Reports

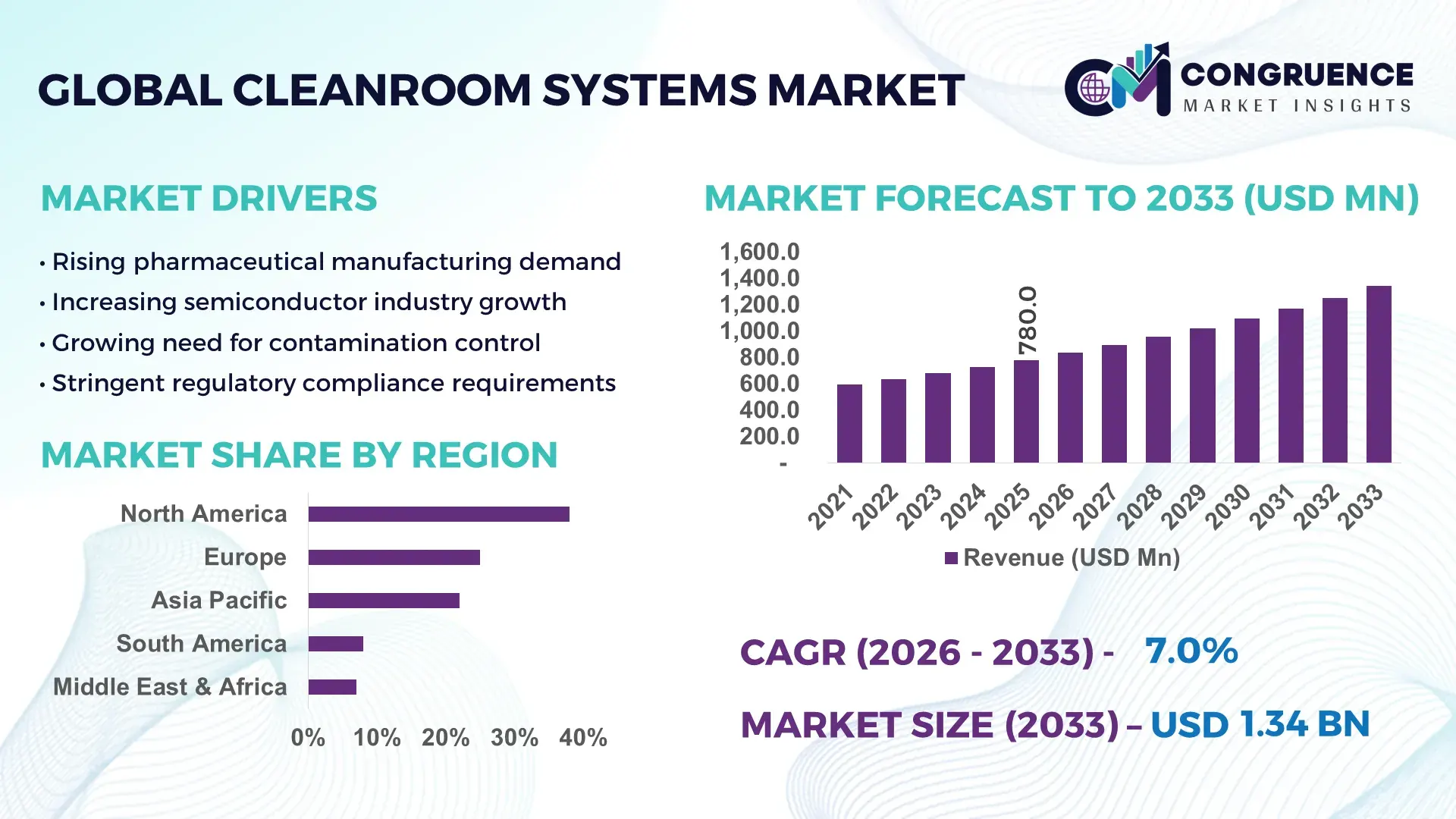

The Global Cleanroom Systems Market was valued at USD 780.0 Million in 2025 and is anticipated to reach a value of USD 1,340.2 Million by 2033 expanding at a CAGR of 7.0% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by increasing demand for contamination-free manufacturing environments across pharmaceuticals, biotechnology, and semiconductor industries.

The United States dominates the Cleanroom Systems Market with strong industrial integration across pharmaceuticals, biotechnology, and semiconductor manufacturing. The country accounts for over 35% of global semiconductor fabrication facilities and hosts more than 2,000 FDA-approved drug manufacturing plants requiring ISO-class cleanrooms. Over 60% of biologics production facilities in North America rely on advanced modular cleanroom systems. Additionally, U.S. investments in semiconductor manufacturing exceeded USD 50 billion between 2022 and 2025, boosting demand for high-efficiency particulate air (HEPA) and ultra-low penetration air (ULPA) filtration systems. Adoption of automated cleanroom monitoring technologies has surpassed 48% among large-scale manufacturers, improving contamination control and operational efficiency.

Market Size & Growth: USD 780.0 Million in 2025, projected to reach USD 1,340.2 Million by 2033, growing at 7.0% CAGR, driven by rising pharmaceutical and semiconductor manufacturing demand.

Top Growth Drivers: 65% rise in biologics production demand, 52% increase in semiconductor fabrication investments, 48% improvement in contamination control efficiency.

Short-Term Forecast: By 2028, operational efficiency in cleanroom facilities is expected to improve by 30% through automation and smart monitoring systems.

Emerging Technologies: AI-based contamination monitoring, modular prefabricated cleanrooms, IoT-enabled environmental control systems.

Regional Leaders: North America (~USD 420 Million by 2033) driven by biotech demand; Asia-Pacific (~USD 500 Million) driven by electronics manufacturing; Europe (~USD 300 Million) driven by regulatory compliance.

Consumer/End-User Trends: Pharmaceutical firms account for over 45% usage, followed by semiconductors at 30%, with increasing adoption in medical devices.

Pilot or Case Example: In 2024, a semiconductor facility reduced contamination rates by 35% using AI-driven cleanroom monitoring systems.

Competitive Landscape: Market leader holds ~18% share, followed by Azbil Corporation, Kimberly-Clark, Illinois Tool Works, and Taikisha Ltd.

Regulatory & ESG Impact: Over 70% of facilities are adopting energy-efficient HVAC systems to comply with environmental standards.

Investment & Funding Patterns: Over USD 12 billion invested globally in semiconductor and pharma infrastructure between 2023–2025.

Innovation & Future Outlook: Integration of robotics and smart filtration systems is expected to redefine operational efficiency and contamination control.

Cleanroom systems are increasingly integrated across pharmaceuticals (45%), semiconductors (30%), and medical devices (15%), reflecting diverse industrial reliance. Innovations such as energy-efficient HVAC systems and real-time contamination monitoring are improving operational precision. Regulatory mandates for ISO certification and sustainability compliance are shaping demand. Asia-Pacific consumption exceeds 40%, driven by manufacturing expansion, while automation and modular construction are emerging as key future trends.

The Cleanroom Systems Market holds strategic importance across high-precision industries where contamination control directly impacts product quality, regulatory compliance, and operational efficiency. Increasing investments in biologics, semiconductor fabrication, and advanced medical device manufacturing are reinforcing the need for high-performance cleanroom environments. For instance, modular cleanroom systems deliver 35% faster installation compared to traditional stick-built cleanrooms, significantly reducing project timelines and operational downtime.

Advanced AI-powered environmental monitoring systems deliver 28% improvement in contamination detection accuracy compared to conventional manual inspection methods. North America dominates in volume, while Asia-Pacific leads in adoption with over 55% of manufacturing enterprises integrating automated cleanroom technologies. By 2028, AI-driven predictive maintenance is expected to reduce system downtime by 32%, enhancing productivity in high-value manufacturing sectors.

From an ESG perspective, firms are committing to energy efficiency improvements, targeting 25% reduction in HVAC energy consumption by 2030. Cleanroom facilities account for nearly 40% of energy consumption in pharmaceutical plants, prompting investments in sustainable airflow and filtration technologies. In 2025, Japan achieved a 20% reduction in cleanroom energy usage through implementation of advanced airflow optimization systems, demonstrating measurable efficiency gains.

Strategically, the Cleanroom Systems Market is evolving as a critical pillar supporting global supply chain resilience, regulatory compliance, and sustainable industrial growth. As industries demand higher precision and operational efficiency, cleanroom systems will remain integral to future manufacturing ecosystems.

The Cleanroom Systems Market is shaped by a combination of industrial expansion, regulatory compliance requirements, and technological innovation. Increasing demand from pharmaceutical and biotechnology industries, which account for over 45% of cleanroom installations, is a primary influence. Semiconductor manufacturing contributes approximately 30% of demand, driven by the need for ultra-clean environments to prevent micro-contamination. Advancements in modular cleanroom systems have reduced installation timelines by nearly 40%, improving scalability and flexibility for manufacturers. Additionally, stringent ISO and GMP standards are compelling companies to upgrade existing facilities. Emerging economies are witnessing over 50% growth in cleanroom adoption across electronics and healthcare manufacturing sectors. Automation and IoT integration are further transforming operational efficiency, enabling real-time monitoring and predictive maintenance. However, high initial investment and operational costs continue to influence purchasing decisions among small and medium enterprises.

The rapid expansion of pharmaceutical and semiconductor industries is significantly driving demand for cleanroom systems. Over 70% of pharmaceutical manufacturing processes require controlled environments to meet regulatory standards, particularly in biologics and vaccine production. Semiconductor fabrication facilities require ISO Class 1–5 cleanrooms, where even microscopic particles can disrupt production yields. Global chip manufacturing capacity increased by more than 20% between 2022 and 2025, necessitating advanced contamination control solutions. Additionally, over 60% of new drug manufacturing plants are incorporating modular cleanrooms for faster deployment. The increasing complexity of medical devices, with nearly 45% requiring sterile production conditions, further accelerates adoption. This surge in high-precision manufacturing is creating sustained demand for advanced cleanroom systems globally.

Cleanroom systems involve significant capital investment, which acts as a restraint for widespread adoption, especially among small and medium enterprises. Installation costs for advanced cleanrooms can be up to 30% higher than conventional industrial setups due to specialized materials, filtration systems, and environmental controls. Operational expenses are also substantial, with HVAC systems accounting for nearly 50% of total energy consumption in cleanroom facilities. Maintenance costs, including periodic filter replacements and system calibration, add further financial burden. Additionally, compliance with evolving regulatory standards requires continuous upgrades, increasing lifecycle costs. Energy-intensive operations and the need for skilled personnel further limit adoption, particularly in developing regions where cost sensitivity remains high.

Technological advancements present significant opportunities for the Cleanroom Systems Market, particularly through automation and smart monitoring systems. Adoption of IoT-enabled sensors has increased by over 45% in advanced facilities, enabling real-time environmental monitoring and predictive maintenance. Modular cleanrooms offer 40% faster deployment, allowing manufacturers to scale operations efficiently. Integration of AI-driven contamination detection systems improves operational accuracy by nearly 30%, reducing product rejection rates. Emerging applications in cell and gene therapy, which require ultra-clean environments, are expanding market scope. Additionally, increasing demand for sustainable solutions is driving innovation in energy-efficient HVAC systems, capable of reducing energy consumption by up to 25%. These advancements are opening new growth avenues across multiple industries.

The Cleanroom Systems Market faces challenges due to complex regulatory requirements and shortages of skilled professionals. Compliance with ISO standards and Good Manufacturing Practices requires rigorous validation and documentation processes, increasing operational complexity. Over 40% of facilities report delays in project completion due to regulatory approvals and inspections. Additionally, there is a shortage of trained personnel capable of managing advanced cleanroom technologies, with nearly 35% of companies facing workforce gaps in technical roles. Continuous upgrades to meet evolving standards further strain resources. Variability in global regulations also complicates international operations, requiring customized solutions for different markets. These challenges impact efficiency, cost management, and scalability for organizations operating in the cleanroom ecosystem.

Increased Adoption of Smart Monitoring Systems: Over 48% of cleanroom facilities have implemented IoT-based monitoring systems, enabling real-time tracking of particulate levels and environmental parameters. These systems improve operational efficiency by 30% and reduce contamination incidents by 25%, enhancing productivity in high-precision manufacturing environments.

Expansion of Modular Cleanroom Solutions: Approximately 55% of new cleanroom installations utilize modular and prefabricated designs, reducing construction time by 40%. These systems allow rapid scalability, particularly in pharmaceutical and semiconductor industries, where demand fluctuations require flexible infrastructure solutions.

Rising Focus on Energy Efficiency: Nearly 70% of cleanroom operators are adopting energy-efficient HVAC systems to reduce operational costs. Advanced airflow management technologies have achieved up to 25% reduction in energy consumption, addressing sustainability goals and regulatory compliance requirements.

Integration of Robotics and Automation: Automation is being integrated into over 45% of cleanroom environments, improving process precision and reducing human-induced contamination by 35%. Robotics applications are particularly prominent in semiconductor and biologics manufacturing, enhancing throughput and consistency.

The Cleanroom Systems Market is segmented based on type, application, and end-user industries, each contributing uniquely to overall demand patterns. By type, modular cleanrooms dominate due to their flexibility and reduced installation timelines, while conventional cleanrooms maintain relevance in large-scale industrial setups. Applications are primarily concentrated in pharmaceuticals, semiconductors, and medical devices, collectively accounting for over 85% of total usage. End-user industries include biotechnology firms, electronics manufacturers, and healthcare institutions, each requiring varying levels of contamination control. Increasing demand for precision manufacturing and regulatory compliance is influencing segmentation trends, with modular and automated solutions gaining traction across industries.

Modular cleanrooms hold the largest share at approximately 48%, driven by their flexibility, faster installation, and cost efficiency. Conventional cleanrooms account for around 32%, preferred for large-scale and permanent installations requiring high customization. However, softwall cleanrooms are the fastest-growing segment, with adoption increasing at a CAGR of 8.5%, due to their affordability and ease of deployment in smaller facilities. Remaining segments, including hardwall and hybrid cleanrooms, collectively contribute about 20% of the market, catering to niche applications requiring specific contamination control levels.

• In 2025, a leading semiconductor manufacturer implemented modular cleanrooms across 5 fabrication units, reducing setup time by 38% and improving production efficiency for over 12 million chips annually.

Pharmaceutical manufacturing leads with a 45% share due to strict regulatory requirements for sterile environments. Semiconductor manufacturing follows with 30%, while medical devices account for 15%. Biotechnology and food processing collectively contribute 10%. Biotechnology applications are the fastest-growing, with a CAGR of 8.2%, driven by advancements in gene therapy and biologics production. In 2025, over 42% of pharmaceutical companies reported upgrading cleanroom systems to meet advanced regulatory standards. Additionally, 38% of semiconductor manufacturers increased investments in cleanroom automation to enhance yield efficiency.

• In 2025, over 150 hospitals globally implemented cleanroom-based sterile processing units, improving infection control efficiency by 28%.

Pharmaceutical and biotechnology companies dominate with a 50% share, followed by electronics manufacturers at 30% and healthcare institutions at 12%. Research laboratories and others contribute the remaining 8%. Biotechnology firms represent the fastest-growing segment with a CAGR of 8.7%, driven by increasing R&D investments. In 2025, more than 40% of enterprises globally reported adopting cleanroom automation technologies to improve operational efficiency. Additionally, 35% of healthcare facilities integrated advanced sterile environments to reduce infection risks.

• In 2025, over 500 biotech firms expanded cleanroom capacities, increasing production efficiency by 25% through advanced automation technologies.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.5% between 2026 and 2033.

North America leads due to strong pharmaceutical and semiconductor industries, while Asia-Pacific benefits from rapid industrialization. Europe holds approximately 25% share, driven by regulatory compliance and sustainability initiatives. South America accounts for 8%, while Middle East & Africa contribute 7%. Asia-Pacific’s growth is supported by over 50% increase in electronics manufacturing capacity, while North America continues to invest heavily in biotech and semiconductor infrastructure.

North America holds approximately 38% market share, driven by pharmaceutical, biotechnology, and semiconductor industries. Regulatory frameworks such as FDA guidelines enforce strict contamination control standards. Over 60% of pharmaceutical facilities utilize advanced cleanroom systems. Companies are adopting automation and AI-driven monitoring, with nearly 50% integration across large facilities. A leading player has implemented smart cleanrooms improving efficiency by 30%. Consumer behavior shows higher enterprise adoption in healthcare and finance sectors.

Europe accounts for around 25% market share, led by Germany, the UK, and France. Strong regulatory requirements and sustainability initiatives drive adoption. Over 65% of facilities are transitioning to energy-efficient systems. Advanced technologies such as modular cleanrooms are widely adopted. Local manufacturers are investing in eco-friendly filtration technologies. Consumer behavior reflects demand for compliance-driven solutions.

Asia-Pacific is the fastest-growing region, with over 50% increase in manufacturing capacity. China, India, and Japan are key markets. Electronics and pharmaceutical industries drive demand. Over 45% of facilities are adopting modular cleanrooms. Local players are expanding production capabilities. Consumer behavior is driven by rapid industrialization and technology adoption.

South America holds around 8% market share, led by Brazil and Argentina. Infrastructure development and healthcare expansion drive demand. Government incentives support industrial growth. Local companies are investing in cleanroom technologies. Consumer behavior is influenced by regional industrialization.

Middle East & Africa account for 7% share, with UAE and South Africa leading. Growth is driven by healthcare and industrial diversification. Technological modernization is increasing adoption. Local regulations support cleanroom implementation. Consumer behavior reflects increasing demand for advanced manufacturing solutions.

United States – 35% Market share: Strong pharmaceutical and semiconductor manufacturing base

China – 28% Market share: Rapid expansion in electronics and industrial production

The Cleanroom Systems Market is moderately fragmented, with over 150 active global and regional players competing across product innovation, customization, and service capabilities. The top five companies collectively account for approximately 45% of the market share, indicating a competitive yet partially consolidated environment. Key players focus on modular cleanroom solutions, energy-efficient HVAC systems, and advanced filtration technologies to differentiate their offerings. Strategic partnerships, mergers, and acquisitions are common, with over 30 major collaborations recorded between 2023 and 2025.

Companies are investing heavily in R&D, with nearly 12% of annual budgets allocated to innovation in automation and contamination monitoring systems. Product launches featuring IoT-enabled cleanroom solutions have increased by 40% in recent years. Regional players compete by offering cost-effective solutions tailored to local regulatory requirements. Competitive intensity is further driven by increasing demand from pharmaceuticals and semiconductor industries, pushing companies to enhance technological capabilities and expand global footprints.

Dupont

Kimtech

Azbil Corporation

Illinois Tool Works Inc.

Ardmac Ltd.

M+W Group (Exyte)

Clean Air Products

Terra Universal Inc.

AES Clean Technology

Angstrom Technology

Connect 2 Cleanrooms

Simplex Isolation Systems

Allied Cleanrooms

Cleanroom systems are increasingly leveraging advanced technologies to enhance contamination control, operational efficiency, and sustainability. IoT-enabled sensors are deployed in over 48% of facilities, enabling real-time monitoring of temperature, humidity, and particulate levels. AI-driven analytics improve contamination detection accuracy by 28%, reducing product rejection rates. Automation technologies, including robotics, are integrated into 45% of cleanroom environments, minimizing human intervention and reducing contamination risks by 35%. Advanced filtration systems such as HEPA and ULPA filters achieve efficiency levels exceeding 99.999%, ensuring ultra-clean environments.

Energy-efficient HVAC systems are reducing power consumption by up to 25%, addressing sustainability concerns. Modular cleanroom technologies allow 40% faster deployment, enhancing scalability for industries with dynamic production needs. Digital twin technology is emerging as a key innovation, enabling simulation and optimization of cleanroom performance. These advancements are transforming cleanroom operations, making them more efficient, reliable, and adaptable to evolving industrial requirements.

• In March 2024, Exyte expanded its cleanroom and high-tech facility capabilities through the acquisition of CollabraTech Solutions in Arizona, strengthening its delivery systems and contract manufacturing expertise for semiconductor and life sciences cleanroom environments. Source: www.exyte.net

• In 2024, Exyte further reinforced its pharmaceutical cleanroom engineering portfolio by acquiring TTP Group, a European consulting and engineering firm, enhancing its ability to design and deliver advanced GMP-compliant cleanroom facilities across biopharma and chemical industries.

• In January 2025, DuPont expanded its cleanroom solutions portfolio by advancing contamination-control materials and protective garment technologies designed for high-performance environments, supporting increased demand from semiconductor and pharmaceutical manufacturing sectors.

• In 2025, Azbil Corporation accelerated deployment of smart cleanroom automation systems integrating IoT-based environmental monitoring and control, improving contamination management and operational efficiency in regulated manufacturing environments.

The Cleanroom Systems Market Report provides a comprehensive analysis of industry dynamics, segmentation, regional trends, and competitive landscape across key global markets. The scope covers various types of cleanroom systems, including modular, conventional, softwall, and hybrid configurations, each serving distinct industrial requirements. Applications analyzed include pharmaceuticals, biotechnology, semiconductors, medical devices, and food processing, collectively accounting for over 85% of market demand. The report evaluates end-user industries such as healthcare, electronics manufacturing, and research laboratories, highlighting their adoption patterns and operational requirements.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, covering more than 20 key countries contributing to global demand. It includes analysis of regulatory frameworks, technological advancements, and infrastructure development influencing market growth. The study also examines emerging trends such as automation, IoT integration, and energy-efficient systems, which are transforming cleanroom operations.

Additionally, the report explores niche segments such as cleanrooms for cell and gene therapy, which are gaining traction due to increasing demand for advanced healthcare solutions. It provides insights into innovation strategies, investment patterns, and competitive positioning of key market players. The scope is designed to support decision-makers with actionable insights, enabling strategic planning and informed investment decisions in the evolving cleanroom systems market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 780.0 Million |

| Market Revenue (2033) | USD 1,340.2 Million |

| CAGR (2026–2033) | 7.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Taikisha Ltd.; Dupont; Kimtech; Azbil Corporation; Illinois Tool Works Inc.; Ardmac Ltd.; M+W Group (Exyte); Clean Air Products; Terra Universal Inc.; AES Clean Technology; Angstrom Technology; Connect 2 Cleanrooms; Simplex Isolation Systems; Allied Cleanrooms |

| Customization & Pricing | Available on Request (10% Customization Free) |