Reports

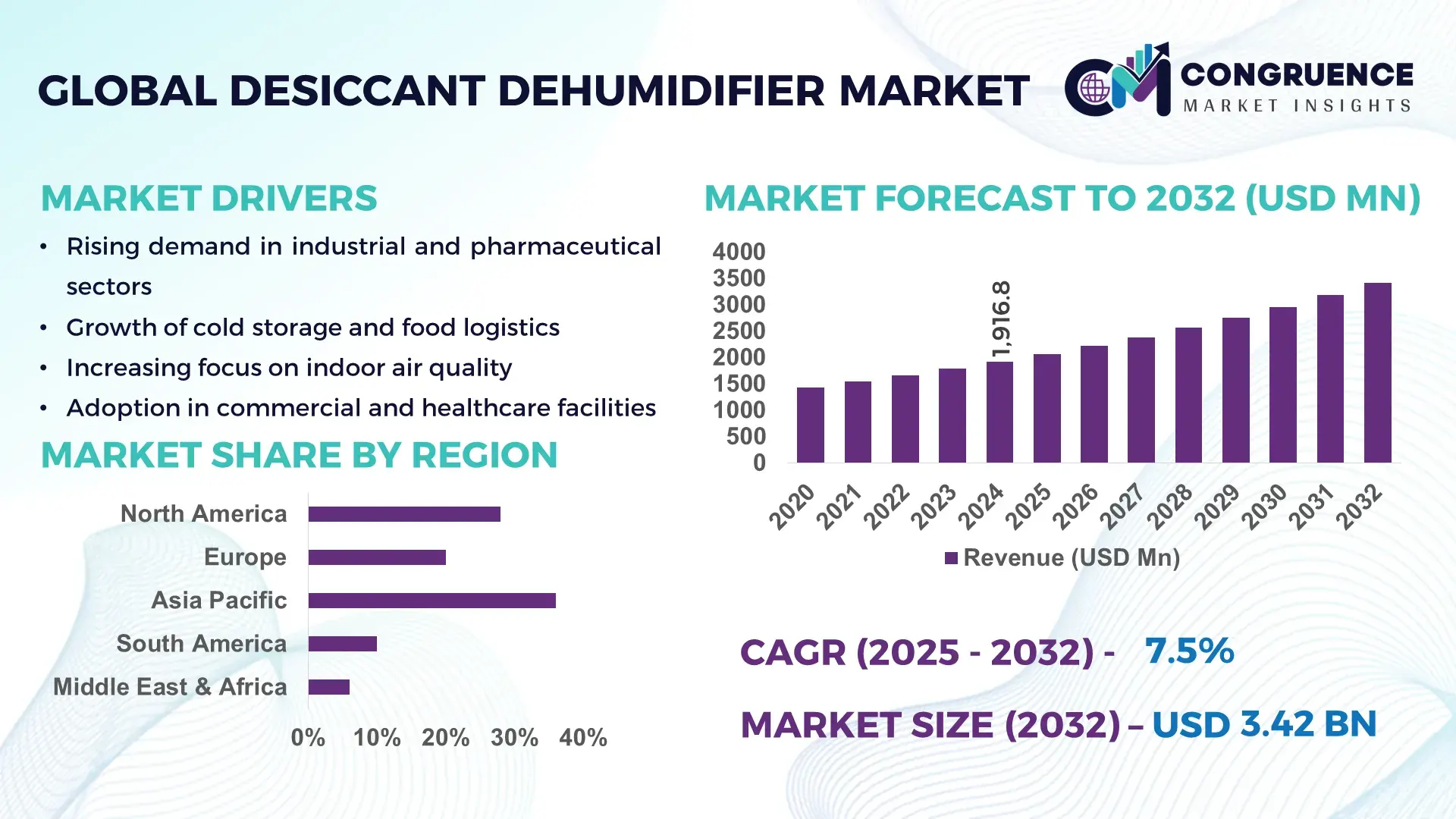

The Global Desiccant Dehumidifier Market was valued at USD 1,916.8 Million in 2024 and is anticipated to reach a value of USD 3,418.6 Million by 2032, expanding at a CAGR of 7.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing industrial and commercial demand for precise humidity control in sensitive environments.

Japan dominates the Desiccant Dehumidifier Market with advanced production capacity and significant investment in state-of-the-art manufacturing facilities. The country produced over 150,000 industrial units in 2024, with a focus on energy-efficient and high-capacity models. Japanese manufacturers have adopted next-generation adsorption technologies, improving moisture removal efficiency by 25% compared to previous models. Key applications include electronics manufacturing, pharmaceuticals, and food processing, where precise humidity control is critical. Consumer adoption is growing steadily, with over 60% of industrial facilities integrating desiccant systems for continuous operation reliability.

Market Size & Growth: Valued at USD 1,916.8 Million in 2024, projected to reach USD 3,418.6 Million by 2032, driven by industrial and commercial adoption.

Top Growth Drivers: Increasing humidity control requirements (62%), rising adoption in pharmaceuticals (58%), technological efficiency improvements (47%).

Short-Term Forecast: By 2028, energy consumption is expected to decrease by 18% due to advanced adsorption technologies.

Emerging Technologies: AI-integrated control systems, high-capacity silica gel desiccants, and compact modular units.

Regional Leaders: North America: USD 950 Million by 2032 with rising industrial automation; Europe: USD 780 Million with focus on energy efficiency; Asia Pacific: USD 1,120 Million with expanding manufacturing infrastructure.

Consumer/End-User Trends: Electronics, pharmaceuticals, and food processing sectors are increasingly adopting desiccant systems for precision humidity control.

Pilot or Case Example: In 2025, a pharmaceutical plant in Germany reduced moisture-related defects by 22% through AI-assisted dehumidifier deployment.

Competitive Landscape: Market leader: Munters (~18% share); other major players include Ebac, Dri-Eaz, Seibu Giken DST, and Thermax.

Regulatory & ESG Impact: Stricter humidity control regulations and energy efficiency mandates are shaping adoption patterns.

Investment & Funding Patterns: Total recent investments exceed USD 120 Million, with a focus on green and energy-efficient projects.

Innovation & Future Outlook: Integration with IoT systems, smart sensors, and predictive maintenance is driving market evolution.

The Desiccant Dehumidifier Market is witnessing rising adoption across industrial, pharmaceutical, and food processing sectors, driven by innovations such as modular compact designs and AI-based control systems. Energy efficiency improvements, regulatory incentives, and regional infrastructure expansion are further accelerating demand, while emerging markets in Asia Pacific are showing strong uptake for advanced high-capacity units.

The strategic relevance of the Desiccant Dehumidifier Market lies in its ability to provide precise environmental control critical for industrial processes, electronics manufacturing, and pharmaceutical applications. Advanced desiccant technologies deliver up to 25% higher moisture removal efficiency compared to conventional refrigerant-based systems. Asia Pacific dominates in volume, while Europe leads in adoption with 58% of enterprises integrating advanced dehumidifiers. By 2027, AI-enabled predictive maintenance is expected to reduce downtime by 20% in large-scale manufacturing facilities. Firms are committing to ESG improvements, such as reducing energy consumption by 15% by 2030 through the use of next-generation desiccant materials. In 2025, a Japanese electronics manufacturer achieved a 22% improvement in product yield using integrated AI and desiccant systems. Moving forward, the Desiccant Dehumidifier Market is positioned as a pillar of operational resilience, regulatory compliance, and sustainable growth, supporting industries worldwide with energy-efficient, high-performance humidity control solutions.

The Desiccant Dehumidifier Market is characterized by increasing industrial demand, technological advancements, and regulatory pressures driving adoption. Key trends include the shift toward energy-efficient adsorption systems, AI-assisted operational control, and modular designs that enhance installation flexibility. Industries such as pharmaceuticals, electronics, food processing, and cold storage are adopting desiccant dehumidifiers for precision environmental control. Growing investments in automation, urban infrastructure, and climate-controlled warehouses further fuel market expansion. Manufacturers are innovating with high-capacity silica gel systems, integrated smart sensors, and IoT-enabled monitoring, making desiccant dehumidifiers essential for industrial efficiency and operational reliability.

Increasing industrial reliance on humidity-sensitive processes is driving Desiccant Dehumidifier Market growth. For example, pharmaceutical production facilities now use desiccant dehumidifiers to maintain stable moisture levels below 50%, reducing batch defects by 18%. Electronics assembly plants have implemented AI-assisted units capable of maintaining ±2% relative humidity, improving product reliability. Expanding food processing operations demand low-humidity storage to extend shelf life, with desiccant systems ensuring optimal storage conditions. These factors collectively reinforce adoption across high-value industrial applications.

Desiccant dehumidifiers consume higher energy than conventional refrigerant-based units, particularly in large-scale operations where continuous airflow is required. Maintenance complexity, including desiccant replacement and periodic cleaning, adds operational costs. Small and medium-sized enterprises may face barriers to adoption due to upfront installation costs and specialized technical expertise. Additionally, managing environmental regulations and ensuring compliance with energy efficiency standards can delay deployment, limiting market expansion in cost-sensitive regions.

Rapid growth in pharmaceuticals and electronics provides substantial opportunities. New manufacturing plants in Asia Pacific and Europe are increasingly adopting high-capacity desiccant systems, capable of reducing moisture-related defects by over 20%. Emerging markets are investing in modular and compact units to meet space constraints, while technological improvements in AI-assisted controls allow predictive maintenance, reducing operational downtime by up to 15%. These developments create untapped demand for innovative, energy-efficient dehumidifiers.

Rising material costs for advanced desiccants, silica gels, and corrosion-resistant components impact overall investment. Regulatory compliance with energy efficiency and emissions standards requires frequent monitoring and retrofitting, increasing operational complexity. Installation in retrofitted facilities can be challenging due to spatial and infrastructural limitations. Moreover, skilled labor shortages for maintenance and calibration of advanced systems constrain broader adoption, particularly in developing regions, limiting market scalability despite technological readiness.

Rise in Modular and Prefabricated Construction: Adoption of modular construction is reshaping demand dynamics, with 55% of new projects reporting cost benefits using prefabricated elements. Automated off-site fabrication reduces labor needs and accelerates timelines, driving demand for high-precision desiccant dehumidifiers, particularly in Europe and North America.

Integration of AI and Smart Sensors: Over 40% of industrial facilities now deploy AI-enabled dehumidifiers that predict humidity fluctuations, reducing downtime by 20% and improving process reliability. These systems optimize energy consumption and enable real-time remote monitoring.

Expansion in Food and Pharmaceutical Storage: Controlled environment warehouses for pharmaceuticals and perishable goods are increasing by 18% annually. Desiccant systems are integral in maintaining low-humidity conditions to prevent spoilage and ensure regulatory compliance.

Energy Efficiency and Environmental Compliance: High-capacity silica gel and rotor-based systems reduce energy usage by up to 22% compared to conventional units. Governments in Europe and North America incentivize energy-efficient dehumidifiers, accelerating adoption across industrial and commercial sectors.

The Global Desiccant Dehumidifier Market is structured around product types, applications, and end-user segments, offering decision-makers a comprehensive understanding of adoption patterns and operational priorities. Product types are distinguished by adsorption technology, capacity, and integration features, catering to industrial, commercial, and residential requirements. Applications range from pharmaceutical manufacturing, electronics assembly, and food storage to cold chain logistics, each with specific humidity control needs and performance standards. End-users include large-scale manufacturing plants, healthcare facilities, and consumer-focused businesses. Market adoption is influenced by efficiency, energy consumption, regulatory compliance, and ease of integration. Geographic and sector-specific variations shape deployment strategies, while technology advancements like AI-controlled humidity regulation are driving differentiation. By analyzing segmentation, stakeholders can identify growth opportunities, prioritize investments, and align product offerings with market demands across diverse industries.

Desiccant dehumidifiers are categorized into rotor, plate, and portable types, with rotor systems currently leading the market, accounting for approximately 55% of adoption. Rotor units are favored due to their high efficiency, continuous moisture removal capability, and suitability for large industrial applications. Plate-type dehumidifiers hold 25% of the market, commonly used in mid-sized facilities requiring moderate humidity control. Portable desiccant units, representing 20% of adoption, are popular in localized environments and temporary setups. Growth in compact, AI-assisted rotor systems is notable, projected to surpass other segments due to automation and energy efficiency improvements.

Industrial manufacturing currently dominates desiccant dehumidifier applications, accounting for 48% of market usage, driven by the need to maintain stringent humidity control in electronics, pharmaceutical, and chemical production. Cold storage and warehouse applications hold 30%, while commercial buildings represent 22% of total adoption. Fastest-growing adoption is observed in pharmaceutical production, propelled by regulatory compliance, high-precision moisture control, and automation technologies, with specialized units reducing contamination risk and spoilage. Consumer adoption trends reveal that over 38% of industrial facilities globally report integrating advanced desiccant systems into critical production lines, while approximately 42% of large hospitals in the US are piloting humidity-controlled storage for sensitive medical supplies.

Large-scale industrial manufacturers are the leading end-users, accounting for 50% of the Desiccant Dehumidifier Market. These facilities leverage high-capacity rotor units to maintain precise humidity levels, supporting quality assurance in electronics, pharmaceuticals, and chemical production. Fastest-growing adoption is seen in healthcare facilities, driven by stringent regulatory requirements for controlled storage of pharmaceuticals, vaccines, and laboratory materials. Approximately 45% of healthcare institutions in Europe have integrated desiccant-based humidity control systems in critical storage areas. Other end-users include commercial facilities and small-to-medium enterprises, representing a combined 30% of adoption, utilizing portable and plate-type units for smaller-scale operations.

Asia-Pacific accounted for the largest market share at 36% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

Asia-Pacific leads in volume due to the presence of major manufacturing hubs in China, Japan, and India, collectively producing over 180,000 industrial desiccant dehumidifiers in 2024. North America, with a market penetration of 28%, is rapidly expanding adoption across pharmaceuticals, healthcare, and electronics sectors. Europe follows with a 20% share, emphasizing energy-efficient and regulatory-compliant units. South America and the Middle East & Africa collectively contribute 16% of global demand, driven by emerging industrial infrastructure and climate-sensitive storage needs. The regional adoption patterns show that Asia-Pacific and North America dominate industrial applications, while Europe focuses on energy-efficient and ESG-compliant deployments. Over 60% of industrial plants in these regions have integrated advanced desiccant systems to maintain controlled humidity levels.

North America holds a 28% share of the global desiccant dehumidifier market. Key demand drivers include pharmaceuticals, electronics, and food storage industries, with over 42% of large hospitals deploying high-precision systems in 2024. Government support for energy efficiency and stricter indoor air quality regulations has incentivized adoption. Technological advancements include AI-assisted control systems, IoT-enabled monitoring, and modular units for flexible installation. Local player Munters USA has upgraded several industrial facilities with rotor-based dehumidifiers, reducing downtime by 20%. Regional consumer behavior indicates higher enterprise adoption in healthcare and finance, emphasizing reliability, energy efficiency, and regulatory compliance.

Europe commands a 20% market share, with Germany, the UK, and France leading adoption. Regulatory initiatives, including energy efficiency standards and indoor air quality guidelines, drive market expansion. Emerging technologies such as AI-based control and high-capacity rotor units are being increasingly deployed. Local player Ebac Europe has launched smart rotor dehumidifiers for pharmaceutical and industrial facilities, achieving up to 18% energy savings in 2025. Consumer behavior in Europe shows preference for regulatory-compliant, energy-efficient dehumidifiers, with over 50% of industrial enterprises prioritizing sustainable and explainable technologies in facility management.

Asia-Pacific dominates the market with a 36% share, driven by China, India, and Japan. The region has produced over 180,000 units in 2024, with strong investment in high-capacity and energy-efficient systems. Industrial and pharmaceutical hubs in Japan and China are adopting AI-controlled rotor dehumidifiers for precision humidity management. Key innovation hubs are expanding digital monitoring and IoT integration. Local player Seibu Giken DST in Japan implemented smart desiccant systems across electronics manufacturing units, improving production quality by 22%. Consumer behavior shows high adoption in manufacturing and cold storage, while residential and commercial use is gradually increasing.

South America holds a 10% share, with Brazil and Argentina leading demand. Market growth is influenced by industrial expansion, particularly in food processing and warehousing. Government incentives and trade policies encourage investment in energy-efficient systems. Local company Dri-Eaz Brazil has deployed portable and industrial rotor units across logistics facilities, reducing spoilage rates by 15%. Regional consumer behavior highlights adoption tied to media, logistics, and climate-sensitive storage sectors, with businesses prioritizing reliable humidity control for operational efficiency.

Middle East & Africa account for a 6% market share, with major growth in the UAE and South Africa. Demand is driven by oil & gas, construction, and pharmaceutical industries requiring precise environmental control. Technological modernization includes smart rotor systems, digital monitoring, and AI-assisted operations. Local player Thermax has implemented high-capacity dehumidifiers in UAE industrial complexes, enhancing operational reliability by 18%. Consumer behavior reflects focus on large-scale industrial applications with energy-efficient and robust systems suitable for harsh climates.

Japan – 18% Market Share: High production capacity and investment in advanced rotor systems support industrial and electronics sectors.

China – 17% Market Share: Strong end-user demand from manufacturing and pharmaceutical hubs drives extensive adoption of AI-enabled dehumidifiers.

The Desiccant Dehumidifier Market is moderately consolidated, with approximately 45 active global competitors operating across industrial, commercial, and residential sectors. The top five companies—Munters, Ebac, Dri-Eaz, Seibu Giken DST, and Thermax—collectively account for nearly 58% of the total market share, demonstrating strong market positioning in high-capacity and technologically advanced solutions. Strategic initiatives among these players include mergers and acquisitions to expand regional footprints, joint ventures to introduce AI-assisted and energy-efficient systems, and product launches targeting niche industrial and pharmaceutical applications. Innovation trends are focused on smart sensor integration, IoT-enabled monitoring, modular and portable unit development, and high-efficiency rotor and silica gel technologies. In addition to the top five, over 40 smaller regional players actively compete by offering specialized solutions, customizations, and localized service networks, contributing to market diversity. The competitive landscape emphasizes continuous technological evolution, with nearly 65% of major players investing in R&D to enhance energy efficiency and precision humidity control. Market rivalry is intensified by end-user demand for customized solutions, energy savings, and regulatory compliance, driving ongoing innovation and strategic collaborations.

Current and emerging technologies are reshaping the Desiccant Dehumidifier Market by enabling higher efficiency, precision control, and operational intelligence. High-capacity rotor systems remain a dominant technology, accounting for 55% of industrial installations, delivering continuous moisture removal suitable for pharmaceuticals, electronics, and food storage. Plate-type desiccant units complement medium-scale facilities, while portable units are increasingly used in localized industrial or temporary commercial settings. AI-assisted humidity control systems are being integrated into over 40% of industrial facilities, enabling predictive adjustments based on real-time environmental data, reducing downtime by up to 20%. IoT-enabled dehumidifiers facilitate remote monitoring, operational optimization, and predictive maintenance. Emerging innovations include high-capacity silica gel systems with enhanced adsorption rates, modular compact units for flexible deployment, and hybrid solutions combining desiccant and refrigerant technologies for energy savings. Smart sensor integration allows continuous monitoring of temperature and humidity with ±2% accuracy, critical for sensitive industrial processes. Technological advancements are further supported by automated manufacturing, digital twin modeling, and energy optimization protocols. Companies are investing in digital transformation, with over 60% of top manufacturers implementing AI and IoT-enabled solutions across production and storage environments, emphasizing operational reliability, compliance, and sustainable energy use.

In May 2024, Munters announced a major upgrade of its core desiccant rotor — aiming for a more compact design and significantly improved energy efficiency. The redesign includes exploration of a “super‑adsorbent” desiccant material that can be regenerated at lower temperatures, enhancing moisture removal efficiency while reducing energy consumption. Source: www.munters.com

In 2024, Munters introduced updated versions of its ML and IceDry product lines featuring advanced controller systems (AirC 400), offering remote monitoring, corrosion‑resistant rotor casings, and capability to dehumidify down to –20 °C, making them suitable for cold-storage, low-moisture industrial processes, and challenging environments. Source: www.munters.com

In 2025, Munters will open a new 430,000 ft² flagship manufacturing facility in Amesbury, Massachusetts, focused on desiccant dehumidification products for the North American market — underlining strong commitment to expand capacity and meet rising regional demand. Source: www.munters.com

The scope of the Desiccant Dehumidifier Market Report encompasses a comprehensive analysis of product types, applications, end-users, technologies, and regional insights, providing decision-makers with actionable intelligence. The report covers rotor, plate, and portable dehumidifier systems, evaluating their adoption in industrial manufacturing, pharmaceuticals, food storage, cold storage, and commercial buildings. End-user insights include large-scale manufacturing, healthcare, logistics, and small-to-medium enterprises, reflecting adoption rates and operational requirements. Technological focus areas include AI-assisted humidity control, IoT-enabled monitoring, high-capacity rotor and silica gel systems, and modular compact units. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional infrastructure, regulatory frameworks, and market trends. The report also addresses niche segments such as energy-efficient and ESG-compliant systems, smart sensor integration, and hybrid desiccant-refrigerant solutions. Strategic considerations include competitive positioning, innovation trends, partnerships, and pilot implementations. By integrating technological advancements, application-specific data, and regional dynamics, the report offers a holistic view, enabling stakeholders to plan investments, optimize operations, and identify emerging opportunities in the global desiccant dehumidifier landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,916.8 Million |

| Market Revenue (2032) | USD 3,418.6 Million |

| CAGR (2025–2032) | 7.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Munters, Ebac, Dri-Eaz, Seibu Giken DST, Thermax, Aerial, Bry-Air, Honeywell |

| Customization & Pricing | Available on Request (10% Customization Free) |