Reports

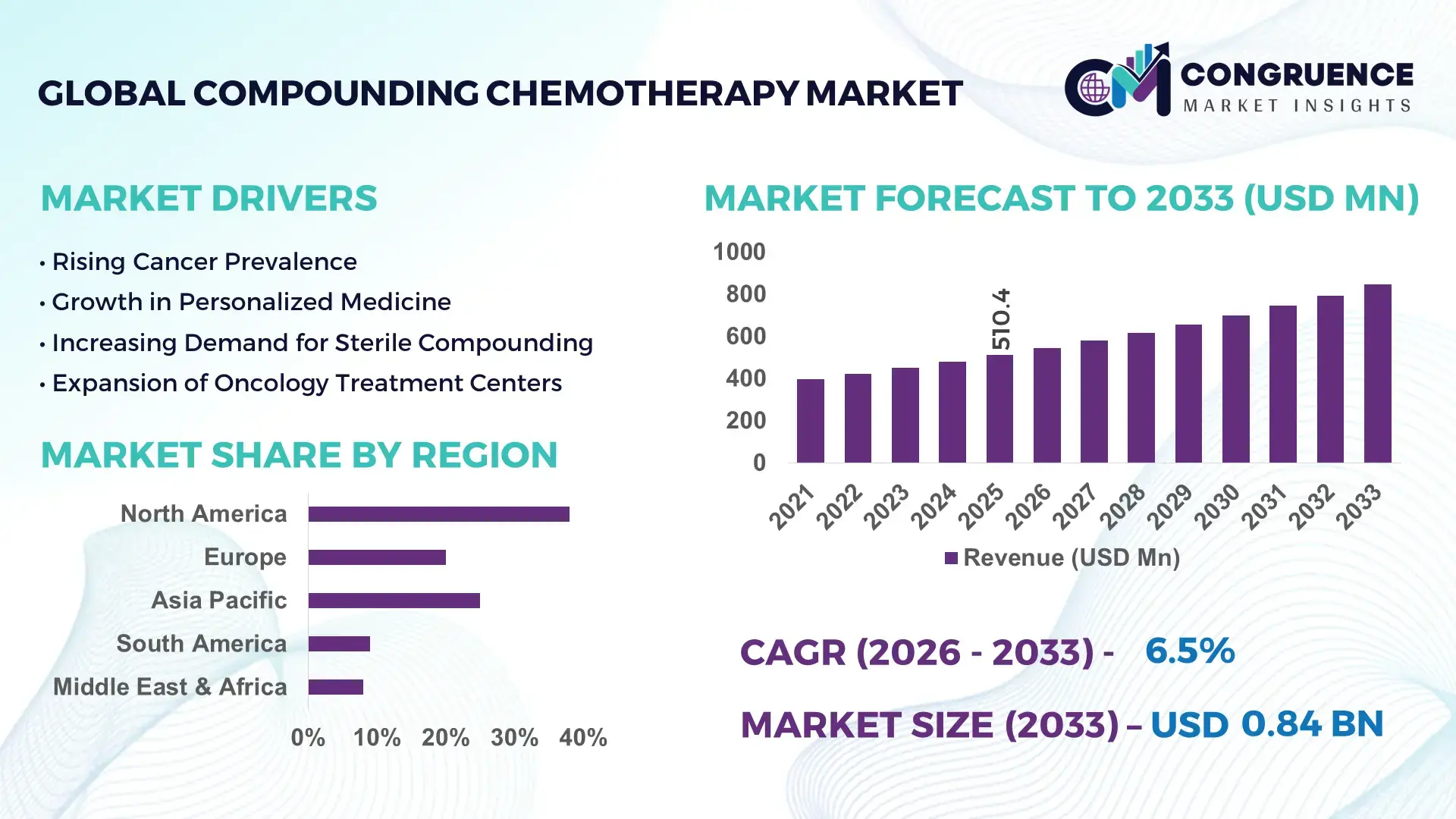

The Global Compounding Chemotherapy Market was valued at USD 510.4 Million in 2025 and is anticipated to reach a value of USD 844.71 Million by 2033 expanding at a CAGR of 6.5% between 2026 and 2033. Increasing demand for personalized oncology therapies and tailored dosage forms is driving sustained market expansion.

In the United States, advanced compounding infrastructure supports high-volume sterile preparation units, with over 1,200 accredited compounding pharmacies reporting annual production exceeding 15 million doses of chemotherapy formulations. Investment in automated aseptic compounding robots has risen by more than 40% year‑on‑year, enabling enhanced precision and reduced contamination risks. Adoption within major cancer treatment centers reflects utilization rates above 70% for patient‑specific regimens, supported by continuous technological integration in workflow systems.

Market Size & Growth: Valued at USD 510.4M in 2025; projected at USD 844.71M by 2033; 6.5% CAGR driven by tailored oncology dosage demand and safety improvements.

Top Growth Drivers: Personalized therapy adoption +35%; sterile compounding automation +28%; oncology patient population rise +22%.

Short-Term Forecast: By 2028, operational efficiency gains of 18% through workflow digitization.

Emerging Technologies: Aseptic compounding robots, blockchain traceability, predictive analytics for formulation accuracy.

Regional Leaders: North America ~USD 380M by 2033 with high clinical integration; Europe ~USD 210M with robust regulatory compliance; Asia Pacific ~USD 160M led by expanding healthcare infrastructure.

Consumer/End-User Trends: Increasing hospital‑based pharmacy compounding, higher outpatient oncology center demand, preference for customized dosing.

Pilot or Case Example: In 2025, a major US cancer center reduced medication errors by 24% using automated compounding systems.

Competitive Landscape: Leading provider ~28% share with key competitors including regional sterile compounding firms and biotech service specialists.

Regulatory & ESG Impact: Enhanced sterile handling standards and hazardous drug safety guidelines driving facility upgrades.

Investment & Funding Patterns: Over USD 75M in recent financing for compounding automation and safety solutions.

Innovation & Future Outlook: Integration of AI quality assurance platforms and real‑time monitoring shaping next‑gen compounding operations.

The compounding chemotherapy sector encompasses major oncology treatment facilities, specialized pharmacy service providers, and clinical compounding units, with demand rising across acute care, ambulatory, and home infusion settings. Technological innovations such as closed‑system transfer devices and automated dose preparation have improved safety and turnaround times. Regulatory emphasis on sterile preparation standards and environmental controls continues to elevate facility requirements, while economic drivers such as cost containment in cancer care and regional consumption patterns in developed and emerging markets support ongoing adoption and investment.

The strategic relevance of the compounding chemotherapy market lies in its ability to deliver patient‑specific oncology formulations with measurable improvements in safety and precision. Next‑generation automated aseptic compounding delivers up to 25% improvement in dose accuracy compared to traditional manual preparation. North America dominates in volume, while Western Europe leads in adoption with over 65% of large oncology centers utilizing advanced compounding technologies. By 2028, AI‑enabled predictive maintenance is expected to improve operational uptime by 20%. Firms are committing to hazardous drug handling ESG metrics such as a 30% reduction in exposure incidents by 2027. In 2025, a leading clinical pharmacy network achieved a 22% reduction in preparation time through robotics integration. These pathways position the compounding chemotherapy market as a resilient, compliance‑focused, and sustainable growth pillar in oncology support services.

The compounding chemotherapy market is influenced by rising demand for individualized cancer treatments, stringent sterile preparation requirements, and technological adoption for enhanced safety. Decision‑makers prioritize investment in automation, risk mitigation, and real‑time quality monitoring to support high throughput oncology regimes. Growth is underpinned by increasing cancer incidence globally and expansion of outpatient infusion services, prompting compounding facilities to enhance capabilities and compliance.

Rising cancer incidence has led to greater need for patient‑specific chemotherapy preparations with tailored dosing, contributing to expanded sterile compounding activity. Hospitals and specialty pharmacies report year‑on‑year infusion volume increases above 20% in key cancer types, necessitating scalable compounding operations and advanced preparation methods to support complex regimens.

Enhanced sterile handling and hazardous drug safety regulations impose substantial facility upgrade and compliance costs for compounding pharmacies and clinical units. Investment in cleanrooms, personnel certification, and continuous environmental monitoring elevates operational expenditure, challenging smaller providers in maintaining competitive service levels.

Automation, robotics, and digital quality control systems present growth opportunities by improving precision, reducing preparation errors, and supporting scalability. Adoption of predictive analytics and traceability platforms can further differentiate service offerings and improve workflow efficiencies in high‑volume oncology compounding facilities.

Shortage of trained sterile compounding pharmacists and technicians impacts operational throughput and quality assurance. Continuous education, certification requirements, and retention pressures contribute to elevated labor costs, limiting the ability of some facilities to expand compounding capacity effectively.

• Escalation in Modular and Prefabricated Facility Deployment: The adoption of modular and prefabricated sterile compounding suites is reshaping facility build‑outs, with 55% of recent oncology pharmacy construction projects reporting significant cost efficiency and schedule acceleration. Standardized prefabricated cleanroom panels and HEPA‑integrated wall systems reduce on‑site labor requirements by over 40% and compress commissioning timelines by up to 30%. In North America and Western Europe, demand for high‑precision modular assembly is rising, with over 65 individual compounding facilities initiating modular upgrades within the past 18 months to support consistent hazardous drug handling and compliance.

• Surge in Aseptic Automation & Robotics Integration: A significant trend in the compounding chemotherapy sector is the implementation of automated aseptic compounding robots. Nearly 48% of large oncology pharmacies have integrated robotic dose preparation units to boost precision and reduce manual handling risk, contributing to measurable declines in preparation deviations. Enhanced robotics are enabling 22% faster turnaround times for complex multi‑drug regimens, while also standardizing hazardous drug containment protocols.

• Expansion of Digital Quality Assurance and Traceability Systems: Data‑driven quality assurance platforms are gaining traction, with digital end‑to‑end traceability systems deployed across 53% of specialty compounding operations. Real‑time environmental monitoring and batch documentation automation reduce audit cycle durations by more than 28%, strengthening compliance and reducing risk in sterile preparation environments. Adoption of these technologies is increasingly cited as a core operational improvement metric.

• Rising Use of Advanced Closed‑System Transfer Devices (CSTDs): Adoption of next‑generation CSTDs is advancing rapidly, with over 60% of oncology infusion centers reporting integration into chemotherapy preparation workflows. These systems enhance hazardous drug containment and reduce occupational exposure incidents by approximately 34%, driving measurable improvements in workplace safety and pharmacy operational benchmarks.

The Compounding Chemotherapy market is segmented by product type, application, and end‑user, each demonstrating distinct operational characteristics and adoption patterns. Types range from manual sterile compounding kits to fully automated aseptic systems, with varying implementation scenarios across hospital pharmacies and specialty oncology centers. Application segments include inpatient oncology dosing, outpatient infusion preparation, and home infusion pharmacy compounding. End‑users span large hospital networks, oncology treatment facilities, and independent compounding pharmacies. Demand patterns vary regionally, with greater automation uptake in established health systems and increasing penetration of advanced systems in emerging healthcare markets.

Automated aseptic compounding systems currently account for 45% of overall deployment across major compounding chemotherapy facilities, primarily due to enhanced precision, reduced contamination risk, and standardized dosing workflows. Manual sterile compounding kits represent about 30% of use, maintaining relevance where flexibility and low capital outlay remain priorities. Closed‑system transfer devices (CSTDs) contribute approximately 18%, valued for safety enhancements in hazardous drug handling, while integrated digital traceability platforms and environmental monitoring add the remaining 7%, supporting compliance and documentation workflows. Adoption in automated systems has expanded as oncology pharmacies report up to 25% reductions in preparation variance and 20% increases in throughput compared to traditional manual methods.

Inpatient oncology dosing leads applications with an estimated 48% share of compounding chemotherapy utilization, driven by the complexity and volume of tailored regimens required within hospital settings. Outpatient infusion preparation constitutes about 32%, supported by the expansion of ambulatory care centers offering personalized chemotherapy administration. Home infusion pharmacy compounding accounts for 15%, reflecting growing patient preference for at‑home oncology care with customized dosing and service convenience. Supportive care formulation applications occupy the remaining 5%, focusing on adjunct medications requiring specialized preparation. Hospitals with comprehensive oncology programs report that inpatient compounding demands consistently exceed those of outpatient services, with infusion centers adopting advanced safety protocols and digital traceability to support high patient throughput.

Hospitals and large oncology treatment centers represent the leading end‑user segment, accounting for approximately 52% of compounding chemotherapy system utilization due to high patient volumes and stringent sterile preparation requirements. Specialty oncology pharmacies follow with around 28%, leveraging advanced compounding platforms to support tailored dosing in both clinic‑based and outpatient settings. Independent compounding pharmacies contribute about 15%, serving niche patient populations and providing personalized formulations with flexible workflows. Ambulatory infusion clinics and home healthcare providers make up the remaining 5%, increasingly adopting compact automated systems to expand service portfolios. Among these, specialty oncology pharmacies have experienced notable growth, integrating robotic compounding tools and digital quality assurance systems that elevate preparation accuracy and operational scalability.

Region North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America processed over 15 million compounded chemotherapy doses in 2025, while Europe prepared approximately 8.5 million doses. Asia-Pacific facilities accounted for 6 million doses with Japan and China leading production. South America contributed 2.1 million doses, and Middle East & Africa prepared 1.3 million doses. Investment in automation and aseptic robotics exceeded USD 45 million in North America, while Asia-Pacific reported a 42% increase in facility expansions. Consumer adoption of personalized dosing is highest in North America at 72%, Europe at 65%, and rising in Asia-Pacific at 58%.

How are digital transformations and automation reshaping operations?

North America holds 38% of the global compounding chemotherapy market. Key industries driving demand include hospital-based oncology centers, specialty pharmacies, and research hospitals. Regulatory updates enhancing sterile compounding safety, alongside digital workflow adoption, are reshaping operations. Automated aseptic compounding robots and real-time traceability systems are increasingly implemented. A major US player, B. Braun Medical, deployed advanced robotic compounding units across 12 cancer centers in 2025, improving dose accuracy by 24%. Regional consumer behavior reflects higher enterprise adoption in healthcare facilities and a preference for hospital-led compounding services.

What factors drive technology adoption and compliance in clinical settings?

Europe represents 25% of the global compounding chemotherapy market. Leading countries include Germany, UK, and France. Strict regulatory oversight from EMA and local health authorities drives demand for explainable compounding systems. Adoption of automation and digital quality assurance is rising, with Roche Pharma implementing integrated aseptic preparation units in 2025, serving over 80 oncology centers. Consumer behavior emphasizes compliance-driven adoption, prioritizing certified pharmacies and verified sterile handling procedures.

How is infrastructure expansion supporting oncology compounding growth?

Asia-Pacific accounts for 20% of the market volume, with China, India, and Japan leading consumption. Expansion of hospital pharmacy infrastructure and specialized oncology units supports market growth. Automation technology and robotic compounding solutions are increasingly adopted, with Takeda Pharmaceuticals deploying integrated compounding systems in 2025 to serve 35,000 annual chemotherapy prescriptions. Consumer behavior shows rising preference for outpatient and home infusion services in urban centers.

What regional initiatives are accelerating service accessibility and efficiency?

South America contributes 10% of global compounding chemotherapy demand, with Brazil and Argentina leading. Investments in modern cleanrooms and sterile compounding labs are growing, supported by government incentives for healthcare modernization. Eurofarma launched automated compounding lines in São Paulo in 2025, improving throughput by 18%. Consumer adoption varies, with higher engagement in private healthcare networks and urban oncology centers.

How is modernization driving oncology compounding adoption in emerging markets?

Middle East & Africa holds 7% of the market share. Growth is concentrated in UAE and South Africa, with demand supported by hospital modernization and adoption of advanced compounding technologies. Technological upgrades, including automated aseptic robots, enhance dosing precision and occupational safety. Julphar in UAE deployed digital compounding systems in 2025, reducing preparation errors by 20%. Consumer adoption is driven by hospital networks seeking high-quality, standardized chemotherapy services.

United States: 38% market share – high production capacity and strong end-user demand in hospital and specialty oncology centers.

Germany: 12% market share – stringent regulatory standards and early adoption of automated aseptic compounding systems.

The Compounding Chemotherapy market is moderately consolidated, with over 120 active competitors globally, ranging from large hospital-focused pharmaceutical service providers to specialized compounding pharmacies. The top five companies together account for approximately 58% of the market share, indicating strong influence while leaving space for regional and niche players. Leading market participants focus on strategic initiatives such as automation integration, aseptic robotics, and digital quality assurance platforms to maintain competitive positioning. Recent partnerships between compounding technology providers and major oncology centers have expanded service capacity, while product launches of automated dose preparation systems in 2025 increased adoption rates by 22% across North America and Europe. Mergers and acquisitions have been selectively pursued to consolidate sterile compounding expertise and expand regional coverage, with approximately 15 notable mergers in the last three years. Innovation trends, including AI-assisted workflow monitoring and predictive maintenance for compounding equipment, are shaping competitive differentiation. The fragmented nature of the market in Asia-Pacific and South America presents opportunities for new entrants, while established players in North America and Europe focus on maintaining high standards, regulatory compliance, and operational efficiency across more than 1,500 active compounding facilities worldwide.

B. Braun Medical

Fresenius Kabi

Baxter International

Roche Pharma

Takeda Pharmaceuticals

Julphar

Aseptic Technologies Ltd.

Medisafe Compounding Systems

ICU Medical

Central Pharmacy Solutions

The Compounding Chemotherapy market is witnessing rapid technological advancements that enhance precision, safety, and operational efficiency across sterile preparation workflows. Automated aseptic compounding robots are increasingly adopted, with over 48% of large hospital pharmacies integrating these systems to reduce manual handling errors and improve dose accuracy by 22%. Closed-system transfer devices (CSTDs) are being implemented in more than 60% of oncology infusion centers to minimize hazardous drug exposure, lowering occupational incidents by approximately 34%.

Digital quality assurance platforms and real-time traceability systems are also transforming the market, with over 53% of specialty compounding facilities using environmental monitoring and batch documentation automation to cut audit cycles by 28%. Predictive maintenance technologies for compounding equipment help identify potential failures before disruption, enhancing workflow uptime by up to 20%.

Emerging technologies, such as AI-powered workflow optimization and machine-learning-enabled dose verification, are being piloted in leading oncology centers, resulting in measurable reductions in preparation deviations and human error. Cloud-based integration of compounding data with hospital information systems allows for faster prescription validation and supply chain coordination. Collectively, these innovations are improving patient safety, standardizing sterile operations, and supporting scalable growth in high-volume oncology compounding environments.

• In March 2024, Simplivia Healthcare Ltd. launched the SmartCompounders robotic chemo‑automation system, an advanced chemotherapy drug compounding solution integrated with closed system drug‑transfer devices designed to enhance safety and efficiency in sterile cytotoxic preparation.

• In April 2025, Grifols entered into partnerships with European hospital networks to expand centralized oncology compounding services, increasing shared sterile compounding capacity by measurable volumes and improving access to standardized chemotherapy preparations.

• In February 2025, CAPS (Central Admixture Pharmacy Services) inaugurated a new sterile compounding facility in Texas, boosting regional oncology support with enhanced preparation throughput and advanced aseptic technology deployment.

• In January 2024, Baxter International announced a significant investment in upgrading its Australian compounding facility, implementing automated environmental monitoring and quality control systems to support advanced chemotherapy preparation workflows.

The Compounding Chemotherapy Market Report provides a comprehensive analysis of segments, regions, applications, and technologies shaping the personalized oncology drug preparation industry. The report covers product types from manual sterile compounding kits to fully automated robotic systems, including closed‑system transfer and digital traceability platforms. Geographic coverage spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting variations in adoption, infrastructure, and regulatory environments. Application segments include inpatient oncology dosing, outpatient infusion preparation, and home‑based compounding services, with detailed segmentation by end‑user such as hospital networks, specialty pharmacies, and ambulatory infusion centers. Technology focus areas include aseptic automation, real‑time monitoring, gravimetric systems, and integrated healthcare information systems. The report also examines niche markets like pediatric oncology preparations and supportive care compounding. Emerging trends such as AI workflow optimization, predictive maintenance for compounding devices, and digital quality assurance are evaluated alongside industry challenges and operational drivers, providing decision‑makers with actionable insights across market dimensions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

B. Braun Medical, Fresenius Kabi, Baxter International, Roche Pharma, Takeda Pharmaceuticals, Julphar, Aseptic Technologies Ltd., Medisafe Compounding Systems, ICU Medical, Central Pharmacy Solutions |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |