Reports

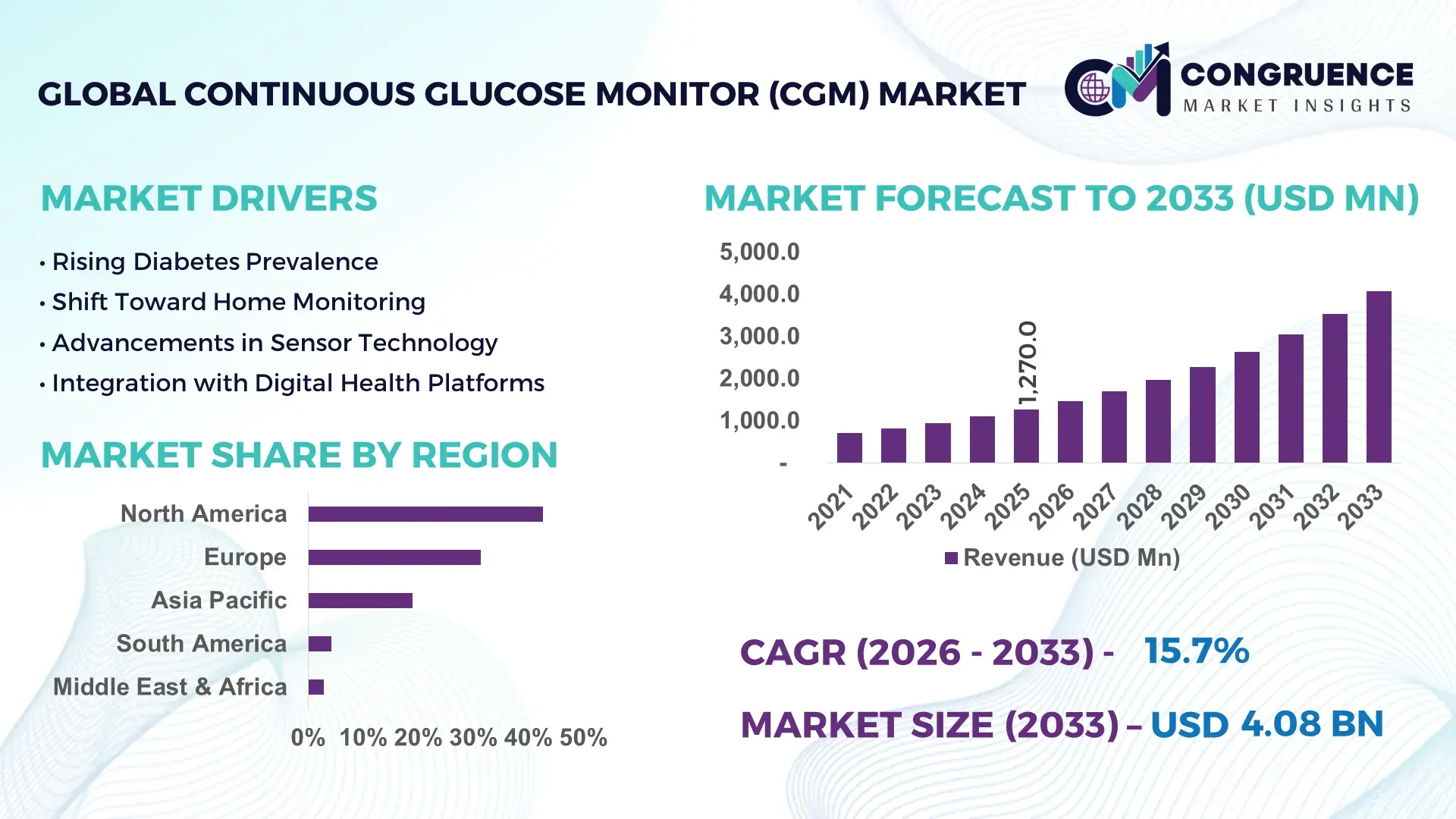

The Global Continuous Glucose Monitor (CGM) Market was valued at USD 1,270.0 Million in 2025 and is anticipated to reach a value of USD 4,078.2 Million by 2033 expanding at a CAGR of 15.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by the rapid shift toward real-time glucose monitoring, rising diabetes prevalence, and wider integration of digital health platforms in routine disease management.

The United States dominates the global Continuous Glucose Monitor (CGM) Market in terms of industrial depth and technological leadership. The country hosts large-scale CGM manufacturing and assembly facilities, with annual sensor production exceeding 35 million units, supported by advanced semiconductor fabrication and biomedical engineering ecosystems. Annual private and public investments in diabetes technology exceed USD 3.5 billion, accelerating innovation in minimally invasive sensors, extended-wear devices, and AI-enabled glucose analytics. CGM adoption in the U.S. has crossed 60% among insulin-dependent diabetic patients, with strong penetration across hospitals, homecare settings, and remote patient monitoring programs. Technological advancements such as factory-calibrated sensors, 14–15 day wear cycles, and smartphone-integrated receivers are widely commercialized, reinforcing the country’s position as a global CGM innovation hub.

Market Size & Growth: Valued at USD 1,270.0 million in 2025, projected to reach USD 4,078.2 million by 2033, growing at 15.7% CAGR, driven by rising demand for continuous and non-invasive glucose monitoring.

Top Growth Drivers: Diabetes patient adoption +18%, remote patient monitoring usage +22%, sensor accuracy improvement +30%.

Short-Term Forecast: By 2028, CGM sensor manufacturing costs are expected to decline by ~20% through automation and scale efficiencies.

Emerging Technologies: AI-driven glucose prediction algorithms, implantable CGM sensors, Bluetooth-enabled multi-device integration.

Regional Leaders: North America (~USD 1.6 billion by 2033) with insurance-backed adoption; Europe (~USD 1.1 billion) driven by public healthcare rollout; Asia Pacific (~USD 0.9 billion) led by rising urban diabetes prevalence.

Consumer/End-User Trends: Homecare users account for over 55% of device usage, with growing preference for smartphone-linked CGM systems.

Pilot or Case Example: In 2024, a U.S.-based hospital network reported a 28% reduction in hypoglycemic events after CGM integration.

Competitive Landscape: Market leader holds ~35% share, followed by Abbott, Medtronic, Senseonics, and Dexcom.

Regulatory & ESG Impact: Supportive reimbursement policies and digital health regulations accelerating CGM adoption in chronic care.

Investment & Funding Patterns: Over USD 6 billion invested globally in CGM-related R&D, startups, and manufacturing expansion since 2022.

Innovation & Future Outlook: Integration with insulin pumps, AI-based alerts, and cloud health platforms shaping next-generation CGM ecosystems.

Continuous Glucose Monitor (CGM) Market adoption is primarily driven by diabetes management (~70% contribution), followed by gestational diabetes and hospital critical-care monitoring. Recent innovations include longer-life sensors, needle-free prototypes, and AI-based glucose forecasting. Regulatory approvals supporting remote monitoring, rising healthcare digitization, strong North American consumption, and fast Asia Pacific growth are shaping future expansion, with personalized and predictive CGM solutions emerging as a key trend.

The Continuous Glucose Monitor (CGM) Market holds strong strategic relevance within the global healthcare and medical device ecosystem as it directly supports chronic disease management, digital health transformation, and value-based care models. CGM systems enable continuous, real-time glucose tracking, significantly improving clinical decision-making and patient self-management. Compared to traditional finger-prick testing, real-time CGM delivers nearly 40% improvement in glycemic control accuracy, reducing acute complications and long-term healthcare burden. Integration with smartphones, insulin pumps, and cloud-based platforms positions CGM as a core component of connected care infrastructure.

From a regional perspective, North America dominates in volume, driven by high device penetration and insurance coverage, while Europe leads in structured adoption, with nearly 48% of insulin-dependent patients enrolled in CGM-supported care pathways. Asia Pacific is emerging rapidly as urban diabetes prevalence increases and governments invest in digital health infrastructure. By 2028, AI-enabled glucose analytics are expected to reduce emergency hypoglycemia incidents by 25%, enhancing patient safety and lowering hospitalization rates.

Compliance and ESG considerations are also shaping the market. Manufacturers are committing to sustainability initiatives such as 30% reduction in electronic waste and sensor material recycling by 2030, aligning with healthcare ESG mandates. In 2024, a U.S.-based CGM manufacturer achieved a 22% improvement in patient adherence through AI-driven alerts and behavioral analytics. Looking ahead, the Continuous Glucose Monitor (CGM) Market is positioned as a pillar of healthcare resilience, regulatory compliance, and sustainable, data-driven growth.

The Continuous Glucose Monitor (CGM) Market is shaped by rising diabetes prevalence, rapid digitalization of healthcare, and increasing preference for continuous, real-time monitoring solutions. Technological advancements in biosensors, wireless connectivity, and AI analytics are redefining device capabilities and clinical outcomes. Healthcare systems are increasingly integrating CGM into chronic disease management programs, remote monitoring, and value-based care models. At the same time, policy support for digital health, growing patient awareness, and expansion of homecare services are reinforcing demand. However, the market also faces challenges related to cost sensitivity, regulatory complexity, and data privacy compliance, influencing adoption patterns across regions.

The growing need for precise, real-time diabetes management is a primary driver of the Continuous Glucose Monitor (CGM) Market. Globally, over 530 million people live with diabetes, with insulin-dependent patients increasingly shifting toward continuous monitoring solutions. CGM systems enable up to 288 glucose readings per day, compared to fewer than 10 with traditional testing, significantly improving treatment accuracy. Clinical studies show CGM usage can reduce severe hypoglycemic episodes by 30–40%, driving adoption among hospitals and homecare users. Increased physician preference for data-driven treatment and expanding telehealth programs further reinforce demand.

High upfront device costs and recurring sensor replacement expenses remain key restraints in the Continuous Glucose Monitor (CGM) Market. Sensors typically require replacement every 10–15 days, creating ongoing affordability challenges, particularly in low- and middle-income regions. Out-of-pocket expenses can limit adoption among non-insured patients, while reimbursement coverage remains inconsistent across countries. Additionally, system integration costs for hospitals and data security compliance requirements increase total ownership costs, slowing adoption in cost-sensitive healthcare systems despite strong clinical benefits.

Digital health integration presents significant opportunities for the Continuous Glucose Monitor (CGM) Market. Integration with AI platforms, mobile health apps, and insulin delivery systems enables predictive analytics and personalized treatment pathways. AI-powered CGM systems can forecast glucose fluctuations with over 85% predictive accuracy, opening opportunities in preventive care and population health management. Expansion of remote patient monitoring programs and employer-sponsored wellness initiatives is creating new demand channels, particularly in emerging economies investing heavily in digital healthcare infrastructure.

Regulatory approval processes and data privacy requirements pose ongoing challenges for the Continuous Glucose Monitor (CGM) Market. CGM devices must comply with stringent medical device regulations, cybersecurity standards, and patient data protection laws. Differences in regulatory frameworks across regions increase time-to-market and compliance costs. Additionally, secure handling of continuous patient data requires robust encryption and IT infrastructure, raising operational complexity for manufacturers and healthcare providers and potentially delaying large-scale deployments.

Expansion of AI-Enabled Predictive Glucose Analytics: Over 45% of newly launched CGM systems now incorporate AI-driven algorithms capable of predicting glucose fluctuations up to 60 minutes in advance, improving clinical intervention accuracy. These systems have demonstrated a 25% reduction in severe hypoglycemic events, particularly in insulin-dependent patients. Adoption is strongest in North America and Europe, where digital health infrastructure supports advanced analytics integration.

Growth of Long-Wear and Implantable CGM Sensors: Demand for extended-wear CGM sensors has increased sharply, with devices offering 14–15 day wear cycles accounting for nearly 50% of new installations. Implantable CGM technologies are gaining traction, reducing sensor replacement frequency by over 70% and improving patient convenience. This trend is particularly impactful in elderly and pediatric care segments.

Rapid Shift Toward Smartphone-Centric CGM Ecosystems: More than 65% of CGM users now rely on smartphone-based receivers instead of standalone monitors. Bluetooth-enabled connectivity has improved data accessibility, enabling real-time sharing with caregivers and clinicians. This shift has increased patient adherence rates by approximately 20%, especially among younger and tech-savvy users.

Integration with Remote Patient Monitoring and Telehealth Programs: CGM integration into remote patient monitoring programs has expanded by 40% since 2022, supporting home-based diabetes management. Hospitals using CGM-linked telehealth platforms report a 30% reduction in diabetes-related emergency visits, highlighting the role of CGM in reducing healthcare system burden while improving patient outcomes.

The Continuous Glucose Monitor (CGM) Market is segmented by type, application, and end-user, reflecting varied clinical use cases, technology maturity levels, and adoption behaviors across healthcare settings. Type-based segmentation highlights differences in device design, sensor placement, and data transmission capabilities, directly influencing patient comfort and monitoring accuracy. Application segmentation underscores how CGM systems are increasingly used beyond traditional diabetes management, expanding into hospital monitoring, gestational care, and preventive health programs. End-user segmentation reveals strong contrasts between institutional adoption and individual home-based usage, driven by reimbursement structures, digital health penetration, and care delivery models. Across all segments, adoption is strongly influenced by ease of use, sensor lifespan, interoperability with digital platforms, and integration with insulin delivery systems, making segmentation a critical lens for strategic planning and investment analysis.

The CGM market by type includes real-time CGM (rtCGM), intermittently scanned CGM (isCGM), and implantable CGM systems. Real-time CGM currently accounts for approximately 48% of total adoption, supported by its continuous data streaming, automated alerts, and strong integration with insulin pumps and mobile applications. Its leadership is reinforced by clinical use in intensive diabetes management and hospital-based monitoring. Intermittently scanned CGM represents about 32% of adoption, favored for lower cost and simplified usage, particularly among type 2 diabetes patients and emerging markets.

Implantable CGM systems, while currently accounting for roughly 20% of adoption, represent the fastest-growing type, with adoption expanding at an estimated 18% annually, driven by extended sensor lifespans of up to 180 days, reduced replacement frequency, and improved patient adherence. Other niche formats and hybrid devices collectively contribute the remaining ~20%, addressing specific clinical or lifestyle needs.

In 2025, a national diabetes program deployed implantable CGM devices across multiple clinical centers, reporting over 25% improvement in long-term patient adherence due to reduced sensor replacement requirements.

By application, diabetes management remains the dominant segment, accounting for nearly 62% of total CGM usage, as CGM systems are increasingly embedded into standard care protocols for type 1 and insulin-dependent type 2 diabetes. Hospital and clinical monitoring follows with approximately 21% adoption, supported by growing use of CGM for inpatient glucose surveillance and post-surgical care. Gestational diabetes monitoring and preventive health screening together contribute around 17%.

Preventive and population health monitoring represents the fastest-growing application, expanding at an estimated 17% annually, driven by employer wellness programs, early-risk identification, and digital health platforms. In 2025, over 40% of hospitals reported piloting CGM systems for inpatient glucose monitoring, while 35% of digitally engaged patients indicated preference for CGM-enabled mobile health applications over traditional testing methods.

In 2024, a large hospital network integrated CGM into inpatient care pathways, achieving a 30% reduction in glucose-related adverse events across monitored patients.

By end-user, homecare and individual patients form the largest segment, representing approximately 55% of total CGM adoption, driven by rising self-management awareness, remote monitoring tools, and smartphone-based interfaces. Hospitals and clinics account for around 28%, reflecting expanding use of CGM in inpatient care, critical care units, and outpatient diabetes clinics. Other end-users, including research institutions, wellness programs, and long-term care facilities, collectively contribute about 17%.

Hospitals represent the fastest-growing end-user segment, with adoption increasing at an estimated 16% annually, supported by digital hospital initiatives, integration with electronic health records, and demand for continuous patient monitoring. In 2025, nearly 42% of hospitals in developed healthcare systems were testing CGM-supported clinical protocols, while over 60% of digitally active patients reported higher confidence in care plans that included continuous monitoring.

In 2025, a nationwide healthcare system implemented CGM across multiple hospitals, reporting a 22% improvement in inpatient glucose stability and shorter average lengths of stay for diabetic patients.

North America accounted for the largest market share at 42.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.4% between 2026 and 2033.

The regional performance of the Continuous Glucose Monitor (CGM) Market reflects disparities in healthcare infrastructure, reimbursement coverage, technology penetration, and diabetes prevalence. North America leads due to high CGM penetration among insulin-dependent patients, strong integration with digital health ecosystems, and widespread insurance reimbursement. Europe follows with structured adoption through public healthcare systems and regulatory-backed digital health frameworks. Asia-Pacific is emerging rapidly, supported by a growing diabetic population exceeding 260 million, expanding manufacturing bases, and increasing smartphone-based health monitoring. South America and the Middle East & Africa represent developing regions, where adoption is accelerating through government programs, private healthcare expansion, and import-led device availability, albeit from smaller bases.

North America holds approximately 42.6% of the global Continuous Glucose Monitor (CGM) Market, making it the largest regional contributor by volume. Demand is primarily driven by diabetes management within hospitals, homecare settings, and integrated digital health platforms. The healthcare sector accounts for over 70% of CGM usage, supported by favorable reimbursement policies covering CGM devices for insulin-dependent patients. Regulatory frameworks increasingly support remote patient monitoring and interoperability with electronic health records. Technologically, over 65% of CGM users rely on smartphone-connected systems, and AI-enabled alerts are widely adopted. A leading regional player has expanded local sensor manufacturing capacity by over 25% to support domestic demand. Consumer behavior reflects high adoption among homecare users, with strong trust in data-driven, app-based glucose monitoring solutions.

Europe accounts for roughly 31.4% of global CGM adoption, with Germany, the UK, and France representing the largest national markets. Public healthcare systems play a central role, with CGM increasingly included in national diabetes management programs. Regulatory bodies emphasize data security, device accuracy, and interoperability, influencing product design and deployment. Sustainability and digital health initiatives have encouraged the adoption of longer-life sensors, reducing medical waste. Over 50% of European CGM users are enrolled through public reimbursement schemes. Regional manufacturers focus on factory-calibrated and minimally invasive sensors to align with regulatory and patient expectations. Consumer behavior in this region reflects cautious but consistent adoption, with strong preference for clinically validated and explainable digital health technologies.

Asia-Pacific ranks as the fastest-growing region by volume expansion, currently accounting for approximately 18.9% of global CGM usage. China, India, and Japan are the top consuming countries, together representing over 75% of regional demand. The region benefits from expanding local manufacturing, with sensor and wearable production capacity increasing by nearly 30% over recent years. Mobile health platforms dominate, with over 60% of users accessing CGM data through smartphones. Innovation hubs in East Asia are advancing compact sensors and cost-optimized designs. A regional manufacturer recently scaled domestic CGM assembly to serve both local and export markets. Consumer behavior is strongly influenced by affordability, e-commerce availability, and mobile-first healthcare engagement.

South America represents around 4.2% of global CGM adoption, led by Brazil and Argentina. Demand is driven by expanding private healthcare networks and increasing diabetes awareness. Urban hospitals account for nearly 55% of regional CGM usage, while homecare adoption is gradually increasing. Governments are introducing healthcare digitization initiatives and reducing import barriers for medical devices, improving accessibility. Local distributors focus on partnerships with global CGM manufacturers to improve availability. Consumer behavior varies widely, with higher adoption in metropolitan areas and among privately insured patients, while rural penetration remains limited but improving.

The Middle East & Africa region contributes approximately 2.9% of global CGM demand, with the UAE and South Africa as key growth countries. Rising diabetes prevalence, exceeding 12% of the adult population in several Gulf nations, is driving demand. Governments are investing heavily in healthcare modernization, smart hospitals, and digital patient monitoring. CGM adoption is strongest in private hospitals and specialty diabetes clinics. A regional healthcare group recently deployed CGM systems across multiple urban hospitals to support chronic disease management. Consumer behavior reflects growing acceptance among high-income patients, while broader adoption is supported through public health initiatives and partnerships.

United States – 38.2% Market Share: High production capacity, widespread insurance reimbursement, and strong homecare adoption drive dominance in the Continuous Glucose Monitor (CGM) Market.

Germany – 9.6% Market Share: Strong regulatory-backed healthcare systems and structured adoption through public diabetes programs support leadership in the Continuous Glucose Monitor (CGM) Market.

The competitive environment in the Continuous Glucose Monitor (CGM) Market is characterized by a mix of well-established multinational medical device firms and innovative emerging players advancing sensor technology, digital integration, and patient engagement solutions. There are 20+ active competitors globally, with competition shaped by product differentiation, regulatory approvals, channel expansion, and strategic partnerships. The market structure remains moderately consolidated, with the top 5 companies collectively holding around 78% of the global CGM market share, reflecting dominance by incumbent leaders while still leaving space for niche innovators.

Market leaders have pursued strategic initiatives such as partnerships with digital health platforms, extended wear sensor development, and over-the-counter (OTC) device launches to expand consumer access. For example, Dexcom strengthened its co-development agreement with Verily Life Sciences to innovate next-generation sensors and digital analytics, and launched the OTC Dexcom Stelo CGM to appeal to broader user segments. Abbott expanded its portfolio with consumer-focused OTC offerings like Lingo and Libre Rio, targeting early-stage and wellness-oriented users. Partnerships between Abbott and Medtronic to integrate FreeStyle Libre technology with automated insulin delivery systems underscore the push for hybrid ecosystem offerings.

Innovation trends influencing competition include enhanced sensor accuracy (MARD <10%), Bluetooth and smartphone connectivity, AI-powered glucose analytics, and implantable CGM systems with extended wear durations. Emerging competitors continue to target white spaces such as non-invasive optical glucose sensing and predictive data analytics, intensifying product differentiation. Regulatory changes enabling OTC CGM sales and broader insurance reimbursements are also reshaping competitive positioning by lowering barriers to consumer adoption and expanding addressable markets.

Senseonics Holdings, Inc.

Ypsomed AG

Roche Diagnostics

Menarini Diagnostics

Signos, Inc.

Tandem Diabetes Care

Insulet Corporation

Bigfoot Biomedical

Ultrahuman (M1 CGM)

GlySens Incorporated

Indigo Diabetes

Profusa, Inc.

Liom (Spiden)

The technological landscape of the Continuous Glucose Monitor (CGM) Market is rapidly evolving, driven by advancements in sensor design, connectivity, data analytics, and user experience. Traditional electrochemical sensors remain the cornerstone of most CGM systems, but current technology improvements have led to sensor accuracy levels below 10% Mean Absolute Relative Difference (MARD), providing clinically actionable glucose readings with minimal calibration needs. Modern sensors aim to reduce warm-up times, enhance wear comfort, and extend functional lifespans, with implantable systems achieving up to 365 days of continuous use through miniaturized, biocompatible components.

Connectivity advancements such as built-in Bluetooth Low Energy (BLE) and smartphone integration are now standard in consumer CGM systems, enabling real-time glucose transmission to mobile apps and cloud platforms. Enhanced digital ecosystems support AI-augmented glucose trend analysis, predictive alerts, and remote clinician access, fostering greater patient engagement and self-management. Industry adoption of over-the-counter (OTC) CGM devices is another significant trend, expanding accessibility beyond traditional prescription channels and allowing broader lifestyle and wellness monitoring.

Hybrid and closed-loop systems represent another frontier in CGM technology, combining continuous glucose data with automated insulin delivery algorithms to create integrated diabetes management solutions. Partnerships between CGM manufacturers and insulin pump developers are resulting in tighter feedback loops, optimizing insulin dosing decisions without manual intervention. Additionally, exploratory research into non-invasive optical sensing technologies, including Raman spectroscopy and plasmonic sensors, aims to further transform the market by eliminating skin penetration entirely, improving comfort and adherence.

Overall, technology trends are converging toward more seamless, accurate, and user-centric CGM ecosystems that empower both patients and healthcare providers with real-time insights while reducing daily management burdens.

• In September 2024, the FDA cleared Senseonics’ Eversense 365, the first implantable CGM capable of lasting a full year with real-time mobile connectivity, enhancing long-term glucose monitoring for adults with diabetes. Source: www.verywellhealth.com

• In July 2025, Abbott Laboratories reported stronger-than-expected quarterly profits driven by robust demand for medical devices including continuous glucose monitors, demonstrating sustained market traction and underlying device demand growth. Source: www.reuters.com

• In May 2025, Oura Labs introduced AI-powered glucose tracking and meal logging features by integrating the Dexcom Stelo CGM with its wearable ecosystem, enabling users to view glucose data alongside other health metrics in the Oura app. Source: www.theverge.com

• In 2025, Tracky (DrStore Healthcare Services) launched India’s first Bluetooth-enabled continuous glucose monitor, offering real-time mobile alerts and automatic syncing every three minutes, aimed at cost-effective diabetes management for local users.

The Continuous Glucose Monitor (CGM) Market Report provides a comprehensive, multi-dimensional overview of the industry’s structure, segmentation, and strategic imperatives shaping the future of glucose monitoring technologies. The report covers key product segments, including standalone and integrated CGM systems, implantable sensors, and over-the-counter (OTC) devices. It also analyzes connectivity technologies such as Bluetooth, NFC, and cloud integration that enable real-time data transmission, remote patient monitoring, and interoperability with mobile health platforms.

Geographically, the scope includes detailed coverage across major regional markets—such as North America, Europe, Asia-Pacific, South America, and Middle East & Africa—highlighting regional demand drivers, regulatory frameworks, and infrastructure readiness that influence CGM adoption. The report examines application areas spanning diabetes management, hospital inpatient monitoring, gestational glucose tracking, and preventive health uses, providing insights into evolving use cases and clinical adoption patterns.

End-user profiles are segmented by hospitals, homecare settings, research institutions, and wellness/consumer health markets, offering a nuanced view of deployment scenarios, purchase behavior, and service models. Emerging and niche market segments such as non-invasive optical CGM technologies, AI-enhanced analytics, and predictive glucose forecasting systems are identified to capture innovation trajectories and competitive disruptions.

In addition, the report includes assessments of regulatory environments, reimbursement landscapes, and healthcare policy impacts, as well as strategic analyses of competitive positioning, partnerships, and product pipelines. By encompassing both current market realities and forward-looking technological trends, the report equips decision-makers with actionable intelligence for investment planning, product development, and market entry strategies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,270.0 Million |

| Market Revenue (2033) | USD 4,078.2 Million |

| CAGR (2026–2033) | 15.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Abbott Laboratories, Dexcom, Inc., Medtronic plc, Senseonics Holdings, Inc., Ypsomed AG, Roche Diagnostics, Menarini Diagnostics, Signos, Inc., Tandem Diabetes Care, Insulet Corporation, Bigfoot Biomedical, Ultrahuman (M1 CGM), GlySens Incorporated, Indigo Diabetes, Profusa, Inc., Liom (Spiden) |

| Customization & Pricing | Available on Request (10% Customization Free) |