Reports

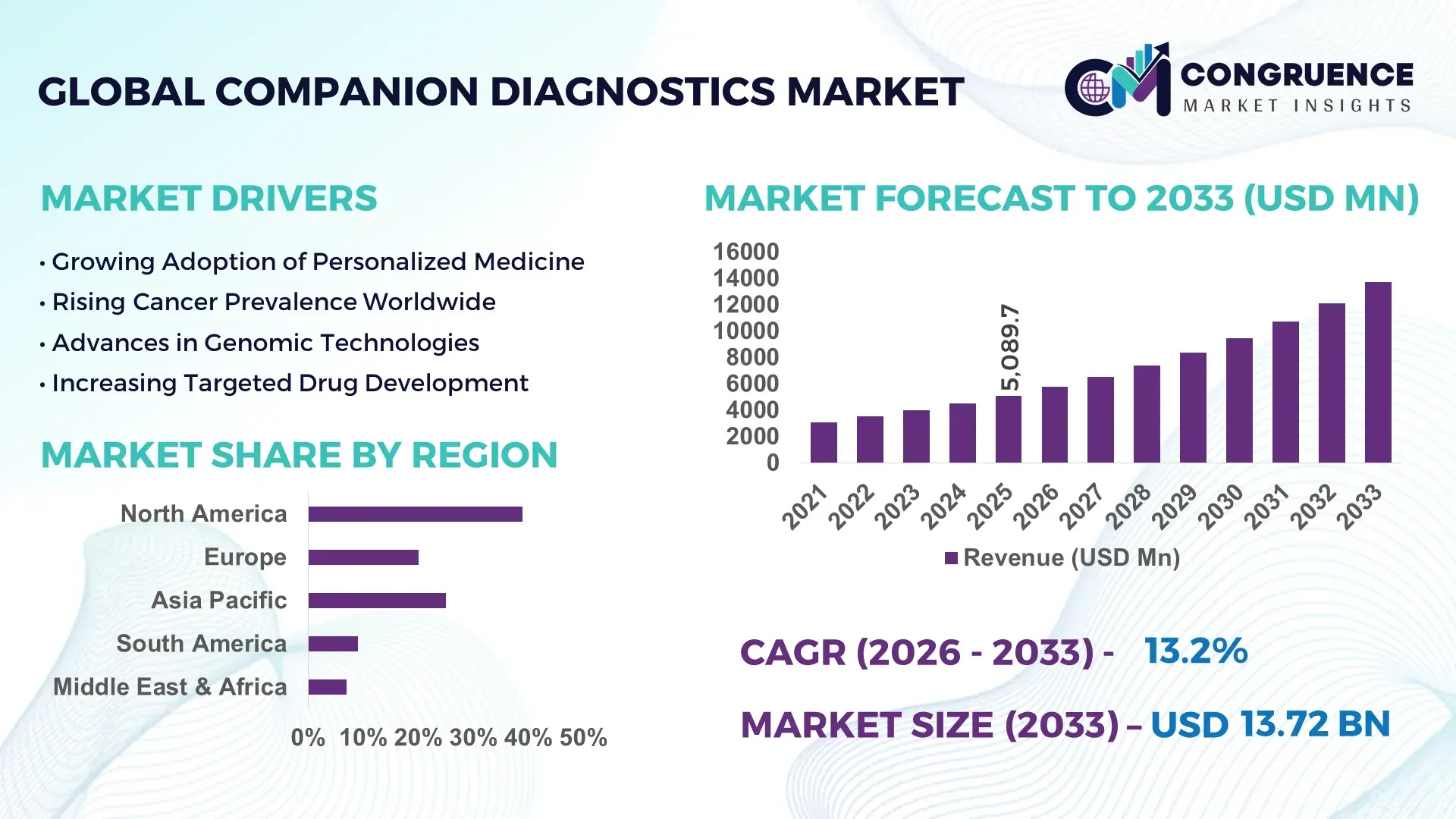

The Global Companion Diagnostics Market was valued at USD 5089.68 Million in 2025 and is anticipated to reach a value of USD 13723.42 Million by 2033 expanding at a CAGR of 13.2% between 2026 and 2033. Market expansion is being driven by accelerated oncology biomarker approvals, rising adoption of next-generation sequencing platforms, and pharmaceutical–diagnostic co-development programs linked to precision immunotherapy pipelines across North America, Europe, and Asia-Pacific.

The United States dominates the global companion diagnostics market with nearly 41% share, supported by advanced oncology infrastructure, over USD 4 billion annual precision medicine investments, and high integration of NGS-based testing across cancer centers. China is rapidly scaling molecular diagnostics capacity through domestic reagent manufacturing and hospital genomics expansion, achieving over 28% growth in oncology testing volumes during 2025–2026 amid regional healthcare localization initiatives and post–supply chain diversification strategies. Germany continues strengthening EU-based CDx manufacturing and regulatory harmonization under IVDR implementation, improving cross-border clinical adoption efficiency by approximately 18%.

Companies prioritizing biomarker-driven therapy partnerships, regional manufacturing resilience, and AI-enabled genomic interpretation platforms are securing stronger commercialization positioning in the high-growth global companion diagnostics ecosystem.

Market Size & Growth: USD 5089.68 Million in 2025 reaching USD 13723.42 Million by 2033, supported by precision oncology expansion and integrated biomarker testing workflows.

Top Growth Drivers: Oncology biomarker adoption increased 31%, NGS testing utilization rose 27%, and pharma-diagnostic partnerships expanded 24% globally.

Short-Term Forecast: By 2028, automated genomic interpretation platforms are projected to reduce diagnostic turnaround time by 35% across advanced hospital laboratories.

Emerging Technologies: AI-enabled sequencing analytics, multiplex PCR panels, and liquid biopsy platforms improved testing accuracy by nearly 22% in high-throughput environments.

Regional Leaders: North America exceeds USD 5.4 billion with immunotherapy-linked adoption, Asia-Pacific surpasses USD 3.8 billion through localized manufacturing, while Europe advances IVDR-compliant deployment.

Consumer/End-User Trends: Over 62% of oncology centers integrated companion diagnostics into first-line treatment selection workflows during 2025–2026.

Pilot/Case Example: In 2026, integrated liquid biopsy programs reduced invasive tissue testing requirements by 29% across selected oncology networks.

Competitive Landscape: Roche holds approximately 19% market share alongside Thermo Fisher Scientific, Agilent Technologies, Illumina, and Qiagen in advanced biomarker diagnostics.

Regulatory & ESG Impact: IVDR alignment and regional manufacturing expansion lowered cross-border compliance delays by nearly 17% amid global supply-chain restructuring.

Investment & Funding: Global investments exceeded USD 2.6 billion in 2025, led by oncology-focused partnerships, automation upgrades, and precision medicine expansion projects.

Innovation & Future Outlook: Multi-cancer early detection platforms and AI-guided therapy matching are accelerating decentralized testing adoption across high-growth healthcare systems.

Companion diagnostics demand is accelerating across oncology, rare disease profiling, and targeted immunotherapy applications as healthcare providers prioritize faster treatment stratification. AI-integrated genomic analytics and liquid biopsy innovations improved clinical workflow efficiency by nearly 21% during 2025–2026. Asia-Pacific manufacturing expansion and stricter regulatory harmonization are reshaping supply resilience while increasing localized testing capacity, creating a stronger foundation for long-term strategic commercialization and partnership planning.

Companion diagnostics is becoming a strategic control point in precision medicine as pharmaceutical companies increasingly link drug commercialization to biomarker-based patient selection. The market is reshaping oncology competition by improving therapy response rates, reducing late-stage clinical trial failures, and accelerating targeted treatment approvals. Regulatory tightening under Europe’s IVDR framework and expanding genomic infrastructure in the United States, Japan, and South Korea are driving laboratory modernization and digital pathology integration. More than 58% of newly approved oncology therapies in 2025 incorporated biomarker-linked diagnostic requirements, reinforcing the market’s central role in therapeutic differentiation.

AI-assisted genomic interpretation platforms are outperforming legacy manual sequencing workflows by reducing diagnostic processing time nearly 40% while improving variant classification consistency across high-volume laboratories. The United States leads in integrated companion diagnostic deployment through large-scale oncology networks, whereas China is expanding cost-efficient localized manufacturing and hospital sequencing capacity at significantly faster operational scale. In 2026, several cancer centers deployed cloud-connected liquid biopsy systems that reduced repeat tissue sampling rates by approximately 26%, improving treatment continuity and laboratory throughput efficiency.

Over the next two to three years, companies are prioritizing co-development partnerships, decentralized testing infrastructure, and automation-led workflow expansion to secure stronger competitive positioning. Firms investing in integrated genomic ecosystems, regional manufacturing resilience, and AI-enabled diagnostic interpretation are expected to achieve faster commercialization cycles, stronger reimbursement alignment, and higher long-term clinical adoption stability.

Rapid expansion of targeted oncology therapies is intensifying demand for companion diagnostics integrated with treatment selection protocols. Nearly 64% of late-stage oncology pipelines now include biomarker-linked stratification models, while NGS-based testing adoption across U.S. cancer centers increased approximately 29% during 2025–2026. Japan and Germany are strengthening precision medicine reimbursement frameworks, accelerating hospital deployment of multiplex genomic testing systems. This structural transition is reducing ineffective therapy allocation and improving clinical trial enrollment precision by nearly 23%. Pharmaceutical companies are responding through co-development alliances, integrated sequencing platforms, and localized manufacturing partnerships to improve regulatory synchronization and commercialization speed. A notable operational shift involves pharmaceutical firms embedding diagnostic development earlier in Phase II programs to shorten downstream approval complexity and improve therapy differentiation.

Companion diagnostics deployment remains constrained by fragmented regulatory pathways, elevated sequencing costs, and inconsistent reimbursement structures across healthcare systems. Under Europe’s IVDR transition, laboratory compliance expenses increased approximately 18%, while smaller diagnostic providers faced certification delays exceeding 12 months in some EU markets. In emerging healthcare systems, advanced genomic testing costs remain 30%–40% higher than conventional pathology workflows, limiting broad clinical integration. Supply dependency on specialized reagents and semiconductor-linked sequencing components also created procurement volatility during recent healthcare supply-chain realignments. Companies are mitigating these pressures through regional manufacturing expansion, multi-supplier procurement contracts, and automated assay optimization platforms that reduce consumable utilization. A key strategic constraint is that delayed reimbursement alignment directly slows hospital purchasing decisions despite strong clinical validation.

AI-driven genomic analytics and decentralized molecular testing infrastructure are opening high-value expansion opportunities beyond traditional oncology hubs. Automated variant interpretation platforms improved laboratory throughput efficiency by nearly 33%, while cloud-connected diagnostic systems reduced reporting delays by approximately 27% across multi-site healthcare networks. India and South Korea are expanding regional genomic infrastructure investments to strengthen localized precision medicine access and reduce overseas dependency for molecular analysis. Liquid biopsy innovation, multi-cancer early detection programs, and real-time clinical decision support systems are creating scalable testing ecosystems with lower operational intensity. Companies are positioning through AI partnerships, digital pathology integration, and regional laboratory collaborations to strengthen long-term market penetration. An emerging strategic advantage involves integrating companion diagnostics into decentralized outpatient oncology networks, improving access while reducing tertiary hospital burden.

Long-term scalability of companion diagnostics is increasingly challenged by fragmented clinical data systems, workforce specialization gaps, and integration complexity across healthcare networks. Approximately 46% of hospitals using advanced genomic testing platforms still operate with partially disconnected pathology and electronic health record environments, limiting real-time treatment coordination. In the United States and Germany, shortages of molecular pathology specialists increased genomic interpretation turnaround pressure by nearly 21% during 2025–2026. Cybersecurity risks surrounding genomic datasets are also intensifying as cloud-connected diagnostics expand across decentralized healthcare systems. Companies must invest in interoperable digital infrastructure, workforce training, and secure AI-enabled clinical platforms to maintain deployment consistency and regulatory compliance. A major operational challenge is ensuring standardized biomarker interpretation across multi-site laboratory ecosystems without compromising diagnostic accuracy or treatment timelines.

• AI-Guided Workflow Expansion Diagnostic laboratories are rapidly integrating AI-based genomic interpretation systems to reduce reporting bottlenecks and improve sequencing throughput. Automated bioinformatics platforms lowered variant analysis time by nearly 38% during 2025–2026, while high-volume oncology centers in the United States improved laboratory utilization rates by approximately 24%. Companies are restructuring pathology workflows through cloud-based analytics partnerships and centralized data management systems to address molecular workforce shortages and rising testing complexity.

• Liquid Biopsy Deployment Scaling Hospitals and specialty cancer networks are accelerating liquid biopsy integration for non-invasive monitoring and therapy selection. Repeat tissue biopsy procedures declined nearly 29% in selected oncology programs, while circulating tumor DNA testing volumes increased more than 32% across Japan and South Korea. Companies are expanding reagent production capacity and decentralized sample-processing infrastructure following recent supply-chain disruptions affecting sequencing consumables and cold-chain logistics reliability.

• Localized Manufacturing Priorities Rising China and India are strengthening domestic molecular diagnostics manufacturing to reduce import dependency and regulatory exposure. Regional production localization improved reagent procurement stability by nearly 26% while lowering cross-border fulfillment delays by approximately 19%. Diagnostic firms are responding through contract manufacturing partnerships, regional distribution hubs, and automated cartridge assembly investments. A non-obvious operational shift involves pharmaceutical companies favoring geographically diversified diagnostic suppliers during therapy commercialization planning.

• Integrated Multi-Omics Testing Growth Enterprise healthcare systems are increasingly combining genomic, proteomic, and transcriptomic profiling within companion diagnostic workflows to improve therapy precision. Multi-omics deployment increased nearly 21% across advanced cancer institutes during 2025–2026, while integrated biomarker analysis improved treatment matching efficiency by approximately 17%. Companies are prioritizing platform interoperability, digital pathology integration, and co-development partnerships to support next-generation targeted therapy ecosystems under evolving precision medicine reimbursement frameworks.

Next-Generation Sequencing (NGS) remains the leading segment due to its scalability, multiplex biomarker capability, and strong integration with targeted oncology therapy pipelines. More than 48% of advanced oncology companion diagnostic workflows now incorporate NGS platforms because they reduce sequential testing requirements and improve mutation detection breadth. Pharmaceutical companies increasingly prioritize NGS-compatible assays during drug development to accelerate biomarker alignment and clinical trial stratification. PCR-Based Diagnostics continues holding strong adoption in cost-sensitive and rapid-turnaround environments, particularly in hospital laboratories requiring high-volume standardized testing with lower operational complexity.

NGS is also the fastest-growing segment as cloud-based bioinformatics integration and automated sequencing workflows improve deployment economics. Sequencing turnaround times declined nearly 34% during 2025–2026 through workflow automation and AI-supported interpretation systems. Immunohistochemistry maintains strategic relevance in pathology-driven cancer diagnostics, while In-Situ Hybridization supports highly specific tissue-based biomarker analysis in complex oncology cases. Gene Expression Profiling is gaining traction in therapy-response prediction and recurrence monitoring applications. Companies are expanding sequencing partnerships, localized reagent manufacturing, and integrated software ecosystems to strengthen long-term precision diagnostics positioning.

Oncology continues dominating companion diagnostics adoption due to the expanding use of targeted therapies, immuno-oncology drugs, and biomarker-driven treatment pathways. Nearly 65% of precision medicine testing volumes are linked to oncology applications, supported by rising integration of NGS panels and liquid biopsy systems across cancer treatment centers. Hospitals in the United States and Germany accelerated deployment of integrated genomic profiling workflows during 2025–2026 to improve therapy selection efficiency and reduce ineffective treatment allocation. Companies are prioritizing oncology-focused co-development partnerships and automated molecular testing infrastructure to strengthen commercialization alignment with pharmaceutical pipelines.

Infectious Diseases is emerging as the fastest-growing application segment as healthcare systems expand molecular surveillance and pathogen-specific therapeutic matching capabilities. Automated infectious disease testing workflows improved sample processing efficiency by approximately 28% in selected hospital networks. Neurology and Genetic Disorders applications are gaining momentum through biomarker discovery initiatives and rare disease sequencing programs, while Cardiology adoption remains concentrated in pharmacogenomic treatment optimization. Companies are expanding decentralized diagnostic access, AI-assisted interpretation systems, and specialty testing collaborations to capture emerging clinical demand beyond oncology-focused deployment models.

Hospitals represent the leading end-user segment due to their large-scale oncology infrastructure, integrated pathology systems, and centralized molecular testing capabilities. Nearly 54% of companion diagnostic testing volumes are processed through hospital-based laboratories where high patient throughput and multidisciplinary cancer care support operational efficiency. Major healthcare networks in the United States and Japan expanded automated sequencing and liquid biopsy workflows during 2025–2026 to reduce diagnostic turnaround times by approximately 31%. Companies are strengthening hospital partnerships through integrated software platforms, long-term reagent supply agreements, and workflow customization strategies tailored to enterprise healthcare systems.

Diagnostic Laboratories are emerging as the fastest-growing end-user segment as outsourced genomic testing demand increases across decentralized healthcare environments. Independent laboratories improved high-throughput biomarker processing capacity by nearly 27% through automation and cloud-connected analytics integration. Pharmaceutical Companies continue expanding co-development models with diagnostic providers, while Research Institutes and Academic Institutions focus on biomarker discovery and translational genomics programs. Specialty Clinics are increasing adoption for targeted oncology management and outpatient precision therapy coordination. Companies are responding with flexible pricing models, regional laboratory alliances, and scalable assay platforms to strengthen competitive positioning across diversified end-user ecosystems.

North America accounted for the largest market share at 39.9% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.8% between 2026 and 2033.

Integrated Precision Oncology Infrastructure Driving Deployment Scale

North America maintains leadership in companion diagnostics through advanced oncology infrastructure, strong pharmaceutical–diagnostic collaboration networks, and rapid deployment of AI-supported genomic testing systems. The region contributes nearly 40% of global testing activity, supported by high adoption of biomarker-linked immunotherapy selection and large-scale sequencing integration across cancer centers. During 2025–2026, automated molecular pathology workflows expanded by approximately 28% across major U.S. healthcare systems, improving reporting efficiency and therapy alignment. Enterprise laboratories are increasingly consolidating digital pathology, liquid biopsy, and genomic analytics into unified platforms to reduce turnaround times and strengthen clinical coordination. Companies are prioritizing strategic acquisitions, decentralized testing expansion, and cloud-based interpretation systems to improve operational scalability and commercialization alignment.

United States Market Outlook: The United States remains the operational center of the companion diagnostics ecosystem due to its concentration of oncology trials, advanced reimbursement infrastructure, and high-volume genomic testing capacity. More than 62% of precision oncology programs integrated companion diagnostics into first-line treatment workflows during 2025–2026. Pharmaceutical companies continue embedding biomarker-linked assays into drug development pipelines earlier to accelerate regulatory alignment, while enterprise laboratories are expanding AI-driven interpretation systems to manage rising sequencing complexity and improve clinical throughput consistency.

Regulatory Harmonization Reshaping Diagnostic Modernization

Europe is strengthening its companion diagnostics landscape through IVDR-driven regulatory standardization, molecular pathology modernization, and expanded precision oncology integration. Germany, France, and the United Kingdom collectively account for a major share of advanced biomarker testing deployment across the region. During 2025–2026, IVDR compliance investments increased laboratory automation adoption by approximately 22% as diagnostic providers upgraded assay validation and digital documentation systems. Hospitals are increasingly adopting multiplex genomic testing and AI-enabled pathology workflows to support targeted therapy expansion while improving operational traceability. Companies are responding through regional manufacturing partnerships, local reagent sourcing, and integrated regulatory support models designed to reduce certification delays and improve deployment continuity.

Germany Market Outlook: Germany remains the region’s most strategically influential market due to its advanced clinical laboratory infrastructure, strong oncology research networks, and early adoption of molecular diagnostics automation. Nearly 58% of large cancer treatment facilities expanded high-throughput genomic testing capabilities during 2025–2026. German healthcare providers are integrating digital pathology and sequencing platforms within centralized oncology networks, enabling faster biomarker validation and more efficient therapy coordination while supporting long-term precision medicine scalability under evolving European compliance standards.

Localized Manufacturing and Sequencing Expansion Accelerating Adoption

Asia-Pacific is emerging as the fastest-scaling companion diagnostics market due to expanding genomic infrastructure, localized reagent manufacturing, and rapid precision oncology deployment. China, Japan, South Korea, and India are increasing sequencing capacity and decentralized testing access to reduce dependency on imported molecular diagnostics components. During 2025–2026, regional liquid biopsy deployment increased approximately 31%, while automated sequencing infrastructure investments improved laboratory throughput efficiency by nearly 26%. Enterprise healthcare systems are integrating AI-supported genomic analytics to address specialist shortages and improve testing scalability. Companies are accelerating regional partnerships, manufacturing localization, and cloud-connected diagnostics deployment to strengthen operational resilience amid ongoing healthcare supply-chain restructuring.

China Market Outlook: China leads the Asia-Pacific companion diagnostics landscape through aggressive genomic infrastructure expansion, domestic manufacturing investment, and strong oncology testing demand. More than 35% of newly established molecular pathology laboratories in major urban healthcare clusters integrated high-throughput sequencing systems during 2025–2026. Chinese diagnostic companies are strengthening localized reagent ecosystems and AI-based analytics capabilities to reduce external technology dependence while improving testing affordability and large-scale deployment efficiency across hospital networks.

Oncology Testing Demand Supporting Regional Expansion

South America is witnessing rising companion diagnostics adoption through oncology care modernization, improving molecular testing infrastructure, and growing demand for targeted therapies. Brazil and Argentina account for the majority of advanced biomarker testing deployment across the region, particularly within private healthcare systems and specialized cancer institutes. During 2025–2026, molecular oncology testing volumes increased approximately 19% as hospitals expanded genomic profiling capabilities and liquid biopsy adoption. However, uneven reimbursement frameworks and limited high-complexity laboratory distribution continue constraining broader deployment consistency. Companies are responding through regional distribution partnerships, localized training programs, and outsourced sequencing collaborations designed to improve operational accessibility and reduce infrastructure dependency.

Brazil Market Outlook: Brazil remains the most strategically significant South American market due to its expanding oncology infrastructure, large private healthcare network, and increasing precision medicine investment. Nearly 44% of advanced cancer treatment facilities in major metropolitan areas integrated companion diagnostic testing into targeted therapy planning during 2025–2026. Diagnostic providers are strengthening laboratory partnerships and localized workflow support services to improve deployment scalability while addressing regional disparities in specialized molecular pathology access.

Healthcare Modernization Investments Expanding Precision Diagnostics

Middle East & Africa is gradually strengthening companion diagnostics adoption through healthcare modernization initiatives, oncology infrastructure investment, and centralized genomic testing expansion. Gulf countries are leading deployment activity with increasing investments in precision medicine programs and digital pathology integration. During 2025–2026, molecular diagnostics infrastructure projects improved high-complexity testing capacity by approximately 23% across selected tertiary healthcare networks. Enterprise healthcare providers are prioritizing centralized sequencing facilities and AI-assisted pathology systems to improve specialist utilization efficiency. Companies are entering strategic partnerships with government-backed healthcare institutions and regional laboratory operators to strengthen long-term market access and operational continuity.

Saudi Arabia Market Outlook: Saudi Arabia is becoming the region’s leading precision diagnostics hub through strong healthcare transformation initiatives, oncology infrastructure development, and government-backed genomic programs. More than 40% of tertiary oncology centers expanded biomarker-linked testing capabilities during 2025–2026 to support targeted cancer therapy deployment. Healthcare institutions are integrating cloud-connected pathology systems and centralized sequencing laboratories to improve diagnostic coordination while reducing dependency on overseas molecular testing workflows.

Roche, Thermo Fisher Scientific, Illumina, Agilent Technologies, and Qiagen dominate competition within the companion diagnostics market, collectively controlling nearly 58% of advanced biomarker testing activity. Global leaders compete through sequencing scale, AI-enabled interpretation, regulatory alignment, and integrated oncology partnerships, while regional diagnostic firms focus on cost-efficient assay deployment and localized manufacturing. Roche and Illumina are competing aggressively in integrated genomic ecosystems, whereas Thermo Fisher and Agilent are strengthening laboratory automation and decentralized testing infrastructure. Sequencing workflow optimization reduced enterprise laboratory processing time by nearly 34%, while automated interpretation systems improved reporting consistency by approximately 22%. Companies are expanding through acquisitions, co-development agreements, reagent localization, and digital pathology integration to secure operational control across precision oncology networks. The competitive shift is moving toward AI-supported multi-omics diagnostics and vertically integrated biomarker platforms. High regulatory compliance costs, specialized workforce requirements, and sequencing infrastructure intensity remain major entry barriers. Winning requires scalable genomic ecosystems, regulatory agility, and clinically integrated automation.

Roche

Thermo Fisher Scientific

Illumina

Agilent Technologies

Qiagen

Abbott Laboratories

BioMérieux

Danaher Corporation

Foundation Medicine

Guardant Health

Myriad Genetics

Bio-Rad Laboratories

Sysmex Corporation

Exact Sciences Corporation

Companion diagnostics technology is rapidly advancing through AI-enabled genomic interpretation, high-throughput sequencing, and integrated liquid biopsy workflows. Next-generation sequencing platforms now support simultaneous multi-biomarker analysis with nearly 35% faster processing efficiency compared with conventional single-gene testing systems. More than 52% of advanced oncology laboratories integrated automated bioinformatics pipelines during 2025–2026 to improve reporting consistency and reduce specialist workload. Companies deploying cloud-connected pathology and sequencing ecosystems are gaining stronger operational scalability and faster biomarker commercialization alignment.

Emerging technologies are reshaping decentralized testing and treatment monitoring capabilities. Liquid biopsy platforms reduced invasive tissue sampling requirements by approximately 29% while improving repeat monitoring flexibility across oncology programs. AI-assisted digital pathology systems enhanced variant classification accuracy by nearly 24% in high-volume cancer centers. Multi-omics integration combining genomic, transcriptomic, and proteomic analysis is expanding precision therapy matching efficiency across complex cancer subtypes. Pharmaceutical companies are increasingly embedding companion diagnostics earlier within clinical trial design to accelerate targeted therapy approval workflows.

Disruptive innovation between 2026 and 2028 will center on real-time molecular monitoring, decentralized sequencing infrastructure, and AI-guided biomarker prediction models. Compared with legacy pathology workflows, integrated automated diagnostic ecosystems improve laboratory throughput nearly 31% while lowering operational redundancy. Companies investing aggressively in scalable genomic infrastructure, localized reagent manufacturing, and AI-driven analytics are expected to secure stronger competitive positioning as precision oncology deployment expands globally.

May 2026 – Roche announced acquisition of PathAI to strengthen AI-powered digital pathology and companion diagnostic capabilities. The deal included USD 750 million upfront plus milestone payments, accelerating automated oncology workflow integration and biomarker discovery expansion across precision medicine networks.

April 2026 – Roche Foundation Medicine acquired SAGA Diagnostics to integrate Pathlight™ molecular residual disease technology with decentralized MRD testing infrastructure. The platform combines whole-genome sequencing with digitalPCR, improving ultra-sensitive tumor DNA detection and expanding precision monitoring accessibility across oncology ecosystems.

October 2025 – Thermo Fisher Scientific agreed to acquire Clario for up to USD 9.4 billion, strengthening clinical trial analytics and biomarker-driven development operations. The acquisition expanded differentiated data intelligence capabilities supporting faster oncology therapy development and integrated companion diagnostic commercialization workflows.

May 2026 – Roche Diagnostics launched the Liver Disease Panel featuring certified AI-based clinical algorithms supporting fibrosis detection and liver cancer surveillance. The platform integrates biomarker diagnostics with automated analytics, improving non-invasive disease assessment efficiency across large-scale clinical management environments.

The report provides detailed analysis of the global companion diagnostics ecosystem across major technologies, applications, end-users, and regional deployment patterns between 2026 and 2033. Coverage includes PCR-Based Diagnostics, Immunohistochemistry, Next-Generation Sequencing, In-Situ Hybridization, and Gene Expression Profiling with strategic evaluation of operational scalability, automation integration, and biomarker deployment intensity. The study assesses demand distribution across Oncology, Infectious Diseases, Neurology, Cardiology, and Genetic Disorders while examining procurement behavior among hospitals, diagnostic laboratories, pharmaceutical companies, specialty clinics, research institutes, and academic institutions.

The report delivers region-wise insights across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting infrastructure modernization, sequencing deployment concentration, and localized manufacturing expansion. More than 55% of analyzed enterprise healthcare systems are actively integrating AI-supported genomic workflows and decentralized testing infrastructure. Strategic coverage includes liquid biopsy adoption, digital pathology integration, multi-omics diagnostics, regulatory transformation, and partnership activity, enabling stakeholders to strengthen investment planning, commercialization strategy, competitive positioning, and long-term operational scalability.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 5089.68 Million |

|

Market Revenue in 2033 |

USD 13723.42 Million |

|

CAGR (2026 - 2033) |

13.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Roche, Thermo Fisher Scientific, Illumina, Agilent Technologies, Qiagen, Abbott Laboratories, BioMérieux, Danaher Corporation, Foundation Medicine, Guardant Health, Myriad Genetics, Bio-Rad Laboratories, Sysmex Corporation, Exact Sciences Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |