Reports

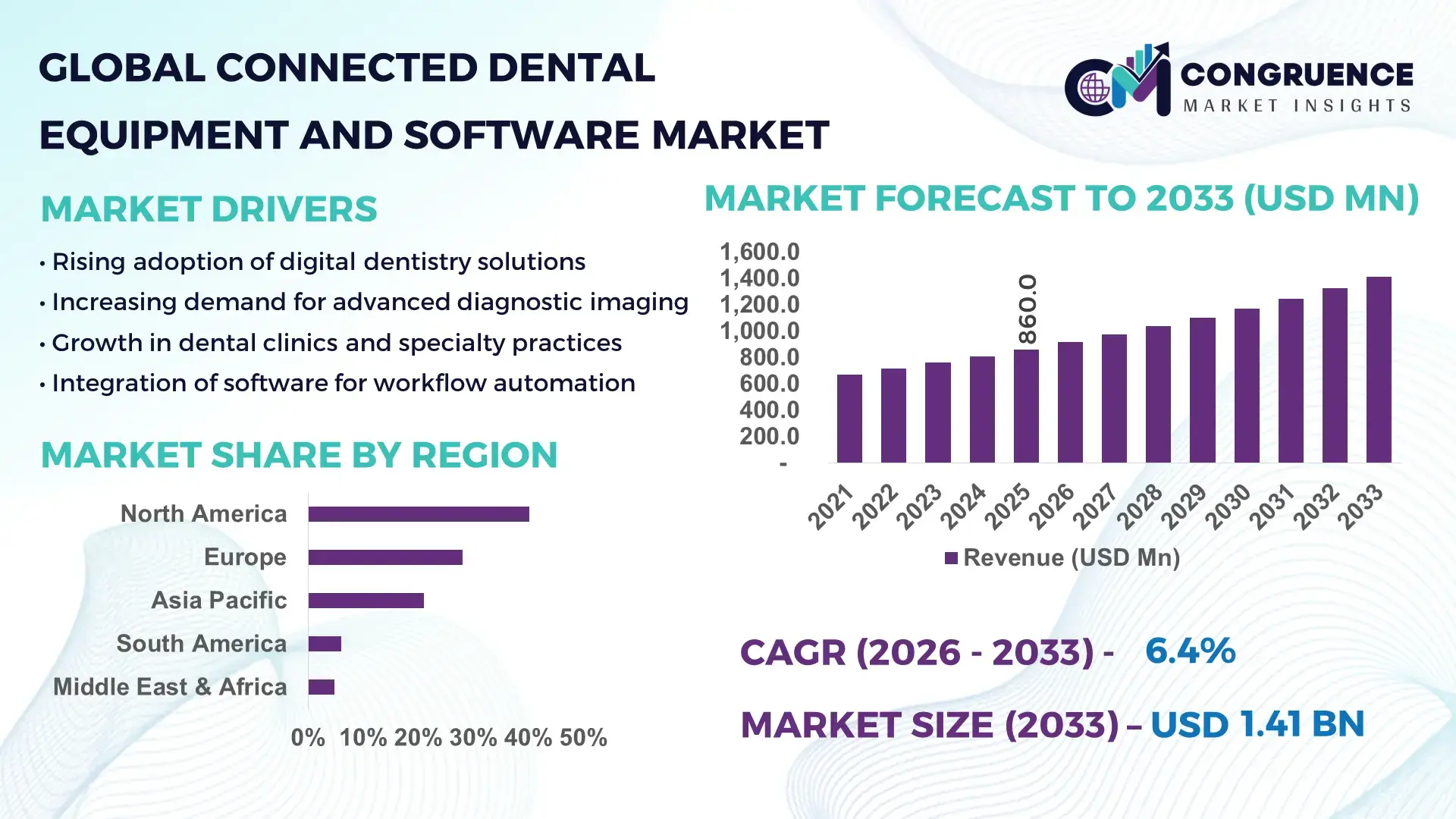

The Global Connected Dental Equipment and Software Market was valued at USD 860.0 Million in 2025 and is anticipated to reach a value of USD 1,412.6 Million by 2033 expanding at a CAGR of 6.4% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is largely supported by the increasing integration of cloud-connected dental imaging systems, AI-enabled diagnostic software, and IoT-enabled treatment equipment across modern dental clinics and hospital networks.

The United States represents the most technologically advanced environment for connected dental equipment and software deployment. The country operates over 200,000 practicing dentists across more than 65,000 dental clinics, many of which have integrated digital imaging, cloud-connected practice management platforms, and AI-enabled diagnostics. More than 62% of U.S. dental practices currently utilize digital radiography systems, while approximately 48% have implemented cloud-based dental practice management software. The U.S. dental equipment manufacturing ecosystem includes major global players developing connected CAD/CAM milling machines, intraoral scanners, and AI-assisted imaging platforms capable of processing millions of patient scans annually. Dental imaging devices alone account for over 30% of connected dental equipment deployments in the country, with dental laboratories increasingly integrating automated design software and 3D printing solutions for prosthetic fabrication. Additionally, more than 40% of orthodontic clinics utilize connected treatment planning platforms, enabling real-time collaboration between dentists, labs, and patients through secure digital ecosystems.

Market Size & Growth: The market was valued at USD 860.0 Million in 2025 and is projected to reach USD 1,412.6 Million by 2033, expanding at 6.4% CAGR due to accelerating digital transformation across dental clinics and laboratories.

Top Growth Drivers: Increasing adoption of digital dental workflows (58% clinics adopting digital imaging), AI-assisted diagnostic efficiency improvement (32% faster case analysis), and cloud practice management adoption (45% clinic adoption globally).

Short-Term Forecast: By 2028, connected dental platforms are expected to improve clinical workflow efficiency by 28%, while reducing patient data processing time by 22%.

Emerging Technologies: AI-powered dental imaging analytics, cloud-integrated dental practice management systems, and IoT-enabled treatment equipment monitoring are transforming dental workflows.

Regional Leaders: North America projected at USD 540 Million by 2033 driven by advanced digital clinics; Europe estimated at USD 390 Million with strong dental laboratory automation adoption; Asia-Pacific approaching USD 310 Million with rising dental clinic digitization.

Consumer/End-User Trends: Dental clinics increasingly deploy integrated platforms connecting intraoral scanners, imaging systems, and patient record software, enabling faster diagnostics and improved treatment planning.

Pilot or Case Example: In 2024, a digital dentistry pilot program integrating AI-assisted radiography reduced diagnostic review time by 35% and improved treatment planning accuracy by 26%.

Competitive Landscape: Dentsply Sirona leads with approximately 16% share, followed by Straumann Group, Align Technology, Carestream Dental, and Planmeca.

Regulatory & ESG Impact: Healthcare data protection frameworks and digital health interoperability regulations are accelerating the adoption of secure connected dental platforms globally.

Investment & Funding Patterns: Over USD 750 Million has recently been invested globally in digital dentistry platforms, AI diagnostics startups, and connected dental device innovation.

Innovation & Future Outlook: Integration of AI-driven diagnostics, 3D printing prosthetics, and cloud-connected dental workflows is expected to reshape the digital dentistry ecosystem over the next decade.

Connected dental equipment and software are increasingly used across general dentistry (42%), orthodontics (21%), prosthodontics (18%), and dental laboratories (19%), reflecting the expansion of digital treatment workflows. Recent innovations include AI-assisted radiography analysis, automated prosthetic design platforms, and cloud-based dental record systems. Regulatory frameworks promoting digital health interoperability and rising patient demand for minimally invasive procedures are accelerating adoption, particularly in North America and Asia-Pacific, while integrated dental ecosystems are emerging as a key operational trend.

The Connected Dental Equipment and Software Market is strategically important for the modernization of global dental healthcare infrastructure. Dental clinics, hospitals, and laboratories are transitioning from fragmented analog systems toward digitally integrated ecosystems that connect imaging devices, treatment equipment, and clinical software platforms. This transformation improves operational efficiency, diagnostic accuracy, and patient outcomes. Digital intraoral scanning technologies now allow dentists to capture high-resolution images in seconds, enabling faster diagnosis and prosthetic design. In comparison, AI-assisted dental imaging analysis delivers nearly 35% faster diagnostic interpretation compared to traditional manual radiographic assessments, significantly improving workflow productivity.

Regionally, North America dominates in equipment volume, supported by a large installed base of dental imaging systems and CAD/CAM equipment, while Europe leads in software adoption with nearly 52% of dental laboratories using integrated digital workflow platforms for prosthetic design and manufacturing. Asia-Pacific is rapidly scaling adoption as dental infrastructure expands and digital dentistry education programs increase. By 2028, AI-driven diagnostic algorithms integrated into connected dental platforms are expected to reduce diagnostic error rates by nearly 25% while improving treatment planning efficiency across multi-clinic networks.

Regulatory compliance and ESG considerations are also shaping the market. Dental organizations are increasingly implementing secure cloud-based patient data systems that align with healthcare data protection standards, while manufacturers are investing in energy-efficient digital imaging devices that reduce operational power consumption by nearly 18%. Sustainability initiatives are also emerging through digital workflows that reduce material waste in prosthetic manufacturing.

A practical example illustrates this transformation: in 2024, a digital dentistry initiative in Germany integrated AI-enabled imaging and cloud-based case management across 120 clinics, resulting in a 31% reduction in treatment planning time. Such initiatives demonstrate the scalability of connected dental ecosystems.

Looking ahead, the Connected Dental Equipment and Software Market will evolve as a critical pillar of healthcare digitization, enabling real-time collaboration among dentists, laboratories, and patients while strengthening regulatory compliance, clinical precision, and sustainable dental healthcare delivery.

The Connected Dental Equipment and Software Market is undergoing significant transformation as dental clinics and laboratories increasingly adopt digital technologies to improve diagnostic precision, treatment planning efficiency, and patient experience. Connected systems integrate intraoral scanners, digital radiography devices, CAD/CAM equipment, and cloud-based practice management software into a unified ecosystem. This connectivity allows dentists to access real-time patient data, collaborate with laboratories remotely, and automate prosthetic design workflows.

Digital dentistry adoption is expanding across developed and emerging markets. Over 60% of newly established dental clinics globally are now equipped with digital imaging devices, while cloud-based patient record systems are being implemented across multi-clinic dental chains to streamline operations. Furthermore, advances in AI-assisted radiographic interpretation and automated prosthetic design software are enabling clinicians to process complex diagnostic data more efficiently. Growing patient expectations for faster treatment outcomes, combined with increasing demand for cosmetic dentistry and orthodontic solutions, are accelerating the adoption of connected dental technologies. The expansion of dental service organizations and multi-clinic networks is further encouraging centralized software platforms that allow seamless coordination across geographically distributed facilities.

The transition from traditional analog dental workflows to fully digital clinical environments is one of the most significant drivers of the Connected Dental Equipment and Software Market. Dental clinics are rapidly adopting digital radiography, intraoral scanning, and CAD/CAM restoration systems that require integrated software platforms to manage patient data and treatment workflows. Digital radiography systems now represent over 65% of imaging installations in developed dental markets, replacing conventional film-based X-ray systems due to faster image processing and improved diagnostic clarity. Connected dental equipment allows clinicians to transmit patient scan data instantly to dental laboratories for prosthetic design and manufacturing. This digital workflow can reduce prosthetic production time by up to 40% compared with traditional manual fabrication processes. Additionally, AI-assisted imaging platforms are capable of identifying dental caries, bone loss, and periodontal disease patterns with diagnostic accuracy improvements exceeding 20% compared to manual evaluation. Dental service organizations managing multiple clinics increasingly rely on centralized cloud platforms to monitor equipment performance, schedule treatments, and coordinate laboratory collaboration. These platforms allow clinics to track treatment progress and patient histories across networks of facilities, significantly improving operational efficiency. As dental professionals continue to invest in integrated digital technologies, connected dental equipment and software platforms are becoming essential infrastructure for modern dental healthcare delivery.

Despite the operational advantages offered by connected dental equipment and software platforms, high initial investment requirements remain a major barrier for smaller dental clinics and independent practitioners. Advanced digital dental ecosystems require the deployment of intraoral scanners, 3D imaging devices, CAD/CAM milling systems, and integrated practice management software, all of which involve substantial capital expenditure. A single high-resolution cone-beam computed tomography system may cost more than USD 80,000, while integrated digital treatment planning platforms require annual licensing and maintenance expenses. Small dental practices often operate under tight financial constraints, limiting their ability to adopt full digital ecosystems. Additionally, integrating connected dental devices into existing clinic infrastructure requires software customization, data migration, and staff training. Dental professionals must also invest time in learning new digital workflows and maintaining compliance with healthcare data protection standards. Another challenge involves interoperability between equipment manufactured by different vendors. Many dental clinics operate devices from multiple suppliers, which can create compatibility issues when integrating them into a unified software platform. This fragmentation increases implementation complexity and may delay digital transformation initiatives, particularly for clinics in emerging markets with limited access to advanced technical support and IT resources.

Artificial intelligence is opening significant opportunities for the Connected Dental Equipment and Software Market by enhancing diagnostic capabilities and improving clinical decision-making processes. AI-enabled dental imaging platforms can analyze thousands of radiographic images within seconds, identifying early signs of dental diseases that might be difficult for clinicians to detect manually. These systems are particularly valuable for detecting early-stage caries, periodontal bone loss, and root canal complications. Clinical studies indicate that AI-assisted radiographic analysis can improve diagnostic accuracy by approximately 25%, enabling dentists to develop more effective treatment plans and reduce the risk of misdiagnosis. AI platforms also integrate with patient management software to generate automated treatment recommendations and predictive oral health assessments based on historical patient data. Furthermore, AI-powered workflow automation is enabling dental laboratories to design prosthetic restorations automatically using digital impressions captured by intraoral scanners. These technologies allow laboratories to process over 70% of prosthetic design tasks digitally, significantly reducing turnaround time and manual labor requirements. As AI capabilities continue to expand, connected dental equipment and software platforms will increasingly become the foundation for intelligent dental healthcare systems that support predictive diagnostics and personalized treatment strategies.

The growing reliance on connected digital platforms in dental healthcare has raised serious concerns regarding cybersecurity and patient data protection. Connected dental systems often store sensitive patient records, diagnostic images, and treatment plans on cloud-based platforms that can be vulnerable to cyberattacks if not adequately secured. Healthcare organizations are among the most targeted sectors for cyber threats, with ransomware attacks increasing significantly in recent years. Dental clinics adopting connected systems must comply with strict healthcare data protection regulations that require encryption, secure authentication mechanisms, and controlled access to patient records. Implementing these security frameworks requires additional investments in IT infrastructure and cybersecurity expertise. Many small clinics lack dedicated IT teams, making it difficult to maintain robust cybersecurity protocols. Another challenge involves ensuring secure data exchange between dental clinics and external laboratories. Prosthetic design workflows often require transferring high-resolution patient scan data across digital platforms. Without secure encryption protocols, these transfers could expose sensitive patient information. As the volume of connected dental devices continues to grow, maintaining secure digital ecosystems will remain a critical challenge for healthcare providers and technology vendors alike.

Rapid Adoption of AI-Assisted Dental Imaging: AI-enabled diagnostic systems are increasingly integrated into connected dental platforms, enabling automated interpretation of radiographic images. Recent deployments show that AI tools can analyze over 2,000 dental scans per hour, improving diagnostic speed by 35% while reducing manual review time by 30%. Approximately 48% of advanced dental clinics now use AI-assisted radiography analysis systems to detect cavities, periodontal disease, and bone loss patterns.

Expansion of Digital Intraoral Scanning Technologies: Intraoral scanners are replacing traditional dental impressions across modern clinics. More than 55% of orthodontic practices globally now utilize digital scanning systems for treatment planning. These scanners capture 3D images with accuracy levels exceeding 95%, enabling dental laboratories to design prosthetic restorations digitally and reducing physical impression material usage by 40%.

Integration of Cloud-Based Dental Practice Management Platforms: Cloud dental software platforms are transforming how clinics manage patient data and treatment workflows. Approximately 46% of multi-clinic dental organizations have adopted centralized cloud platforms capable of synchronizing patient records across facilities. These systems enable dentists to access treatment histories remotely while reducing administrative workload by 27%.

Growth in Digital Dental Laboratory Automation: Dental laboratories are increasingly adopting connected design and manufacturing systems. Automated CAD/CAM design platforms now handle over 60% of prosthetic design tasks in advanced dental labs. Combined with 3D printing technologies capable of producing dental crowns in less than 45 minutes, these systems significantly accelerate restoration production while improving manufacturing precision.

The Connected Dental Equipment and Software Market is segmented based on type, application, and end-user, reflecting the diverse technological ecosystem within modern digital dentistry. Equipment categories include connected imaging devices, intraoral scanning systems, and integrated CAD/CAM restoration platforms, while software solutions encompass practice management systems, imaging analysis platforms, and digital treatment planning tools. Applications span diagnostic imaging, orthodontic treatment planning, prosthetic design, and clinical workflow management. End-users include dental clinics, hospitals, dental laboratories, and academic institutions involved in dental training and research. As digital dentistry continues to expand, the integration of connected devices with cloud-based software platforms is becoming essential for improving treatment efficiency, enabling remote collaboration between clinicians and laboratories, and supporting data-driven patient care strategies.

Connected dental equipment and software can be categorized into connected imaging equipment, intraoral scanners, CAD/CAM dental systems, and dental practice management software platforms. Among these, connected imaging equipment currently represents the leading segment, accounting for approximately 38% of overall deployments, as digital radiography and cone-beam CT scanners are essential for diagnostic imaging in dental clinics. These systems enable dentists to capture high-resolution images and instantly transmit data to diagnostic software platforms, improving clinical decision-making speed. Intraoral scanners account for roughly 24% of installations, supporting digital impression capture for orthodontic and prosthetic treatment planning. However, CAD/CAM dental systems represent the fastest-growing segment, expanding at nearly 8.2% adoption growth annually, as dental laboratories increasingly automate restoration design and fabrication processes. These systems enable the production of crowns, bridges, and aligners with high precision using digital design tools. Dental practice management software platforms represent around 18% of connected system deployments, enabling clinics to manage patient records, billing systems, and treatment workflows in a centralized digital environment. Other niche solutions such as AI-assisted diagnostic software and cloud imaging platforms collectively contribute approximately 20% of the market ecosystem, supporting advanced analytics and integrated clinical operations.

• According to a 2025 report by the National Institute of Dental and Craniofacial Research, digital radiography systems are installed in more than 70% of advanced dental clinics in developed healthcare markets.

The Connected Dental Equipment and Software Market serves several clinical applications including diagnostic imaging, orthodontic treatment planning, prosthetic restoration design, and dental clinic workflow management. Among these, diagnostic imaging remains the leading application, accounting for nearly 41% of connected system usage, as dentists rely heavily on digital X-ray and cone-beam CT technologies to detect oral diseases and evaluate treatment outcomes. Orthodontic treatment planning represents approximately 26% of the application landscape, with digital intraoral scanners enabling orthodontists to design aligners and braces using advanced 3D modeling software. However, prosthetic restoration design is emerging as the fastest-growing application, expanding at nearly 7.8% adoption growth, supported by increasing demand for digitally fabricated crowns, bridges, and dental implants. Other applications, including patient management and dental workflow automation systems, collectively account for 33% of connected dental technology usage, particularly within large dental service organizations managing multiple clinics. These platforms allow practitioners to track patient appointments, treatment histories, and diagnostic data in real time. In 2025, more than 44% of dental clinics globally reported integrating digital imaging platforms with patient management software to streamline treatment workflows.

• According to a 2024 report by the International Association for Dental Research, digital orthodontic planning systems were deployed in more than 12,000 clinics globally, improving treatment planning efficiency for millions of orthodontic patients.

End-users of connected dental equipment and software include dental clinics, hospitals, dental laboratories, and academic or research institutions. Among these, dental clinics represent the dominant segment with approximately 57% of total system adoption, as private clinics form the primary delivery channel for dental treatments worldwide. Clinics increasingly invest in digital imaging equipment and integrated practice management software to improve patient experience and streamline clinical workflows. Dental laboratories account for nearly 23% of connected technology adoption, particularly through the use of CAD/CAM restoration design systems and digital manufacturing platforms. However, hospitals represent the fastest-growing end-user segment, expanding at around 7.1% adoption growth, driven by the integration of dental departments into larger hospital digital health systems. Academic institutions and dental training centers contribute the remaining 20% of system deployments, using connected platforms for education, research, and advanced treatment experimentation. These institutions often pilot emerging technologies such as AI-assisted imaging analysis and 3D printed dental prosthetics. In 2025, approximately 52% of multi-clinic dental service organizations reported deploying centralized digital practice management systems to coordinate patient care across multiple facilities.

• According to a 2025 report by the American Dental Education Association, more than 80% of dental schools in North America have integrated digital dentistry training using intraoral scanners and CAD/CAM systems for clinical education.

North America accounted for the largest market share at 40.2% in 2025, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.8% between 2026 and 2033.

The global Connected Dental Equipment and Software Market has expanded rapidly as dental clinics and hospitals increasingly deploy cloud-enabled imaging systems, AI-driven diagnostics, and integrated practice management software. In 2025, the global market size for connected dental equipment and software reached approximately USD 6.4 billion, with more than 70% of dental clinics worldwide adopting digital or connected practice platforms. North America generated over USD 2.5 billion of the total market value, driven by widespread adoption of digital imaging systems and software platforms integrated with electronic health records. Europe followed with around 28% share, supported by the presence of over 61,000 dental clinics and increasing software integration in treatment planning systems. Asia-Pacific accounted for about 21% of the global demand in 2025, with China, Japan, and India leading investments in dental digitalization. Latin America represented around 6% share, while the Middle East & Africa held nearly 4.8% of the market as dental tourism and healthcare modernization expand across emerging economies.

North America held the largest regional share of approximately 40.2% of the global Connected Dental Equipment and Software Market in 2025, reflecting strong technological adoption across dental clinics, hospitals, and dental support organizations. The United States accounts for the majority of regional demand, with over 72% of dental practices already digitized and using integrated practice management or imaging software systems. Key industries driving demand include dental clinics, multi-clinic dental service organizations (DSOs), orthodontic practices, and academic dental hospitals, all of which rely on connected imaging devices, cloud-based data storage, and AI-enabled diagnostics. Government regulations such as HIPAA compliance requirements and digital healthcare interoperability standards have accelerated adoption of secure cloud-based dental software. In addition, initiatives encouraging electronic health record integration have expanded the market for connected treatment planning systems and imaging equipment. Technological advancements include AI-assisted radiology analysis, cloud-based patient management platforms, and connected intraoral scanners integrated with CAD/CAM systems. A notable regional player, Planet DDS, has expanded its Denticon cloud dental software platform, which supports more than 13,000 dental practices and over 90,000 dental professionals globally, enabling centralized patient data management across multi-location clinics. Consumer behavior in the region shows high enterprise-level adoption, with dental groups prioritizing real-time analytics, automated appointment systems, and remote collaboration tools to improve operational efficiency and patient outcomes.

Europe represented approximately 28% of the global Connected Dental Equipment and Software Market share in 2025, supported by extensive dental care infrastructure and strong regulatory oversight across healthcare technologies. Major markets include Germany, the United Kingdom, France, Italy, and Spain, which collectively account for more than 70% of regional demand for digital dentistry platforms and connected imaging equipment. The region has over 61,000 dental clinics, creating a significant demand for digital patient record systems and practice management software. Regulatory oversight by bodies such as the European Medicines Agency (EMA) and compliance frameworks under GDPR and EU Medical Device Regulations (MDR) have driven the need for secure and explainable digital healthcare platforms. As a result, connected dental software solutions increasingly incorporate advanced encryption, secure cloud data exchange, and interoperable health record systems. Emerging technologies adopted in the region include AI-assisted treatment planning, digital impression systems, and 3D printing integrated with CAD/CAM dental manufacturing workflows. For instance, Planmeca, a Finland-based manufacturer, has expanded its Planmeca Romexis digital platform, enabling integrated imaging, CAD/CAM restoration design, and patient data management within a single connected ecosystem used by thousands of dental clinics. Consumer behavior in the region is influenced by strict regulatory compliance and data transparency requirements, leading to strong demand for explainable AI tools, secure data storage, and interoperable digital dental solutions.

Asia-Pacific ranked third globally in 2025 in terms of total market volume, accounting for approximately 21% of the Connected Dental Equipment and Software Market. The region is driven by large populations, rising oral healthcare awareness, and rapid expansion of private dental clinics. The top consuming countries include China, Japan, India, South Korea, and Australia, which collectively represent more than 80% of regional demand. Infrastructure expansion is a key growth driver. China and India alone have seen thousands of new private dental clinics established over the past decade, many of which are adopting digital imaging systems, intraoral scanners, and cloud-connected patient management platforms. Manufacturing hubs in China and Japan have also accelerated the production of CAD/CAM dental systems, imaging sensors, and digital diagnostic tools. Innovation hubs in cities such as Shenzhen, Tokyo, and Bengaluru are increasingly involved in developing AI-based dental diagnostic software, mobile treatment planning tools, and tele-dentistry platforms. For example, Shining 3D, a China-based dental technology company, has expanded its Aoralscan intraoral scanner ecosystem, enabling real-time cloud data sharing between dentists and dental laboratories. Consumer behavior across Asia-Pacific highlights strong mobile and digital-first adoption patterns, where dental clinics increasingly utilize cloud platforms, mobile AI applications, and e-commerce distribution channels for dental equipment procurement and patient engagement.

South America accounted for approximately 6% of the global Connected Dental Equipment and Software Market in 2025, with Brazil and Argentina representing the largest national markets in the region. Brazil alone accounts for nearly 45% of regional demand, supported by its large dental workforce and expanding private dental clinic networks. The region has experienced growth in dental technology adoption as urban healthcare infrastructure improves and cosmetic dentistry demand increases. Infrastructure trends include expanding private dental clinics, specialized orthodontic centers, and dental tourism services, particularly in Brazil and Colombia. Government incentives for healthcare modernization and favorable trade policies have also facilitated the import and distribution of advanced dental imaging systems and cloud-based practice management platforms. Local companies are increasingly integrating digital technologies. For example, Neodent, headquartered in Brazil, has expanded its digital dentistry solutions by integrating implant planning software with digital scanning systems used in restorative dentistry workflows. Such integrations help dental clinics streamline implant procedures and treatment planning. Consumer behavior in South America is influenced by language localization and regional service networks, with demand rising for software platforms offering Portuguese and Spanish interfaces, localized training programs, and cloud-based remote technical support.

The Middle East & Africa represented approximately 4.8% of the global Connected Dental Equipment and Software Market in 2025, but demand is increasing rapidly as governments invest in healthcare modernization and digital infrastructure. Key growth countries include the United Arab Emirates, Saudi Arabia, South Africa, and Egypt, where dental tourism, private healthcare investment, and digital healthcare initiatives are expanding the adoption of advanced dental technologies. Regional demand is supported by growth in medical tourism, hospital expansion projects, and private dental clinic chains, particularly in the UAE and Saudi Arabia. Healthcare transformation initiatives such as Saudi Vision 2030 encourage the adoption of digital medical technologies, including connected imaging systems and electronic dental record platforms. Technological modernization includes the introduction of AI-assisted imaging diagnostics, cloud-based dental practice management systems, and digital orthodontic treatment planning tools. For example, Dubai-based dental technology distributors and clinics increasingly deploy integrated CAD/CAM systems and digital scanning technologies to support advanced restorative procedures. Consumer behavior in the region varies widely but generally reflects growing demand for premium dental services and digitally enabled treatment planning, particularly among urban populations seeking advanced orthodontic and cosmetic dental solutions.

United States – 22.7% Market Share: Strong digital adoption across dental clinics and widespread deployment of AI-enabled dental imaging and practice management platforms.

Germany – 9.4% Market Share: It’s dominance is supported by advanced dental manufacturing capabilities, extensive clinical infrastructure, and strong adoption of CAD/CAM dental technologies.

The Connected Dental Equipment and Software Market is characterized by moderate fragmentation with strong technological competition, as companies focus on integrating hardware, imaging systems, and cloud-based software into unified digital dentistry ecosystems. The market includes over 120 active global and regional competitors, ranging from large medical device manufacturers to specialized dental software developers and digital dentistry platform providers.

The top five companies collectively account for approximately 38–42% of the global market share, indicating a competitive environment where innovation and ecosystem integration play a critical role in differentiation. Major companies compete through product innovation, AI-enabled diagnostics, strategic partnerships with dental laboratories, and acquisitions of digital dentistry startups.

Technology integration has become a central competitive factor. Companies are increasingly combining intraoral scanners, CBCT imaging systems, and CAD/CAM design software into connected platforms that streamline clinical workflows. Strategic partnerships between equipment manufacturers and cloud software developers are also increasing, enabling seamless patient data management and real-time treatment planning.

In addition, mergers and acquisitions have increased by more than 20% in the digital dentistry sector since 2022, as larger healthcare technology firms acquire specialized software developers and imaging technology providers. The competitive landscape is further shaped by innovation in AI-based diagnostic algorithms, 3D printing integration for dental prosthetics, and tele-dentistry platforms, which are transforming how dental practices deliver care and manage patient data.

Dentsply Sirona

Align Technology

Planmeca Oy

Carestream Dental

Henry Schein Inc.

Patterson Companies

Straumann Group

3Shape A/S

Medit Corp.

Planet DDS

Biolase Inc.

GC Corporation

A-dec Inc.

Curve Dental

Shining 3D

Technological innovation is the primary driver shaping the Connected Dental Equipment and Software Market, with digital dentistry platforms transforming clinical workflows, treatment planning, and patient engagement. One of the most significant developments is the widespread adoption of cloud-based dental practice management systems, which now account for over 78% of new dental software deployments globally. Cloud platforms allow clinics to centralize patient records, integrate imaging systems, and enable remote collaboration between dentists and dental laboratories.

Artificial intelligence is increasingly embedded in dental diagnostic systems. AI-based algorithms can analyze CBCT scans, intraoral images, and digital X-rays to identify cavities, periodontal disease, and structural abnormalities with improved accuracy. In many dental clinics, AI tools now support automated charting, treatment planning, and predictive analytics, helping dentists identify potential oral health risks earlier and improve case acceptance rates.

Another major technological trend is the integration of CAD/CAM (Computer-Aided Design and Manufacturing) technologies with connected dental equipment. Digital impression systems and intraoral scanners generate highly detailed 3D models of a patient’s teeth, which are transmitted to cloud-based design software for prosthetic design and manufacturing. These workflows significantly reduce treatment times by enabling same-day crowns and restorations through in-clinic milling machines and 3D printers.

The adoption of 3D printing in dentistry has also accelerated, particularly for orthodontic aligners, surgical guides, and dental prosthetics. Dental laboratories increasingly rely on connected digital workflows where scanning, design, and printing processes are fully integrated within a digital platform.

Interoperability is another important technological development. Modern dental software platforms are designed to integrate with electronic health record (EHR) systems, imaging hardware, and billing platforms, enabling seamless data exchange. Additionally, emerging standards such as FHIR-based healthcare data exchange protocols are improving connectivity between dental and broader healthcare systems.

Tele-dentistry is also gaining traction as connected equipment and cloud software allow dentists to review imaging scans remotely, conduct virtual consultations, and monitor orthodontic treatment progress through digital platforms. These technological advancements collectively support a more efficient, data-driven, and patient-centric dental care ecosystem.

• In September 2024, the company introduced Primescan 2, described as the first cloud-native intraoral scanning solution powered by the DS Core platform. The wireless scanner allows dentists to scan patients using any internet-connected device, with scan data automatically stored and processed in the cloud to enable collaboration with labs and specialists. Source: www.investor.dentsplysirona.com

• In December 2024, the company expanded its digital platform with DS Core Enterprise, designed specifically for dental service organizations (DSOs). The solution provides centralized dashboards to monitor connected dental equipment, analyze usage across clinics, and manage user accounts and billing through a single enterprise portal.

• In July 2025, the company integrated its CEREC digital dentistry system with the DS Core cloud platform, enabling real-time data sharing between scanning, design, and milling workflows. This integration supports faster same-day dental restorations and more efficient chairside digital treatment workflows.

• In September 2025, the company announced a partnership with Pearl to integrate the Second Opinion AI radiology software into the DS Core platform. The integration enables automatic exchange of X-ray data and provides AI-assisted analysis to help dentists identify cavities and bone loss more accurately.

The Connected Dental Equipment and Software Market Report provides a comprehensive evaluation of the global digital dentistry ecosystem, covering equipment manufacturers, dental software developers, healthcare providers, and dental laboratory networks involved in connected dental technologies. The report examines multiple market segments, including connected dental imaging systems, intraoral scanners, CAD/CAM systems, cloud-based practice management software, AI diagnostic platforms, and tele-dentistry solutions.

From a product perspective, the report analyzes equipment categories such as CBCT imaging systems, intraoral cameras, digital X-ray devices, and chairside CAD/CAM restoration equipment, all of which are increasingly integrated with connected software platforms. Software segments include practice management systems, imaging software, treatment planning tools, patient engagement platforms, and cloud-based dental data management solutions.

The report also evaluates end-user segments including dental clinics, hospitals, dental laboratories, and dental service organizations (DSOs). Dental clinics represent the largest user base globally, accounting for a significant portion of connected equipment deployments, while DSOs increasingly adopt centralized cloud platforms to manage multi-location operations.

Geographically, the report provides analysis across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering more than 25 key countries with varying levels of digital dentistry adoption. Regional analysis examines infrastructure development, regulatory environments, healthcare spending patterns, and technology adoption trends influencing the connected dental ecosystem.

Additionally, the report explores emerging niche segments such as AI-powered dental diagnostics, mobile dental imaging platforms, remote orthodontic monitoring tools, and digital workflow integration between clinics and dental laboratories. By combining technological insights, competitive analysis, and regional demand patterns, the report provides decision-makers with a detailed understanding of current market dynamics and the strategic opportunities shaping the future of connected dentistry.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 860.0 Million |

| Market Revenue (2033) | USD 1,412.6 Million |

| CAGR (2026–2033) | 6.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Danaher Corporation; Dentsply Sirona; Align Technology; Planmeca Oy; Carestream Dental; Henry Schein Inc.; Patterson Companies; Straumann Group; 3Shape A/S; Medit Corp.; Planet DDS; Biolase Inc.; GC Corporation; A-dec Inc.; Curve Dental; Shining 3D |

| Customization & Pricing | Available on Request (10% Customization Free) |