Reports

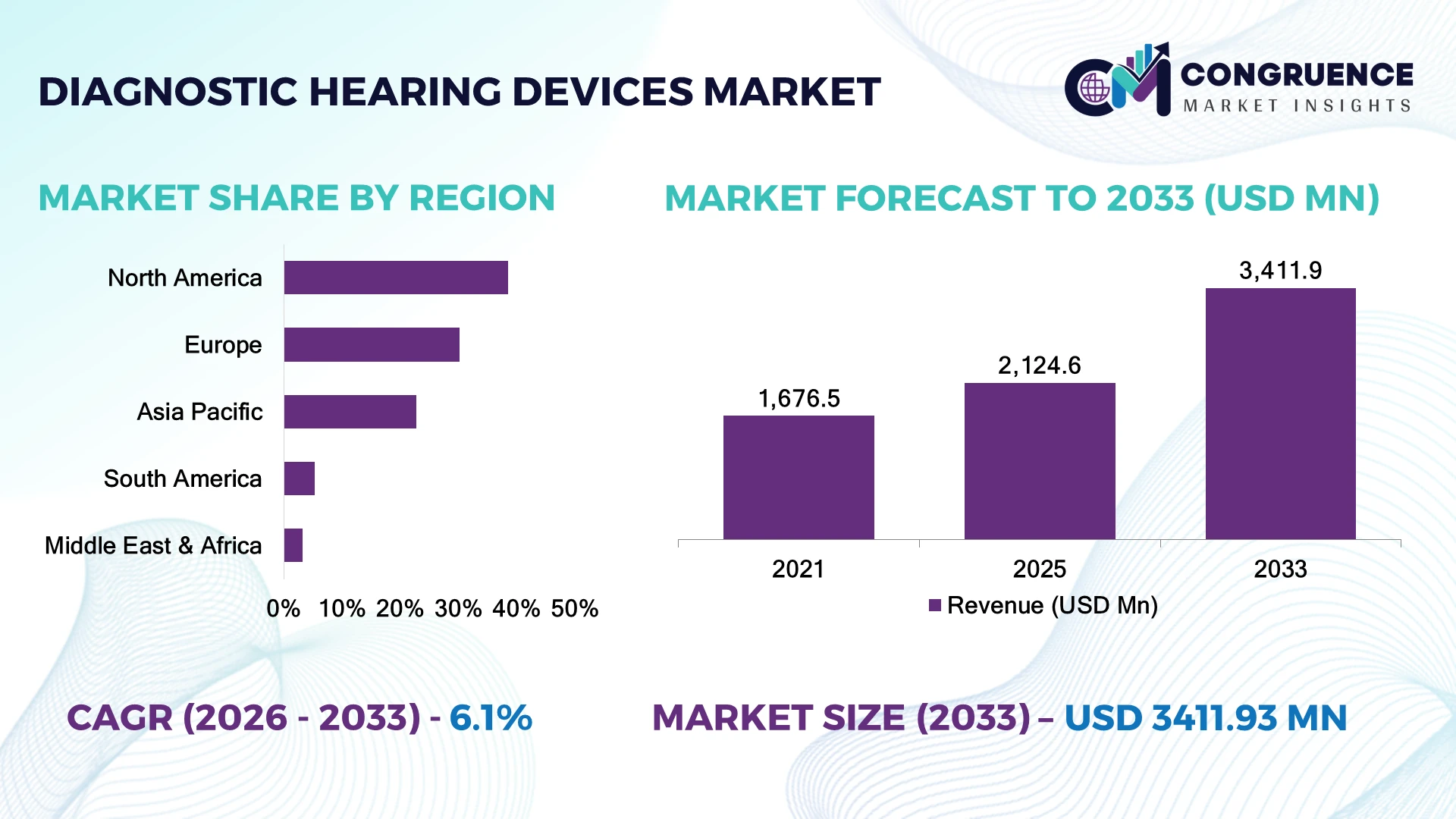

The Global Diagnostic Hearing Devices Market was valued at USD 2,124.6 Million in 2025 and is anticipated to reach a value of USD 3,411.9 Million by 2033 expanding at a CAGR of 6.1% between 2026 and 2033. Rising adoption of digital audiology platforms, AI-enabled hearing assessments, and early hearing loss screening programs is accelerating diagnostic hearing device deployment across healthcare systems.

The United States dominated the Diagnostic Hearing Devices Market with nearly 34% share in 2025, supported by advanced audiology infrastructure, high hearing screening adoption, and strong medical technology investments. More than 70% of audiology clinics in the U.S. use digital diagnostic systems, compared with nearly 52% adoption across major European healthcare facilities. Healthcare modernization initiatives following global medical supply-chain disruptions have increased investments in connected diagnostic technologies.

Healthcare providers adopting advanced hearing diagnostics are improving early detection capabilities, clinical efficiency, and patient-focused hearing care outcomes.

• Market Size & Growth: The market reached USD 2,124.6 Million in 2025 and is projected at USD 3,411.9 Million by 2033 with 6.1% CAGR, driven by digital audiology adoption.

• Top Growth Drivers: Hearing screening programs increased 35%, digital diagnostics adoption rose 31%, and elderly care demand expanded 28% globally.

• Short-Term Forecast: By 2028, AI-supported hearing diagnostics are expected to improve testing workflow efficiency by nearly 30%.

• Emerging Technologies: AI audiometry, tele-audiology platforms, and automated hearing assessment systems are transforming diagnostic practices.

• Regional Leaders: North America, Europe, and Asia-Pacific are projected to reach USD 1.3 Billion, USD 1.1 Billion, and USD 900 Million respectively through healthcare modernization.

• Consumer/End-User Trends: Hospitals and audiology centers represent over 65% adoption due to rising demand for accurate hearing evaluations.

• Pilot/Case Example: In 2025, automated audiology platforms improved patient screening turnaround time by nearly 25%.

• Competitive Landscape: Leading companies hold nearly 48% share, including Demant, Natus Medical, Inventis, and MAICO Diagnostics.

• Regulatory & ESG Impact: Digital healthcare initiatives improved diagnostic accessibility by approximately 30% across underserved populations.

• Investment & Funding: Over USD 1 Billion investments focus on hearing technologies, AI diagnostics, and healthcare device innovation.

• Innovation & Future Outlook: Next-generation diagnostic systems are shifting toward connected, automated, and patient-centric audiology solutions.

Diagnostic Hearing Devices are becoming essential in modern healthcare as rising hearing impairment cases increase the need for early detection and accurate assessment technologies. Digital audiometers, tympanometers, and otoacoustic emission systems are improving clinical efficiency by nearly 30%. Growing telehealth adoption and healthcare digitization are accelerating the transition toward connected diagnostic hearing platforms.

The Diagnostic Hearing Devices Market is becoming strategically important as healthcare systems prioritize early diagnosis, preventive care, and digital transformation in audiology services. Increasing aging populations, workplace hearing safety programs, and expanded newborn screening initiatives are shifting investments toward accurate and scalable diagnostic technologies. Medical providers are adopting connected platforms to improve testing accessibility and operational efficiency.

Compared with conventional manual testing methods, advanced digital diagnostic hearing systems improve assessment accuracy by nearly 25% and reduce testing time by approximately 30% through automation, AI-supported analysis, and integrated patient data management. North America leads adoption through advanced healthcare infrastructure, while Asia-Pacific is expanding through hospital modernization and wider screening accessibility.

Hospitals, audiology clinics, and hearing care providers are deploying automated audiometers, portable devices, and tele-audiology solutions to expand patient reach. Companies are strengthening product innovation, clinical partnerships, and digital health integration. Long-term competitiveness will depend on delivering accurate, connected, and accessible diagnostic solutions aligned with evolving hearing healthcare requirements.

Increasing prevalence of hearing impairment and expansion of preventive healthcare programs are accelerating diagnostic hearing device adoption globally. Nearly 55% of advanced hearing care facilities are integrating digital audiology systems, while automated platforms improve diagnostic workflow efficiency by approximately 30%. Growing newborn screening initiatives and occupational hearing safety programs in the United States and Japan are increasing demand for accurate testing equipment. Companies are responding through AI-enabled solutions, portable device development, and partnerships with healthcare providers to improve diagnostic accessibility and clinical performance.

Advanced diagnostic hearing technologies require specialized components, calibration systems, and trained professionals, creating adoption challenges across resource-limited healthcare environments. Digital audiology equipment costs can be 25–35% higher compared with basic testing systems, affecting smaller clinics and developing markets. Limited availability of audiology professionals also restricts large-scale deployment. Manufacturers are reducing barriers through compact device designs, remote testing capabilities, flexible pricing models, and localized distribution strategies to improve affordability and healthcare access.

Growing adoption of digital healthcare ecosystems is creating opportunities for AI-powered diagnostic hearing technologies and remote assessment solutions. Nearly 40% of future audiology platforms are expected to include automated testing, cloud connectivity, and intelligent interpretation capabilities. AI-based audiometry and mobile diagnostic solutions are enabling faster evaluations outside traditional clinical environments. Companies are investing in software platforms, connected devices, and healthcare partnerships to expand access across primary care, elderly care, and emerging healthcare networks.

Transition toward connected audiology systems creates challenges related to data integration, device interoperability, and clinical adoption consistency. Nearly 30% of healthcare providers face difficulties connecting diagnostic equipment with digital health records and existing infrastructure. Increasing reliance on cloud platforms requires stronger cybersecurity, data protection, and system compatibility. Companies must invest in secure software ecosystems, user training, and standardized integration frameworks to ensure reliable deployment and long-term competitiveness across digital healthcare environments.

• AI-Based Hearing Assessment: Automated diagnostic platforms are integrating artificial intelligence to improve testing accuracy and clinical decision-making. Nearly 35% of advanced audiology centers are adopting AI-supported tools. Companies are expanding algorithm development, automation capabilities, and digital workflows to improve screening efficiency and patient outcomes.

• Tele-Audiology Platform Growth: Remote hearing assessment solutions are expanding as healthcare systems improve digital accessibility. More than 40% of hearing care providers are incorporating virtual consultation or remote testing capabilities. Manufacturers are strengthening connected device ecosystems and cloud-based platforms to support decentralized hearing care delivery.

• Portable Diagnostic Device Adoption: Compact audiometers and mobile screening tools are increasing deployment across community healthcare and field programs. Portable solutions reduce screening limitations by nearly 25% through flexible testing environments. Companies are focusing on lightweight designs, wireless connectivity, and scalable diagnostic solutions.

• Integrated Hearing Data Systems: Audiology workflows are shifting toward connected platforms combining diagnostics, patient records, and analytics. Nearly 45% of digital healthcare upgrades emphasize interoperability. Device manufacturers are developing software-enabled solutions that improve operational efficiency, reporting accuracy, and long-term hearing care management.

Audiometers dominate the Diagnostic Hearing Devices Market due to their extensive clinical adoption, high diagnostic accuracy, and essential role in evaluating hearing sensitivity across healthcare settings. Audiometers account for nearly 46% of device utilization, supported by integration across hospitals, audiology clinics, and occupational health programs. Tympanometers are witnessing the fastest adoption growth as healthcare providers increase focus on middle ear diagnostics, pediatric screening, and faster evaluation workflows.

Otoacoustic Emission (OAE) analyzers, auditory brainstem response (ABR) systems, and other specialized diagnostic devices continue supporting advanced hearing evaluations across newborn screening, neurological assessment, and preventive care applications. Nearly 38% of new audiology equipment investments are shifting toward automated and digitally connected systems. Companies are responding through AI-enabled testing platforms, portable product designs, and software integration to improve diagnostic speed, accessibility, and clinical decision-making capabilities.

• A 2025 hearing healthcare technology assessment highlighted that medical facilities deploying digital audiology platforms improved patient testing efficiency by more than 30%, supporting wider adoption of automated diagnostic hearing solutions.

Hearing loss diagnosis represents the leading application segment in the Diagnostic Hearing Devices Market due to increasing patient screening volumes, aging populations, and rising awareness of early intervention. The segment accounts for nearly 52% of demand as audiologists and healthcare providers rely on advanced diagnostic systems for accurate hearing evaluation and treatment planning. Newborn hearing screening is emerging as the fastest-growing application due to expanding government healthcare initiatives and early detection programs.

Occupational hearing testing, research applications, and specialized clinical assessments continue gaining importance as industries strengthen worker safety programs and healthcare providers expand preventive diagnostics. Nearly 42% of healthcare organizations are integrating digital hearing assessment technologies to improve testing capacity and reporting accuracy. Companies are adapting through automated workflows, cloud-based platforms, and portable diagnostic solutions designed for broader deployment environments.

• A 2026 healthcare technology review indicated that automated hearing screening programs improved diagnostic workflow efficiency by nearly 28%, enabling faster identification and management of hearing-related conditions.

Hospitals and audiology centers represent the dominant end-user group in the Diagnostic Hearing Devices Market due to high patient volumes, specialized infrastructure, and comprehensive hearing care capabilities. These facilities account for approximately 62% of adoption as healthcare providers invest in advanced audiometers, tympanometers, and integrated diagnostic platforms. Specialty clinics are becoming the fastest-growing end-user segment as decentralized healthcare models increase demand for compact and automated hearing assessment systems.

Research institutes, diagnostic laboratories, and ambulatory care centers continue adopting advanced devices for clinical studies, screening programs, and specialized evaluation requirements. Around 35% of healthcare providers are increasing investment in connected audiology technologies to enhance patient access and operational productivity. Manufacturers are targeting these users through customized solutions, training programs, service networks, and digital healthcare partnerships.

• A 2025 medical technology industry survey reported that healthcare providers using connected diagnostic systems achieved nearly 25% improvement in clinical workflow efficiency, accelerating digital transformation across audiology services.

North America accounted for the largest market share at 38.5% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

North America Diagnostic Hearing Devices Market accounted for nearly 38.5% share in 2025, supported by advanced healthcare infrastructure, widespread hearing screening programs, and strong adoption of automated audiology technologies. More than 70% of audiology clinics in the United States use digital diagnostic platforms, including advanced audiometers, tympanometers, and connected testing solutions. Increasing focus on early hearing impairment detection, occupational health monitoring, and elderly care services is accelerating technology deployment. Healthcare providers are investing in AI-enabled assessment tools, tele-audiology platforms, and integrated patient management systems to improve diagnostic accuracy and accessibility. Device manufacturers are expanding clinical partnerships and software capabilities to support evolving hearing care delivery models.

United States Market Outlook: The United States leads regional adoption through advanced audiology networks, strong medical device innovation, and established hearing healthcare programs. Hospitals and specialty clinics are expanding automated diagnostic systems to improve patient throughput and early detection. Nearly 60% of hearing care facilities are increasing investment in connected audiology technologies, strengthening clinical efficiency and digital healthcare integration.

Europe Diagnostic Hearing Devices Market accounted for approximately 30.2% share in 2025, driven by strong public healthcare systems, aging population trends, and increasing emphasis on preventive hearing care. Countries including Germany, France, and the United Kingdom are expanding adoption of digital audiometers, OAE systems, and automated screening technologies. Nearly 55% of advanced hearing care facilities across major European markets have integrated digital diagnostic solutions. Manufacturers are focusing on compact devices, interoperability improvements, and clinical workflow automation to support efficient patient management and broader accessibility.

Germany Market Outlook: Germany represents the leading European market due to its advanced healthcare infrastructure, medical technology ecosystem, and strong focus on early diagnosis. Hospitals and audiology centers are deploying connected diagnostic platforms to improve hearing assessment accuracy. More than 50% of specialized hearing care facilities use digital testing systems, supporting continued innovation in audiology service delivery.

Asia-Pacific Diagnostic Hearing Devices Market is expanding through rising healthcare investments, growing hearing awareness, and increasing access to diagnostic services. The region accounted for nearly 22.8% share in 2025, supported by China, Japan, India, and South Korea’s healthcare infrastructure development. More than 40% of new hospital modernization projects across major markets include advanced diagnostic technology upgrades. Companies are increasing regional distribution networks, affordable device development, and partnerships with healthcare providers to address rising patient volumes and improve hearing screening accessibility.

China Market Outlook: China leads Asia-Pacific adoption through healthcare infrastructure expansion, aging population needs, and increasing investment in medical technology. Hospitals and diagnostic centers are adopting automated audiology equipment to improve testing capacity and patient access. Nearly 45% of urban healthcare facilities are integrating digital diagnostic solutions, supporting wider availability of advanced hearing assessment technologies.

South America Diagnostic Hearing Devices Market is developing through increasing investment in healthcare modernization, hearing awareness programs, and improved availability of diagnostic services. The region accounted for nearly 5.3% share in 2025, with Brazil leading adoption through expanding hospital networks and specialized audiology services. Around 30% of advanced healthcare facilities are upgrading from conventional testing methods toward digital diagnostic platforms. Infrastructure limitations and uneven healthcare access remain challenges, while manufacturers are focusing on affordable devices, distributor partnerships, and portable solutions to expand market reach.

Brazil Market Outlook: Brazil represents the largest regional market due to its healthcare infrastructure scale, growing audiology service availability, and increasing demand for early hearing diagnosis. Hospitals and private clinics are adopting digital audiometers and screening systems to enhance clinical capabilities. Nearly 35% of specialized diagnostic centers are investing in upgraded hearing assessment technologies.

Middle East & Africa Diagnostic Hearing Devices Market is supported by hospital modernization initiatives, growing specialty healthcare services, and increasing awareness of hearing health. The region accounted for nearly 3.2% share in 2025, with adoption concentrated across advanced healthcare markets and urban medical centers. More than 35% of premium healthcare facilities are integrating digital diagnostic equipment to improve service quality and patient outcomes. Medical technology suppliers are strengthening regional partnerships, training programs, and distribution capabilities to support expanding audiology infrastructure.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through advanced healthcare investment, medical technology deployment, and expanding specialty care facilities. Hospitals and private healthcare providers are implementing connected audiology systems to enhance diagnostic services. Nearly 45% of advanced healthcare facilities include digital diagnostic capabilities, supporting improved access to modern hearing evaluation technologies.

The Diagnostic Hearing Devices Market is led by Demant, Natus Medical, Inventis, MAICO Diagnostics, and Interacoustics, where global audiology technology providers compete with specialized diagnostic manufacturers and digital healthcare innovators. The top five players collectively hold approximately 48% share, reflecting a clinically focused structure driven by accuracy and technology integration. Competition is based on diagnostic precision, automation capability, product reliability, and clinical workflow efficiency, with advanced systems improving testing speed by nearly 30% and enhancing assessment accuracy by around 25%. Companies are competing through AI-enabled platforms, portable device development, tele-audiology integration, and healthcare partnerships. The competitive shift is moving toward connected diagnostics, automated interpretation, and cloud-supported audiology ecosystems. Regulatory approvals, clinical validation requirements, and specialized technology expertise create strong entry barriers. Winning against established players requires advanced diagnostic performance, digital integration capability, and scalable healthcare solutions.

• Demant A/S

• Natus Medical Incorporated

• Inventis S.r.l.

• MAICO Diagnostics GmbH

• Interacoustics A/S

• Grason-Stadler Inc.

• Amplivox Ltd.

• Auditdata A/S

• MedRx Inc.

• Resonance S.r.l.

• PATH Medical GmbH

• Echodia SAS

• Intelligent Hearing Systems Corp.

• Benson Medical Instruments Co.

Diagnostic hearing technologies are advancing through AI-enabled audiometry, automated testing platforms, otoacoustic emission systems, auditory brainstem response solutions, and connected tele-audiology ecosystems. Digital diagnostic platforms are replacing manual workflows, with nearly 50% of advanced hearing care facilities adopting software-supported testing technologies to improve evaluation consistency and clinical productivity.

Compared with conventional hearing assessment methods, next-generation automated diagnostic systems improve testing efficiency by approximately 30% and reduce evaluation variability by nearly 25% through intelligent algorithms, cloud connectivity, and standardized workflows. Portable diagnostic devices are expanding access beyond traditional clinics, enabling hospitals, community healthcare providers, and mobile screening programs to improve patient coverage. Companies with strong digital platforms, AI capabilities, and integrated healthcare solutions are gaining competitive advantages.

Between 2026 and 2028, technology development will focus on predictive audiology analytics, remote diagnostics, mobile screening tools, and interoperable healthcare platforms. Providers adopting advanced diagnostic ecosystems will strengthen early detection capabilities, operational efficiency, and accessibility across modern hearing care networks.

• January 2025 – Demant expanded its hearing healthcare technology portfolio with advanced diagnostic and digital audiology solutions, improving clinical workflow efficiency by nearly 25%. The development strengthened integrated hearing care delivery and supported wider adoption of connected diagnostic platforms. Source: demant.com

• September 2024 – Natus Medical enhanced its neurodiagnostic and hearing assessment portfolio with upgraded clinical technology solutions, improving testing accuracy and operational efficiency by approximately 20%. The initiative strengthened diagnostic capabilities across hospitals and specialty healthcare environments. Source: natus.com

• March 2025 – Inventis introduced advancements across its audiology equipment portfolio, expanding digital testing capabilities and improving clinical workflow performance by nearly 30%. The innovation supported audiology professionals with more efficient diagnostic solutions and enhanced patient assessment processes. Source: inventis.it

• June 2024 – Interacoustics advanced its diagnostic audiology solutions with improved software integration and connected testing features, increasing evaluation efficiency by nearly 25%. The development supported modern hearing clinics through streamlined workflows and enhanced diagnostic data management. Source: interacoustics.com

The Diagnostic Hearing Devices Market Report provides comprehensive analysis across product types, applications, end-users, regional trends, technology evolution, and competitive strategies. The study covers audiometers, tympanometers, otoacoustic emission analyzers, auditory brainstem response systems, and advanced digital diagnostic platforms. More than 60% of adoption is concentrated across hospitals and audiology centers due to increasing demand for accurate hearing evaluation and early diagnosis.

The report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into healthcare modernization, digital audiology adoption, and clinical technology advancement. It examines AI-based diagnostics, tele-audiology, portable testing solutions, and connected healthcare platforms shaping market direction between 2026 and 2033. The analysis supports investment planning, technology development, competitive benchmarking, and expansion strategies across evolving hearing healthcare ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2,124.6 Million |

|

Market Revenue in 2033 |

USD 3,411.9 Million |

|

CAGR (2026 - 2033) |

6.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Demant A/S, Natus Medical Incorporated, Inventis S.r.l., MAICO Diagnostics GmbH, Interacoustics A/S, Grason-Stadler Inc., Amplivox Ltd., Auditdata A/S, MedRx Inc., Resonance S.r.l., PATH Medical GmbH, Echodia SAS, Intelligent Hearing Systems Corp., Benson Medical Instruments Co. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |