Global Circulating Tumor DNA (ctDNA) Market Report Overview

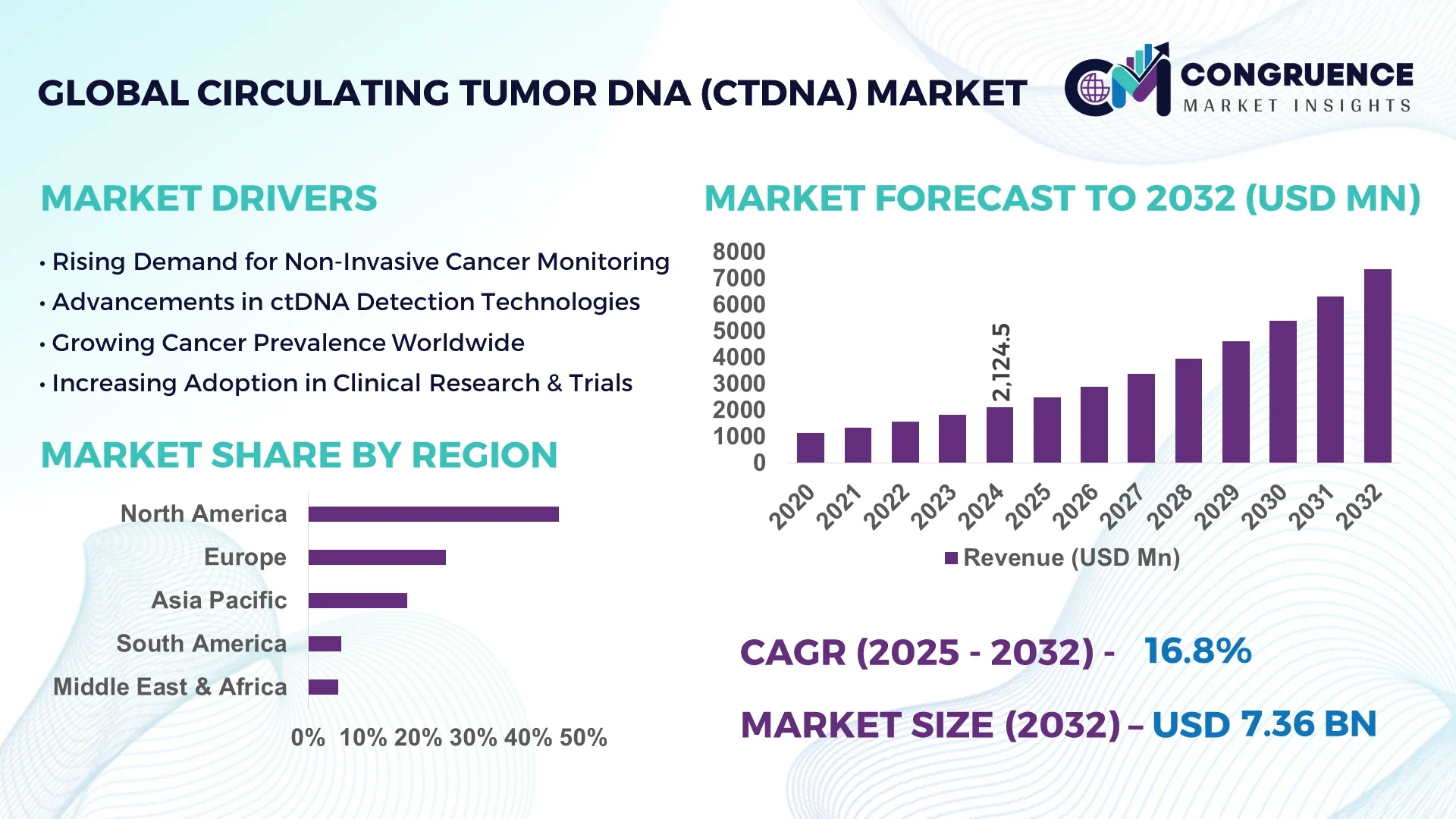

The Global Circulating Tumor DNA (ctDNA) Market was valued at USD 2,124.5 Million in 2024 and is anticipated to reach a value of USD 7,358.7 Million by 2032, expanding at a CAGR of 16.8% between 2025 and 2032.

The United States leads the global ctDNA market, driven by its advanced healthcare infrastructure, substantial investments in cancer research, and a robust regulatory framework that supports the adoption of innovative diagnostic technologies.

The ctDNA market is experiencing significant growth, influenced by factors such as the increasing prevalence of cancer, advancements in non-invasive diagnostic technologies, and the rising demand for personalized medicine. Key industry sectors contributing to this growth include oncology diagnostics, where ctDNA is utilized for early cancer detection, monitoring treatment responses, and detecting minimal residual disease. Technological innovations, particularly in next-generation sequencing (NGS) and digital PCR platforms, have enhanced the sensitivity and accuracy of ctDNA assays. Regulatory support, such as FDA approvals for ctDNA-based companion diagnostics, has further propelled market expansion. Regional consumption patterns indicate a strong demand in North America and Europe, with emerging markets in Asia-Pacific showing promising growth due to increasing healthcare investments and awareness. The future outlook for the ctDNA market remains positive, with ongoing research and development efforts aimed at expanding the clinical applications of ctDNA testing.

How is AI Transforming Circulating Tumor DNA (ctDNA) Market?

Artificial Intelligence (AI) is revolutionizing the Circulating Tumor DNA (ctDNA) Market by enhancing the efficiency and accuracy of ctDNA analysis. AI algorithms are employed to analyze complex genomic data, enabling the identification of novel biomarkers and the prediction of treatment responses. These advancements facilitate the development of personalized treatment plans, improving patient outcomes. AI-driven platforms also streamline data processing workflows, reducing the time required for ctDNA assay results and allowing for real-time monitoring of disease progression. The integration of AI with ctDNA testing is expected to lead to more precise and timely interventions in cancer treatment, thereby transforming clinical practices and patient management strategies.

"In 2024, an AI-based platform was introduced that analyzes ctDNA sequencing data to predict tumor evolution, aiding in the early detection of resistance mutations."

Circulating Tumor DNA (ctDNA) Market Dynamics

The Circulating Tumor DNA (ctDNA) Market is influenced by several dynamic factors that shape its growth trajectory. Technological advancements in sequencing technologies and bioinformatics tools have significantly improved the sensitivity and specificity of ctDNA assays. Regulatory approvals for ctDNA-based diagnostic tests have facilitated their integration into clinical practice, expanding their applications in oncology. Economic factors, such as healthcare expenditure and reimbursement policies, impact the accessibility and adoption of ctDNA testing. Additionally, the increasing demand for personalized medicine and non-invasive diagnostic methods is driving the market's expansion. These dynamics collectively contribute to the evolving landscape of the ctDNA market, presenting opportunities and challenges for stakeholders across the healthcare sector.

DRIVER:

Advancements in Sequencing Technologies

The continuous improvement in sequencing technologies, such as next-generation sequencing (NGS) and digital PCR, has significantly enhanced the detection capabilities of ctDNA assays. These advancements allow for the identification of low-frequency mutations and the monitoring of tumor heterogeneity, thereby providing more comprehensive insights into cancer biology. As a result, clinicians can make more informed decisions regarding treatment strategies, leading to improved patient outcomes.

RESTRAINT:

High Cost of ctDNA Testing

The high cost associated with ctDNA testing remains a significant barrier to its widespread adoption, particularly in low-resource settings. The expenses related to advanced sequencing technologies, specialized reagents, and bioinformatics analysis contribute to the overall cost of ctDNA assays. This financial constraint limits access to ctDNA testing for certain patient populations, hindering its potential impact on global cancer care.

OPPORTUNITY:

Expansion of ctDNA Applications

The expanding applications of ctDNA testing present significant opportunities for market growth. Beyond its established role in detecting minimal residual disease, ctDNA is increasingly being explored for applications in early cancer detection, monitoring treatment responses, and assessing tumor evolution. The development of novel ctDNA-based assays and the integration of AI-driven analytics further enhance the potential of ctDNA testing in personalized medicine.

CHALLENGE:

Regulatory Hurdles

Navigating the regulatory landscape for ctDNA-based diagnostic tests poses challenges for developers and manufacturers. The need for rigorous validation studies, adherence to regulatory standards, and obtaining necessary approvals can delay the introduction of new ctDNA assays into the market. These regulatory hurdles can impede innovation and affect the timely availability of advanced ctDNA testing solutions.

Circulating Tumor DNA (ctDNA) Market Latest Trends

-

Integration of AI in ctDNA Analysis: The incorporation of artificial intelligence into ctDNA analysis platforms is enhancing the precision and efficiency of genomic data interpretation, leading to more accurate and timely cancer diagnostics.

-

Development of Liquid Biopsy Panels: The creation of comprehensive liquid biopsy panels that analyze multiple biomarkers simultaneously is improving the sensitivity and specificity of ctDNA testing, facilitating early detection and monitoring of various cancer types.

-

Expansion of ctDNA Applications: The exploration of ctDNA testing in diverse clinical scenarios, including early cancer detection, treatment monitoring, and assessment of minimal residual disease, is broadening its utility in oncology.

-

Advancements in Sequencing Technologies: Ongoing improvements in sequencing technologies, such as next-generation sequencing and digital PCR, are enhancing the detection capabilities of ctDNA assays, enabling the identification of low-frequency mutations and tumor heterogeneity.

Segmentation Analysis

The Circulating Tumor DNA (ctDNA) Market is systematically segmented into types, applications, and end-users, each reflecting distinct facets of its expansive growth. These segments collectively underscore the market's adaptability and the increasing preference for non-invasive diagnostic methodologies.

By Type

The ctDNA market encompasses various types, including instruments, reagents, and software platforms. Instruments dominate the market, accounting for a significant share. These tools are essential for collecting and analyzing ctDNA samples, such as blood, to detect biomarkers like ctDNA. Reagents, which include kits and consumables, play a crucial role in the preparation and processing of samples, ensuring accurate results. Software platforms are increasingly integrated to facilitate data analysis, enhancing the efficiency and precision of ctDNA procedures.

By Application

The applications of ctDNA span several areas, including early cancer detection, treatment monitoring, and minimal residual disease detection. Early cancer detection is the leading application, as ctDNA offers a non-invasive alternative to traditional tissue biopsies, enabling earlier diagnosis and intervention. Treatment monitoring is another significant application, allowing clinicians to assess the effectiveness of therapies in real-time and make necessary adjustments. Minimal residual disease detection is gaining traction, as it helps in identifying small amounts of cancer cells that may lead to relapse, thereby guiding post-treatment strategies.

By End-User

End-users of ctDNA services include hospitals and laboratories, academic and research centers, and specialty clinics. Hospitals and laboratories are the primary end-users, accounting for a substantial share of the market. These institutions are equipped with the necessary infrastructure and expertise to perform ctDNA tests, making them central to the diagnostic process. Academic and research centers play a pivotal role in advancing ctDNA technologies through research and development, contributing to the evolution of the field. Specialty clinics, focusing on specific medical areas, are increasingly adopting ctDNA techniques to offer personalized care to patients.

Circulating Tumor DNA (ctDNA) Market Report Summary

| Report Attribute/Metric |

Report Details |

|

Market Revenue in 2024

|

USD 2124.5 Million

|

|

Market Revenue in 2032

|

USD 7358.7 Million

|

|

CAGR (2025 - 2032)

|

16.8%

|

|

Base Year

|

2024

|

|

Forecast Period

|

2025 - 2032

|

|

Historic Period

|

2020 - 2024

|

|

Segments Covered

|

By Type

By Application

By End-User

|

|

Key Report Deliverable

|

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape

|

|

Region Covered

|

North America, Europe, Asia-Pacific, South America, Middle East, Africa

|

|

Key Players Analyzed

|

Guardant Health, Roche Diagnostics, Thermo Fisher Scientific, Illumina, QIAGEN, Foundation Medicine, Bio-Rad Laboratories, Agilent Technologies, Sysmex Corporation, Natera

|

|

Customization & Pricing

|

Available on Request (10% Customization is Free)

|