2024, embedded solutions accounted for a significant portion of digital policies across sectors like mobility, e-commerce, and fintech. Strategic alliances with retail and payment providers are enabling insurers to reach millions of new customers seamlessly at the point of purchase. This approach not only expands customer bases but also drives higher engagement and loyalty by offering tailored coverage directly within consumer journeys.

• Adoption of Generative AI in Operations: Generative AI tools are revolutionizing underwriting, claims processing, and customer engagement in the Digital Insurance Platform Market. By 2025, more than 70% of global insurers are piloting or scaling AI-driven automation that reduces claims processing times by up to 60%. AI-powered virtual assistants are managing policyholder queries efficiently, freeing human resources for complex tasks. This trend is enabling insurers to reduce error rates, streamline policy issuance, and deliver hyper-personalized products at scale.

• Increased Focus on Cybersecurity Enhancements: With rising volumes of sensitive customer data being processed, cybersecurity is a critical trend shaping the Digital Insurance Platform Market. Insurers are investing heavily in advanced encryption, zero-trust architectures, and AI-driven fraud detection systems. In 2024, cyber resilience programs expanded significantly across North America and Europe, driven by regulatory compliance and heightened threat landscapes. Strengthening digital defenses is not only safeguarding insurers against cyber risks but also reinforcing consumer confidence in digital-first insurance ecosystems.

The Digital Insurance Platform Market is segmented by type, application, and end-user, each contributing distinct value drivers to overall industry growth. Types of offerings are broadly divided into platforms and services, with platforms maintaining a dominant position due to their widespread adoption across insurers seeking core system modernization. Services, however, are registering accelerated growth as insurers increasingly demand consulting, integration, and support functions. Applications such as claims management and policy administration form the backbone of adoption, while emerging areas like customer engagement platforms and risk assessment tools are experiencing rapid uptake. End-user segmentation highlights large enterprises as the dominant adopters, leveraging scale and resources to integrate digital insurance systems, while small and medium enterprises (SMEs) represent the fastest-growing group, driven by affordability of cloud solutions and rising demand for agility in digital operations.

In the Digital Insurance Platform Market, platforms hold the leading share as they serve as the backbone for underwriting, claims, and policy management. Their dominance stems from the growing replacement of outdated legacy systems with flexible, scalable, and AI-enabled solutions. Cloud-native platforms are in particularly high demand, enabling insurers to deliver faster processing and improve customer interactions. Services are emerging as the fastest-growing type, fueled by rising needs for consulting, integration, and technical support to ensure smooth adoption of digital ecosystems. Many insurers are turning to managed services to reduce the burden of maintaining complex IT infrastructure. Other types, such as standalone digital modules for niche applications like fraud detection or automated compliance management, play a specialized role by addressing insurer-specific challenges. Collectively, the balance of robust platforms and supporting services creates a comprehensive ecosystem, ensuring efficiency, scalability, and customer-centricity within the market.

Claims management is the leading application segment in the Digital Insurance Platform Market, as insurers increasingly adopt digital tools to improve accuracy, reduce processing times, and elevate customer experience. Automated workflows and AI-driven analytics allow insurers to settle claims within days instead of weeks, creating measurable operational gains. Policy administration, however, is emerging as the fastest-growing application, supported by advancements in cloud computing and generative AI that streamline policy issuance, renewals, and compliance reporting. Customer engagement platforms also play a vital role, with insurers deploying chatbots, personalized dashboards, and predictive analytics to retain clients and boost satisfaction. Additionally, risk assessment and fraud detection applications are gaining relevance, especially in regions with high exposure to fraud-related losses. These collective applications are redefining how insurers operate, enhancing efficiency across value chains while ensuring agility in meeting regulatory and customer demands.

Large enterprises dominate the Digital Insurance Platform Market, leveraging their financial strength and global networks to implement large-scale digital ecosystems. Their focus on end-to-end transformation—spanning claims, underwriting, and customer service—makes them primary drivers of platform demand. Small and medium enterprises (SMEs), however, represent the fastest-growing end-user segment. Their rapid adoption is fueled by cost-effective cloud-based solutions and modular platforms that lower entry barriers, enabling SMEs to compete with established players through improved agility and customer-centric innovation. Public sector insurers and government-backed institutions are also contributing by modernizing systems to enhance transparency and meet regulatory mandates. Niche players, including insurtech startups, are expanding adoption with specialized tools that offer targeted solutions such as microinsurance and on-demand coverage. This evolving end-user mix reflects a market where both scale and adaptability play pivotal roles in shaping adoption strategies and future growth trajectories.

North America accounted for the largest market share at 39% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

Regional dynamics are shaped by technological maturity, regulatory reforms, and insurance penetration across diverse economies. While North America leads with strong digital infrastructure and early adoption of AI-based platforms, Asia-Pacific’s rapid growth is propelled by expanding middle-class populations, fintech integration, and government-backed digitization initiatives. Europe continues to focus on sustainability-driven insurance models, while South America and the Middle East & Africa are increasingly adopting platforms aligned with evolving customer needs and regulatory modernization.

Advanced Insurtech Adoption Driving Market Expansion

The North American Digital Insurance Platform Market held 39% of the global share in 2024, with adoption driven by industries such as healthcare, automotive, and financial services. The U.S. remains the largest contributor, supported by a highly digitized insurance ecosystem and strong investment in AI-enabled claims automation. Regulatory updates, including stricter data protection measures, have accelerated the shift toward cloud-based platforms that prioritize compliance and security. Digital transformation initiatives are widely adopted across insurers, with technologies such as predictive analytics, robotic process automation, and generative AI reshaping customer service and underwriting practices. These advancements are ensuring the region maintains its leadership position in the global market.

Regulatory Innovation Shaping the Insurance Technology Landscape

The European Digital Insurance Platform Market represented 27% of the global share in 2024, with Germany, the UK, and France emerging as leading contributors. The region’s market dynamics are influenced by sustainability-focused regulations, such as Solvency II and ESG-related reporting, which are encouraging insurers to adopt more transparent and data-driven systems. Adoption of digital twins and blockchain solutions is growing, particularly in risk management and fraud detection. Government initiatives across multiple nations support digital innovation, while collaboration between insurtech startups and established insurers enhances platform capabilities. This focus on compliance, sustainability, and technology integration continues to strengthen the market’s competitive outlook.

Digital Ecosystem Expansion Fueling Market Growth

The Asia-Pacific Digital Insurance Platform Market ranked second in market volume in 2024, with China, India, and Japan being the top consuming countries. Rising adoption of mobile-first insurance platforms and embedded insurance within e-commerce and payment systems is fueling regional demand. Infrastructure advancements, including 5G connectivity and cloud expansion, are enabling scalable deployment of digital platforms. Innovation hubs in China and India are driving insurtech solutions that integrate AI, blockchain, and IoT for hyper-personalized coverage. Japan’s insurance market, supported by a highly connected digital economy, is also accelerating modernization. This regional momentum positions Asia-Pacific as the fastest-growing market globally.

Government Incentives Supporting Digital Insurance Transformation

The South American Digital Insurance Platform Market is led by Brazil and Argentina, accounting for a significant portion of the regional share in 2024. Demand is rising from industries such as energy, agriculture, and transportation, where risk management is critical. Infrastructure expansion projects, coupled with the digitization of financial services, are fueling adoption of modern insurance platforms. Government incentives supporting fintech growth, particularly in Brazil, have accelerated insurtech innovation and the use of mobile-first insurance solutions. Trade policies and regional regulatory shifts are encouraging insurers to adopt platforms that enhance compliance and operational efficiency across diverse industries.

Technological Modernization Reshaping Insurance Practices

The Middle East & Africa Digital Insurance Platform Market is experiencing growing demand, particularly from sectors such as oil and gas, construction, and healthcare. The UAE and South Africa are leading adoption, supported by rapid digital transformation and government initiatives to modernize insurance infrastructure. Technological upgrades such as AI-powered fraud detection and blockchain-enabled contract management are becoming integral to regional platforms. Local regulations promoting transparency and consumer protection are fostering stronger digital adoption. Trade partnerships and foreign investments are further accelerating innovation, positioning the region as an emerging market with significant long-term potential.

United States | 31% market share: Dominance driven by advanced AI adoption and high insurer investments in digital transformation.

China | 18% market share: Strength supported by large-scale fintech integration and rapid development of mobile-first insurance platforms.

The Digital Insurance Platform Market is characterized by a highly competitive landscape with more than 200 active players globally, ranging from established multinational insurers to agile insurtech startups. Leading competitors are focusing on strategic collaborations, acquisitions, and the launch of AI-driven platforms to enhance operational efficiency and customer engagement. Partnerships between insurers and technology providers are becoming increasingly common, particularly in areas such as embedded insurance, fraud detection, and cloud-native deployments. Innovation trends show a marked shift toward generative AI, blockchain-based smart contracts, and predictive analytics that improve underwriting accuracy and claims settlement. Competitors are also investing in cybersecurity upgrades to meet regulatory requirements and ensure consumer trust. The competition is further intensified by regional insurtech ecosystems in Asia-Pacific and North America, which are producing scalable solutions that challenge traditional market leaders. This dynamic competitive environment highlights a strong emphasis on technology integration, customer-centric product innovation, and strategic alliances aimed at gaining long-term market positioning.

IBM Corporation

Microsoft Corporation

Oracle Corporation

SAP SE

TCS (Tata Consultancy Services)

DXC Technology

Cognizant Technology Solutions

Guidewire Software Inc.

Majesco

Pegasystems Inc.

FINEOS Corporation

Duck Creek Technologies

Salesforce Inc.

The Digital Insurance Platform Market is undergoing rapid technological evolution, driven by the convergence of AI, cloud computing, blockchain, and IoT integration. Cloud-native solutions are dominating adoption, with over 65% of insurers migrating core functions such as underwriting and claims management to scalable, flexible infrastructures. Hybrid cloud models are increasingly popular, enabling data sovereignty and regulatory compliance while maintaining agility.

Artificial intelligence is playing a central role, with machine learning models improving fraud detection accuracy by up to 50% and predictive analytics enabling faster, more precise underwriting. Generative AI is also advancing customer experience by automating policy issuance and providing real-time, tailored product recommendations. Robotic process automation (RPA) has reduced claims processing times by as much as 60%, boosting both efficiency and customer satisfaction.

Blockchain is emerging as a critical enabler for secure, transparent transactions. Smart contracts are reducing manual intervention in policy management and settlement, while distributed ledger systems are strengthening fraud prevention. IoT-enabled platforms are providing insurers with real-time data streams from connected vehicles, smart homes, and health devices, empowering risk-based pricing and proactive engagement strategies. Collectively, these technologies are creating a dynamic ecosystem where digital insurance platforms deliver efficiency, personalization, and resilience to meet evolving industry demands.

• In February 2023, Guidewire Software announced the launch of its new Claims Autopilot module, enabling automated claims triage and processing. Early trials showed insurers reducing claim settlement times by 45%, improving operational efficiency and enhancing customer satisfaction.

• In July 2023, Majesco introduced a generative AI-powered underwriting assistant to support insurers in risk assessment. The tool integrates real-time data feeds and machine learning, allowing underwriters to evaluate policies 30% faster while maintaining compliance with regulatory frameworks.

• In March 2024, Zurich Insurance rolled out its AI-based customer relationship management platform across Europe, applying a “three-click” service rule. The system reduced service response times by over 70%, centralizing policy data and improving customer engagement significantly.

• In November 2024, Duck Creek Technologies unveiled a cloud-native distribution management solution tailored for embedded insurance. The solution enabled insurers to integrate with e-commerce platforms seamlessly, accelerating new policy distribution channels and expanding customer acquisition opportunities.

The scope of the Digital Insurance Platform Market Report encompasses a comprehensive analysis of the industry across types, applications, end-users, regions, and emerging technologies. It evaluates core offerings such as digital platforms and services, with emphasis on cloud-native infrastructure, hybrid deployment models, and modular solutions that insurers are increasingly adopting for scalability and compliance.

The report also highlights diverse applications, ranging from claims management and policy administration to fraud detection, customer engagement platforms, and risk analytics tools. These applications collectively illustrate how digital insurance systems are transforming operational workflows and customer experience across industries. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing how regional economic conditions, regulatory frameworks, and technological maturity influence adoption. For instance, North America leads with strong insurtech ecosystems, while Asia-Pacific shows the fastest expansion due to fintech integration and mobile-first platforms.

Technological insights include the growing use of AI, generative models, blockchain, IoT, and cybersecurity innovations shaping the market landscape. The report further addresses industry-specific focus areas such as embedded insurance, sustainability-driven solutions, and SME adoption patterns. By covering both dominant and niche segments, the report provides decision-makers with a structured overview of opportunities, challenges, and future growth trajectories in the Digital Insurance Platform Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 91856.38 Million |

|

Market Revenue in 2032 |

USD 167517.2 Million |

|

CAGR (2025 - 2032) |

7.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM Corporation, Microsoft Corporation, Oracle Corporation, SAP SE, TCS (Tata Consultancy Services), DXC Technology, Cognizant Technology Solutions, Guidewire Software Inc., Majesco, Pegasystems Inc., FINEOS Corporation, Duck Creek Technologies, Salesforce Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |