Reports

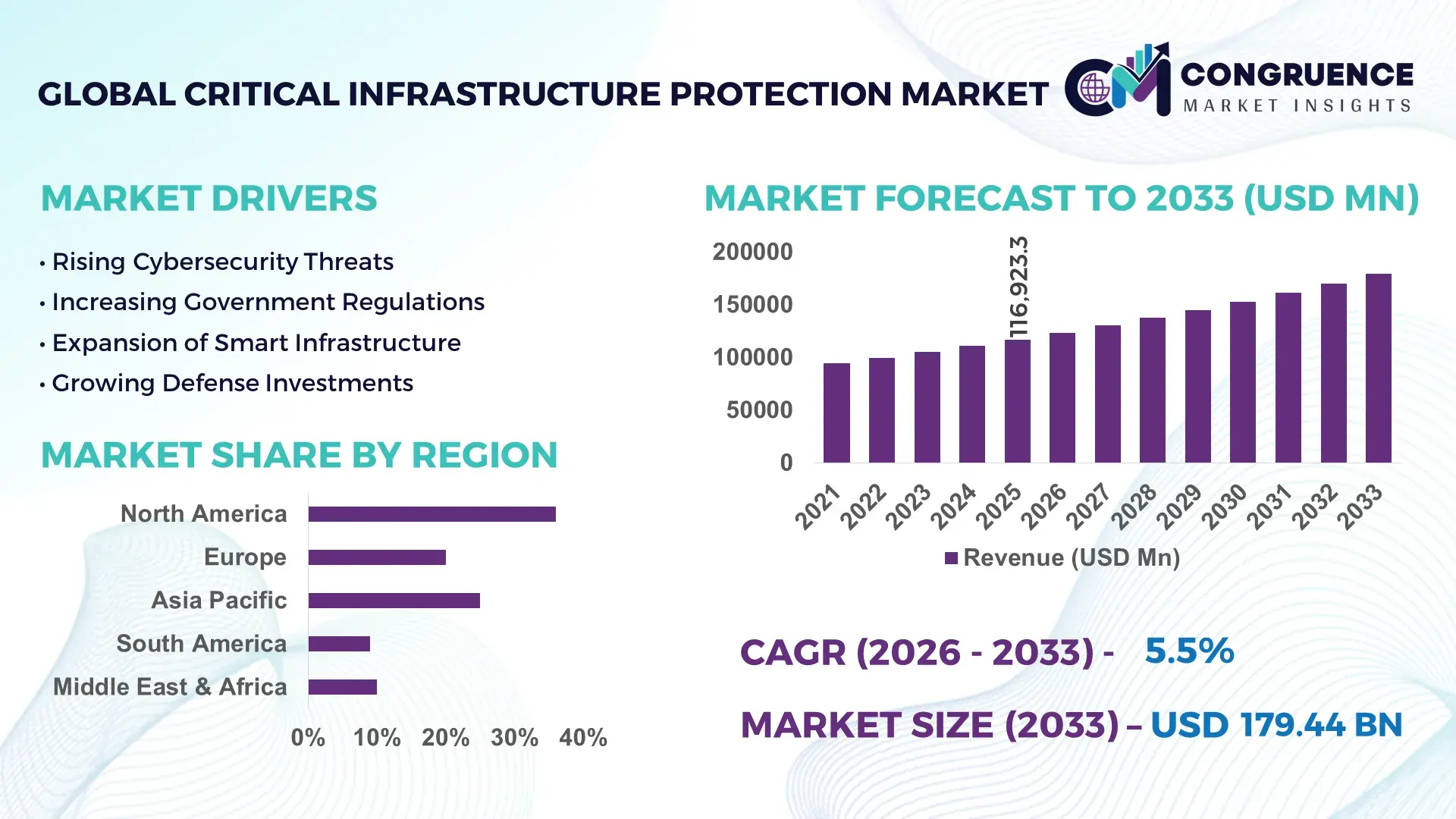

The Global Critical Infrastructure Protection Market was valued at USD 116923.27 Million in 2025 and is anticipated to reach a value of USD 179440.57 Million by 2033 expanding at a CAGR of 5.5% between 2026 and 2033. Rapid integration of AI-enabled threat detection, industrial cybersecurity platforms, and advanced surveillance infrastructure is accelerating deployment across energy grids, transportation hubs, defense networks, and smart utility systems, with predictive monitoring reducing operational disruption rates by nearly 28% in high-risk facilities.

The United States dominates the global critical infrastructure protection landscape with approximately 34% market share, supported by over USD 25 billion in federal resilience modernization programs and extensive deployment across defense, oil & gas, utilities, and transportation sectors. More than 72% of large-scale energy operators in the country integrated AI-driven security analytics and industrial control system monitoring by 2026, compared with under 46% adoption across several emerging economies. Investments in grid modernization, airport surveillance automation, and cyber-physical protection systems continue to outpace regional competitors, while Europe prioritizes regulatory compliance and Asia-Pacific focuses on smart city-linked infrastructure resilience initiatives.

Organizations prioritizing integrated cyber-physical protection architectures and real-time operational intelligence are positioned to achieve stronger asset continuity, lower incident recovery costs, and long-term infrastructure resilience advantages.

Market Size & Growth: USD 116923.27 million in 2025 rising to USD 179440.57 million by 2033 at 5.5% CAGR, driven by AI-based infrastructure security modernization and grid resilience investments.

Top Growth Drivers: Cyberattack incidents increased 31%, smart utility deployment expanded 24%, and industrial IoT integration crossed 40% across critical sectors.

Short-Term Forecast: By 2027, predictive infrastructure monitoring reduces downtime by 26% while automated threat response lowers incident recovery costs by 18%.

Emerging Technologies: AI surveillance, digital twin infrastructure modeling, and edge-based industrial cybersecurity improve threat detection accuracy by over 35%.

Regional Leaders: North America exceeds USD 58 billion with defense-led adoption, Europe crosses USD 42 billion through compliance upgrades, and Asia-Pacific expands beyond USD 39 billion via smart city expansion.

Consumer/End-User Trends: Over 68% of utilities and transport operators prioritize integrated cyber-physical security platforms over standalone monitoring systems.

Pilot/Case Example: In 2025, a large-scale smart grid modernization project improved outage response efficiency by 33% through AI-enabled infrastructure analytics.

Competitive Landscape: Leading firms collectively control nearly 38% share, with strong competition among integrated cybersecurity, defense technology, and industrial automation providers.

Regulatory & ESG Impact: Infrastructure resilience mandates improved compliance investments by 29%, while energy-efficient monitoring systems reduced facility power usage by 14%.

Investment & Funding: Global investments surpassed USD 32 billion between 2024 and 2026, fueled by strategic partnerships, defense modernization, and regional infrastructure expansion.

Innovation & Future Outlook: Autonomous security orchestration, quantum-resistant encryption, and unified operational intelligence platforms are reshaping next-generation critical infrastructure resilience strategies.

Energy and utilities contribute nearly 36% of global critical infrastructure protection deployments, followed by transportation and logistics at 24% and defense-related infrastructure at 19%, reflecting heightened focus on operational continuity and cyber resilience. Advanced AI surveillance systems, industrial digital twins, and real-time SCADA security platforms improved threat response efficiency by over 30% across high-risk facilities in 2026. North America maintains the strongest deployment intensity, while Asia-Pacific recorded more than 27% growth in smart infrastructure security integration due to rapid urban infrastructure expansion and manufacturing digitization. Regulatory tightening around national cyber resilience frameworks and supply chain security validation is accelerating adoption of integrated protection ecosystems. The market is steadily shifting toward predictive, autonomous, and fully converged cyber-physical infrastructure defense strategies.

Critical infrastructure protection is rapidly transforming from a compliance-focused function into a strategic investment priority as governments, utilities, transportation operators, and industrial enterprises confront escalating cyber-physical threats targeting national assets. Accelerating digitalization of energy grids, industrial automation systems, and smart transportation corridors is forcing organizations to optimize resilience spending and operational continuity frameworks simultaneously. Regulatory tightening across North America, Europe, and Asia after repeated ransomware attacks on utilities and logistics networks is shifting procurement toward integrated protection ecosystems combining AI surveillance, industrial cybersecurity, and predictive analytics. AI-enabled threat intelligence platforms improve detection efficiency by 41% while reducing operational response costs by 24% compared to legacy rule-based monitoring systems.

North America leads in deployment volume due to large-scale defense and grid modernization programs, while Asia-Pacific leads in infrastructure innovation adoption with over 38% growth in smart city-linked security integration. Within the next two to three years, automated infrastructure monitoring systems are projected to reduce critical outage durations by 27% and improve asset recovery efficiency by 31%. ESG-linked infrastructure resilience programs are also becoming competitive differentiators, with energy-efficient monitoring architectures lowering operational power consumption by nearly 16% across advanced utility facilities.

In 2025, a major European rail infrastructure modernization initiative integrated AI-powered perimeter security and predictive threat analytics, improving incident response time by 34% while lowering false-alert volumes by 29%. Large technology integrators and industrial cybersecurity firms are aggressively shifting capital allocation toward unified cyber-physical protection platforms, edge intelligence, and sovereign infrastructure security partnerships. Organizations prioritizing scalable, interoperable, and intelligence-driven protection frameworks are securing stronger operational resilience, faster compliance alignment, and long-term competitive positioning across critical national infrastructure ecosystems.

Escalating attacks on energy grids, transport systems, and industrial networks are accelerating demand for integrated critical infrastructure protection solutions across public and private sectors. More than 68% of utility operators increased cybersecurity and physical surveillance budgets in 2025, while industrial ransomware incidents targeting operational technology environments surged by 32%. Supply chain restructuring after Red Sea logistics disruptions and regional geopolitical conflicts forced governments to prioritize resilient infrastructure modernization programs. This pressure is driving rapid adoption of AI-enabled monitoring systems that improve threat detection accuracy by 37% and reduce operational downtime significantly. In response, leading companies are accelerating strategic partnerships, expanding security operations centers, and increasing investment in predictive infrastructure analytics to strengthen resilience and secure long-term infrastructure continuity.

High implementation costs and fragmented legacy infrastructure systems are constraining large-scale deployment of advanced critical infrastructure protection platforms. Nearly 44% of infrastructure operators still rely on outdated operational technology environments incompatible with modern AI-driven security architectures, increasing integration complexity and deployment delays. Hardware component inflation and semiconductor supply concentration in East Asia increased advanced surveillance and industrial cybersecurity equipment costs by approximately 18% between 2024 and 2026. Regulatory fragmentation across regions is also extending certification and compliance timelines for multinational operators. These constraints directly impact scalability, capital allocation efficiency, and project execution speed. To mitigate risks, companies are diversifying supplier networks, adopting modular security architectures, and negotiating long-term procurement agreements while accelerating transition toward cloud-based and edge-enabled protection ecosystems.

Next-generation AI-driven infrastructure resilience platforms are redefining growth opportunities across energy, transportation, water management, and smart city ecosystems. Automated predictive maintenance systems reduce infrastructure failure rates by nearly 29%, while digital twin-enabled monitoring improves operational planning efficiency by 33%. Emerging economies across Southeast Asia and the Middle East are increasing national infrastructure security spending by over 26% as urban digitization and industrial automation accelerate. A major innovation shift toward autonomous cyber-physical orchestration platforms is creating new demand for integrated analytics, edge computing, and real-time threat intelligence solutions. Companies are responding through aggressive R&D expansion, sovereign infrastructure partnerships, and ecosystem-based service models designed to secure long-term recurring revenue, strengthen operational interoperability, and establish strategic dominance across high-growth infrastructure security markets.

Rapid infrastructure digitization is exposing operational vulnerabilities that existing protection frameworks struggle to manage at scale. More than 47% of critical infrastructure operators report workforce shortages in industrial cybersecurity and AI-enabled threat management, limiting deployment efficiency and increasing response delays. Aging grid infrastructure across developed economies is creating performance bottlenecks, while integration failures between IT and operational technology systems increase incident recovery times by approximately 21%. Rising energy consumption from high-density monitoring networks and data-intensive analytics platforms is also placing pressure on sustainability targets and operating costs. To remain competitive, companies must accelerate workforce training, strengthen cross-industry technology partnerships, modernize interoperability standards, and invest aggressively in scalable low-power security architectures capable of supporting continuously expanding infrastructure ecosystems.

AI-driven monitoring adoption increased 39% across utilities and transport infrastructure in 2026, reshaping operational security execution. Infrastructure operators are replacing fragmented monitoring tools with unified AI-enabled command platforms capable of reducing false-positive alerts by 31% and improving response coordination speed by 28%. Companies are scaling edge analytics deployment and restructuring security operations around centralized threat visibility to optimize asset continuity amid rising cross-border cyber risks.

Cloud-integrated industrial security deployments expanded 34%, forcing major operators to redesign legacy protection frameworks. Energy and telecom providers are shifting from hardware-centric systems toward hybrid cloud and edge-enabled architectures, reducing infrastructure maintenance costs by nearly 22%. Labor shortages in industrial cybersecurity are accelerating managed security partnerships and automated workflow adoption, while vendors are prioritizing interoperable platforms to capture multi-site infrastructure modernization contracts.

Asia-Pacific smart infrastructure protection projects surged 36%, redefining regional deployment intensity and vendor expansion models. Governments and infrastructure developers are integrating surveillance automation, biometric access systems, and predictive monitoring into transportation corridors and urban utility networks. In contrast, Europe is prioritizing compliance-driven cybersecurity integration following stricter infrastructure resilience mandates, forcing providers to accelerate localized partnerships and sovereign data protection capabilities.

Subscription-based infrastructure protection services increased 27%, shifting the market from equipment ownership toward recurring operational models. Critical infrastructure operators are prioritizing scalable protection ecosystems with continuous monitoring, real-time analytics, and remote incident management capabilities. This transition is improving deployment flexibility by 24% while reducing upfront capital exposure. Companies are responding through platform consolidation, bundled service contracts, and cybersecurity-as-a-service expansion to strengthen long-term client retention and operational scalability.

The critical infrastructure protection market is segmented by type, application, and end-user, with cybersecurity solutions and threat detection platforms capturing the largest demand concentration due to rising cyber-physical attack exposure across utilities and transport networks. Government and energy sectors collectively account for over 48% of deployment activity because of high operational dependency and regulatory pressure. Demand is rapidly shifting toward AI-enabled infrastructure monitoring and incident management systems, which improved response efficiency by nearly 30% in large-scale facilities during 2026. Companies are prioritizing integrated protection ecosystems combining surveillance, access control, and network security to optimize resilience, reduce operational disruption, and strengthen long-term infrastructure continuity across high-risk industries.

Cybersecurity Solutions dominate the critical infrastructure protection market with approximately 32% share, driven by escalating ransomware attacks, operational technology vulnerabilities, and expanding regulatory mandates across utilities, transportation, and government networks. Their structural dominance comes from centralized threat visibility, scalable deployment capability, and strong integration with industrial control systems. Network Security is emerging as the fastest-growing segment, expanding by nearly 29% due to increasing adoption of edge computing, cloud-connected infrastructure, and real-time threat analytics. Compared with traditional Physical Security Systems, advanced Network Security platforms improve response efficiency by 34% while reducing manual monitoring dependency significantly. Surveillance Systems and Access Control Systems collectively account for nearly 38% share, maintaining strategic relevance in airports, defense infrastructure, logistics hubs, and smart city projects where biometric authentication and AI-enabled monitoring are accelerating. Companies are shifting investment toward integrated cyber-physical protection architectures, expanding AI-enabled security portfolios, and accelerating interoperability-focused innovation. Demand is steadily moving away from standalone hardware-heavy systems toward software-centric intelligent security ecosystems with predictive operational capabilities.

“According to a 2025 report by the International Society of Automation, cybersecurity solutions were adopted by over 71% of industrial infrastructure operators, resulting in a 33% improvement in threat response efficiency, reinforcing their growing strategic importance.”

Threat Detection leads the critical infrastructure protection market with nearly 28% share because infrastructure operators prioritize real-time visibility against increasingly sophisticated cyber-physical attacks. High deployment concentration exists across utilities, transportation networks, and defense-linked systems where rapid anomaly identification directly impacts operational continuity. Infrastructure Monitoring is the fastest-growing application, expanding by approximately 31% as AI-driven predictive analytics and digital twin technologies redefine asset management efficiency. Compared with mature Risk Management systems focused primarily on compliance and assessment workflows, advanced Infrastructure Monitoring platforms improve operational uptime by 27% and reduce unplanned maintenance disruptions substantially. Emergency Response, Data Protection, and Incident Management collectively represent around 46% of market deployment, supported by rising demand for coordinated crisis response and secure data orchestration. Companies are accelerating deployment of unified command centers, automating incident workflows, and repositioning product portfolios around predictive intelligence capabilities. Demand is clearly shifting toward continuously monitored, analytics-driven protection environments that combine operational resilience with faster recovery execution across critical infrastructure ecosystems.

“According to a 2025 report by the National Institute of Standards and Technology, threat detection platforms were deployed across over 4,500 critical infrastructure organizations, improving detection accuracy by 36%, highlighting their rapid operational adoption.”

Government remains the leading end-user segment with approximately 30% share due to national security mandates, large-scale infrastructure ownership, and continuous investment in defense-grade cyber-physical resilience systems. Demand concentration is strongest in border security, transportation networks, and public utility protection where operational continuity carries strategic national importance. Energy and Utilities is the fastest-growing end-user category, expanding by nearly 32% as smart grid deployment, renewable integration, and industrial automation increase exposure to cyber and operational threats. Compared with the established Government segment, Healthcare and IT and Telecom are demonstrating more agile adoption behavior through cloud-native monitoring and AI-enabled threat management integration. Transportation, BFSI, Healthcare, and IT and Telecom collectively account for roughly 52% of deployment activity, driven by rising digital dependency and stricter infrastructure resilience requirements. Companies are responding through industry-specific platform customization, subscription-based pricing models, and strategic partnerships with infrastructure operators. Future demand is shifting toward sectors managing high-volume real-time data environments and distributed operational ecosystems requiring continuous infrastructure visibility.

“According to a 2025 report by the International Energy Agency, adoption among energy and utilities operators increased by 35%, with over 3,200 organizations implementing AI-enabled infrastructure protection systems, leading to a 26% improvement in operational efficiency, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America maintains demand concentration through extensive deployment across defense infrastructure, smart utilities, and transportation security networks, while Europe accounts for nearly 27% share driven by regulatory-led modernization and cyber resilience mandates. Asia-Pacific holds approximately 29% market share and is accelerating rapidly due to smart city expansion, industrial automation, and large-scale digital infrastructure deployment across China, India, Japan, and Southeast Asia. Europe leads in compliance-driven innovation with over 42% adoption of integrated cyber-physical monitoring platforms, while Asia-Pacific leads in deployment scale and infrastructure expansion speed. Ongoing geopolitical tensions and supply chain restructuring are forcing governments to localize infrastructure resilience investments. Global companies are increasingly prioritizing Asia-Pacific expansion while strengthening high-value cybersecurity partnerships across North America and Europe.

North America controls nearly 36% of global critical infrastructure protection demand, supported by large-scale deployment across defense, energy grids, airports, and telecom infrastructure. Utilities and transportation operators are aggressively adopting AI-enabled threat analytics and industrial cybersecurity platforms, with more than 69% of major infrastructure operators integrating predictive monitoring systems by 2026. Federal resilience mandates and rising ransomware attacks targeting operational technology environments are reshaping procurement priorities across the region. Infrastructure modernization programs improved incident response efficiency by approximately 32%, while cloud-integrated monitoring reduced operational downtime significantly. Enterprises increasingly prefer interoperable cyber-physical protection ecosystems over fragmented legacy systems, accelerating long-term vendor partnerships and managed security adoption. Companies continue prioritizing this region because of regulatory intensity, large-scale modernization budgets, and high-value infrastructure protection demand.

Europe represents approximately 27% of the global critical infrastructure protection market, with strong demand concentrated in Germany, France, and the United Kingdom due to advanced industrial infrastructure and strict cyber resilience regulations. Sustainability-focused modernization and compliance with infrastructure security directives are accelerating adoption of energy-efficient monitoring systems and AI-enabled threat detection platforms. More than 44% of infrastructure operators across the region integrated unified cyber-physical protection frameworks by 2026 to improve operational continuity and regulatory alignment. Enterprises are prioritizing high-reliability, compliance-driven security architectures over low-cost standalone systems, particularly across transportation and energy sectors. Regional governments also expanded critical infrastructure digitalization programs by nearly 24%, strengthening demand for predictive monitoring technologies. Companies targeting Europe must prioritize regulatory adaptability, interoperability, and sustainability-focused innovation to remain competitive.

Asia-Pacific ranks as the fastest-expanding regional market, accounting for nearly 29% of global deployment activity driven by rapid infrastructure digitization across China, India, Japan, and Southeast Asia. Smart city investments, industrial automation growth, and large-scale transportation modernization are accelerating demand for integrated cyber-physical protection systems. More than 38% of new infrastructure projects launched in 2026 incorporated AI-enabled surveillance and predictive monitoring capabilities from initial deployment stages. Regional operators prioritize deployment speed, scalable architectures, and cost-efficient integrated platforms to support expanding urban infrastructure networks. Governments and private enterprises are also increasing localized production and infrastructure security partnerships to reduce import dependency and improve operational resilience. Global vendors continue prioritizing Asia-Pacific because of unmatched deployment scale, fast digital transformation cycles, and accelerating infrastructure modernization investments.

South America contributes nearly 6% of global critical infrastructure protection demand, with Brazil and Argentina leading deployment activity across energy, transportation, and public utility networks. Rising cyber risks targeting industrial operations and grid infrastructure are increasing demand for centralized monitoring and incident management systems. However, infrastructure modernization remains constrained by budget limitations, import dependency, and uneven regulatory frameworks across regional economies. Approximately 34% of large utility operators accelerated phased cybersecurity upgrades in 2026, focusing on cost-efficient cloud-based protection platforms instead of full-scale infrastructure replacement. Enterprises demonstrate strong price sensitivity and prefer modular solutions capable of scaling gradually with operational requirements. Technology providers view the region as a strategic long-term expansion opportunity but must balance affordability, localized service support, and infrastructure adaptation to capture sustainable market penetration.

Middle East & Africa account for approximately 8% of the global critical infrastructure protection market, supported by large-scale infrastructure modernization across the UAE, Saudi Arabia, and South Africa. Oil and gas facilities, smart city projects, airports, and utility networks are driving strong demand for integrated surveillance, access control, and industrial cybersecurity systems. National transformation programs increased infrastructure security investment intensity by nearly 28% between 2024 and 2026, accelerating deployment of AI-enabled monitoring platforms and predictive operational analytics. Enterprises increasingly prioritize centralized command systems capable of supporting high-value critical assets and cross-border infrastructure operations. Governments are also expanding partnerships with global cybersecurity and defense technology firms to strengthen sovereign infrastructure resilience capabilities. Companies are targeting this region because of aggressive modernization agendas, infrastructure diversification programs, and rising strategic security investments.

United States Critical Infrastructure Protection Market – 34% share: Dominates through large-scale defense modernization, advanced utility infrastructure, and extensive adoption of AI-driven cyber-physical security systems.

China Critical Infrastructure Protection Market – 21% share: Leads through rapid smart city deployment, industrial automation expansion, and strong government-backed infrastructure resilience investments.

The critical infrastructure protection market is dominated by global cybersecurity leaders, industrial automation providers, defense technology firms, and integrated surveillance specialists competing aggressively across utilities, transportation, defense, and telecom sectors. Companies such as Honeywell, Siemens, Cisco Systems, Johnson Controls, and Thales collectively control nearly 41% market share, competing against regional infrastructure security integrators focused on cost optimization and localized deployment. Competition is increasingly centered on AI-enabled threat analytics, interoperability, deployment speed, and predictive operational intelligence, with integrated platforms improving response efficiency by 34% and reducing downtime by 26% compared with fragmented legacy systems. Major players are accelerating cloud-security partnerships, expanding sovereign cybersecurity operations, and vertically integrating monitoring capabilities to strengthen recurring service revenue. Rapid digital infrastructure expansion is also triggering consolidation across industrial cybersecurity and surveillance segments. High regulatory compliance costs, operational technology integration complexity, and long-term infrastructure contracts continue to create strong entry barriers. Winning requires scalable cyber-physical ecosystems, localized execution capability, and continuous innovation.

Honeywell International Inc.

Siemens AG

Cisco Systems Inc.

Johnson Controls International plc

Thales Group

Raytheon Technologies Corporation

Lockheed Martin Corporation

BAE Systems plc

ABB Ltd.

Schneider Electric SE

Huawei Technologies Co. Ltd.

IBM Corporation

General Dynamics Corporation

Northrop Grumman Corporation

AI-enabled threat intelligence, industrial cybersecurity orchestration, and predictive infrastructure monitoring are becoming the operational core of critical infrastructure protection deployments. By 2026, over 67% of large utility and transportation operators integrated AI-driven anomaly detection systems capable of improving incident response accuracy by 38% while reducing manual monitoring dependency by 24%. Unified cyber-physical command platforms are also optimizing operational continuity by integrating surveillance, access control, and network analytics into centralized ecosystems. Compared with legacy rule-based monitoring systems, AI-native protection architectures improve detection speed by 41% and lower response costs by nearly 22%, creating strong competitive advantages for large-scale infrastructure operators.

Edge computing, digital twin infrastructure modeling, and autonomous incident management platforms are emerging as high-impact technologies reshaping execution-level infrastructure security. More than 43% of newly deployed smart infrastructure projects in 2026 incorporated edge-enabled monitoring to reduce latency and improve localized threat response efficiency. Industrial digital twins are reducing predictive maintenance errors by approximately 29%, while automated orchestration platforms are shortening recovery timelines by 31%. Companies are aggressively expanding cloud-edge integration partnerships and restructuring security operations around real-time operational intelligence frameworks.

Between 2026 and 2028, quantum-resistant encryption, autonomous AI agents, and self-healing infrastructure networks are expected to redefine resilience execution across energy grids, airports, and telecom ecosystems. Technology providers specializing in interoperable AI-security ecosystems and low-power monitoring architectures are positioned to capture strategic advantage as governments accelerate sovereign infrastructure modernization programs. Organizations delaying migration from fragmented legacy infrastructure face rising operational risk, slower compliance execution, and increasing vulnerability exposure across continuously digitizing critical infrastructure networks.

April 2026 – Siemens AG launched a Managed Detection and Response service for critical infrastructure operators, enabling 24/7 OT cybersecurity monitoring across energy, airport, and industrial networks. The platform reduced capital expenditure by up to 80% and lowered cyber defense operating costs by nearly 50%, accelerating infrastructure resilience deployment. [OT Defense Shift] Source: Siemens Press Release

June 2024 – Cisco Systems Inc. introduced AI-powered infrastructure security and observability solutions integrated with its networking cloud architecture, improving enterprise-wide visibility and automated threat response capabilities. The company simultaneously launched a USD 1 billion AI investment initiative to strengthen secure infrastructure innovation and hyperscale resilience deployment. [AI Infrastructure Push] Source: Cisco Newsroom

April 2024 – Cisco Systems Inc. unveiled Cisco Hypershield, an AI-native distributed security architecture designed for cloud, industrial, and data center infrastructure environments. The solution enabled autonomous network segmentation and near-instant exploit protection while reducing downtime exposure across highly distributed infrastructure ecosystems. [Distributed Security Layer] Source: Cisco Security Announcement

May 2026 – Cisco Systems Inc. accelerated restructuring toward AI-focused infrastructure security, reallocating investments into cybersecurity, silicon, optics, and AI networking after hyperscaler AI infrastructure orders exceeded USD 5.3 billion. Data-center switching orders increased more than 40%, strengthening next-generation infrastructure protection and resilience capabilities. [Infrastructure Realignment] Source: Reuters Technology Update

This report delivers comprehensive analysis of the critical infrastructure protection market across key technology categories including cybersecurity solutions, surveillance systems, access control platforms, industrial network security, and AI-enabled infrastructure monitoring. The study evaluates major applications such as threat detection, incident management, emergency response, infrastructure monitoring, and data protection across government, energy and utilities, transportation, BFSI, healthcare, and IT and telecom sectors. Regional coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed assessment of deployment intensity, operational modernization trends, and infrastructure resilience priorities.

The report analyzes more than 25 strategic market indicators including technology adoption rates, operational efficiency improvements, deployment concentration, and end-user demand distribution. Over 67% of large infrastructure operators are shifting toward integrated cyber-physical security architectures, while AI-enabled monitoring adoption exceeded 40% across smart infrastructure projects in 2026. The scope also includes emerging technologies such as digital twins, edge intelligence, autonomous incident response, and quantum-resistant security frameworks expected to influence infrastructure resilience execution between 2026 and 2033.

The report supports strategic decision-making through detailed competitive benchmarking, regional investment analysis, operational deployment trends, and technology positioning insights, enabling organizations to optimize expansion strategies, infrastructure modernization priorities, and long-term resilience investments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 116923.27 Million |

|

Market Revenue in 2033 |

USD 179440.57 Million |

|

CAGR (2026 - 2033) |

5.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Honeywell International Inc., Siemens AG, Cisco Systems Inc., Johnson Controls International plc, Thales Group, Raytheon Technologies Corporation, Lockheed Martin Corporation, BAE Systems plc, ABB Ltd., Schneider Electric SE, Huawei Technologies Co. Ltd., IBM Corporation, General Dynamics Corporation, Northrop Grumman Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |