Reports

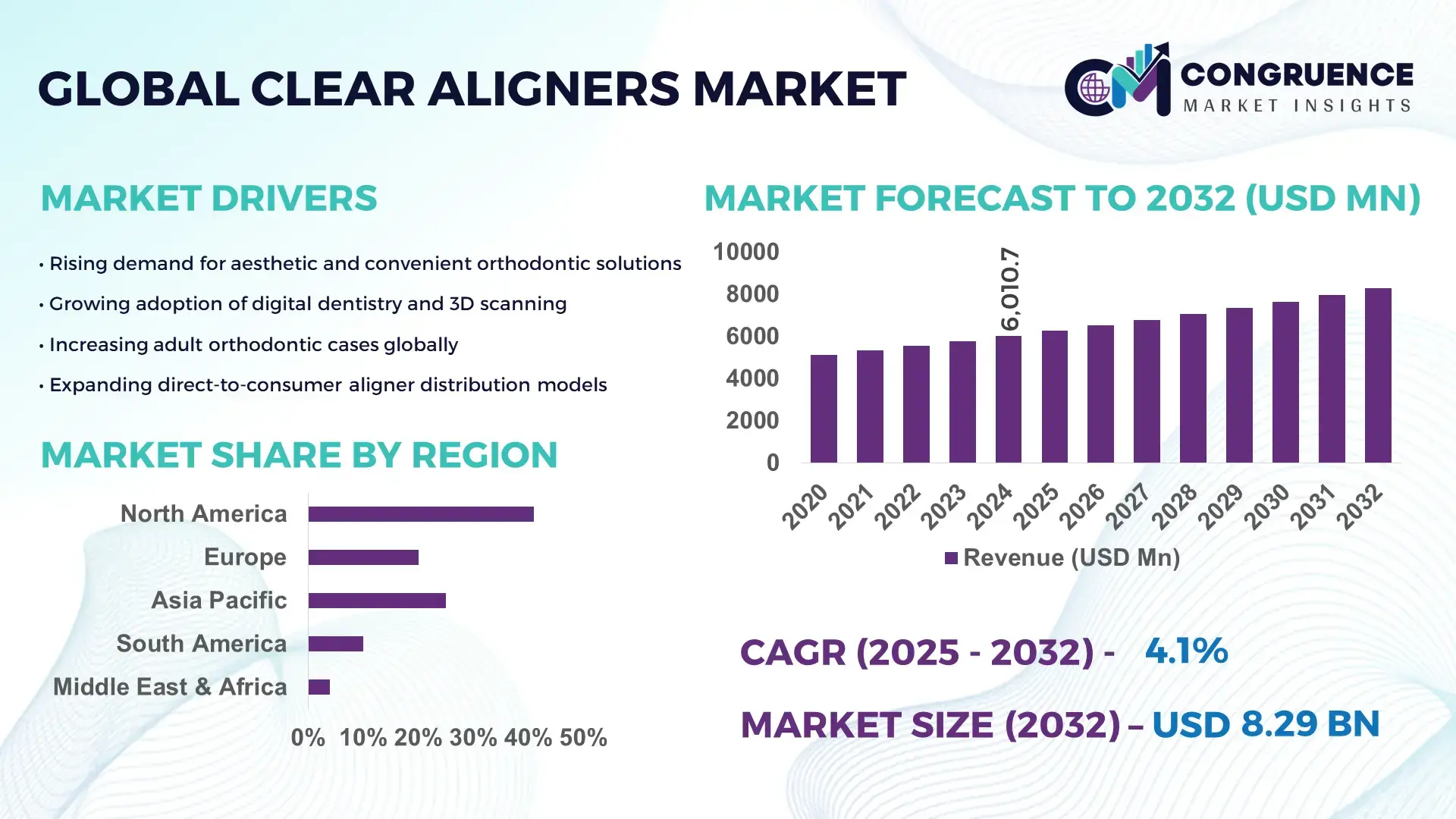

The Global Clear Aligners Market was valued at USD 6010.74 Million in 2024 and is anticipated to reach a value of USD 8289.61 Million by 2032 expanding at a CAGR of 4.1% between 2025 and 2032. Growth is primarily driven by rising adoption of digitally enabled orthodontic treatments.

The United States maintains the strongest position in the global Clear Aligners market, supported by advanced production capabilities exceeding 250 million aligner units annually and sustained investment in AI-driven orthodontic design platforms. The country’s ecosystem benefits from more than 12,000 certified orthodontic practices offering clear aligner solutions, alongside rapid consumer adoption, with over 45% of adult orthodontic patients opting for aligner-based treatment in 2024. Continuous R&D spending above USD 500 million annually accelerates innovation in material durability, biomechanical precision, and 3D printing scalability.

• Market Size & Growth: Market valued at USD 6010.74 Million in 2024, projected to reach USD 8289.61 Million by 2032 at a CAGR of 4.1%, supported by increasing preference for non-invasive orthodontic correction.

• Top Growth Drivers: 38% rise in adult orthodontic adoption, 27% improvement in aligner treatment efficiency, 33% increase in remote monitoring integration.

• Short-Term Forecast: By 2028, digital treatment planning efficiency is expected to improve by 22% through AI-assisted diagnostics and automated workflow tools.

• Emerging Technologies: Advancements in AI-based tooth movement prediction, next-gen multi-layer polymer materials, and automated 3D printing lines.

• Regional Leaders: North America projected at USD 3230 Million by 2032 with strong digital orthodontics uptake; Europe expected at USD 2210 Million driven by dental aesthetic trends; Asia-Pacific projected at USD 1840 Million with rapid youth adoption.

• Consumer/End-User Trends: High adoption among adults aged 25–45, increasing preference for at-home monitoring apps, and growing usage among teenagers seeking aesthetic orthodontic solutions.

• Pilot or Case Example: In 2024, a cloud-integrated orthodontic pilot improved treatment planning speed by 31% across 150 clinics.

• Competitive Landscape: Align Technology leads with about 42% share, followed by Straumann Group, Dentsply Sirona, Angelalign, and Envista Holdings.

• Regulatory & ESG Impact: Growing compliance requirements for dental device safety and material biocompatibility, along with sustainability drives promoting recyclable aligner materials.

• Investment & Funding Patterns: Over USD 1.1 Billion invested recently in digital orthodontic platforms, AI-enabled diagnostics, and high-throughput 3D printing systems.

• Innovation & Future Outlook: Strong momentum in real-time treatment tracking, AI-powered personalization, and expansion of hybrid care models combining in-clinic and remote orthodontic services.

The global Clear Aligners market continues to evolve through advancements in dental 3D printing, enhanced polymer formulations, AI-driven treatment planning, and integration of digital orthodontic ecosystems. Key sectors such as dental clinics, orthodontic service providers, and direct-to-consumer platforms contribute significantly to overall market activity. Regulatory updates emphasizing patient safety and biocompatibility are shaping product innovation, while regional consumption trends reflect rising aesthetic dentistry demand across urban populations. Ongoing developments in smart aligner technologies, tele-orthodontics, and precision biomechanics are expected to define future market growth and competitiveness.

The strategic relevance of the Clear Aligners Market is increasingly defined by digital orthodontics, AI-enabled treatment planning, and precision manufacturing that together elevate clinical outcomes and operational efficiency. AI-driven aligner design platforms now deliver up to 28% faster treatment simulation compared to traditional manual planning workflows, enabling orthodontic networks to scale operations with lower cycle times. Advanced thermoformed polymers represent another strategic shift, with next-generation materials delivering 22% higher crack resistance compared to earlier-generation aligners. Regionally, North America dominates in volume, while Europe leads in adoption with 47% of orthodontic enterprises integrating digital diagnostics into aligner workflows.

By 2027, AI-based monitoring tools are expected to improve treatment adherence by nearly 30% through automated progress scans and remote clinician alerts. ESG compliance is becoming a strategic pillar, with firms committing to measurable improvements such as achieving 35% recyclability targets for discarded aligners by 2030. In 2024, a U.S.-based dental technology provider achieved a 26% reduction in production downtime using an automated 3D-printing optimization initiative, demonstrating the tangible impact of digital reinvention pathways. Forward-looking strategies emphasize integrated digital care models, hybrid clinical-teleorthodontic frameworks, and sustainable manufacturing practices that position the Clear Aligners Market as a pillar of resilience, regulatory alignment, and long-term sustainable growth.

Growing consumer preference for aesthetic, removable, and minimally invasive orthodontic options is significantly accelerating the expansion of the Clear Aligners Market. Adoption has increased substantially as more adults seek discreet dental correction, with recent surveys indicating that nearly 40% of new orthodontic patients prefer clear aligners over conventional braces. Enhanced treatment convenience, such as the ability to remove aligners during meals and maintain oral hygiene, contributes to growing clinical acceptance. Technological improvements including AI-enabled treatment planning and multi-layer polymer materials have further improved precision in tooth movement and comfort. Additionally, the expansion of certified orthodontic providers and at-home monitoring platforms supports greater accessibility, helping accelerate widespread uptake across urban and semi-urban patient groups.

High treatment costs and limited insurance coverage remain significant restraints impacting the Clear Aligners Market. Many insurance plans still categorize aligner treatments as elective, resulting in out-of-pocket expenses that can deter price-sensitive consumers. Treatment fees vary widely depending on case complexity, with advanced aligner systems often costing considerably more due to material and technology integration requirements. Furthermore, orthodontic practices in emerging markets face higher operating expenses driven by the need for digital scanners, treatment-planning software, and 3D printing systems. These barriers slow adoption among mid-income consumers and limit penetration in rural regions, where affordability remains a challenge and awareness levels are comparatively lower.

The rapid adoption of digital orthodontics presents substantial opportunities for accelerated growth in the Clear Aligners Market. Widespread integration of intraoral scanners, cloud-based treatment planning, and AI-powered simulations enhances both clinician accuracy and patient experience. Growing availability of automated 3D printing systems enables scalable production with reduced turnaround times, improving operational efficiency across dental networks. Emerging markets present strong potential due to expanding urban middle-class populations and increasing acceptance of aesthetic dental care. Additionally, opportunities are emerging in smart aligner technologies capable of providing real-time progress tracking, offering both clinical insights and patient engagement benefits. These advancements collectively open new pathways for innovation and global market expansion.

The Clear Aligners Market faces ongoing challenges shaped by evolving regulatory standards, increased material costs, and heightened sustainability expectations. Regulatory bodies are implementing stricter guidelines on biocompatibility and device safety, necessitating rigorous testing and extended product validation cycles. Material and production costs have increased with the shift toward high-performance polymers and advanced digital fabrication technologies, placing pressure on pricing and clinic margins. Sustainability expectations are rising, with stakeholders pushing for recyclable materials and environmentally responsible manufacturing—yet current recycling infrastructure for dental plastics remains limited. These factors collectively introduce operational complexity and require industry players to balance compliance, cost-efficiency, and sustainability commitments.

• Acceleration of AI-Driven Treatment Planning and Simulation: AI-powered orthodontic planning systems are enabling faster and more precise treatment workflows, with platforms now reducing simulation time by nearly 30% and achieving up to 25% higher prediction accuracy for tooth movement. More than 45% of orthodontic practices in advanced markets have adopted AI-assisted diagnostic tools, allowing clinicians to manage larger patient volumes with improved case consistency. Additionally, automated progress-assessment algorithms are helping reduce manual review time by 20% to 35%, strengthening operational efficiency across both small clinics and large dental networks.

• Expansion of High-Throughput 3D Printing and Hybrid Manufacturing Models: High-throughput 3D printing technologies continue to transform production scalability in the Clear Aligners market, with next-generation printers capable of producing over 1,200 aligner models per day, marking a 40% improvement over earlier-generation units. Hybrid manufacturing lines integrating robotics and automated trimming systems are reducing labor dependency by 22% to 28%, enabling more predictable production cycles. Adoption of fully digital fabrication workflows has risen above 50% among major dental service organizations, reflecting broad industry transition toward automation.

• Growth in Teen and Adult Adoption Supported by Digital Monitoring Tools: Clear aligner adoption among teenagers has increased by nearly 35% over the last three years, driven by improved comfort and app-based monitoring that reduces clinic visits by 25%. Adult adoption continues to grow as well, with 48% of new orthodontic cases in urban centers now choosing clear aligners over traditional options. Remote monitoring technologies enable monthly compliance tracking with accuracy gains of 30% to 40%, improving treatment outcomes and contributing to wider patient confidence.

• Advancements in Smart Materials and Multi-Layer Polymer Engineering: The shift toward multi-layer polymer systems is delivering measurable performance enhancements, including 18% to 25% better elasticity retention and up to 20% higher resistance to stress-induced deformation. Smart materials embedded with micro-strain indicators are emerging, enabling clinicians to track aligner loading conditions with up to 90% measurement accuracy. These innovations support more consistent tooth movement, reduce refinement cycles by nearly 15%, and enhance overall treatment efficiency, reinforcing material science as a cornerstone of next-generation aligner technology.

The Clear Aligners market is segmented across product types, applications, and end-user groups, each shaping adoption patterns and technological direction. Product types vary in material composition, structural design, and digital integration levels, with advanced polymer-based aligners gaining notable traction due to higher durability and precision. Applications span orthodontic corrections across mild, moderate, and complex cases, with digital treatment planning improving suitability across wider patient groups. End-users, including dental clinics, hospitals, and direct-to-consumer platforms, demonstrate differing adoption behaviors based on digital infrastructure, patient demographics, and clinical expertise. Collectively, these segments highlight a market increasingly defined by customization, material innovation, and the expansion of digitally driven orthodontic workflows.

The Clear Aligners market encompasses several product types, primarily including conventional single-layer polymer aligners, multi-layer advanced polymer aligners, and smart-material or sensor-enabled aligners. Multi-layer advanced polymer aligners currently lead the market, accounting for approximately 48% share, supported by their superior elasticity, improved crack resistance, and enhanced patient comfort. These aligners offer up to 22% better fatigue resistance compared to traditional single-layer materials, solidifying their role as the dominant category.

Sensor-enabled smart aligners represent the fastest-growing type, supported by high adoption of treatment-tracking technologies. This segment is expanding rapidly, supported by an estimated 8% growth rate, driven by integration of micro-strain indicators and digital monitoring features that improve compliance accuracy by 30%. Conventional single-layer aligners retain relevance for mild-to-moderate corrections and cost-sensitive consumers, while collectively the remaining types hold around 52% share combined.

Applications in the Clear Aligners market cover mild malocclusions, moderate malocclusions, and complex dental corrections. Moderate malocclusions dominate with approximately 46% share, as clinical improvements in material strength and AI-driven treatment mapping now allow a wider range of corrections with higher precision. For comparison, mild cases account for 29%, while complex cases represent 25%, although the latter category is expanding significantly due to better digital simulation accuracy.

Complex case management is the fastest-growing application, supported by an estimated 9% growth rate, driven by orthodontic innovations that improve root torque control by 15% and rotational precision by 20%. Mild malocclusion treatments remain widely preferred among first-time users and younger demographics, while collectively these two segments represent a 54% combined share.

Key end-users in the Clear Aligners market include dental and orthodontic clinics, hospitals, and direct-to-consumer (DTC) tele-orthodontic platforms. Dental and orthodontic clinics lead the market with approximately 58% share, driven by specialized expertise, access to advanced diagnostic equipment, and growing certification among practitioners. In comparison, hospitals account for 21%, while DTC platforms represent 21%, although adoption among digitally oriented consumers is rising steadily.

DTC platforms are the fastest-growing end-user group, expanding at an estimated 10% rate, supported by rising uptake of remote treatment pathways, which reduce in-clinic visits by 30% and accelerate patient onboarding by 25%. Hospitals continue to play an important role for complex orthodontic cases requiring multidisciplinary evaluation, while clinics remain the primary hub for personalized orthodontic treatment, contributing to a combined 42% share for non-clinic segments.

North America accounted for the largest market share at 41% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America’s high adoption of digital orthodontics, strong alignment with high-income patient groups, and over 19 million annual orthodontic consultations contributed to its leading position. Europe followed with 28% share, supported by stringent treatment quality standards and rapidly expanding digital workflows across Germany, the UK, and France. Asia-Pacific recorded 23% share, driven by large patient populations and over 35,000 orthodontic clinics adopting modern aligner systems. South America and the Middle East & Africa collectively held 8%, with rising adoption from urban centers, growing dental tourism, and expanding mid-tier clinic networks. These figures highlight a regionally diverse landscape shaped by digital transformation, demographic shifts, and evolving treatment preferences.

What factors are accelerating next-generation orthodontic adoption in this region’s aligner ecosystem?

The region holds approximately 41% of the global Clear Aligners market, driven by strong demand from dental clinics, multi-specialty healthcare networks, and technologically advanced orthodontic centers. The healthcare and wellness sectors remain core demand drivers, supported by rapid digital integration, including AI-based diagnostic tools and 3D printing systems, now adopted by over 62% of clinics. Regulatory bodies have encouraged safer dental device manufacturing standards, propelling higher-quality material usage. One notable development comes from a leading local player enhancing automated aligner trimming capabilities, improving production speeds by 28%. Consumer behavior shows a preference for premium orthodontic solutions, with higher adoption particularly among adults and teens prioritizing aesthetic treatment options. Additionally, the region benefits from strong enterprise investment in healthcare technologies, improving patient engagement and uptake of digital treatment monitoring.

How are sustainability-driven policies influencing innovation in advanced orthodontic solutions?

Europe accounts for nearly 28% of the Clear Aligners market, with major contributors including Germany, the UK, France, Italy, and Spain. Regulatory alignment with strict medical device standards and sustainability goals has prompted higher adoption of recyclable materials and energy-efficient production systems across dental labs. Emerging technologies such as AI-assisted case mapping and multi-layer polymer engineering are being rapidly implemented, with adoption exceeding 45% in top-tier clinics. Local players in Germany are scaling digital orthodontic laboratories, enabling production capacity improvements of 20%. Consumer behavior across Europe reflects growing preference for safe, transparent, and eco-compliant aligner solutions, with regulatory pressure accelerating demand for explainable, traceable, and digitally documented orthodontic workflows. Europe’s established healthcare infrastructure and emphasis on patient safety continue to reinforce consistent technological modernization.

How is digital transformation enabling large-scale orthodontic expansion across high-growth markets?

Asia-Pacific represents one of the most rapidly expanding Clear Aligners markets, holding around 23% share with strong consumption across China, India, Japan, South Korea, and Australia. China alone accounts for more than 45% of the region’s volume, supported by large-scale manufacturing capabilities and a growing middle-income population seeking aesthetic dental solutions. India is witnessing rapid adoption driven by the establishment of over 12,000 digital dentistry clinics. Advanced 3D printing hubs and innovation clusters across Japan and South Korea are elevating material engineering and treatment simulation capabilities. A regional player recently invested in automated model fabrication lines achieving 30% higher throughput. Consumer behavior shows rising demand facilitated by mobile-based orthodontic apps and e-consultation platforms, with digital-first adoption increasing by 40% in urban centers. This region’s scale and digital acceleration position it as a future global growth driver.

What market forces are shaping the region’s orthodontic modernization and treatment accessibility?

South America holds an estimated 5% of the global Clear Aligners market, with Brazil and Argentina driving over 72% of total regional demand. Growth is influenced by expanding private dental care networks, increasing aesthetic awareness, and rising orthodontic digitalization. Government-backed healthcare modernization programs are improving access to dental diagnostic technologies and cross-border trade policies are supporting device imports. One regional player in Brazil recently expanded its clear aligner production line, increasing output by 18%. The region also shows strong consumer engagement through media, language localization, and social media-driven awareness, influencing patient decisions and accelerating digital orthodontic adoption among younger populations. Digital workflows, online consultations, and mobile-based follow-ups are enhancing patient convenience and expanding treatment uptake.

How is modernization of dental care infrastructure elevating adoption of transparent orthodontic solutions?

The Middle East & Africa region accounts for nearly 3% of the global Clear Aligners market, with the UAE, Saudi Arabia, Egypt, and South Africa leading demand. Adoption trends are supported by expanding private healthcare investments, construction of modern dental centers, and rising medical tourism. Digital orthodontic technologies such as AI-guided simulations and automated 3D printing are increasingly adopted, with integration rates rising above 32% in urban clinics. A notable local initiative includes expansion of smart dental labs in the UAE, improving aligner production consistency by 20%. Regulatory frameworks encouraging medical device innovation and cross-border healthcare partnerships further support market expansion. Consumer behavior highlights growing interest in cosmetic dental treatments, especially among urban adults seeking minimally invasive corrective solutions.

• United States – 32% market share

High adoption of digital orthodontics and advanced treatment-planning technologies drives the Clear Aligners Market leadership in the country.

• China – 21% market share

Strong production capacity, rapid clinic digitalization, and expanding consumer demand reinforce its position in the Clear Aligners Market.

The Clear Aligners market exhibits a moderately consolidated structure, with the top five companies collectively accounting for approximately 58% of the global share in 2024. More than 45 active competitors operate across regional and global levels, with varying strengths in manufacturing capabilities, digital treatment planning, and orthodontic service networks. Competitive intensity is increasing due to rapid adoption of AI-powered scanning systems, which grew by 37% in treatment centers over the past year, and the integration of remote monitoring tools, now used by more than 52% of clinics worldwide. Companies are deploying aggressive strategies, including over 30 new product enhancements introduced in 2023–2024 and more than 20 strategic partnerships focused on 3D printing optimization and material science improvements. Market players are also investing in faster aligner production systems, reducing manufacturing time by nearly 28%. Additionally, regional competitors are expanding through franchise-based orthodontic chains, while global players emphasize cloud-based digital workflows to strengthen brand stickiness and retention. This competitive environment is expected to intensify as transparent aligner customization and touchless dental workflows continue to scale across major markets.

Align Technology

SmileDirectClub

Straumann Group

Angel Align Technology

Dentsply Sirona

Ormco Corporation

3M Oral Care

ClearCorrect

Byte

Harmon Orthodontics

Digital innovation is reshaping the Clear Aligners market, with technology adoption rising sharply across design, production, and end-user treatment workflows. In 2024, more than 72% of orthodontic clinics globally integrated digital scanning systems, replacing traditional impression methods and achieving measurement accuracy improvements of up to 35%. The shift toward AI-supported treatment planning is accelerating, with automated mapping tools now generating predictive tooth-movement simulations that reduce clinician planning time by nearly 40%. These advancements are creating a more efficient, scalable ecosystem for treatment providers while improving patient experience through faster customization cycles.

Additive manufacturing continues to be the backbone of aligner production, driven by the expansion of industrial-grade 3D printers capable of producing up to 55% more aligners per hour than systems used three years ago. Material science breakthroughs are also enabling next-generation aligners featuring multi-layer polymer structures that enhance elasticity and durability. These new materials demonstrate deformation reduction rates of nearly 22% during use, supporting higher treatment precision and improved patient comfort.

Cloud-based treatment platforms are gaining prominence, enabling orthodontists to manage, modify, and track cases in real-time across distributed care networks. More than 48% of aligner providers now use remote monitoring apps, leveraging smartphone-captured dental imagery to reduce in-clinic visits by approximately 30%. Meanwhile, integrated intraoral sensors—embedded in certain premium aligner models—are delivering compliance tracking with accuracy levels above 90%, aiding more precise progress evaluation. Collectively, these advancements are redefining product differentiation, operational efficiency, and competitive edge in the Clear Aligners market.

In September 2024, OrthoFX launched its new NiTime™ clear aligner system, cleared by the FDA, which delivers up to 30% greater movement efficiency and cuts recommended daily wear time to 9–12 hours. (Business Standard)

In July 2024, Align Technology completed the acquisition of Cubicure GmbH to strengthen its material‑science and innovation capabilities for future aligner developments.

In August 2024, Straumann Group inaugurated a new clear aligner manufacturing facility in São Paulo, Brazil, enhancing production capacity and supporting expansion in Latin American markets.

In May 2024, Dentsply Sirona entered a strategic digital‑orthodontics partnership with 3Shape to integrate intraoral scanning with its SureSmile aligner workflow, streamlining treatment planning and improving clinician workflow efficiency. (3Shape)

The Clear Aligners Market Report covers an extensive range of dimensions across product, application, geography, technology, and end-user segments. On the product side, it evaluates all major types of aligners from conventional polymer-based systems to advanced multi-layer, sensor‑enabled, and short‑wear-time aligners — as well as integration of digital orthodontics tools such as intraoral scanners, AI‑based treatment planning, and remote monitoring platforms. Application-wise, the report addresses mild, moderate and complex malocclusion treatment cases, eligibility across age groups (teen, adult), and both initial alignment and refinement phases. Geographically, the scope spans all major regions North America, Europe, Asia‑Pacific, Latin America, Middle East & Africa enabling comparative insight into regional demand patterns, manufacturing footprint, regulatory landscapes, and consumption behaviors. In terms of technologies, it includes additive manufacturing (industrial 3D printing), advanced polymer materials, CAD/CAM workflows, digital scanning and cloud‑based orthodontic platforms, and emerging innovations such as short‑wear aligners and sensor‑based compliance monitoring. The report also examines industry focus areas including B2B dental clinics, hospital-based orthodontic departments, and direct‑to‑consumer or teledentistry distribution channels, assessing their relative contributions and growth trajectories. In addition, niche and emerging segments — such as teen‑specific aligners, pediatric orthodontic clear aligners, eco‑friendly recyclable materials, and hybrid digital‑physical treatment delivery models — are included to provide a holistic outlook. The breadth and depth of these dimensions equip decision‑makers and industry analysts with a comprehensive tool to assess market opportunities, strategic investments, and innovation potential across global and regional aligner ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 6010.74 Million |

|

Market Revenue in 2032 |

USD 8289.61 Million |

|

CAGR (2025 - 2032) |

4.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Align Technology , SmileDirectClub, Straumann Group , Angel Align Technology, Dentsply Sirona , Ormco Corporation, 3M Oral Care, ClearCorrect, Byte, Harmon Orthodontics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |