Reports

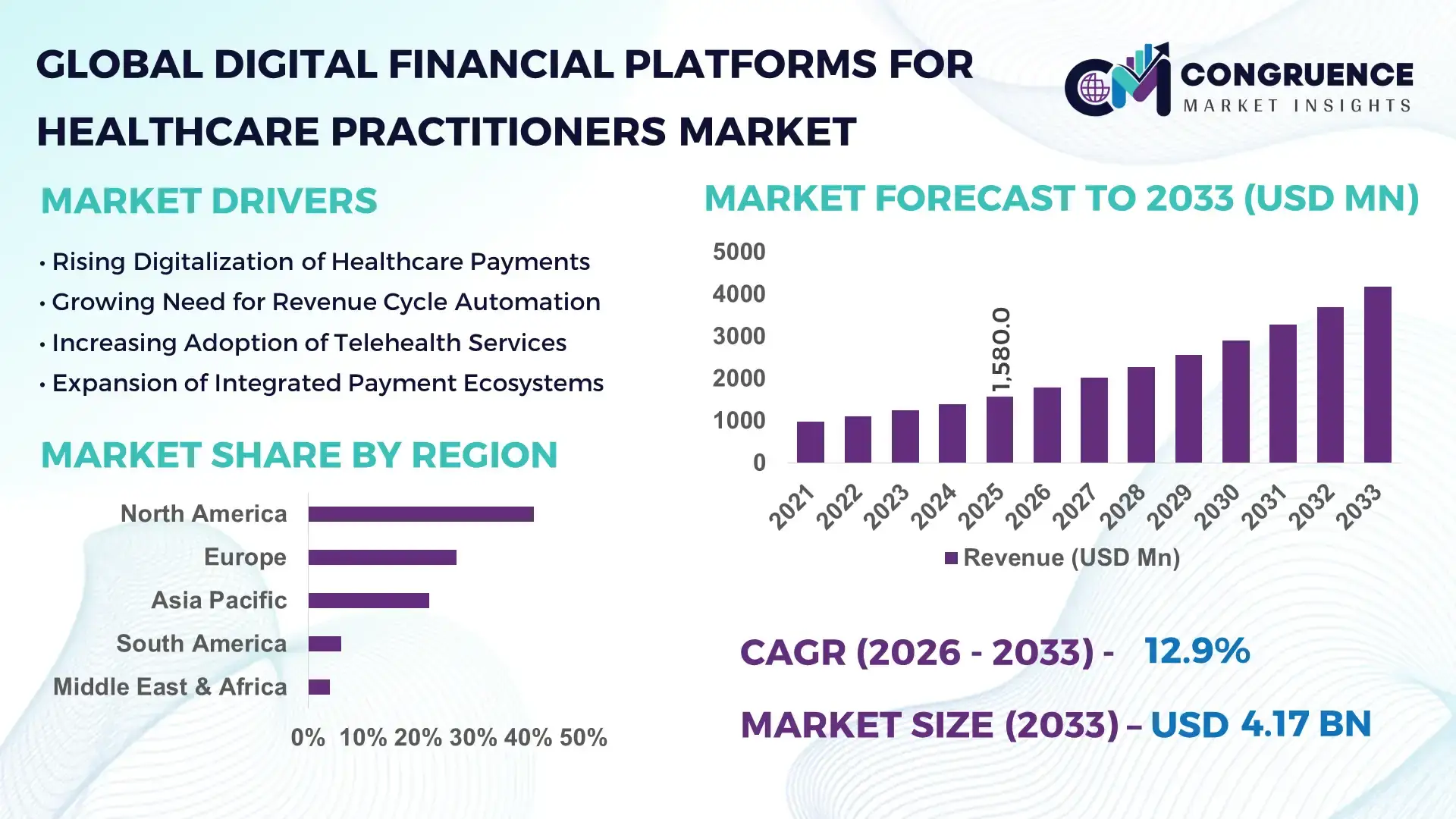

The Global Digital Financial Platforms for Healthcare Practitioners Market was valued at USD 1,580.0 Million in 2025 and is anticipated to reach USD 4,170.7 Million by 2033, expanding at a CAGR of 12.9% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is being propelled by the rapid digitization of provider revenue cycles and the shift toward real-time payments, automation, and interoperable financial data across healthcare ecosystems.

The United States hosts over 6,100 hospitals and ~1 million active physicians, of which more than 70% of large health systems now operate cloud-based revenue-cycle platforms supported by >12 GW of healthcare-grade data center capacity. Annual digital health investment has exceeded USD 15–20 billion in recent years, with dedicated fintech-for-healthcare programs in at least 28 states. National payers process over 90% of claims electronically, while major platforms increasingly embed AI-driven reconciliation engines, real-time payments, and API-enabled financial data exchange across thousands of clinics, pharmacies, and labs.

Market Size & Growth: USD 1.58 billion in 2025 to USD 4.17 billion by 2033; growth driven by automation of revenue cycles and real-time payment adoption.

Top Growth Drivers: 65% rise in cloud adoption; 40% reduction in manual billing errors; 35% faster claims processing.

Short-Term Forecast (2028): Average provider billing cycle expected to shrink by 28%.

Emerging Technologies: AI/ML claims validation, blockchain audit trails, and API-based open finance integrations.

Regional Leaders (2033): North America ~USD 1.6 billion (real-time payments); Europe ~USD 1.1 billion (compliance-first adoption); Asia-Pacific ~USD 900 million (cloud scaling).

End-User Trends: Hospitals prioritize automation; clinics favor plug-and-play SaaS; telehealth drives digital wallets.

Pilot Example (2024): A multi-hospital network cut claim denials by 32% using AI reconciliation.

Competitive Landscape: Market leader ~30% share; key players include Change Healthcare, Stripe Healthcare, Adyen, Square, and Flywire.

Regulatory & ESG Impact: Stronger data localization, carbon-aware cloud procurement, and green data centers.

Investment Patterns: Over USD 6 billion in recent funding toward embedded healthcare finance and interoperability tools.

Future Outlook: Deeper integration with EHRs, instant settlements, and predictive revenue analytics.

Hospitals and large health systems account for the majority of platform usage, while specialty clinics and telehealth providers are expanding fastest through cloud-native tools. AI-driven payment integrity, real-time settlement rails, and API-based interoperability are reshaping workflows. Tighter data-privacy rules, energy-efficient cloud migration, and rising labor costs are accelerating automation. North America leads in transaction intensity, Europe in compliance-driven adoption, and Asia-Pacific in mobile-first deployment, with embedded finance and instant payments defining the market’s next phase.

Digital financial platforms are becoming core infrastructure for modern healthcare delivery rather than back-office utilities. They connect clinical workflows with financial outcomes—linking scheduling, care delivery, claims processing, and settlement into a single interoperable loop. Strategically, this alignment reduces administrative friction, improves cash flow predictability for providers, and enhances transparency for payers and patients.

From a performance standpoint, AI-driven claims reconciliation delivers ~35% fewer denials compared to legacy rule-based systems, while automated eligibility checks can cut pre-authorization turnaround times by 20–25%. Integration with EHRs and national health exchanges is also enabling near-real-time financial visibility at the point of care, which is increasingly treated as a competitive differentiator for large health systems.

Regionally, North America leads in transaction volume, supported by deep payer-provider digital integration, while Europe leads in adoption intensity, with roughly 55–60% of mid-to-large healthcare enterprises using standardized digital finance platforms tied to national reimbursement schemes. Asia-Pacific is scaling fastest in cloud-based billing for private hospital chains and telehealth providers.

In the short term (by 2028), generative AI and automated agent systems are expected to reduce end-to-end revenue-cycle costs by 20–30%, particularly in coding, auditing, and payer disputes. Real-time payment rails and embedded wallets are likely to push same-day settlements from niche pilots to mainstream use.

On the ESG and compliance front, leading firms are committing to 30–40% reductions in on-premise energy use by 2030 by migrating workloads to energy-efficient cloud data centers and adopting carbon-aware computing. Data governance frameworks are also tightening, with mandatory encryption, audit trails, and interoperability standards becoming table stakes.

A practical micro-scenario illustrates the impact: in 2024, a U.S. integrated delivery network deployed AI-assisted payment integrity tools that cut avoidable write-offs by 28% and reduced audit-related downtime by 22% across 18 hospitals.

Looking ahead, the Digital Financial Platforms for Healthcare Practitioners Market is poised to become a pillar of resilient, compliant, and sustainable healthcare finance—anchoring real-time payments, data interoperability, and trust-driven digital ecosystems.

The Digital Financial Platforms for Healthcare Practitioners Market is being reshaped by the convergence of cloud computing, AI, and interoperable health data standards. Providers are moving away from fragmented billing systems toward unified platforms that integrate scheduling, clinical data, claims management, and payments. Payers are simultaneously demanding cleaner data, faster adjudication, and stronger fraud prevention, which is accelerating investment in analytics-driven platforms. Real-time payment rails, embedded finance tools, and digital wallets are altering cash-flow dynamics, reducing days-in-receivable and administrative overhead. Regulatory pressure around data privacy, interoperability (such as FHIR standards), and price transparency is forcing vendors to build more secure, compliant, and modular systems. At the same time, rising labor shortages in medical billing and coding are pushing automation adoption. Competition is intensifying as fintech firms enter healthcare, creating hybrid solutions that blend banking, payments, and clinical data into single workflows for practitioners.

Healthcare organizations face chronic staffing shortages in billing, coding, and claims management, with administrative labor costs accounting for nearly 15–25% of total hospital operating expenses in many systems. Digital financial platforms reduce dependence on manual workflows by embedding AI-driven coding, automated eligibility checks, and real-time claims validation. Large health systems report 25–40% reductions in manual touchpoints per claim after platform adoption, which directly lowers labor intensity and improves throughput. Automation also minimizes human error in medical coding—a leading cause of claim rejections—where error rates can exceed 10% in traditional processes. By integrating directly with EHRs and payer portals, platforms enable straight-through processing for routine claims, accelerating reimbursements and freeing clinical staff from administrative burdens. As providers scale telehealth and multi-site operations, automated financial orchestration becomes essential for maintaining profitability and service continuity.

Despite progress on standards like FHIR, many hospitals still operate on fragmented legacy systems that cannot seamlessly exchange financial and clinical data. Roughly 30–40% of mid-sized providers rely on partially integrated billing platforms, forcing manual reconciliation between EHRs, clearinghouses, and payer systems. This creates data silos that limit the full value of digital finance tools. Integration projects are costly and time-consuming, often requiring months of customization and specialist labor. Smaller clinics in particular struggle with migration costs, cybersecurity risks, and downtime during system transitions. Concerns over data breaches—healthcare remains one of the most targeted sectors—also make some organizations hesitant to shift sensitive financial workflows entirely to cloud platforms. These interoperability and security barriers slow adoption, especially among resource-constrained providers.

Embedded finance is unlocking new revenue streams and operational efficiencies for healthcare providers by integrating payments, lending, and insurance directly into clinical workflows. Point-of-care payment tools allow patients to settle bills instantly through digital wallets or installment plans, reducing bad debt rates that can reach 5–10% of total receivables in some systems. For practitioners, real-time settlements improve liquidity and reduce reliance on external credit lines. Platforms that connect providers with fintech lenders can offer working capital based on predictive cash-flow analytics rather than historical statements. Additionally, API-driven financial services enable automated vendor payments, payroll processing, and procurement financing, cutting transaction costs by 15–25%. As regulatory frameworks evolve to support open banking and real-time payments, embedded finance is likely to become a core growth vector for digital healthcare finance platforms.

Healthcare data breaches are among the most expensive globally, with average incident costs often exceeding USD 10 million per breach. As digital financial platforms handle both medical and payment data, providers must invest heavily in encryption, identity management, continuous monitoring, and third-party risk assessments. Compliance requirements such as HIPAA, HITECH, and emerging data localization laws add further operational complexity and legal exposure. Smaller providers frequently lack the dedicated IT and compliance teams needed to manage these obligations, making platform adoption more daunting. Moreover, cyber insurance premiums for healthcare organizations have risen sharply—sometimes 100–300% in recent years—increasing the total cost of digital transformation. These security and regulatory burdens can slow deployments, particularly in fragmented or resource-limited markets.

Rise in Modular and Prefabricated Construction for Digital Infrastructure: About 55% of recent healthcare IT build-outs report lower capital costs when using modular, prefabricated data center components for financial platforms. Off-site automated fabrication of server racks, cooling units, and cabling has cut deployment timelines by 20–30% and reduced on-site labor needs by roughly 25%. Adoption is strongest in Europe and North America, where hospitals are modernizing back-end infrastructure to support real-time payments and AI analytics.

AI-Powered Payment Integrity at Scale: Hospitals using AI-based payment integrity tools have achieved 25–35% reductions in improper payments and trimmed audit workloads by nearly 30%. Large health systems are now processing millions of claims per month through automated anomaly detection engines, significantly lowering rework and compliance risk.

Expansion of Real-Time Payment Rails: By 2025–2026, more than 60% of leading U.S. health systems began piloting instant settlement rails for provider-to-vendor and payer-to-provider payments, cutting settlement times from weeks to hours. Early adopters report 18–22% improvements in working capital efficiency.

Cloud-Native Revenue Platforms: Cloud migration of financial operations has accelerated, with approximately 70% of new deployments now cloud-first. Providers report 30–40% lower infrastructure costs and faster software update cycles, enabling continuous compliance with evolving reimbursement rules.

The Digital Financial Platforms for Healthcare Practitioners Market is structured around technology types, functional applications, and diverse end-users, reflecting the operational complexity of modern healthcare finance. By type, deployment models range from cloud-native systems to hybrid and on-premise architectures, with increasing emphasis on API-enabled and embedded finance platforms that integrate directly into clinical workflows. Application-wise, the market spans revenue cycle management, claims processing, payment orchestration, fraud analytics, and patient financial engagement tools, each addressing distinct pain points across the provider–payer continuum. Hospitals and large health systems remain the heaviest users due to high transaction volumes, while specialty clinics, diagnostics networks, pharmacies, and telehealth providers are rapidly digitizing to streamline billing and settlements. Regional variations in reimbursement policies, interoperability standards, and data privacy rules shape segmentation patterns, with more modular, interoperable solutions gaining preference in mature markets and cost-efficient SaaS models dominating adoption in emerging regions.

Cloud-based digital financial platforms currently lead the market with an estimated 48% share, driven by scalability, lower infrastructure overhead, and faster compliance updates compared with legacy systems. Hybrid platforms account for roughly 26% of adoption, appealing to large health systems that need to retain sensitive workloads on-premise while leveraging cloud analytics. Traditional on-premise solutions still represent about 16%, mainly in public hospitals and highly regulated environments. The remaining 10% is split across mobile-first tools and API/embedded finance platforms serving niche use cases such as point-of-care payments and real-time vendor settlements.

The fastest-expanding category is API-enabled embedded finance platforms, growing at approximately 22% per year, as providers increasingly demand seamless integration with EHRs, banks, and real-time payment rails. Their growth is fueled by rising use of instant settlements, programmable payments, and automated reconciliation across multi-site health networks.

Mobile-first platforms are gaining traction among small practices for lightweight billing, while specialized fraud-analytics modules are emerging as add-ons for large systems handling millions of claims annually.

• In 2025, a major U.S. hospital consortium deployed an API-based embedded finance layer across 32 hospitals, enabling real-time vendor payments and reducing manual treasury processing by 34%.

Revenue cycle management (RCM) is the leading application with about 44% share, as providers prioritize end-to-end automation from scheduling to final payment. Payment processing platforms hold roughly 24%, while claims management represents 18% of usage. Fraud, waste, and abuse analytics plus patient financial engagement tools together account for the remaining 14%.

The fastest-growing application is patient financial engagement, expanding at roughly 20% annually, supported by rising demand for digital bills, payment plans, and transparent cost estimates before care delivery.

Adoption trends show that in 2025 around 41% of hospitals were piloting real-time payment tools integrated with their billing systems, and 58% of patients reported preferring fully digital statements over paper invoices.

In practice, RCM platforms are increasingly bundled with AI-driven coding, automated eligibility checks, and predictive denials management, reducing administrative friction across provider networks. Payment orchestration tools are shifting from batch processing to instant settlements, while fraud analytics systems are using machine learning to flag suspicious billing patterns in near real time.

• In 2025, a large European public health network digitized billing across 120 hospitals, cutting duplicate payments by 27% and shortening reimbursement cycles by more than two weeks.

Hospitals and integrated health systems dominate with approximately 52% share, reflecting their high transaction volumes, complex payer mixes, and regulatory exposure. Specialty clinics account for about 21%, diagnostics laboratories roughly 11%, while pharmacies, telehealth providers, and solo practices together represent the remaining 16%.

The fastest-growing end-user segment is telehealth providers, expanding at about 23% per year, driven by virtual care models that require instant billing, digital wallets, and cross-border payment capabilities.

Among other users, large diagnostic chains are standardizing cloud billing across regional networks, and community pharmacies are adopting embedded payment tools to handle insurance co-pays in real time. Industry adoption rates are rising: in 2025, about 46% of U.S. hospitals were testing AI-enabled financial tools that link clinical records with billing data, while 62% of digitally mature clinics now offer instant pay or installment options at the point of care.

End-users are also prioritizing platforms that integrate with EHRs, comply with data privacy rules, and support analytics-driven decision-making across multi-site operations.

• In 2025, a global hospital group implemented AI-assisted payment integrity tools across 45 facilities, reducing avoidable write-offs by 28% and cutting audit-related downtime by 22%.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.8% between 2026 and 2033.

North America’s leadership is supported by high digital maturity, with over 72% of hospitals using integrated digital billing and payment platforms and more than 90% of insurance claims processed electronically. Europe follows with 27% share, driven by standardized reimbursement systems and regulatory compliance requirements across public healthcare networks. Asia-Pacific holds 22% share, underpinned by rapid healthcare digitization across China, India, and Southeast Asia, where mobile-first payment adoption exceeds 65% among private hospitals. South America represents 6% share, while Middle East & Africa account for 4%, supported by healthcare infrastructure investments and national digital health programs. Cross-region data shows cloud-based deployment penetration above 68% globally, API-based payment orchestration adoption at 45%, and real-time settlement usage nearing 38% among large healthcare providers worldwide.

The region held a 41% market share in 2025, reflecting deep integration of digital finance across hospitals, specialty clinics, and payer networks. Demand is driven primarily by hospitals, multi-state health systems, telehealth providers, and diagnostic chains handling high transaction volumes. Regulatory frameworks such as HIPAA, HITECH, and interoperability mandates have accelerated adoption of secure, compliant platforms. Technological trends include AI-based claims validation, real-time payment rails, and EHR-integrated billing engines, with over 60% of large providers using automation in revenue-cycle operations. Local players such as Change Healthcare and Square Healthcare Solutions are expanding embedded finance and instant settlement tools. Regional consumer behavior shows higher enterprise adoption, with more than 58% of patients preferring digital billing and payment portals over paper-based processes.

Europe accounted for 27% market share in 2025, led by Germany, the UK, and France. Public healthcare systems and centralized reimbursement models drive standardized digital financial workflows. Regulatory bodies emphasize data protection, transparency, and explainability, increasing demand for compliant and auditable platforms. Adoption of cloud-native billing systems exceeds 55% among Western European hospitals, while AI-supported fraud detection is used by nearly 40% of national health agencies. Regional players such as Adyen Healthcare focus on cross-border payment orchestration and compliance-ready financial APIs. Consumer behavior reflects regulation-driven trust, with healthcare providers prioritizing explainable and auditable digital finance solutions.

Asia-Pacific captured 22% market share in 2025, ranking as the third-largest region by volume. China, India, and Japan are the top consumers, supported by large patient populations and rapid expansion of private healthcare networks. Infrastructure trends include cloud-first deployments and mobile payment integration, with over 70% of private hospitals in urban centers accepting digital wallets. Innovation hubs in India, Singapore, and South Korea are advancing API-based billing and AI-enabled claims automation. Local platforms such as Practo and Ping An HealthTech are embedding finance into telemedicine ecosystems. Regional consumer behavior shows growth driven by mobile apps and digital-first healthcare services, with mobile payment usage exceeding 68%.

South America held 6% market share in 2025, with Brazil and Argentina as key markets. Growth is supported by healthcare system modernization and increased private sector participation. Digital billing infrastructure adoption stands at approximately 42% among urban hospitals, while cloud penetration continues to expand. Government incentives promoting electronic invoicing and digital payments are strengthening platform uptake. Local fintech-healthcare integrators in Brazil are enabling real-time settlements for private clinics. Consumer behavior reflects localized digital adoption, with rising demand for Portuguese and Spanish-language financial interfaces and mobile payment compatibility.

The region accounted for 4% market share in 2025, led by the UAE, Saudi Arabia, and South Africa. Demand is linked to healthcare infrastructure expansion and national digital health initiatives. Technological modernization includes cloud-hosted billing systems and centralized claims exchanges, with digital claims processing adoption nearing 48% in Gulf Cooperation Council countries. Regulatory alignment and public-private partnerships support cross-border healthcare payments. Regional platforms and hospital groups are deploying integrated financial modules within hospital information systems. Consumer behavior varies, with institution-led adoption dominating over individual practitioner use.

United States – 34% Market Share: Strong dominance driven by high healthcare IT spending, large provider networks, and advanced payment infrastructure.

Germany – 11% Market Share: Leadership supported by standardized reimbursement systems, strict compliance requirements, and widespread digital hospital adoption.

The competitive environment in the Digital Financial Platforms for Healthcare Practitioners Market is dynamic and moderately consolidated, with a diverse mix of established fintechs, healthcare payment specialists, and integrated health IT providers shaping the landscape. Over 300+ active competitors operate globally, ranging from legacy financial services firms to startup innovators focused on provider revenue cycle automation and digital payments infrastructure. The top 5 companies collectively account for approximately 30–35% of industry influence, reflecting significant fragmentation alongside peer consolidation. Major players include traditional payment processors extending into healthcare payments, agile SaaS specialists, and vertically integrated healthcare technology firms embedding finance into clinical workflows.

Innovation trends influencing competition include cloud-native payment hubs, AI-enhanced claims and payment reconciliation tools, real-time settlement rails, and interoperable APIs that connect financial data with electronic health records (EHRs) to reduce administrative friction. Strategic initiatives regularly observed include product launches that embed patient financial engagement tools, partnerships between payment technology and EHR vendors, targeted acquisitions to build full-stack revenue cycle offerings, and expansion into emerging markets with mobile-first solutions. For instance, large payment processors are integrating tokenization and digital wallet capabilities for patient billing, while specialist platforms are offering predictive analytics for provider cash flow optimization. The market’s competitive nature drives continuous product evolution, partnerships with healthcare systems and payers, and investment in cybersecurity and regulatory compliance features to address the sector’s complex requirements.

Zelis Healthcare LLC

InstaMed

Mastercard Incorporated

Visa Inc.

Fiserv, Inc.

Optum, Inc.

Allscripts Healthcare Solutions, Inc.

Rectangle Health

Waystar Health

PatientPay Inc.

AccessOne MedCard Inc.

ClearBalance Healthcare Inc.

PayZen Inc.

The Digital Financial Platforms for Healthcare Practitioners Market is being transformed by cutting-edge technologies that streamline financial operations, optimize payment flows, and enhance interoperability across healthcare ecosystems. Cloud computing remains foundational, enabling scalable, multi-tenant platforms that support real-time billing, automated claims workflows, and secure data exchange across providers, payers, and patients. Cloud deployments increasingly integrate APIs and microservices architectures, facilitating seamless connections between revenue cycle management systems, EHRs, practice management software, and third-party payment processors.

Artificial intelligence (AI) and machine learning (ML) are core enablers for next-generation financial workflows, powering automated eligibility verification, predictive denials management, anomaly detection for fraud or billing discrepancies, and intelligent reconciliation engines that reduce manual intervention. AI-driven insights are also helping providers forecast cash flows and optimize workforce resource allocation. Real-time payment rails and distributed ledger technologies are gaining traction to support instant settlements between health systems, payers, and vendors, minimizing days-in-accounts receivable and improving liquidity. Advanced tokenization and biometric authentication technologies are enhancing transaction security, reducing fraud risks, and protecting sensitive payer and patient data across digital channels.

Mobile and digital wallet integrations are bridging the gap between traditional healthcare billing and consumer payment expectations, allowing patients to make secure payments via smartphones, contactless methods, or in-app experiences tied to provider portals. This mobile-first approach is crucial in regions with high smartphone adoption and supports omnichannel payment experiences that meet patient preferences.

Interoperability technologies such as FHIR-based APIs are enabling richer financial data flows between disparate systems, linking clinical events with financial triggers to reduce errors and administrative overhead. Collectively, these emerging technologies are reshaping financial operations in healthcare—improving transparency, reducing administrative load, and enhancing the overall financial engagement experience for both providers and patients.

• In July 2025, Waystar Health announced the acquisition of Iodine Software for USD 1.25 billion, integrating AI-driven documentation and payment tracking capabilities into its revenue cycle platform, bolstering automation and claims accuracy for healthcare providers. Source: www.wsj.com

• In September 2025, Google and PayPal entered a strategic multi-year partnership to embed AI-powered payment processing and checkout solutions across platforms, aiming to enhance transaction security and user experience for enterprise financial services including healthcare payments. Source: www.reuters.com

• In May 2025, Getepay received final authorization from the Reserve Bank of India to operate as an online payment aggregator, expanding its digital payments reach and enabling secure, scalable payment acceptance for merchants and service providers across sectors, including healthcare. Source: www.timesofindia.indiatimes.com

• In October 2025, Zoho Payment Technologies expanded its fintech offerings with PoS devices, QR solutions, virtual accounts, and payout capabilities after securing a PAPG license, enhancing collections and disbursement workflows for businesses including healthcare practices. Source: www.timesofindia.indiatimes.com

The Digital Financial Platforms for Healthcare Practitioners Market Report provides a comprehensive evaluation of technological interfaces, deployment models, application domains, and geographic footprints shaping modern healthcare finance ecosystems. It covers platform types ranging from cloud-native financial engines to hybrid and API-centric solutions that unify billing, claims processing, payment orchestration, fraud detection, and patient engagement. The report also examines system features such as real-time payment rails, tokenization services, biometric authentication, predictive analytics, and EHR integration levels that influence provider operational efficiency.

Geographically, this report spans regional insights across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with data on adoption metrics, platform maturity, and regulatory drivers unique to each territory. It delves into application segments including revenue cycle management, claims automation, patient financial engagement, embedded finance, and interoperability frameworks that connect digital financial platforms with broader health IT infrastructure. End-user focus areas include hospitals, multi-specialty clinics, specialty care centers, pharmacy networks, telehealth providers, and ancillary care settings, highlighting adoption rates and platform customization trends.

The report evaluates key innovation vectors such as mobile wallet adoption in emerging economies, AI/ML-enabled reconciliation engines, blockchain for secure transactions, and open API ecosystems enabling new provider and fintech partnerships. It also considers operational challenges such as data privacy, compliance with healthcare regulations, integration complexity, and patient payment behavior patterns. Overall, the report is structured to inform strategic decisions by showcasing competitive dynamics, technology adoption curves, user needs, and future readiness frameworks adopted by market participants.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,580.0 Million |

| Market Revenue (2033) | USD 4,170.7 Million |

| CAGR (2026–2033) | 12.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | PayPal; Stripe; JPMorgan Chase; Zelis; InstaMed; Mastercard; Visa; Fiserv; Optum; Allscripts; Rectangle Health; Waystar; PatientPay; AccessOne; ClearBalance; PayZen |

| Customization & Pricing | Available on Request (10% Customization Free) |