Reports

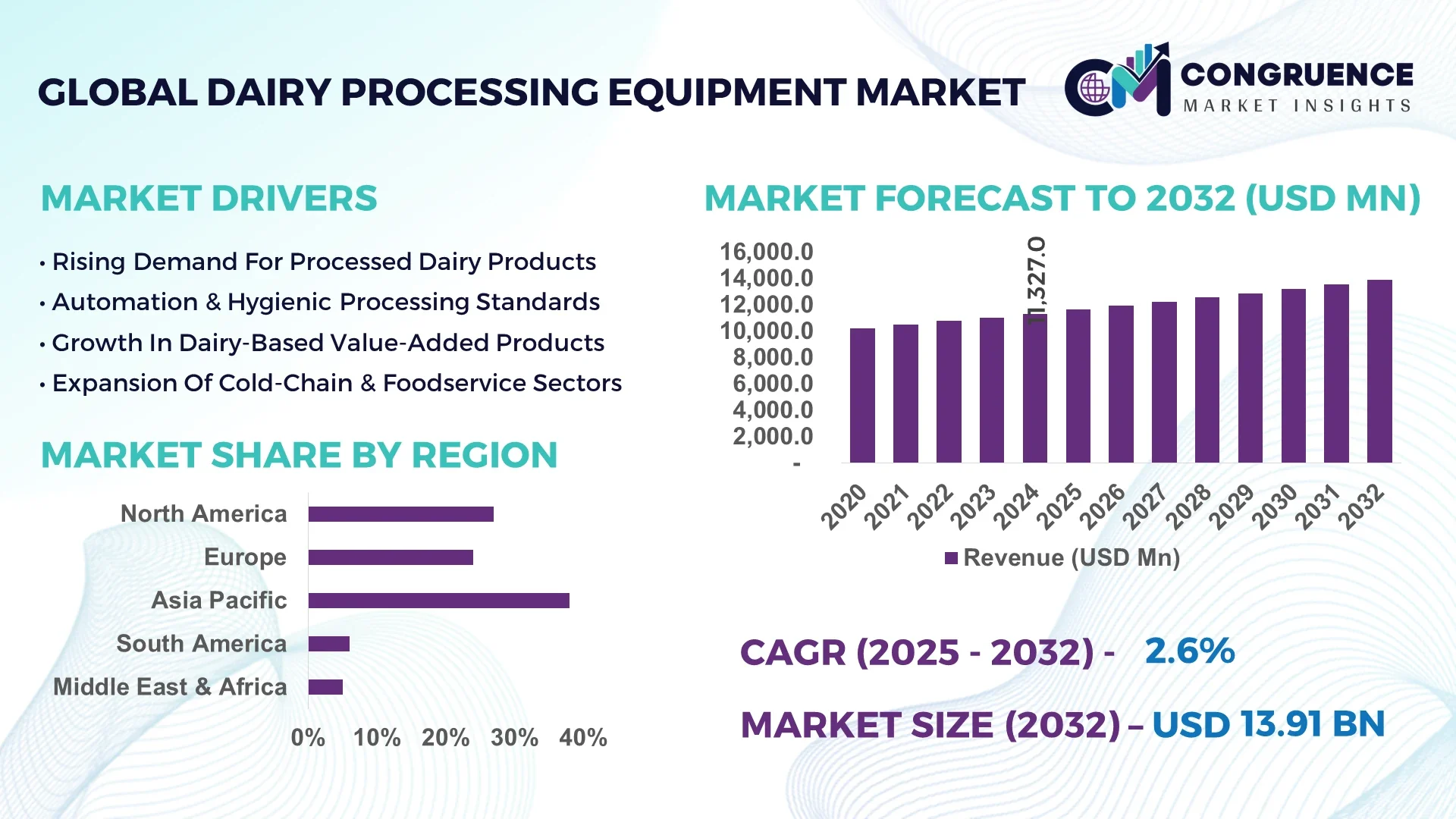

The Global Dairy Processing Equipment Market was valued at USD 11,327.04 Million in 2024 and is anticipated to reach a value of USD 13,908.98 Million by 2032 expanding at a CAGR of 2.6% between 2025 and 2032.

Germany exhibits robust strength in the Dairy Processing Equipment Market, with substantial capacity in stainless-steel processing machinery and emulsification systems, significant capital deployment into hygienic and modular processing lines, and advanced integration of CIP (clean-in-place) automation across key cheese and UHT milk applications.

Key industry sectors include milk pasteurization systems, membrane filtration units, cheese and yogurt processing machinery, and drying technologies for milk powder production. Recent innovations involve high-pressure homogenization, energy-efficient heat recovery systems, and hygienic self-cleaning modules designed to minimize downtime. Regulatory and environmental drivers like stringent food safety mandates, dairy effluent treatment guidelines, and incentives for energy-saving retrofits are influencing procurement decisions. Economically, rising disposable incomes and premium dairy consumption are accelerating upgrades across North American and APAC markets. Demand growth is especially strong in ready-to-drink and functional dairy drink segments, with increasing adoption of digital automation, IoT-enabled process controls, and traceability networks emerging as defining growth vectors.

Artificial Intelligence is reshaping the Dairy Processing Equipment Market through the deployment of advanced analytics and automation that drive precision, resilience, and performance. In the Dairy Processing Equipment Market, AI-powered predictive maintenance tools now monitor vibration, temperature, and acoustic signals on critical machinery—such as UHT cartons, separators, and homogenizers—identifying wear patterns and alerting operators weeks in advance, thereby reducing unexpected breakdowns and maintenance downtime by up to 15%. Smart process control systems use real-time data analytics within the Dairy Processing Equipment Market to fine-tune pasteurization curves and homogenization pressure settings, thereby standardizing product consistency and reducing wasted batches due to deviations.

Within the Dairy Processing Equipment Market, digital twin platforms are increasingly adopted for virtual simulation of processing lines and operator training, allowing safe trial of process tweaks without interrupting production. Machine vision combined with AI in the Dairy Processing Equipment Market enables high-speed inspection of product surfaces—detecting textural anomalies, foreign particulates, or fill-level deviations with over 95% accuracy, greatly reducing packaging rejects.

AI-driven supply chain orchestration tools in the Dairy Processing Equipment Market optimize raw milk scheduling through advanced demand forecasting, ensuring processing operations align closely with supply dynamics—this enhances throughput and minimizes spoilage. AI applications are now embedded across the Dairy Processing Equipment Market spectrum—from raw milk intake to packaging—improving efficiency, lowering costs, enhancing food safety, and supporting smarter operational strategies.

"In early 2025, an AI-powered computer vision system implemented in a European dairy facility achieved 96% accuracy in detecting packaging defects in real time, reducing rejection rates by 30% while processing over 50,000 units per day."

The Dairy Processing Equipment Market is experiencing a steady evolution driven by the convergence of automation, food safety compliance, and consumer demand for diversified dairy products. Key trends include the integration of energy-efficient designs, AI-enabled quality control, and modular processing units that enable rapid product line shifts. Regulatory pressures for hygienic design and traceability are prompting investments in advanced stainless-steel equipment and CIP (Clean-In-Place) systems. Growing consumption of value-added dairy products such as probiotic yogurts, lactose-free milk, and fortified cheese is influencing manufacturers to adopt flexible and high-capacity machinery. Additionally, technological advancements like membrane filtration, high-pressure processing, and robotics are enhancing operational precision while reducing downtime, positioning the market toward higher productivity and compliance readiness.

Stringent international and regional food safety regulations are a significant growth driver in the Dairy Processing Equipment Market. The introduction of advanced hygienic design standards and CIP (Clean-In-Place) systems has increased the adoption of automated cleaning technologies, reducing microbial risks and improving product shelf life. For instance, the use of seamless stainless-steel fabrication and non-porous contact surfaces ensures contamination control, aligning with global dairy hygiene benchmarks. Manufacturers are increasingly integrating inline monitoring sensors capable of detecting microbial activity in real time, reducing contamination incidents by up to 40%. These advancements not only protect consumer health but also enhance operational efficiency, as cleaning cycles are optimized and downtime is minimized, making equipment more productive and cost-effective.

While innovation is propelling growth, the Dairy Processing Equipment Market faces a notable restraint in the form of high upfront costs for advanced machinery. Automated high-pressure homogenizers, robotic milk processing lines, and energy-efficient pasteurizers require substantial initial investment, often exceeding the budgets of small and medium-sized dairy producers. The cost barrier is further compounded by the need for skilled operators and ongoing maintenance expenses, which can be significant for complex, sensor-integrated systems. Additionally, compliance with evolving food safety standards may necessitate frequent equipment upgrades, increasing financial strain. As a result, smaller processors may delay modernization or opt for refurbished equipment, limiting the market’s penetration in certain regions despite clear operational advantages.

The growing consumer preference for specialty dairy products presents a lucrative opportunity for the Dairy Processing Equipment Market. Demand for organic milk, probiotic yogurts, plant-protein-fortified dairy drinks, and artisanal cheeses is expanding globally, prompting dairy processors to invest in flexible, multi-function equipment capable of handling diverse formulations. The rise of lactose-free and nutrient-enriched dairy products has created demand for precision membrane filtration systems and specialized pasteurization units. Global dietary trends, particularly in urban markets, favor premium dairy options with enhanced nutritional profiles, creating long-term growth avenues for equipment suppliers. By offering customizable processing solutions, manufacturers can cater to niche segments and establish strong partnerships with premium dairy brands aiming to differentiate in competitive markets.

A key challenge in the Dairy Processing Equipment Market is the complexity of maintaining advanced, automated machinery while minimizing downtime. High-capacity pasteurizers, homogenizers, and robotic handling systems require specialized technical expertise for repairs and calibration. Any unplanned stoppage can disrupt the production chain, leading to product spoilage and revenue loss, particularly in continuous-flow dairy operations. Additionally, spare parts for sophisticated equipment may have long procurement lead times, further extending downtime. Compliance audits and hygiene inspections also add pressure to adhere to strict cleaning schedules, often requiring halts in production. Addressing this challenge necessitates robust maintenance strategies, skilled workforce training, and improved supply chain efficiency for spare components.

Rise in Modular and Prefabricated Equipment Installations: The growing use of modular and prefabricated construction is transforming infrastructure development for dairy plants. Equipment such as pre-assembled pasteurization units and skid-mounted homogenizers can be installed in less than half the time compared to traditional builds. Automated cutting and welding techniques used in off-site fabrication ensure millimeter-level precision, significantly reducing on-site labor requirements. This approach has seen accelerated adoption in Europe and North America, where construction efficiency and plant commissioning speed are critical for maintaining competitive production cycles.

Integration of IoT and Smart Sensors: Smart sensors and IoT-based monitoring systems are becoming standard in modern dairy facilities. These sensors track variables such as temperature, pH levels, and pressure in real time, with deviations triggering instant alerts. The adoption of such technology has been shown to reduce batch rejection rates by over 20% and extend equipment lifespan by enabling predictive maintenance. Real-time analytics from IoT platforms also help operators fine-tune production settings, optimizing energy and water consumption without compromising quality.

Adoption of Non-Thermal Processing Technologies: Non-thermal techniques, including high-pressure processing (HPP) and pulsed electric field (PEF) systems, are gaining traction for their ability to extend shelf life while retaining nutritional value. In large-scale milk processing lines, HPP can achieve microbial reduction comparable to pasteurization while consuming less energy. This trend is particularly relevant in premium dairy segments such as probiotic yogurt and specialty cheese, where preserving texture and flavor is critical to market differentiation.

Automation in Packaging and End-Line Operations: End-line automation, including robotic packing arms and automated sealing systems, is increasing operational throughput in dairy plants. High-speed robotic arms can package up to 120 units per minute with consistent accuracy, reducing labor dependency and packaging errors. This trend is driven by rising labor costs and growing demand for customizable packaging formats, particularly in single-serve dairy product categories such as flavored milk drinks and snack-sized cheese portions.

The Dairy Processing Equipment Market is segmented by type, application, and end-user, each influencing the industry’s growth trajectory. Types range from pasteurizers and homogenizers to separators, filtration systems, and evaporators, each serving a unique role in dairy production. Applications span fluid milk processing, cheese manufacturing, yogurt production, milk powder drying, and specialty dairy product lines. End-users include large-scale commercial dairy processors, medium-sized regional plants, and small-scale specialty producers. Pasteurizers dominate due to their universal necessity across product lines, while membrane filtration is gaining momentum for specialized processing. Fluid milk processing remains the most widespread application, but functional and value-added dairy products are accelerating equipment diversification. Large-scale industrial dairies lead end-user adoption, though artisanal and niche producers are increasingly investing in compact, automated systems to enhance output efficiency.

Pasteurizers remain the leading type within the Dairy Processing Equipment Market due to their universal role in ensuring product safety and extending shelf life. Modern pasteurizers integrate heat recovery systems to lower energy consumption, making them both economically and environmentally viable. Homogenizers follow closely, particularly in flavored milk and cream production, where uniform texture is crucial for consumer appeal. Membrane filtration systems, including microfiltration and ultrafiltration units, are the fastest-growing type, driven by rising demand for protein-enriched dairy beverages and lactose-free milk. Separators, vital for cream extraction and milk standardization, continue to see consistent demand in large-scale plants. Evaporators and dryers hold a niche but critical position in milk powder and whey protein production, especially for export-focused facilities. The trend toward multi-functional, modular units is enabling processors to adapt quickly to market changes while optimizing plant space and reducing operational costs.

Fluid milk processing leads the Dairy Processing Equipment Market as it is a core product category in both developed and developing nations, supported by consistent consumer demand for fresh and fortified milk. Cheese production ranks second, benefiting from increasing global consumption of specialty and artisanal cheeses, which require precise processing equipment for quality control. Yogurt manufacturing is the fastest-growing application, fueled by rising interest in probiotic-rich functional foods and plant-protein blends. Milk powder processing continues to be significant for export markets and emergency food supply chains, with high-capacity spray dryers being central to this segment. Specialty dairy products, including lactose-free milk and fortified beverages, are carving out a growing share, necessitating versatile processing systems capable of handling varied formulations. Equipment designed for flexibility and quick product changeovers is gaining traction, particularly among producers seeking to diversify offerings in competitive markets.

Large-scale industrial dairy processors dominate the Dairy Processing Equipment Market due to their expansive production capacities, ability to invest in cutting-edge equipment, and integration of end-to-end automation. These facilities often operate multiple processing lines simultaneously, catering to diverse dairy segments from milk to specialty cheese. Medium-sized regional processors hold a strong presence, particularly in emerging economies where they balance volume production with localized product variety. The fastest-growing end-user group is small-scale specialty dairy producers, driven by consumer interest in artisanal, organic, and niche dairy offerings. These producers are increasingly investing in compact, modular equipment that delivers high efficiency within limited space. Cooperative dairies also play an important role, especially in rural areas where shared processing resources help maximize output while reducing costs. Across all segments, the push toward automation, hygiene compliance, and flexible processing capability is influencing investment decisions, reshaping operational models throughout the industry.

Asia-Pacific accounted for the largest market share at 38% in 2024 however, South America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

The Dairy Processing Equipment Market in Asia-Pacific is driven by its robust manufacturing base, expanding urban consumption, and investment in high-capacity facilities across China, India, and Southeast Asia. Rising demand for value-added dairy products, integration of smart automation systems, and government-backed modernization programs have further solidified its position. In contrast, South America is experiencing rapid market expansion fueled by domestic dairy production growth, export-oriented investments, and increasing adoption of energy-efficient processing solutions to meet sustainability targets.

Advanced Automation and Sustainability Driving Dairy Innovations

Holding approximately 27% share of the Dairy Processing Equipment Market, the region benefits from a strong industrial base and high demand for premium dairy products. The market is heavily supported by the cheese and yogurt sectors, which drive consistent investment in automated pasteurization, homogenization, and packaging lines. Regulatory bodies have intensified hygiene and food safety standards, prompting widespread upgrades to CIP-enabled systems. Digital transformation is evident through IoT-connected processing lines, AI-based quality inspection, and predictive maintenance technologies that minimize downtime while maximizing output. Government support for sustainable manufacturing practices is also fostering the adoption of energy-efficient heat exchangers and low-waste processing systems.

Technological Precision and Sustainability at the Core of Dairy Processing

Accounting for around 24% of the Dairy Processing Equipment Market, the region is led by Germany, France, and the UK, where established dairy industries prioritize high standards of efficiency and product quality. EU food safety regulations and the Green Deal sustainability agenda are accelerating the adoption of eco-friendly and energy-saving technologies. Innovations such as high-pressure processing, modular production lines, and advanced membrane filtration systems are increasingly implemented to meet both environmental goals and evolving consumer preferences. Strong engineering expertise and the presence of leading equipment manufacturers make the region a hub for precision dairy technology development and export.

Scaling Production to Meet Rising Dairy Consumption

With the largest market volume in the Dairy Processing Equipment Market, countries such as China, India, and Japan lead in consumption and processing capacity. Expanding dairy farming operations, government-backed modernization programs, and investments in urban dairy infrastructure are driving rapid industrial scaling. Manufacturing hubs in China and India are producing both domestic-use and export-oriented equipment, reducing procurement costs for regional processors. Technological advancements such as automated milk testing systems, robotic packaging arms, and smart process controls are being deployed to improve efficiency and product safety, positioning the region as a global leader in production capabilities.

Emerging Export Hubs and Infrastructure Modernization Boosting Growth

Led by Brazil and Argentina, the Dairy Processing Equipment Market in the region accounts for about 6% of global share. Brazil’s large-scale dairy farms and Argentina’s specialty cheese production are fueling equipment demand, particularly in pasteurization and milk powder processing lines. Government incentives for agricultural modernization and trade agreements facilitating dairy exports are increasing investment in high-efficiency machinery. Upgrades in processing infrastructure, particularly in refrigeration and packaging, are helping local producers meet international quality standards and expand their market reach, while regional renewable energy adoption is reducing operational costs for processing facilities.

Modernization and Diversification Driving Dairy Equipment Demand

Representing approximately 5% of the Dairy Processing Equipment Market, this region’s growth is anchored by the UAE, Saudi Arabia, and South Africa. Rising consumer demand for fresh and long-life dairy products is prompting investments in advanced pasteurizers, separators, and automated filling lines. Governments are encouraging domestic production through agricultural subsidies and public-private partnerships. Technological modernization, such as IoT-enabled monitoring and precision filling equipment, is increasingly used to improve output consistency and hygiene standards. Expanding cold chain infrastructure and trade partnerships with major dairy exporters are further supporting market development across the region.

China – 21%

High production capacity combined with rapid adoption of automated dairy processing lines supports its leadership in the Dairy Processing Equipment Market.

United States – 18%

Strong demand for premium and specialty dairy products drives continuous investment in advanced processing technologies and automation within the Dairy Processing Equipment Market.

The Dairy Processing Equipment Market is characterized by intense competition among approximately 30–35 globally active manufacturers, alongside a significant number of regional and specialized players. The competitive environment is shaped by technological innovation, product diversification, and the ability to meet evolving regulatory and sustainability requirements. Leading companies are focusing on integrating automation, IoT-enabled monitoring, and energy-efficient solutions to differentiate themselves in a saturated market. Strategic initiatives such as partnerships with dairy cooperatives, acquisitions to expand regional footprints, and joint ventures for technology development are increasingly common. Product launches featuring modular designs, improved CIP systems, and advanced filtration technologies are driving competitive advantages. Innovation trends are heavily influenced by demand for high-capacity, multi-functional equipment capable of processing diverse dairy products while minimizing operational costs. Companies with strong after-sales service networks, customization capabilities, and adherence to global food safety standards hold a competitive edge in securing long-term client relationships and global market positioning.

GEA Group AG

Tetra Pak International S.A.

SPX FLOW, Inc.

Alfa Laval AB

Krones AG

Paul Mueller Company

Feldmeier Equipment, Inc.

JBT Corporation

Scherjon Dairy Equipment Holland B.V.

IDMC Limited

The Dairy Processing Equipment market is witnessing significant technological evolution, driven by automation, digitalization, and sustainable engineering. Modern processing plants are increasingly integrating advanced automation systems, such as programmable logic controllers (PLCs) and supervisory control and data acquisition (SCADA), to enhance operational efficiency, reduce downtime, and ensure consistent product quality. Sensor-based monitoring technologies enable real-time tracking of parameters like temperature, pH, and viscosity, which are critical in dairy processing. The adoption of membrane filtration systems, including ultrafiltration and reverse osmosis, is improving protein separation and water recovery rates, supporting cost efficiency and sustainability goals.

Emerging innovations include energy-efficient pasteurization techniques such as regenerative heat exchange, which significantly lowers energy consumption. Robotics is playing a growing role in packaging, palletizing, and cleaning processes, improving hygiene standards and reducing labor dependency. Furthermore, Internet of Things (IoT) connectivity allows predictive maintenance, minimizing equipment failures and optimizing productivity. Manufacturers are also investing in 3D printing for rapid prototyping of machine components, reducing lead times for replacement parts.

Sustainability is shaping technology adoption, with equipment designed for water reuse, reduced chemical consumption in Cleaning-in-Place (CIP) systems, and lower carbon footprints. Digital twins are enabling virtual simulations of processing lines, allowing faster commissioning and process optimization. These advancements collectively enhance productivity, product safety, and regulatory compliance, ensuring competitive advantage in a rapidly evolving dairy sector.

In January 2024, GEA Group introduced its latest continuous butter making machine, featuring enhanced energy efficiency and improved churning control for higher product consistency in large-scale dairy production.

In September 2023, Tetra Pak launched its new high-shear mixer designed to handle a wider variety of dairy formulations, offering faster mixing times and reduced waste in processing operations.

In June 2024, SPX FLOW announced the development of a modular membrane filtration system capable of higher throughput while reducing water consumption by up to 25%, targeting sustainability-conscious dairy processors.

In March 2023, Alfa Laval unveiled an advanced plate heat exchanger model optimized for dairy pasteurization, delivering improved thermal efficiency and simplified maintenance compared to conventional designs.

The Dairy Processing Equipment Market Report provides a comprehensive analysis of the industry’s structure, trends, and growth potential across multiple dimensions. It covers a broad range of equipment categories, including pasteurizers, homogenizers, separators, evaporators, dryers, membrane filtration units, and packaging systems, along with their technological advancements and market adoption patterns. The geographic scope spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering region-specific insights into demand dynamics, production capacities, and regulatory frameworks.

The report further segments the market by application areas such as milk processing, cheese production, yogurt and cultured dairy products, butter and cream manufacturing, and milk powder production. Industry focus areas include efficiency enhancement, sustainability integration, and digital transformation, with special attention to automation, IoT-enabled equipment, and energy-efficient processing technologies.

In addition, the study examines end-user industries ranging from large-scale industrial dairy plants to small and medium-sized processing units, identifying opportunities in both established and emerging markets. The analysis highlights innovation trends, competitive strategies, and niche market opportunities such as plant-based dairy alternatives, which are increasingly utilizing similar processing equipment. The scope ensures a complete, business-relevant perspective for stakeholders aiming to understand both current market realities and future opportunities in the dairy processing sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 11,327.04 Million |

|

Market Revenue in 2032 |

USD 13,908.98 Million |

|

CAGR (2025 - 2032) |

2.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

GEA Group AG, Tetra Pak International S.A., SPX FLOW, Inc., Alfa Laval AB, Krones AG, Paul Mueller Company, Feldmeier Equipment, Inc., JBT Corporation, Scherjon Dairy Equipment Holland B.V., IDMC Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |