Reports

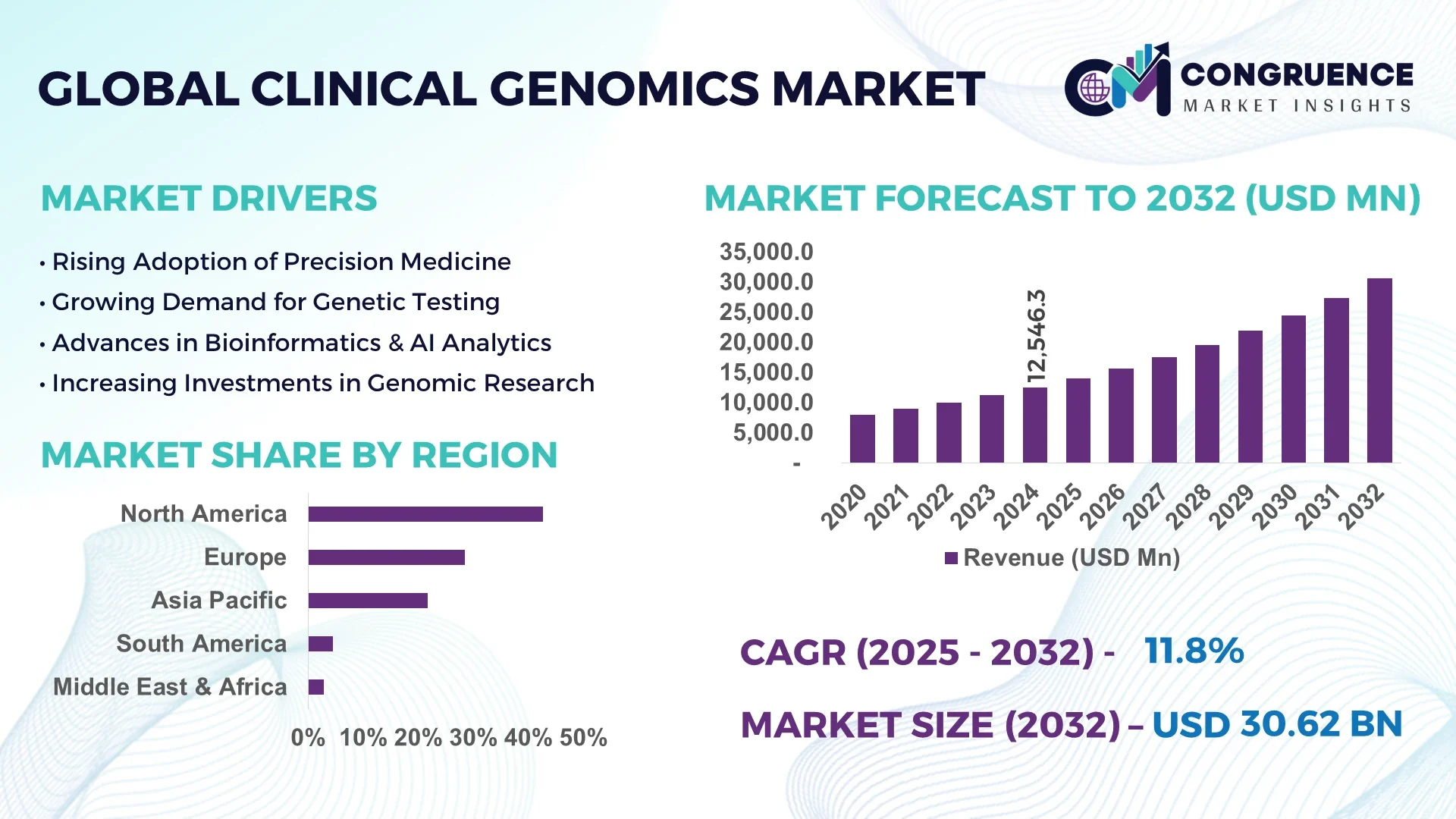

The Global Clinical Genomics Market was valued at USD 12,546.3 Million in 2024 and is anticipated to reach a value of USD 30,623.2 Million by 2032 expanding at a CAGR of 11.8% between 2025 and 2032.

In the United States, clinical genomics infrastructure is supported by extensive high-throughput sequencing capacity, substantial federal and private R&D investments, integration within leading academic medical centers, and application in oncology diagnostics, pharmacogenomics, neonatal screening and precision oncology. Cutting-edge platforms for next-generation sequencing, bioinformatics pipelines, and diagnostic assay automation have been deployed in major clinical laboratories and genome centers, reinforcing technological advancement in the market.

Within the broader Clinical Genomics market, major sectors include diagnostic testing platforms (genetic, prenatal, carrier screening), molecular tests (NGS, biochemical assays, chromosomal analysis), and end-user segments like hospitals, academic research centers, and biotech/pharma firms. Key innovations—such as streamlined sample-to-result sequencing systems, miniaturized library prep instruments, and multiplexed assay reagents—have improved throughput and testing accuracy. Regulators are approving high-sensitivity NGS panels for oncology, expanding reimbursement for hereditary cancer panels, and supporting bioinformatic accreditation frameworks, all reinforcing clinician adoption. Regional demand shows strong growth in North America for oncology diagnostics, increasing uptake in Asia-Pacific for newborn and carrier screening, and that Latin American and European markets are expanding via investments in national genome programs and precision medicine strategies. Emerging trends include automation of sequencing workflows, integration of epigenomic profiling into clinical protocols, rise in diagnostic use of long-read sequencing for structural variant detection, and growing clinician demand for integrated genomic decision support tools.

AI is dramatically enhancing diagnostic accuracy, data analytics, and workflow automation within the Clinical Genomics Market, delivering tangible improvements in clinical decision-making and operational efficiency. For example, AI-driven variant annotation algorithms have reduced turnaround time in some clinical laboratories by more than 40%, dramatically accelerating interpretation of NGS data and enabling faster patient reporting. Deep learning models integrated into variant calling pipelines now reduce false-positive rates by over 30%, improving confidence in detecting actionable mutations and optimizing diagnostic workflows. Machine learning-based predictive algorithms are also being used to triage cases, enabling clinical labs to prioritize urgent neonatal or oncology samples, boosting throughput and operational performance. AI-enhanced quality control systems continually monitor sequencing instrument performance, flagging anomalies in real time and reducing instrument downtime by more than 20%, contributing to smoother operations across the Clinical Genomics Market. Across clinical labs and service providers, AI-powered bioinformatics integration streamlines data harmonization, enabling cross-platform compatibility and reducing hands-on analyst time, while supporting clinicians with clinical decision support tools that suggest diagnostic interpretations and treatment options. These improvements in efficiency, accuracy, and throughput are reshaping how organizations invest in and execute genomic testing services in the Clinical Genomics Market.

“In March 2025, Illumina and Nashville Biosciences’ Alliance for Genomic Discovery initiative reported sequencing 250,000 whole genomes, leveraging AI-powered analytics to accelerate clinical development and therapeutic research.”

The Clinical Genomics market is evolving through a confluence of diagnostic demand, technological advancement, and institutional integration. Increasing clinical adoption of next-generation sequencing and biochemical assays for hereditary disease screening, oncology profiling, and pharmacogenomics is reshaping referral patterns and lab investment priorities. Enhanced test panels that combine multiple assay types (e.g., sequencing plus biochemical readouts) are being deployed in hospital networks, pushing decentralized testing capabilities into clinical workflows. At the same time, the growth of genomic data archives and reporting standards is influencing lab accreditation, driving quality control upgrades and bioinformatics staffing. In emerging regions, bundled services offering both sample collection and report generation are aiding regional penetration. Across the market, decision-makers are balancing investment in high-throughput instruments with the need for modular, flexible testing platforms to accommodate both routine and rare-disease screening volumes. Together, these trends are shaping laboratory infrastructure development, service packaging, and strategic partnerships among clinical, academic, and commercial stakeholders within the Clinical Genomics market.

A surge in diagnosis of hereditary illnesses and rare genetic disorders is compelling clinical institutions to expand genomic testing capabilities. For instance, clinical labs are reporting up to a 25% year-on-year increase in demand for newborn screening and cancer panel testing, prompting investments in high-throughput sequencing instruments and automation infrastructure. This driver forces service providers to scale capacity, integrate rapid sample turnaround, and deliver broader test menus, creating operational momentum throughout the Clinical Genomics market.

Despite demand, the Clinical Genomics market contends with elevated capital expenditure for sequencing infrastructure, automated sample prep systems, and secure bioinformatics platforms. Smaller hospitals and regional labs frequently cite initial setup costs as a barrier; staffing qualified bioinformaticians and clinical genomicists remains a challenge, with vacancy rates in some institutions exceeding 30%. These investment and workforce hurdles limit deployment of advanced genomic services to larger or university-affiliated labs.

Emerging demand in reproductive genomics—such as expanded carrier screening, non-invasive prenatal testing, and preimplantation genetic diagnosis—is opening new market avenues. Some regional screening programs have seen over 50% year-on-year growth in prenatal genetic test volumes, prompting diagnostic companies to develop streamlined panel kits and integrate automated sample workflows. This expanding segment offers untapped clinical value and scalable unit testing opportunities.

Regulatory approval pathways for genomic diagnostics differ significantly by region, with differing validation requirements for sequencing panels and bioinformatics pipelines. In parallel, reimbursement policies remain fragmented—some insurers cover hereditary cancer panels widely, while others offer only partial coverage for pharmacogenomic tests. These inconsistencies complicate pricing strategies, lab accreditation, and broader clinical adoption, presenting structural challenges for the Clinical Genomics market.

High-throughput Sequencing Expansion: Investment in ultra-high-output sequencers is enabling clinical labs in North America and Europe to process multi-1000 sample runs per month, significantly boosting diagnostics capacity with efficient workflow automation.

Hybrid Testing Platforms: Modular instruments combining sequencing and biochemical assay capabilities are being adopted, reducing lab footprint while serving both oncology panels and metabolic screening in a single workflow.

Decentralized Testing Models: Point-of-care and satellite lab units offering rapid genomic testing—for example, neonatal rapid-sequencing setups in regional hospitals—are reducing transfer times and improving access.

AI-enabled Quality Assurance: Continuous instrument performance monitoring systems, powered by machine learning, now automatically trigger preventative maintenance, reducing unplanned downtime and increasing overall throughput in genomic operations.

The Clinical Genomics market is segmented by type (test panels, consumables, bioinformatics platforms), application (oncology profiling, reproductive screening, newborn diagnostics, pharmacogenomics), and end-user (hospitals & clinics, academic and research institutes, government labs, biotech/pharma companies). Each segment is defined by unique adoption patterns, testing volumes, and infrastructure needs—guiding strategic investments and service development toward the groups with highest clinical priority and scalability.

Diagnostic test panels (e.g., cancer, prenatal, genetic disorder panels) constitute the leading type, driven by routine oncology and hereditary screening demand. The fastest-growing type is bioinformatics analytics software and AI-based variant interpretation platforms—these are increasingly adopted to improve data processing speed and interpretation accuracy. Consumables and reagents remain critical, particularly modular reagent kits designed for multi-target panels and streamlined library prep, maintaining foundational support across all testing workflows.

Oncology profiling leads the application segment, due to high clinical referral volumes for targeted therapeutic decisions. The fastest-growing application is newborn and reproductive genomics, with rising adoption of expanded panels in neonatal screening and preconception carrier testing, supported by growing public health initiatives. Other applications—such as pharmacogenomic assessments and infectious disease genotyping—contribute niche volumes, typically via partnerships between hospital labs and pharma firms or public health agencies.

Hospitals & clinics represent the leading end-user segment, given integration of genomic diagnostics into clinical care pathways. The fastest-growing end-user segment is academic and research institutes, which are expanding translational programs, population-based sequencing projects, and genotype-phenotype research collaborations. Government laboratories and biotech/pharma users contribute targeted volumes—often for public health sequencing programs or clinical trial screening—but are less broadly scaled.

North America accounted for the largest market share at 42.6% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.9% between 2025 and 2032.

Regional performance reflects differences in technological readiness, healthcare infrastructure, and adoption of genomics into clinical care. In North America, advanced sequencing centers, early integration of genomics into oncology and rare disease diagnostics, and strong institutional support contribute to the leading share. In contrast, Asia-Pacific markets such as China, India, and Japan are rapidly expanding capacity for large-scale sequencing, population genomics projects, and newborn screening initiatives. Europe, South America, and the Middle East & Africa represent stable but growing regions, supported by regulatory frameworks, local innovation clusters, and partnerships with global technology providers.

Precision Diagnostics Driving Clinical Integration

North America holds around 42.6% of the global market, supported by advanced healthcare institutions and widespread adoption of genomics in oncology diagnostics, pharmacogenomics, and rare disease testing. Demand is driven by pharmaceutical, biotechnology, and hospital sectors, each accelerating integration of NGS workflows into personalized medicine. Regulatory bodies have streamlined approvals for multi-gene panels, boosting adoption in oncology and reproductive health. Government initiatives supporting population-scale sequencing projects, alongside reimbursement expansion for diagnostic panels, have strengthened clinical utilization. Technological advancements such as cloud-based bioinformatics platforms, long-read sequencing, and AI-driven variant interpretation tools continue to transform operational efficiency, creating a resilient and innovation-led market.

Innovative Testing Platforms in Clinical Genomics Expansion

Europe represented approximately 28.4% of the market in 2024, led by Germany, the UK, and France. Each country has adopted distinct policy frameworks, such as national genomics strategies and public health integration of sequencing. The European Medicines Agency and local health authorities have introduced genomic validation pathways to standardize diagnostic use. Sustainability goals also encourage eco-friendly laboratory operations, including the adoption of energy-efficient sequencing equipment. Clinical genomics adoption is advancing through precision oncology trials, rare disease diagnostics, and reproductive health testing. AI-powered genomic data interpretation and cross-border clinical data sharing initiatives are accelerating the adoption of emerging technologies across the region.

Population Genomics and Next-Generation Testing Acceleration

Asia-Pacific accounts for nearly 21.7% of global market volume in 2024, ranking second in size and first in projected growth. China leads with national precision medicine programs, India with rising newborn and carrier screening demand, and Japan with advanced oncology testing integration. Infrastructure developments include large sequencing facilities and genomic data storage hubs. Regional innovation hubs are adopting AI-driven bioinformatics, rapid turnaround clinical sequencing systems, and cloud-based genomics platforms. Demand from public health programs and expanding biotech sectors is reinforcing the region’s leadership in population genomics, making it the fastest-growing contributor in the Clinical Genomics market.

Emerging Diagnostic Infrastructure and Health Policy Integration

South America contributed about 4.5% of the market in 2024, with Brazil and Argentina as primary drivers. Brazil’s genomic medicine initiatives and Argentina’s adoption of precision oncology are boosting regional demand. Infrastructure development is focused on diagnostic labs equipped with next-generation sequencing platforms and partnerships with global technology providers. Government incentives, particularly in Brazil, are strengthening genomic R&D, while regional trade policies are promoting access to clinical genomics technologies. Public-private collaborations in oncology and reproductive health testing are accelerating market adoption, even as healthcare infrastructure remains uneven across smaller economies in the region.

Modernization and Healthcare Diversification in Clinical Genomics

The Middle East & Africa accounted for 2.8% of the market in 2024, with the UAE and South Africa as major growth contributors. Demand is driven by precision medicine adoption in tertiary hospitals, integration into oncology testing, and reproductive health diagnostics. Government investments in genomics centers and partnerships with international institutions are fostering modernization. Technological advancements include digital bioinformatics platforms and mobile health integration, bridging infrastructure gaps. Regional trade partnerships are encouraging knowledge transfer and strengthening clinical genomics adoption across healthcare facilities. Although smaller in market size, the region represents a steadily diversifying opportunity.

United States – 39.5% Market Share

Strong clinical infrastructure, extensive sequencing capacity, and regulatory support drive leadership in oncology and rare disease genomics.

China – 15.2% Market Share

Large-scale population genomics projects and rising investment in sequencing infrastructure underpin dominance in clinical genomics adoption.

The Clinical Genomics market is highly competitive, with more than 150 active players globally ranging from diagnostic platform developers to bioinformatics providers and clinical service organizations. Competition is defined by continuous innovation in sequencing technologies, AI-powered analytics, and cloud-based genomic data platforms. Leading companies are pursuing mergers and acquisitions to consolidate testing portfolios, while partnerships with hospitals and academic research centers are expanding access to clinical data. Strategic initiatives include launching streamlined multi-panel diagnostic kits, scaling up population genomics projects, and enhancing long-read sequencing solutions. Innovation trends such as integration of liquid biopsy, epigenomic profiling, and decentralized testing solutions are intensifying competitive positioning, compelling companies to focus on differentiation through accuracy, turnaround time, and cost efficiency.

Illumina Inc.

Thermo Fisher Scientific Inc.

QIAGEN N.V.

F. Hoffmann-La Roche Ltd.

BGI Genomics Co. Ltd.

Agilent Technologies Inc.

Oxford Nanopore Technologies Plc

Pacific Biosciences of California Inc.

Color Genomics Inc.

Foundation Medicine Inc.

Technological progress is the central driver reshaping the Clinical Genomics market. Next-generation sequencing (NGS) platforms dominate due to scalability and high throughput, processing tens of thousands of samples monthly in leading facilities. Long-read sequencing is gaining traction for detecting structural variants and complex genomic rearrangements missed by short-read systems. Digital transformation trends, including cloud-based genomic data storage and distributed computing, are enabling faster cross-institutional collaboration while meeting data security standards. AI-powered bioinformatics pipelines reduce interpretation time from weeks to hours, while integrated clinical decision support systems are helping physicians adopt genomics more confidently in routine care. Point-of-care sequencing solutions, including portable rapid sequencing units, are improving accessibility in hospitals and regional labs. Reagent miniaturization and multiplexed panel development are cutting costs and broadening adoption, especially in reproductive and oncology genomics. Together, these technologies are driving efficiency, scalability, and clinical integration across the global Clinical Genomics market.

In February 2024, Illumina launched its NovaSeq X Plus sequencer upgrade, capable of producing over 20,000 whole genomes per year, reducing per-sample costs and supporting large-scale clinical diagnostics.

In April 2024, QIAGEN introduced its QIAseq Targeted cfDNA Panels designed for liquid biopsy testing in oncology, improving detection sensitivity for early-stage cancers.

In July 2023, BGI Genomics announced the establishment of a large-scale sequencing facility in Singapore, expanding capacity for population genomics and clinical diagnostic services across Asia-Pacific.

In October 2023, Thermo Fisher Scientific unveiled its Ion Torrent Genexus Dx Integrated Sequencer for clinical diagnostics, offering sample-to-report automation within a single day workflow.

The Clinical Genomics Market Report provides comprehensive coverage of global industry performance, segmented by type, application, end-user, and regional insights. The scope includes diagnostic test panels, consumables, bioinformatics platforms, and sequencing technologies shaping industry workflows. Applications span oncology profiling, reproductive genomics, newborn screening, and pharmacogenomics, each analyzed for adoption patterns and sectoral integration. End-user insights cover hospitals & clinics, academic institutions, government labs, and biotech/pharma companies. Geographically, the report evaluates North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing differences in demand drivers, infrastructure maturity, and regulatory landscapes. Emerging technologies such as AI-driven bioinformatics, long-read sequencing, cloud-based genomics, and portable point-of-care devices are highlighted as transformative. The report also explores niche growth areas including liquid biopsy, epigenomic profiling, and population genomics initiatives. By consolidating technological, regulatory, and strategic dimensions, this market report provides a precise roadmap for decision-makers, investors, and industry professionals navigating the Clinical Genomics landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 12546.3 Million |

|

Market Revenue in 2032 |

USD 30623.2 Million |

|

CAGR (2025 - 2032) |

11.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Illumina Inc., Thermo Fisher Scientific Inc., QIAGEN N.V., F. Hoffmann-La Roche Ltd., BGI Genomics Co. Ltd., Agilent Technologies Inc., Oxford Nanopore Technologies Plc, Pacific Biosciences of California Inc., Color Genomics Inc., Foundation Medicine Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |