Reports

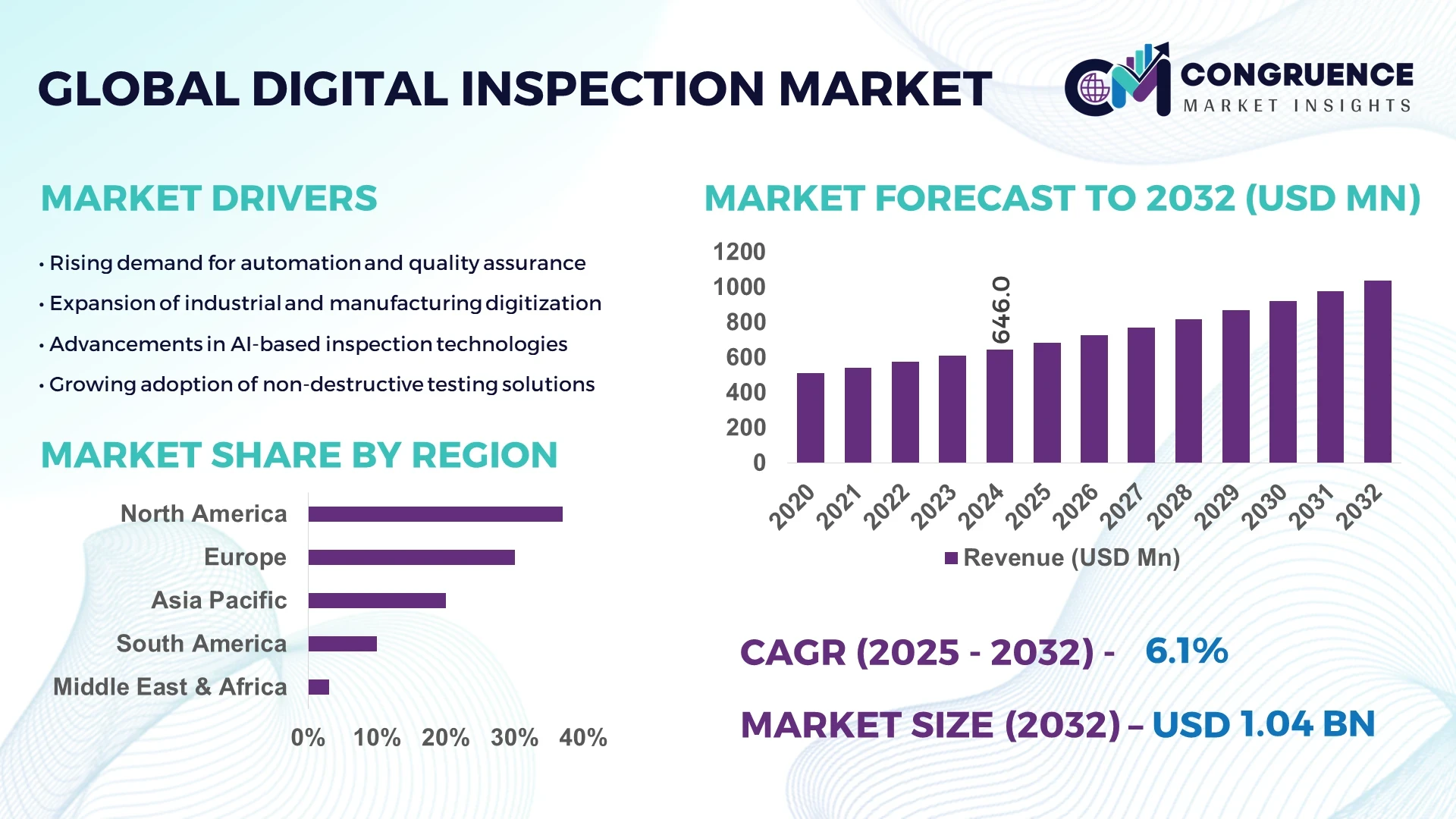

The Global Digital Inspection Market was valued at USD 646 Million in 2024 and is anticipated to reach a value of USD 1,037.42 Million by 2032, expanding at a CAGR of 6.1% between 2025 and 2032. This growth is primarily driven by the increasing adoption of automation and the need for enhanced quality control across various industries.

The United States stands as a significant player in the digital inspection market, with substantial investments in advanced manufacturing technologies. In 2023, approximately 34.8% of global digital inspection deployments were located in North America, driven by the U.S.'s advanced manufacturing base. The automotive sector leads adoption, with nearly 42% of U.S. automotive manufacturers utilizing inline digital inspection systems. Additionally, about 29% of U.S. electronics producers have adopted non-contact digital inspection equipment, highlighting the country's commitment to technological advancement in quality assurance processes.

Market Size & Growth: Valued at USD 646 Million in 2024, projected to reach USD 1,037.42 Million by 2032, expanding at a CAGR of 6.1% due to increased automation and quality control demands.

Top Growth Drivers: Automation adoption (42%), quality assurance enhancement (29%), and regulatory compliance (18%).

Short-Term Forecast: By 2028, a 15% reduction in inspection-related downtime is anticipated through advanced digital inspection technologies.

Emerging Technologies: Integration of AI-driven analytics, adoption of drone-based inspection systems, and utilization of 3D imaging technologies.

Regional Leaders: North America (USD 450 Million by 2032), Europe (USD 350 Million by 2032), and Asia-Pacific (USD 250 Million by 2032), each exhibiting unique adoption trends in manufacturing and infrastructure sectors.

Consumer/End-User Trends: Increased adoption among automotive and electronics manufacturers, with a shift towards automated and non-contact inspection methods.

Pilot or Case Example: A 2024 pilot project in the automotive sector led to a 20% improvement in production line efficiency through the implementation of inline digital inspection systems.

Competitive Landscape: Market leader holding approximately 25% share, followed by Cognex Corporation, Hexagon, Nikon Corporation, and OMRON Corporation.

Regulatory & ESG Impact: Implementation of stricter quality control regulations and environmental standards driving the adoption of digital inspection technologies.

Investment & Funding Patterns: Over USD 500 Million invested in digital inspection technologies in 2024, with a focus on AI integration and automation solutions.

Innovation & Future Outlook: Development of real-time analytics platforms and predictive maintenance tools to enhance inspection processes and reduce operational costs.

The digital inspection market encompasses various technologies and applications aimed at enhancing the efficiency and accuracy of inspection processes across multiple industries. Key sectors driving market growth include manufacturing, automotive, aerospace, and electronics, where the demand for precision and quality assurance is paramount. Recent technological advancements, such as the integration of artificial intelligence and machine learning algorithms, have enabled real-time data analysis and predictive maintenance, further propelling market expansion. Additionally, the increasing emphasis on regulatory compliance and environmental sustainability has led to the adoption of digital inspection solutions that minimize waste and reduce human error. Regional consumption patterns indicate a significant uptake in North America and Europe, attributed to the presence of established industrial bases and stringent quality standards. Emerging trends, including the use of drones for remote inspections and the development of 3D imaging technologies, are expected to shape the future landscape of the digital inspection market, offering enhanced capabilities and broader applications across various sectors.

The Digital Inspection Market is strategically vital for industries aiming to enhance operational efficiency, ensure compliance, and foster sustainable growth. By integrating advanced technologies like AI, machine learning, and digital twins, companies can achieve significant improvements in quality control processes. For instance, implementing AI-powered predictive maintenance systems can reduce downtime by up to 30% compared to traditional methods. Regionally, North America leads in volume, while Asia-Pacific dominates in adoption, with approximately 40% of enterprises in the region utilizing digital inspection technologies. In the short term, by 2027, the adoption of AI-driven inspection systems is expected to improve defect detection accuracy by 25%. From an ESG perspective, firms are committing to sustainability goals such as a 20% reduction in carbon emissions through the adoption of energy-efficient digital inspection systems by 2030. A notable example is a 2024 initiative in Germany, where a manufacturing company achieved a 15% reduction in waste through the implementation of digital inspection technologies. Looking forward, the Digital Inspection Market is poised to be a cornerstone of resilience, compliance, and sustainable growth, driving innovation and efficiency across various industries.

The surge in industrial automation is a primary driver of the Digital Inspection Market. As manufacturing processes become more automated, the need for precise and efficient inspection systems grows. Automated digital inspection technologies, such as machine vision and non-destructive testing, enable manufacturers to detect defects in real-time, reducing the reliance on manual inspections and minimizing human error. This shift not only enhances product quality but also improves throughput and operational efficiency. Industries like automotive and electronics are particularly benefiting from these advancements, leading to increased adoption of digital inspection solutions.

Despite the advantages, several challenges impede the widespread adoption of Digital Inspection technologies. High initial investment costs for advanced equipment and integration complexities with existing systems are significant barriers, especially for small and medium-sized enterprises. Additionally, the need for specialized skills to operate and maintain these systems can limit their implementation. Compatibility issues with legacy equipment and the potential disruption to established workflows further complicate the adoption process. Addressing these challenges is crucial for accelerating the integration of digital inspection solutions across various industries.

The Digital Inspection Market presents numerous untapped opportunities, particularly in emerging industries and regions. The growing emphasis on quality control in sectors like food and pharmaceuticals is driving demand for advanced inspection systems. Additionally, the expansion of manufacturing activities in developing economies offers a fertile ground for the adoption of digital inspection technologies. The integration of artificial intelligence and machine learning into inspection systems also opens new avenues for predictive maintenance and defect detection. Leveraging these opportunities can lead to significant advancements in product quality and operational efficiency.

Regulatory complexities pose a significant challenge to the Digital Inspection Market. Industries such as aerospace, automotive, and healthcare are subject to stringent quality standards and compliance requirements. Navigating these regulations can be cumbersome, and failure to comply can result in costly penalties and damage to brand reputation. Digital inspection technologies must be adaptable to meet varying regulatory standards across different regions and sectors. Ensuring that inspection systems are compliant with these regulations is essential for their successful implementation and widespread adoption.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Digital Inspection market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Surge in AI-Driven Inspection Systems: Artificial Intelligence is revolutionizing digital inspection processes. AI-powered systems are now capable of detecting defects with up to 98% accuracy, significantly outperforming traditional methods. Industries such as automotive and electronics are increasingly adopting AI-based inspection technologies to enhance product quality and reduce human error, leading to more efficient manufacturing processes.

Expansion of Drone-Based Inspection Applications: The use of drones for inspection purposes is rapidly growing. Drones equipped with high-resolution cameras and sensors are being utilized for inspecting infrastructure, power lines, and other critical assets. This method not only reduces inspection time but also enhances safety by minimizing human involvement in hazardous environments.

Advancements in 3D Imaging Technologies: 3D imaging technologies are transforming digital inspection by providing detailed and accurate representations of objects and structures. These technologies enable inspectors to analyze components from multiple angles, improving the detection of defects and anomalies. Industries such as aerospace and manufacturing are leveraging 3D imaging to ensure the highest standards of quality control.

The Digital Inspection Market is segmented into various categories, including technology, offering, dimension, and end-user industries, each contributing uniquely to the market's expansion. Technologically, the market encompasses machine vision, metrology, and non-destructive testing (NDT), each serving distinct inspection needs. Offerings are divided into hardware, software, and services, with hardware leading due to the demand for advanced inspection tools. Dimensions are categorized into 2D and 3D, with 3D gaining prominence for its precision in complex inspections. End-user industries span electronics and semiconductor, manufacturing, oil & gas, aerospace & defense, automotive, energy and power, public infrastructure, and food and pharmaceuticals, reflecting the widespread applicability of digital inspection technologies.

The Digital Inspection Market is primarily divided into machine vision, metrology, and non-destructive testing (NDT). Machine vision holds the largest share, driven by its widespread use in automated inspection systems across various industries. Metrology is the fastest-growing segment, with advancements in precision measurement technologies fueling its adoption, particularly in sectors requiring high accuracy. NDT remains crucial for industries like aerospace and oil & gas, where structural integrity is paramount. Together, these segments cater to the diverse inspection needs of modern industries.

Digital inspection finds applications across various sectors, including manufacturing, electronics and semiconductor, oil & gas, aerospace & defense, automotive, energy and power, public infrastructure, and food and pharmaceuticals. Manufacturing leads in adoption due to the industry's emphasis on quality control and efficiency. The aerospace & defense sector is witnessing rapid growth in digital inspection adoption, driven by the need for stringent quality standards and compliance with regulatory requirements. Emerging applications in food and pharmaceuticals highlight the expanding role of digital inspection in ensuring product safety and compliance with health regulations.

The leading end-user segment in the Digital Inspection Market is manufacturing, accounting for a significant share due to the industry's focus on automation and quality assurance. The automotive sector is the fastest-growing end-user, with a projected annual growth rate of 8%, driven by the industry's push towards smart manufacturing and the integration of Industry 4.0 technologies. Other notable end-users include aerospace & defense, electronics and semiconductor, and oil & gas, each contributing to the market's diversification and resilience.

North America accounted for the largest market share at 37% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.0% between 2025 and 2032.

In 2024, North America led the global digital inspection market with an estimated value of USD 7.5 billion, driven by advanced manufacturing sectors and early adoption of Industry 4.0 technologies. Asia-Pacific's market volume stood at USD 4.5 billion, with China and India emerging as significant contributors due to rapid industrialization and a growing emphasis on quality control. Europe's market size was approximately USD 6.0 billion, with Germany, the UK, and France leading in aerospace, automotive, and manufacturing sectors. South America's market share was modest, with Brazil and Argentina showing increasing adoption in infrastructure and energy sectors. The Middle East & Africa region exhibited varied demand trends, with countries like the UAE and South Africa focusing on oil & gas and construction industries.

How is the digital inspection market evolving in North America?

North America maintained a dominant position in the digital inspection market in 2024, accounting for approximately 37% of the global market share. The region's growth is propelled by key industries such as aerospace, automotive, and electronics, which prioritize precision and quality control. Regulatory frameworks, including stringent safety and quality standards, have further accelerated the adoption of digital inspection technologies. Technological advancements, particularly in machine vision and non-destructive testing (NDT), have enhanced inspection accuracy and efficiency. Local players like Cognex Corporation have been instrumental in driving innovation, offering advanced vision systems tailored for various industrial applications. Consumer behavior in North America reflects a higher enterprise adoption rate in sectors like healthcare and finance, where compliance and risk mitigation are paramount.

What factors are influencing the digital inspection market in Europe?

Europe's digital inspection market was valued at approximately USD 6.0 billion in 2024. Countries such as Germany, the UK, and France are at the forefront, with strong industrial bases in automotive, aerospace, and manufacturing sectors. Regulatory bodies like the European Union have implemented directives that mandate high standards for product quality and safety, driving the demand for advanced inspection solutions. The adoption of emerging technologies, including artificial intelligence and robotics, is enhancing the capabilities of digital inspection systems. Companies like Zeiss Group are leading the way by integrating AI into their inspection processes, improving defect detection and reducing human error. Consumer behavior in Europe shows a trend towards regulatory compliance, with industries seeking explainable and transparent inspection processes to meet stringent standards.

What are the key developments in the digital inspection market in Asia-Pacific?

Asia-Pacific's digital inspection market was valued at approximately USD 4.5 billion in 2024, with China and India emerging as significant contributors. The region's rapid industrialization, particularly in manufacturing and electronics, is fueling the demand for advanced inspection technologies. Infrastructure development and urbanization are also driving the adoption of digital inspection solutions in construction and public infrastructure projects. Technological trends such as the integration of Internet of Things (IoT) and artificial intelligence are enhancing the efficiency and accuracy of inspection processes. Local players like Omron Corporation are expanding their presence by offering tailored solutions for various industries, including automotive and electronics. Consumer behavior in Asia-Pacific reflects a growing inclination towards mobile AI applications and e-commerce platforms, influencing the demand for digital inspection technologies in these sectors.

What are the dynamics shaping the digital inspection market in South America?

South America's digital inspection market is gradually expanding, with Brazil and Argentina leading the way. The region's market share remains modest, but increasing investments in infrastructure and energy sectors are driving the adoption of digital inspection technologies. Government incentives and trade policies aimed at modernizing industries are further contributing to market growth. Technological advancements, though at an early stage, are beginning to influence sectors such as manufacturing and construction. Local players are exploring opportunities to introduce cost-effective and scalable inspection solutions tailored to regional needs. Consumer behavior in South America indicates a demand for media and language localization, influencing the customization of digital inspection technologies to cater to diverse linguistic and cultural contexts.

How is the digital inspection market evolving in the Middle East & Africa?

The Middle East & Africa region exhibits varied demand trends in the digital inspection market, with countries like the UAE and South Africa focusing on sectors such as oil & gas and construction. Technological modernization trends are evident, with increasing investments in automation and quality control measures. Local regulations and trade partnerships are shaping the adoption of digital inspection technologies, with an emphasis on safety and compliance standards. Companies operating in the region are leveraging digital inspection solutions to enhance operational efficiency and reduce downtime. Consumer behavior in the Middle East & Africa reflects a growing awareness of the benefits of digital inspection, leading to increased adoption across various industries.

United States: Approximately 35% market share; driven by advanced manufacturing and stringent quality standards.

Germany: Approximately 12% market share; strong presence in automotive and industrial sectors.

The Digital Inspection market is characterized by a fragmented competitive landscape, with over 50 active global players. The top five companies collectively hold approximately 30% of the market share, highlighting a diverse and competitive environment. Strategic initiatives such as mergers, acquisitions, and partnerships are common, as companies aim to enhance technological capabilities and expand market reach. For example, Wabtec Corp's acquisition of Evident's Inspection Technologies division for $1.78 billion demonstrates consolidation efforts to enter high-growth sectors like rail, mining, and manufacturing.

Innovation serves as a key differentiator, with companies investing heavily in research and development to integrate AI, machine learning, and IoT into inspection solutions. These advancements enable more efficient, accurate, and scalable inspection processes. Product launches and service expansions are also shaping market dynamics, catering to evolving demands in industries such as automotive, aerospace, and energy.

Regulatory compliance and regional standards further influence competition. Companies capable of navigating complex regulations while offering innovative, cost-effective solutions are positioned to capture greater market share. Overall, the Digital Inspection market remains highly competitive, driven by technological innovation, strategic collaborations, and responsiveness to industry-specific requirements.

Nikon Corporation

Olympus Corporation

MISTRAS Group

Faro Technologies

Basler AG

Omron Corporation

Keyence Corporation

The Digital Inspection Market is increasingly driven by cutting-edge technologies that enhance accuracy, efficiency, and scalability across industrial applications. Machine vision systems remain the cornerstone, accounting for nearly 42% of adoption in automated inspection processes. These systems utilize high-resolution cameras and advanced image processing algorithms to detect defects and deviations in real-time, enabling manufacturers to maintain stringent quality standards. Non-destructive testing (NDT) technologies, including ultrasonic, X-ray, and eddy current methods, contribute approximately 28% of market implementation, particularly in aerospace, automotive, and energy sectors where structural integrity is critical.

Emerging technologies such as artificial intelligence (AI) and machine learning are reshaping inspection capabilities. AI-enabled platforms can analyze complex datasets from multiple inspection points, identifying anomalies with up to 98% accuracy compared to traditional manual methods. Predictive analytics powered by AI is improving maintenance schedules, reducing downtime, and optimizing production line performance. Additionally, 3D imaging and laser scanning technologies are expanding rapidly, offering volumetric inspection and dimensional verification for intricate components, representing around 18% of new technology deployments.

Integration of Internet of Things (IoT) sensors allows for real-time monitoring of equipment and materials, facilitating predictive maintenance and quality assurance. Cloud-based inspection platforms enable centralized data management and remote access, enhancing operational visibility and decision-making across geographically distributed production facilities. Recent advancements also include drone-based inspection systems, increasingly used for infrastructure and energy applications, reducing inspection times by over 25% and minimizing safety risks. These technologies collectively position the Digital Inspection Market at the forefront of industrial innovation, enabling precision, compliance, and operational excellence.

Cognex Corporation introduced the 380 Modular Vision Tunnel in March 2024, enhancing high-throughput barcode reading capabilities for logistics and manufacturing sectors. The system integrates the DataMan® 380 barcode reader, offering improved data capture and processing efficiency.

Hexagon AB acquired 3D Systems' Geomagic software suite in December 2024 for $123 million. This acquisition strengthens Hexagon's position in 3D modeling and inspection, enabling the creation of high-quality 3D models from multiple sources, including laser scanning.

General Electric Aerospace partnered with Waygate Technologies in October 2024 to develop an AI-assisted commercial jet engine borescope inspection solution. This collaboration aims to enhance defect recognition capabilities, improving maintenance efficiency and safety in the aerospace sector.

Nikon Corporation launched Scatter Correction CT software in September 2024, addressing X-ray scatter artifacts in industrial CT scanning. This advancement enhances image quality and measurement accuracy, benefiting industries requiring precise internal inspections.

The Digital Inspection Market Report offers a comprehensive analysis of the industry's current landscape and future projections. It encompasses various segments, including hardware, software, and services, with a focus on technologies such as machine vision, non-destructive testing (NDT), and metrology. The report delves into applications across multiple sectors, including manufacturing, automotive, aerospace, energy, and public infrastructure. Geographically, the report provides insights into regional markets, highlighting North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It examines market dynamics within each region, considering factors like technological adoption rates, regulatory environments, and industry-specific demands.

The report also addresses emerging trends and innovations shaping the market, such as the integration of artificial intelligence, Internet of Things (IoT) connectivity, and cloud-based inspection solutions. It explores the impact of these technologies on inspection accuracy, efficiency, and scalability. Additionally, the report identifies key drivers and challenges influencing market growth, including the increasing demand for quality control, the need for compliance with stringent regulations, and the high costs associated with implementing advanced inspection systems. It provides strategic recommendations for stakeholders to navigate these dynamics and capitalize on opportunities within the evolving digital inspection landscape.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 646 Million |

Market Revenue in 2032 | USD 1037.42 Million |

CAGR (2025 - 2032) | 6.1% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Cognex Corporation, Hexagon AB, General Electric, Nikon Corporation, Olympus Corporation, MISTRAS Group, Faro Technologies, Basler AG, Omron Corporation, Keyence Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |