Reports

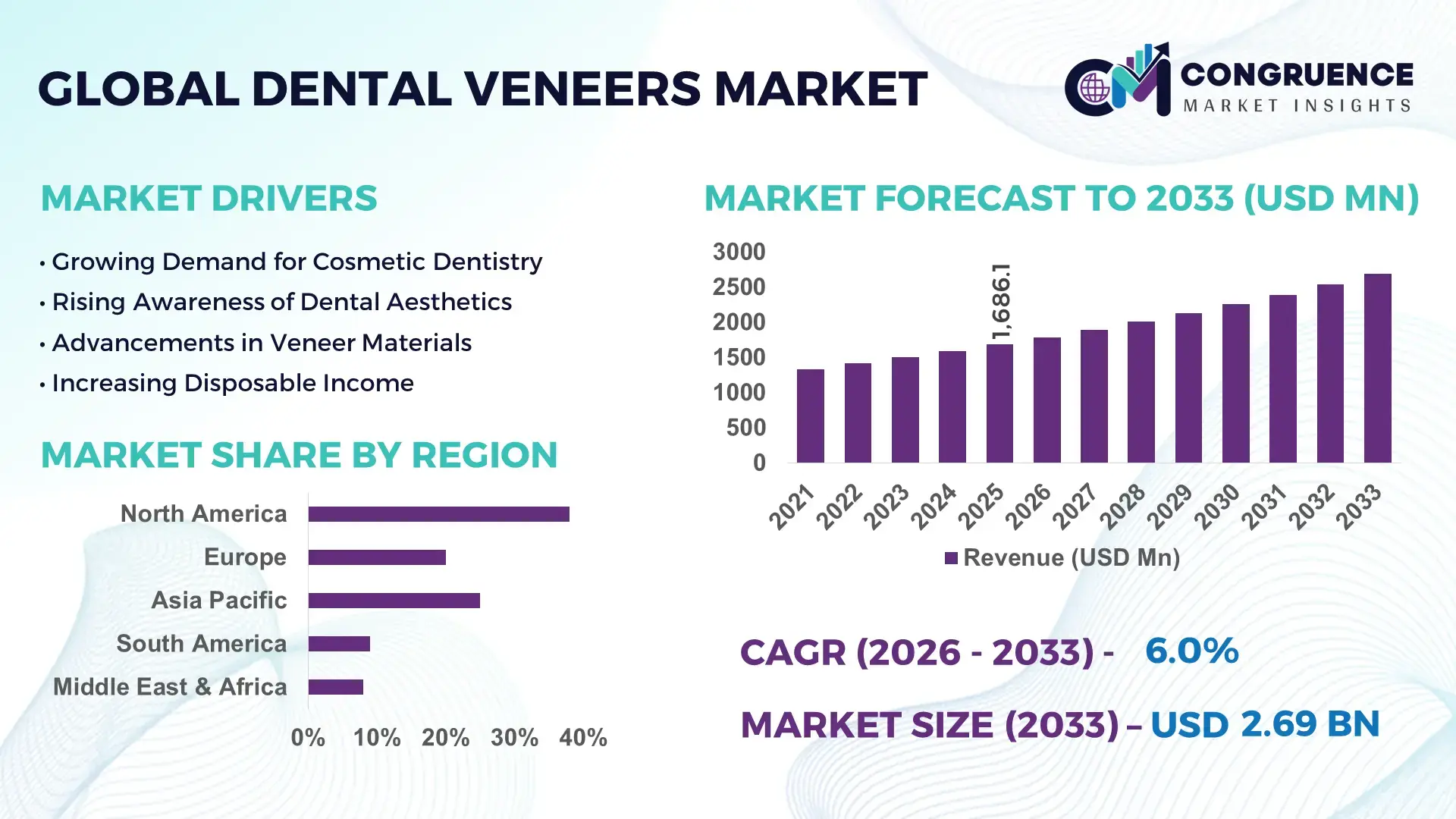

The Global Dental Veneers Market was valued at USD 1686.07 Million in 2025 and is anticipated to reach a value of USD 2687.34 Million by 2033 expanding at a CAGR of 6% between 2026 and 2033. Rising adoption of minimally invasive cosmetic dentistry, rapid digital smile-design integration, and expanded zirconia-ceramic manufacturing capacity across advanced dental laboratories are accelerating high-value veneer procedures globally.

The United States accounted for nearly 34% of global dental veneers procedure volume in 2025, supported by over USD 1.2 billion in cosmetic dental technology investments and digital dentistry adoption exceeding 58% across premium clinics. Germany maintained stronger ceramic veneer export efficiency with laboratory turnaround times nearly 18% lower than North America, while South Korea expanded dental tourism inflows by 22% through AI-assisted smile simulation systems amid rising Asia-Pacific elective dentistry demand following post-pandemic healthcare normalization.

Manufacturers and dental service organizations are prioritizing digital workflow scalability, regional laboratory partnerships, and premium material differentiation to strengthen competitive positioning in the high-growth cosmetic dentistry ecosystem.

Market Size & Growth: USD 1686.07 Million in 2025 reaching USD 2687.34 Million by 2033 at 6% CAGR, driven by advanced CAD/CAM veneer fabrication and digital cosmetic dentistry expansion.

Top Growth Drivers: Cosmetic dentistry demand increased 21%, digital smile-design adoption reached 58%, and zirconia veneer utilization expanded 17% globally during 2025.

Short-Term Forecast: By 2027, chairside veneer workflow efficiency improves 26% while laboratory production costs decline approximately 14% through automation integration.

Emerging Technologies: AI-assisted smile simulation, 3D intraoral scanning, and nano-ceramic veneer materials improved procedural precision by nearly 24% across premium clinics.

Regional Leaders: North America exceeds USD 920 Million with strong cosmetic clinic penetration, Europe crosses USD 640 Million through ceramic innovation, while Asia-Pacific expands fastest with dental tourism growth above 19%.

Consumer/End-User Trends: Nearly 47% of urban cosmetic dentistry patients now prefer minimally invasive veneers over orthodontic correction for faster aesthetic outcomes.

Pilot/Case Example: In 2025, digitally integrated dental laboratories reduced veneer remakes by 31% and shortened delivery timelines by 4–6 days.

Competitive Landscape: The top five players control approximately 38% market share, with leading activity concentrated among premium ceramic manufacturers and digital dentistry solution providers.

Regulatory & ESG Impact: Sustainable ceramic processing reduced laboratory material waste by 16%, while stricter European medical device compliance accelerated premium product standardization.

Investment & Funding: Global cosmetic dentistry infrastructure investments surpassed USD 780 Million in 2025, supported by cross-border partnerships and Asia-Pacific laboratory expansion.

Innovation & Future Outlook: Next-generation ultra-thin veneers and AI-driven treatment planning are strengthening personalized cosmetic dentistry and improving clinic conversion rates by over 20%.

The Dental Veneers Market is advancing through higher demand for ultra-thin ceramic veneers, AI-powered smile visualization, and rapid chairside restoration systems across cosmetic dentistry networks. Digital workflow integration improved treatment acceptance rates by nearly 23% in 2025, particularly in urban dental clinics. Expanding dental tourism hubs in Asia and stricter aesthetic dentistry quality standards in Europe are reshaping laboratory sourcing, premium material procurement, and strategic clinic partnerships across the global value chain.

The Dental Veneers Market has become strategically important as cosmetic dentistry shifts from premium elective care toward digitally integrated aesthetic treatment ecosystems. Dental service organizations, advanced laboratories, and material suppliers are consolidating operations to improve turnaround efficiency and patient conversion rates. In 2026, supply-chain restructuring across ceramic and zirconia materials accelerated localized manufacturing in Germany, South Korea, and the United States, reducing import dependency and improving laboratory fulfillment reliability by nearly 19%.

AI-assisted smile-design platforms and chairside CAD/CAM systems now complete veneer workflows nearly 32% faster than traditional manual laboratory modeling while reducing remake rates by approximately 24%. The United States leads in high-value digital cosmetic dentistry deployment, with more than 60% of premium clinics using intraoral scanning systems, while Turkey and Thailand are expanding cross-border dental tourism through lower procedural costs and rapid digital restoration capabilities. Over the next 2–3 years, same-day veneer procedures are expected to exceed 28% of urban cosmetic dental treatments globally.

Major dental groups are expanding partnerships with digital scanner manufacturers, ceramic suppliers, and cloud-based treatment planning providers to standardize multi-location operations. Clinics adopting vertically integrated laboratory networks are strengthening procedural consistency, pricing control, and patient retention, positioning digital veneer ecosystems as a long-term competitive differentiator in aesthetic dentistry.

Rapid deployment of digital dentistry infrastructure is accelerating veneer procedure volumes across urban cosmetic clinics and multi-location dental service organizations. In 2025, nearly 58% of premium dental clinics integrated intraoral scanners and AI-assisted smile simulation platforms, improving treatment acceptance rates by 21% and reducing procedural adjustments by approximately 18%. The United States and South Korea expanded chairside CAD/CAM installations to shorten veneer delivery timelines from 10 days to under 48 hours. Rising consumer preference for minimally invasive cosmetic correction is driving ceramic veneer utilization, particularly among patients aged 25–45. In response, companies are investing in automated milling systems, regional laboratory hubs, and strategic partnerships with digital workflow providers to improve scalability, reduce remakes, and strengthen operational margins within high-throughput cosmetic dentistry networks.

High dependence on imported ceramic blocks, zirconia materials, and precision milling equipment continues to constrain cost optimization across the dental veneers ecosystem. In 2025, advanced lithium disilicate veneer materials experienced price fluctuations of nearly 14%, while laboratory energy and logistics expenses increased approximately 11% across European manufacturing hubs. Smaller clinics in India, Brazil, and Southeast Asia face deployment limitations due to high digital equipment acquisition costs and uneven technician availability. Regulatory compliance requirements for dental ceramics and adhesive materials are also increasing certification timelines for suppliers. To reduce operational exposure, companies are localizing procurement networks, expanding distributor agreements, and adopting hybrid manufacturing strategies combining centralized milling with regional finishing laboratories to maintain profitability and improve delivery consistency.

AI-enabled treatment planning and next-generation ultra-thin veneer materials are creating high-value opportunities across cosmetic dentistry networks. Digital smile-design systems improved procedural planning efficiency by nearly 27% in 2025, while ultra-thin ceramic veneers reduced enamel removal requirements by approximately 35%, strengthening patient preference for minimally invasive treatment. China and the United Arab Emirates are rapidly expanding premium dental infrastructure through smart clinic investments and medical tourism initiatives linked to advanced aesthetic dentistry services. Companies are developing cloud-connected diagnostic ecosystems integrating imaging, treatment simulation, and automated manufacturing workflows. A non-obvious opportunity is emerging in subscription-based cosmetic dental maintenance programs, where clinics bundle veneer monitoring, whitening, and digital follow-up services to improve long-term patient retention and recurring procedural demand.

Maintaining consistent veneer quality across expanding digital dentistry networks remains a major execution challenge. In 2025, nearly 29% of cosmetic clinics reported workflow inefficiencies linked to interoperability gaps between intraoral scanners, CAD software, and milling systems. Advanced veneer fabrication also requires highly trained dental technicians, yet technician shortages exceeded 18% across Germany and the United Kingdom due to rising demand for precision cosmetic restorations. Inconsistent shade matching, software calibration issues, and fragmented laboratory systems continue to affect procedural consistency and patient satisfaction. Companies must invest in technician training academies, interoperable digital platforms, and centralized quality-control systems to sustain large-scale deployment efficiency. Stronger collaboration between dental technology providers and laboratory operators will determine long-term competitiveness and operational reliability in advanced cosmetic dentistry markets.

AI-Led Smile Design Expansion AI-assisted treatment planning platforms increased deployment by 33% across premium cosmetic dental chains during 2025, while digital case acceptance rates improved nearly 26%. Clinics in the United States and South Korea are integrating intraoral scanners with cloud-based veneer simulation software to reduce consultation timelines from 5 days to under 24 hours. Companies are responding through software partnerships and vertically integrated digital workflows to improve procedural precision and reduce remake-related operational losses.

Localized Ceramic Supply Networks Rising logistics volatility and stricter European material traceability standards pushed nearly 21% of veneer manufacturers to restructure ceramic sourcing during 2025. Germany and Türkiye expanded regional milling and finishing operations to reduce import dependency and shorten delivery cycles by approximately 17%. Dental laboratories are increasingly shifting toward hybrid production models combining centralized CAD design with localized finishing hubs, improving supply continuity and lowering inventory pressure for high-volume cosmetic clinics.

Chairside Workflow Automation Growth Automated chairside veneer fabrication systems reduced procedural turnaround time by almost 38% compared to conventional laboratory workflows. More than 54% of urban cosmetic dentistry centers in Japan and the United States adopted same-day restoration technologies to address technician shortages and rising patient scheduling demand. Equipment manufacturers are expanding leasing models and bundled scanner-milling packages to accelerate deployment among mid-sized clinics with limited capital flexibility.

Minimally Invasive Veneer Adoption Ultra-thin veneer procedures increased approximately 29% in 2025 as clinics prioritized enamel-preserving cosmetic treatments for younger patient groups. Composite-enhanced ceramic materials improved fracture resistance by nearly 16%, supporting broader deployment in alignment correction and chipped tooth restoration cases. Companies are scaling biocompatible material portfolios and investing in low-prep veneer technologies as sustainability-focused healthcare procurement and patient retention metrics become increasingly linked to minimally invasive dentistry outcomes.

Porcelain Veneers remained the leading segment in 2025, accounting for nearly 48% of total veneer procedures due to superior durability, stain resistance, and compatibility with digital CAD/CAM fabrication systems. Premium cosmetic clinics in the United States and Germany increasingly standardized porcelain workflows because automated ceramic milling reduced procedural remakes by approximately 22% and improved long-term restoration consistency. Composite Veneers maintained strong adoption among mid-cost dental providers because treatment costs remained nearly 35% lower than porcelain alternatives, supporting higher procedural accessibility in India and Brazil. Temporary Veneers continued to play a transitional role in multi-stage smile restoration procedures, particularly in high-throughput dental tourism clinics.

Lumineers emerged as the fastest-growing type, with adoption increasing approximately 27% during 2025 as minimally invasive cosmetic dentistry gained traction among patients aged 25–40. Their reduced enamel preparation requirements improved treatment acceptance and shortened clinical preparation time by nearly 18%. Removable Veneers remained niche but gained visibility through direct-to-consumer cosmetic dentistry platforms. Manufacturers are expanding ultra-thin ceramic portfolios, partnering with digital dentistry providers, and scaling localized milling capabilities to strengthen premium veneer differentiation and procedural efficiency.

Smile Makeover remained the dominant application segment in 2025, representing approximately 42% of veneer utilization due to rising demand for full-mouth aesthetic enhancement and digitally customized treatment planning. Cosmetic dentistry centers in the United States, Türkiye, and Thailand expanded integrated smile-design packages combining veneers, whitening, and alignment correction to improve patient conversion rates by nearly 24%. Teeth Whitening continued to support veneer demand through bundled cosmetic treatment programs, while Chipped Tooth Repair maintained stable procedural volume across restorative dentistry networks focused on rapid aesthetic correction and minimally invasive restoration workflows.

Alignment Improvement emerged as the fastest-growing application, with veneer-assisted correction procedures increasing nearly 28% during 2025 as patients sought faster alternatives to long-duration orthodontic treatment. AI-assisted smile simulation and ultra-thin ceramic technologies improved procedural precision and reduced chairside adjustments by approximately 19%. Gap Correction procedures also gained traction among younger patient groups seeking short-cycle cosmetic enhancement. Dental providers are investing in integrated digital imaging systems, automated treatment planning software, and multi-service cosmetic packages to improve operational efficiency and strengthen premium treatment positioning.

Dental Clinics remained the dominant end-user segment in 2025, contributing nearly 46% of veneer procedure deployment due to high patient throughput, direct cosmetic consultation capabilities, and expanding chairside digital dentistry infrastructure. Large clinic networks in the United States and South Korea increased investment in intraoral scanning and same-day veneer fabrication systems, reducing treatment completion timelines by approximately 34%. Cosmetic Dentistry Centers followed closely, benefiting from rising demand for premium aesthetic procedures and personalized smile-design services. Dental Laboratories maintained strategic importance through centralized ceramic milling and precision finishing operations supporting multi-location clinic networks.

Specialty Dental Centers emerged as the fastest-growing end-user group, with procedure volumes increasing approximately 26% during 2025 due to specialization in minimally invasive cosmetic restoration and AI-assisted treatment workflows. Hospitals expanded veneer integration mainly through dental reconstruction and multidisciplinary cosmetic treatment programs, while Academic Dental Institutes increased adoption of digital simulation systems for advanced cosmetic dentistry training. Companies are strengthening partnerships with clinic chains, offering scanner-milling equipment bundles, and developing subscription-based laboratory support models to secure long-term procedural volume and strengthen competitive positioning across advanced aesthetic dentistry ecosystems.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

Digital Cosmetic Dentistry Consolidation Accelerates

North America maintained leadership in the dental veneers market through high digital dentistry penetration, advanced cosmetic clinic networks, and strong laboratory automation infrastructure. Nearly 62% of premium cosmetic dental centers in the United States and Canada integrated chairside CAD/CAM systems during 2025, reducing veneer turnaround timelines by approximately 36%. Multi-location dental service organizations increasingly consolidated procurement and laboratory operations to improve pricing control and procedural consistency. Same-day veneer procedures expanded rapidly across metropolitan clinics, supported by AI-assisted smile simulation and cloud-based treatment planning platforms. Strategic partnerships between scanner manufacturers, ceramic suppliers, and cosmetic dentistry chains strengthened workflow integration and accelerated premium veneer deployment across urban healthcare infrastructure.

United States Market Outlook: The United States remained the operational center of North American veneer deployment, supported by high cosmetic dentistry spending, advanced dental laboratory infrastructure, and rapid adoption of digital workflows. More than 58% of cosmetic dental clinics deployed intraoral scanning systems by 2025, while integrated laboratory networks reduced procedural remakes by nearly 23%. Enterprise dental groups are expanding vertically integrated milling facilities and subscription-based cosmetic treatment programs to strengthen patient retention and operational scalability.

Precision Ceramic Manufacturing Shapes Competition

Europe strengthened its market position through precision ceramic manufacturing, stringent medical device compliance, and modernization of cosmetic dental laboratories. Germany, Italy, and Switzerland accounted for a major share of advanced veneer material production, with automated milling deployment increasing approximately 19% during 2025. Regulatory emphasis on biocompatibility and material traceability accelerated premium ceramic veneer adoption across advanced cosmetic clinics. European dental laboratories increasingly shifted toward localized production models to reduce logistics dependency and improve procedural turnaround efficiency. Sustainability-focused procurement also encouraged the adoption of low-waste ceramic processing technologies and digitally optimized veneer fabrication systems across high-volume cosmetic dentistry networks.

Germany Market Outlook: Germany led the European dental veneers market through advanced laboratory engineering, high-precision ceramic manufacturing, and strong digital dentistry infrastructure. Nearly 64% of premium dental laboratories in Germany integrated automated milling and AI-supported design workflows by 2025. The country’s strong export ecosystem for dental materials and equipment continues to support cross-border cosmetic dentistry expansion while enabling rapid deployment of ultra-thin ceramic veneer technologies across specialized aesthetic treatment centers.

Dental Tourism and Digital Scaling Drive Expansion

Asia-Pacific emerged as the fastest-expanding market due to rising dental tourism, rapid cosmetic clinic expansion, and increasing deployment of cost-efficient digital dentistry systems. South Korea, China, Thailand, and India accelerated investment in smart dental infrastructure, while veneer procedure volumes increased approximately 28% across urban cosmetic dentistry centers during 2025. Regional laboratories expanded localized ceramic finishing operations to reduce import dependency and improve delivery speed. AI-assisted smile-design systems and chairside restoration technologies gained rapid adoption among premium clinics targeting international patients. Companies are prioritizing franchise clinic expansion, digital workflow integration, and strategic partnerships with dental tourism facilitators to capture rising cross-border cosmetic procedure demand.

South Korea Market Outlook: South Korea established itself as a major innovation hub for cosmetic dentistry through AI-enabled smile simulation, high-density cosmetic clinic networks, and advanced same-day veneer deployment capabilities. More than 52% of premium cosmetic dentistry providers adopted integrated digital veneer workflows by 2025. The country’s strong dental tourism ecosystem and rapid procedural turnaround capacity continue attracting international patients seeking minimally invasive aesthetic restoration supported by advanced digital treatment planning infrastructure.

Affordable Cosmetic Dentistry Expands Access

South America experienced rising veneer adoption through expanding cosmetic dentistry awareness and increasing availability of mid-cost digital restoration services. Brazil accounted for the largest deployment concentration in the region, supported by strong cosmetic healthcare culture and growing investment in dental imaging infrastructure. Composite veneer procedures increased nearly 24% during 2025 as clinics prioritized cost-efficient aesthetic restoration for middle-income patient groups. However, uneven access to automated milling systems and imported ceramic materials continues to affect procedural consistency outside major urban centers. Companies are responding through regional laboratory partnerships, localized training initiatives, and flexible equipment financing strategies to improve operational scalability across emerging cosmetic dentistry networks.

Brazil Market Outlook: Brazil remained the largest cosmetic dentistry market in South America due to high aesthetic treatment demand and broad private dental clinic penetration. Approximately 47% of urban cosmetic clinics integrated digital imaging systems by 2025 to improve treatment planning and shorten veneer consultation timelines. Domestic dental distributors are expanding partnerships with ceramic material suppliers and CAD/CAM equipment providers to strengthen local availability and reduce dependency on imported laboratory technologies.

Premium Dental Infrastructure Modernization Accelerates

The Middle East & Africa market expanded through premium healthcare infrastructure modernization, rising medical tourism investment, and increasing adoption of advanced cosmetic dentistry technologies. The United Arab Emirates and Saudi Arabia accounted for the highest deployment concentration, with luxury dental centers expanding same-day veneer services and AI-assisted treatment planning capabilities. Cosmetic dentistry facility upgrades increased approximately 18% during 2025, supported by private healthcare investment and smart clinic development initiatives. African markets remained comparatively underpenetrated due to uneven specialist availability and limited digital laboratory infrastructure. Companies are focusing on strategic clinic partnerships, regional training programs, and high-value cosmetic treatment ecosystems to strengthen long-term deployment capacity across premium urban healthcare hubs.

United Arab Emirates Market Outlook: The United Arab Emirates emerged as the leading Middle East cosmetic dentistry hub through premium private healthcare infrastructure, international patient inflows, and rapid digital dentistry deployment. Nearly 49% of advanced cosmetic dental centers integrated chairside CAD/CAM systems by 2025 to support same-day veneer restoration services. Enterprise dental groups are investing heavily in luxury aesthetic treatment ecosystems, multilingual digital consultation platforms, and specialized cosmetic dentistry training to strengthen competitive positioning in the regional medical tourism market.

Dentsply Sirona, Ivoclar, 3M, Glidewell, and Ultradent Products compete directly across premium ceramic veneers, digital workflow systems, and cosmetic dentistry materials, while regional laboratories and low-cost ceramic suppliers challenge pricing and delivery speed in emerging markets. The top five players collectively account for nearly 41% of market concentration, driven by strong laboratory integration and advanced CAD/CAM compatibility.

Competition centers on procedural precision, customization speed, material durability, and digital workflow efficiency. AI-assisted smile-planning systems improved consultation efficiency by nearly 26%, while automated milling technologies reduced fabrication timelines by approximately 31% compared to conventional laboratory methods. Companies are strengthening competitiveness through localized ceramic production, vertically integrated milling operations, strategic scanner partnerships, and same-day veneer deployment models.

The competitive landscape is shifting toward digitally connected cosmetic dentistry ecosystems, with technology-led providers gaining advantage over conventional laboratories. Rising compliance costs, technician shortages, and advanced equipment investments continue creating high operational entry barriers. Long-term market leadership depends on scalable digital infrastructure, premium material innovation, and consistent multi-location procedural quality.

Dentsply Sirona

Ivoclar

3M

Glidewell

Ultradent Products

Kuraray Noritake Dental

Coltene Holding AG

VITA Zahnfabrik

Shofu Inc.

Planmeca Group

GC Corporation

Den-Mat Holdings

Henry Schein

Straumann Group

Digital dentistry platforms, intraoral scanners, and chairside CAD/CAM systems currently dominate veneer workflow modernization across premium cosmetic clinics. More than 58% of advanced dental centers integrated digital smile-design software during 2025, reducing consultation timelines by approximately 24% and lowering remake rates by nearly 18%. Compared with conventional laboratory impressions, AI-assisted digital scanning improved procedural precision by almost 31% while shortening veneer fabrication cycles from 7–10 days to under 48 hours. Large clinic networks in the United States and Germany are scaling cloud-connected treatment planning ecosystems to improve procedural consistency and multi-location workflow management.

Emerging technologies between 2026 and 2028 include ultra-thin nano-ceramic veneers, AI-guided shade matching, and automated robotic milling systems. High-translucency ceramic materials improved fracture resistance by approximately 16% while reducing enamel preparation requirements by nearly 35%. Around 41% of premium cosmetic dentistry providers in South Korea and Japan have started deploying integrated same-day veneer restoration platforms, strengthening patient retention and operational throughput. Dental laboratories are increasingly partnering with software providers to standardize design automation and reduce technician dependency.

Disruptive competitive advantage now centers on fully connected digital veneer ecosystems. Companies controlling scanner integration, ceramic production, and cloud-based workflow infrastructure are achieving approximately 22% faster treatment conversion rates and stronger procedural scalability. Early adopters of AI-driven cosmetic dentistry platforms are expected to secure premium patient concentration and operational efficiency advantages through 2028.

September 2025 – Dentsply Sirona unveiled an expanded AI-powered CEREC workflow with new CEREC Primemill Lite systems supporting single-visit dentistry. The integrated workflow reduced chairside restoration processing steps by approximately 30%, strengthening same-day veneer deployment efficiency across connected clinics and laboratories. Source: Dentsply Sirona

June 2025 – Dentsply Sirona launched the CEREC Cercon 4D Multidimensional Zirconia Abutment Block featuring advanced 3-dimensional layering technology for enhanced aesthetic restorations. The innovation improved translucency performance while maintaining high-strength ceramic durability, accelerating premium veneer customization capabilities for digital cosmetic dentistry providers. Source: FairsOnline

January 2026 – Patterson Dental and Dentsply Sirona renewed their U.S. dental technology distribution partnership to expand connected digital dentistry access nationwide. The collaboration strengthened integrated scanner and CAD/CAM deployment across regional clinics, supporting faster digital veneer workflow adoption and broader operational scalability within cosmetic dentistry networks.

May 2026 – Dentsply Sirona introduced Smart View-Detect, the first FDA-cleared AI-enabled CBCT diagnostic aid, delivering nearly 46% relative improvement in periapical radiolucency detection. The deployment enhanced digital treatment planning accuracy and improved cosmetic restoration diagnostics for advanced veneer and smile-design procedures.

The report delivers detailed strategic analysis of the global dental veneers market across material technologies, cosmetic dentistry applications, deployment models, and end-user ecosystems between 2026 and 2033. It evaluates operational trends across Porcelain Veneers, Composite Veneers, Lumineers, Temporary Veneers, and Removable Veneers while assessing adoption across smile makeover, alignment improvement, chipped tooth repair, and aesthetic restoration procedures. The study covers Dental Clinics, Cosmetic Dentistry Centers, Hospitals, Dental Laboratories, Academic Dental Institutes, and Specialty Dental Centers, with over 60% of assessed demand concentrated within digitally enabled cosmetic treatment networks.

The report further examines regional deployment dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting digital workflow penetration, laboratory modernization, and dental tourism expansion. It includes analysis of AI-assisted smile-design systems, CAD/CAM integration, ultra-thin ceramic materials, and same-day restoration technologies shaping procedural efficiency and competitive positioning. Strategic insights support expansion planning, partnership development, infrastructure investment, procurement optimization, and long-term cosmetic dentistry market positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1686.07 Million |

|

Market Revenue in 2033 |

USD 2687.34 Million |

|

CAGR (2026 - 2033) |

6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Dentsply Sirona, Ivoclar, 3M, Glidewell, Ultradent Products, Kuraray Noritake Dental, Coltene Holding AG, VITA Zahnfabrik, Shofu Inc., Planmeca Group, GC Corporation, Den-Mat Holdings, Henry Schein, Straumann Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |