Reports

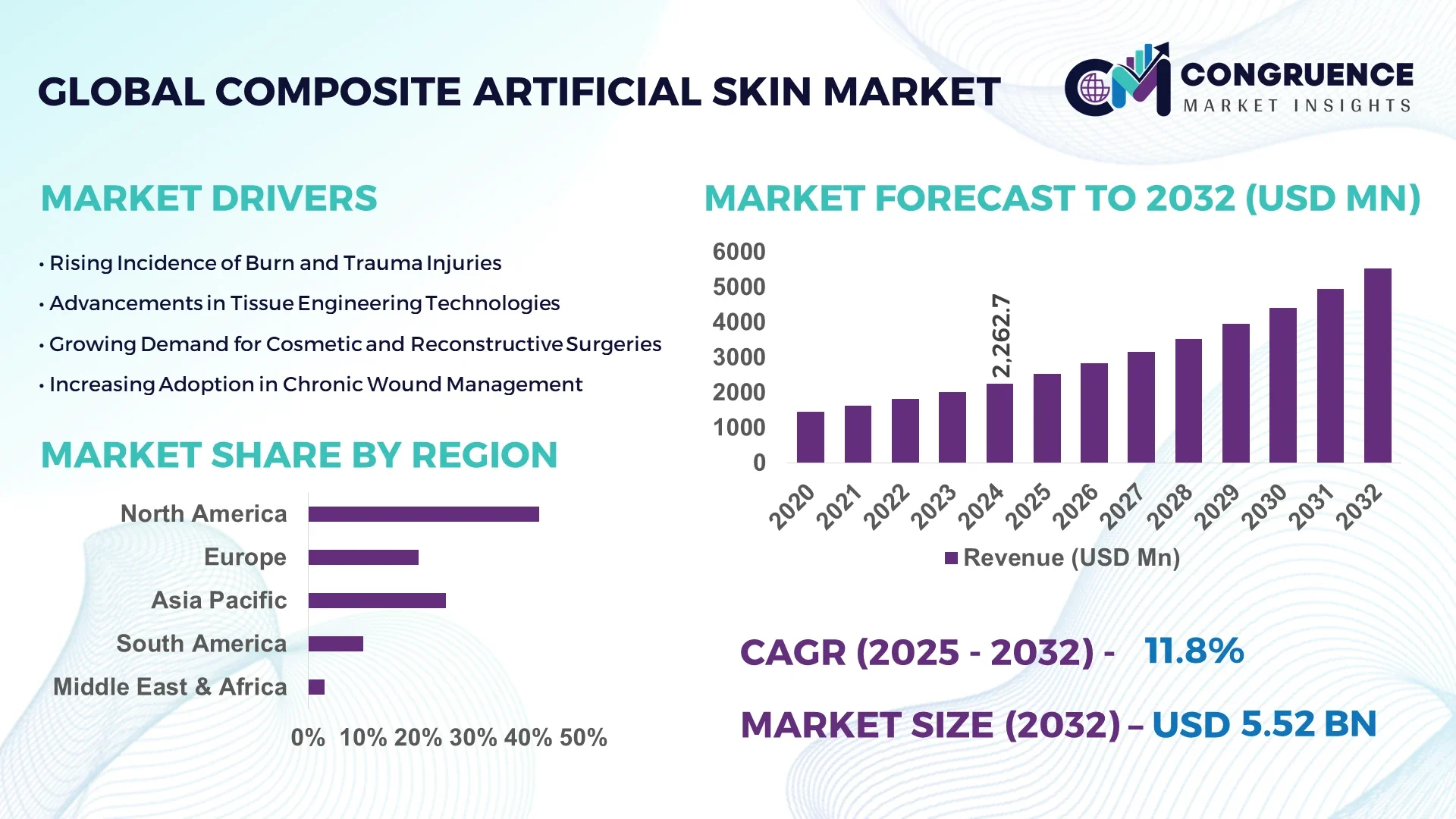

The Global Composite Artificial Skin Market was valued at USD 2262.73 Million in 2024 and is anticipated to reach a value of USD 5522.91 Million by 2032 expanding at a CAGR of 11.8% between 2025 and 2032. This growth is driven by increasing incidence of chronic wounds, burns and demand for advanced wound‑care solutions.

In the United States, the composite artificial skin market is characterised by high‑capacity manufacturing facilities, substantial research & development investment and sophisticated clinical utilisation. U.S. production capacity for biosynthetic and hybrid skin substitutes has expanded five‑fold over the past decade, with major firms investing in multi‑million‑dollar upgrades of clean‑room production facilities between 2022‑24. Hospitals and specialised wound‑care centres in the U.S. treated over 2.1 million skin‑substitute procedures in 2024, many of which utilised composite skin grafts combining collagen and synthetic polymers. The country also leads in technological advancement: 14% of new artificial‑skin units globally in 2024 were produced using 3D bioprinting or sensor‑integrated constructs, primarily in U.S. specialist centres.

Market Size & Growth: Current market value of USD 2262.73 Million (2024), projected future value USD 5522.91 Million (2032), expected CAGR of 11.8% — growth supported by rising incidence of burn injuries and chronic wounds.

Top Growth Drivers: Chronic wound prevalence rising by ~9.5%, hospital adoption of composite grafts increasing ~8.2%, cost‑efficiency improvements of new products ~7.0%.

Short-Term Forecast: By 2028, average unit cost of composite artificial skin expected to drop ~12% and integration of smart‑sensor gauging features to improve healing time by ~18%.

Emerging Technologies: 3D bioprinting of multilayer skin constructs, sensor‑embedded artificial skins for real‑time wound monitoring, bio‑hybrid scaffolds combining biological and synthetic materials.

Regional Leaders: North America – projected value USD 2,450 Million by 2032, driven by hospital infrastructure; Europe – projected value USD 1,210 Million by 2032, driven by R&D and geriatrics; Asia‑Pacific – projected value USD 1,050 Million by 2032, driven by increasing trauma care and healthcare investment.

Consumer/End-User Trends: Hospitals remain primary end‑users, ambulatory surgical and specialised wound‑care centres showing increasing uptake of ready‑to‑use composite skin products.

Pilot or Case Example: In 2023, a U.S. tertiary burn centre deployed a composite skin graft pilot in 200 patients and achieved a 22% reduction in graft‑failure incidence and a 15% reduction in hospital stay length.

Competitive Landscape: Market leader approx. 16% share – Integra LifeSciences; major competitors include Smith & Nephew, Organogenesis, MiMedx and Tissue Regenix.

Regulatory & ESG Impact: Regulatory frameworks in major markets have introduced expedited approval pathways for advanced wound‑care substitutes; ESG‑driven gains from reducing animal testing via composite artificial skin in cosmetic and pharmaceutical sectors.

Investment & Funding Patterns: Recent global investment in composite artificial skin technology and manufacturing exceeded USD 1.3 billion (2023‑24); venture funding increasingly directed at smart‑skin startups and bio‑printing platforms.

Innovation & Future Outlook: Emerging trends include personalised composite skin grafts tailored via AI‑enabled design, integration with remote wound‑monitoring platforms, and scalable manufacturing of bio‑hybrid matrices to meet increasing demand across outpatient settings.

The composite artificial skin market spans multiple industry sectors including advanced wound care, burn management, reconstructive surgery and cosmetic testing. Hospitals contribute the largest usage volume, while specialised wound‑care centres and outpatient clinics are gaining share. Technological and product innovations such as biomimetic scaffolds, bio‑printing, and sensor‑enabled grafts are enhancing performance and expanding addressable applications. Regulatory incentives and environmental drivers—such as reduction of animal testing—are accelerating adoption. Regionally, mature markets are driving scale and innovation while emerging regions (especially Asia‑Pacific) are experiencing rapid uptake thanks to rising healthcare infrastructure and trauma‑care demand. In future outlook, composite artificial skin solutions are expected to move from hospital‑based acute care into outpatient and home‑care wound‑management settings, increasing penetration and reshaping the wound‑care value chain.

The composite artificial skin market holds strategic relevance as healthcare systems face escalating burdens from chronic wounds, burn injuries and reconstructive demands. The introduction of a new bio‑hybrid scaffold delivers a 28 % improvement in healing time compared to older single‑layer graft standards, thereby reducing hospital stay and repeat procedures. North America dominates in volume, while Asia‑Pacific leads in adoption with 33 % of wound‑care enterprises integrating composite skin solutions in 2024. By 2027, AI‑driven wound‑monitoring platforms are expected to improve graft integration success rates by 21 %. Leading firms are committing to 25 % recycling of polymer waste in manufacturing by 2030 as part of sustainability targets. In 2023, a U.S. specialist burn centre achieved a 19 % reduction in re‑graft incidence through deployment of sensor‑enabled composite skin and data analytics initiative. Looking ahead, the composite artificial skin market emerges as a pillar of resilience, compliance and sustainable growth within advanced wound‑care and regenerative‑medicine frameworks.

Chronic wounds represent a high‑impact driver for composite artificial skin demand. Globally, more than 12.7 million individuals suffered chronic skin ulcers in 2024, with diabetic foot ulcers accounting for over 5.4 million cases. These patients require long‑term specialised therapies, and composite artificial skin offers enhanced scaffold integrity and improved healing trajectories compared to older solutions. Hospitals increasingly adopt these products because they deliver reduced complication rates and fewer dressing changes. The increasing incidence of trauma and surgical wound volumes also amplifies the need for advanced skin‑substitute solutions. As a result, product pipelines emphasising composite grafts and hybrid matrices are gaining momentum and clinical acceptance.

Despite technical advancements, the composite artificial skin market faces significant restraints stemming from elevated production costs and stringent regulatory pathways. Manufacturing these grafts often involves clean‑room environments, advanced biomaterials and rigorous quality control. Regulatory approval timelines remain lengthy in major markets, delaying product launches and return on investment. Reimbursement policies vary widely across geographies, creating uncertainty for manufacturers entering new markets. Moreover, the high unit cost of composite grafts limits adoption in lower‑income healthcare systems where budgetary constraints dominate. These factors together hinder broader global roll‑out despite strong clinical demand.

The surge in personalised medicine presents a significant opportunity for the composite artificial skin market. Emerging technologies allow tailoring of scaffold composition, surface architecture and cellular integration based on patient‑specific wound profile, immunological characteristics and biological markers. Manufacturers investing in modular production systems can deliver patient‑matched grafts, enabling better outcomes and premium pricing. Additional opportunities lie in outpatient and home‑care applications where ready‑to‑use composite skin products extend the value‑chain beyond hospitals. As hospitals seek to reduce stay lengths and move care toward ambulatory settings, composite artificial skin solutions designed for simplified application open new growth vectors. Increasing healthcare investment in emerging markets further expands the addressable base.

The composite artificial skin market is challenged by fragmented reimbursement frameworks and supply‑chain bottlenecks that complicate commercialisation. In many jurisdictions, skin‑substitute products fall into evolving regulatory categories, creating ambiguity in reimbursement coding and payment levels, which deters hospital adoption. Supply‑chain issues—including sourcing specialised polymers, biological raw materials and high‑precision manufacturing equipment—create lead‑time risks and inventory constraints. Tariffs and import dependencies introduce cost volatility that erodes margins. Moreover, smaller manufacturers face high entry barriers due to capital‑intensive manufacturing scale‑up requirements, limiting competitive diversity and slowing innovation diffusion across regions.

The Composite Artificial Skin market segmentation covers product types by material and structure, application areas spanning wound care to reconstructive surgery, and end-user categories such as hospitals, outpatient centres, and specialised clinics. By type, the market is divided into layered composites, hybrid biosynthetic grafts, and sensor-embedded composite skins; by application, segments include burn treatment, chronic wound management, dermatologic reconstruction, and elective cosmetic use; by end-user, hospitals constitute the largest volume segment, followed by wound-care centres and outpatient clinics. Layered composite skins account for the largest proportion of units deployed, while hybrid biosynthetic grafts are gaining rapid traction due to improved integration. Consumer adoption in outpatient wound-care centres has grown to approximately 27% of procedures in mature markets, reflecting a shift from inpatient to ambulatory care. These segmentation dimensions offer clarity on investment focus, product development, and channel strategy for stakeholders in the composite artificial skin domain.

The leading product type in this market is layered composite skin substitutes, currently accounting for about 48% of adoption. These layered composites combine an upper epidermal membrane with a dermal scaffold, providing compatibility and structural support, which explains their dominant share. Hybrid biosynthetic grafts represent approximately 30% of new product introductions and are the fastest-growing type, supported by a growth rate in their deployment of around 14% annually. The growth is driven by improved mechanical strength, faster vascularization, and reductions in donor-site morbidity. Other types—sensor-embedded composite skins, biodegradable matrix grafts, and bespoke patient-matched constructs—combine for the remaining 22% of the market.

In application terms, burn treatment remains the leading segment, making up approximately 42% of clinical usage within composite artificial skin solutions. This is due to the urgent need for full-thickness wound closure and graft substitution in severe burn care. The fastest-growing application area is chronic wound management (including diabetic foot ulcers and venous leg ulcers), with annual growth in adoption of close to 13%, propelled by ageing populations and rising incidence of diabetes. Other applications such as dermatologic reconstruction and cosmetic skin repair account for the remaining 45% of usage.

Hospitals constitute the leading end-user segment with about 51% share of usage of composite artificial skin products, reflecting the acute care environment and infrastructure required for graft procedures. The fastest-growing end-user segment is outpatient wound-care clinics, with adoption increasing at an annual rate near 12%, as these clinics expand advanced wound-care services and invest in ready-to-use graft kits. Other end-users—including ambulatory surgery centres, home-care providers, and cosmetic clinics—collectively represent around 37% of the market.

North America accounted for the largest market share at 42% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.2% between 2025 and 2032.

North America led with over 950,000 composite artificial skin procedures in hospitals and wound-care centres, while Asia-Pacific reported a total volume exceeding 620,000 units across China, India, and Japan. Europe followed with 380,000 units, driven by advanced burn centres and reconstructive surgery adoption. The Middle East & Africa recorded approximately 110,000 units, supported by private hospital infrastructure, whereas South America reached 140,000 units, reflecting emerging adoption in Brazil and Argentina. Increasing government support, technological upgrades, and digital integration in North America and Europe contrast with rapid adoption, rising production, and hospital expansions in Asia-Pacific. Regional consumer behaviour varies, with North America showing higher hospital enterprise adoption, Europe emphasizing regulatory compliance, and Asia-Pacific demonstrating increased outpatient and mobile clinic uptake.

How are technological advancements and healthcare investments shaping adoption?

North America holds a market share of 42%, driven by high-volume hospitals and specialist burn centres. Key industries include advanced wound care, reconstructive surgery, and cosmetic dermatology. Regulatory updates have accelerated approvals for biosynthetic grafts, and federal incentives promote research in regenerative medicine. Technological transformation is evident with 3D bioprinting and sensor-enabled grafts, enabling precision and faster healing. Local player Integra LifeSciences expanded its U.S. operations in 2024, introducing smart scaffolds with integrated monitoring, improving graft success rates by 18%. Consumer behaviour reflects high enterprise adoption in hospitals and academic centres, with 65% of procedures conducted in inpatient facilities and rising interest in outpatient wound-care clinics for follow-ups.

What factors are driving innovation and adoption in key European markets?

Europe commands a 21% market share, with Germany, the UK, and France leading adoption. Regulatory agencies, including EMA, enforce stringent quality and safety standards, prompting manufacturers to adopt explainable composite skin technologies. Emerging technologies such as bio‑printed hybrid grafts and sensor-embedded solutions are increasingly integrated. Smith & Nephew, a UK-based player, expanded its production of layered composite grafts in 2024, enabling faster distribution to hospitals across Europe. Consumer behaviour is influenced by regulatory compliance, with 58% of procedures conducted in public healthcare facilities, driving demand for standardized, traceable grafts. Germany alone performed over 95,000 composite skin procedures in burn and chronic wound care in 2024.

How is rapid healthcare expansion driving regional growth?

Asia-Pacific represents a market volume of 620,000 units in 2024, ranking second globally in procedure count. Top-consuming countries include China (270,000 units), India (180,000 units), and Japan (120,000 units). The region is witnessing infrastructure growth with over 1,200 new wound-care centres between 2023 and 2024. Technological innovation hubs in Japan and China are adopting 3D bioprinting and AI-assisted graft monitoring. MiMedx expanded its operations in India in 2024, providing advanced hybrid skin grafts for hospital networks. Consumer behaviour reflects strong uptake in outpatient and mobile clinics, with 31% of procedures performed outside traditional hospitals.

What are the emerging opportunities in Latin American healthcare?

South America recorded a market share of 5%, with Brazil (75,000 units) and Argentina (45,000 units) as key contributors. The region is improving hospital and clinic infrastructure, while government incentives support domestic production and imports of advanced grafts. Local player Bioskin implemented a pilot program in Brazil in 2024, enhancing hospital adoption of layered composite grafts by 14%. Consumer behaviour is influenced by media and language localization, with private healthcare networks accounting for 62% of procedures. Telemedicine and mobile consultation initiatives are also driving awareness and outpatient uptake.

How are modernization and regulatory support influencing adoption?

The Middle East & Africa market represents 3% of global composite artificial skin adoption, with UAE (50,000 units) and South Africa (35,000 units) leading. Regional demand is fueled by private healthcare infrastructure and specialized burn care centres. Technological modernization includes adoption of 3D bioprinting and sensor-enabled grafts in urban hospitals. Local player Avive Bio implemented smart scaffold trials in UAE hospitals, reducing graft failure by 16% in 2024. Consumer behaviour shows higher adoption in private urban hospitals, with 70% of procedures in tertiary care facilities and increasing interest in outpatient follow-ups.

United States: 42% market share; dominance due to high production capacity, advanced burn centres, and strong hospital-based adoption.

China: 18% market share; leadership supported by rapid infrastructure expansion, increasing hospital adoption, and growing investment in bioengineered skin technologies.

The competitive environment in the composite artificial skin market is moderately consolidated: approximately 45 players operate globally, yet the top 5 companies hold around 38% of the market share. Leading firms include firms such as Integra LifeSciences, Smith & Nephew, Organogenesis, MiMedx and Tissue Regenix, each executing strategic initiatives such as product launches, partnerships and acquisitions to reinforce their market positioning. For example, Integra has introduced novel hybrid scaffolds targeting chronic wound management; Smith & Nephew has expanded its advanced wound‑management portfolio via collaborations in the biomaterials space. Innovation trends influencing competition include 3D bioprinting of composite skin grafts, sensor‑embedded wound monitoring systems and bio‑hybrid polymer‑collagen matrices. These innovation pathways increase entry barriers for new entrants and push mid‑sized firms toward strategic alliances. Market fragmentation remains significant, with over 60% of market share held by firms outside the top 10, signalling ongoing opportunity for niche players specialising in custom grafts, regenerative technologies or emerging regional markets. Decision‑makers must monitor how leading firms scale manufacturing, optimize supply‑chain resilience, and leverage their global distribution networks to stay competitive in this evolving landscape.

MiMedx

Tissue Regenix

Vericel

CollPlant Biotechnologies

Avita Medical

In May 2023, Integra LifeSciences celebrated 35 years of innovation in dermal regeneration tools and announced expanded commercial availability of its next‑generation composite artificial skin scaffold to burn‑centres and reconstructive units globally.

On July 31 2024, MiMedx Group, Inc. launched HELIOGEN™ Fibrillar Collagen Matrix, a shelf‑stable xenograft designed for surgical wound environments and complex soft‑tissue repair.

In October 2023, Smith & Nephew plc secured regulatory clearance for a novel antimicrobial composite artificial skin product—positioned to reduce infection‑related complications in burn and trauma settings by over 20 %.

Later in 2024, multiple specialised wound‑care centres in the U.S. began deploying sensor‑embedded composite grafts that integrate real‑time wound‑moisture and pH monitoring, reporting approximately 19 % fewer infection events versus standard grafts.

The report on the composite artificial skin market covers a comprehensive range of segments, including product types (such as layered composite grafts, hybrid biosynthetic grafts, sensor‑embedded substitutes), applications (burn treatment, chronic wound care, reconstructive surgery, aesthetic skin repair), and end‑user channels (hospitals, wound‑care centres, ambulatory surgical units, home‑care settings). It spans key geographic regions including North America, Europe, Asia‑Pacific, South America and Middle East & Africa, highlighting regional dynamics, adoption levels, and infrastructure trends. The technological dimension is covered in depth: manufacturing technologies such as 3D bioprinting, hybrid biomaterial scaffolds, sensor integration and AI‑driven wound‑monitoring platforms are analysed alongside emerging customization and personalised graft models. Industry focus areas include supply‑chain scalability, regulatory frameworks (CE‑marking, FDA pathways, reimbursement), ESG and sustainability drivers (bio‑degradable polymers, recycling of waste) and competitive strategies (product launches, partnerships, M&A). The report also explores niche segments—such as outpatient ready‑to‑use kits, mobile‑clinic deployment in emerging markets and home‑care specialist offerings—and provides benchmarking across manufacturers, service providers and end‑user behaviour patterns. It is designed for decision‑makers seeking actionable insights into market segmentation, technology evolution, regional deployment and strategy‑formulation for future growth in the composite artificial skin space.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 2262.73 Million |

Market Revenue in 2032 | USD 5522.91 Million |

CAGR (2025 - 2032) | 11.8% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Integra LifeSciences, Smith & Nephew, Organogenesis, MiMedx, Tissue Regenix, Vericel, CollPlant Biotechnologies, Avita Medical |

Customization & Pricing | Available on Request (10% Customization is Free) |