Reports

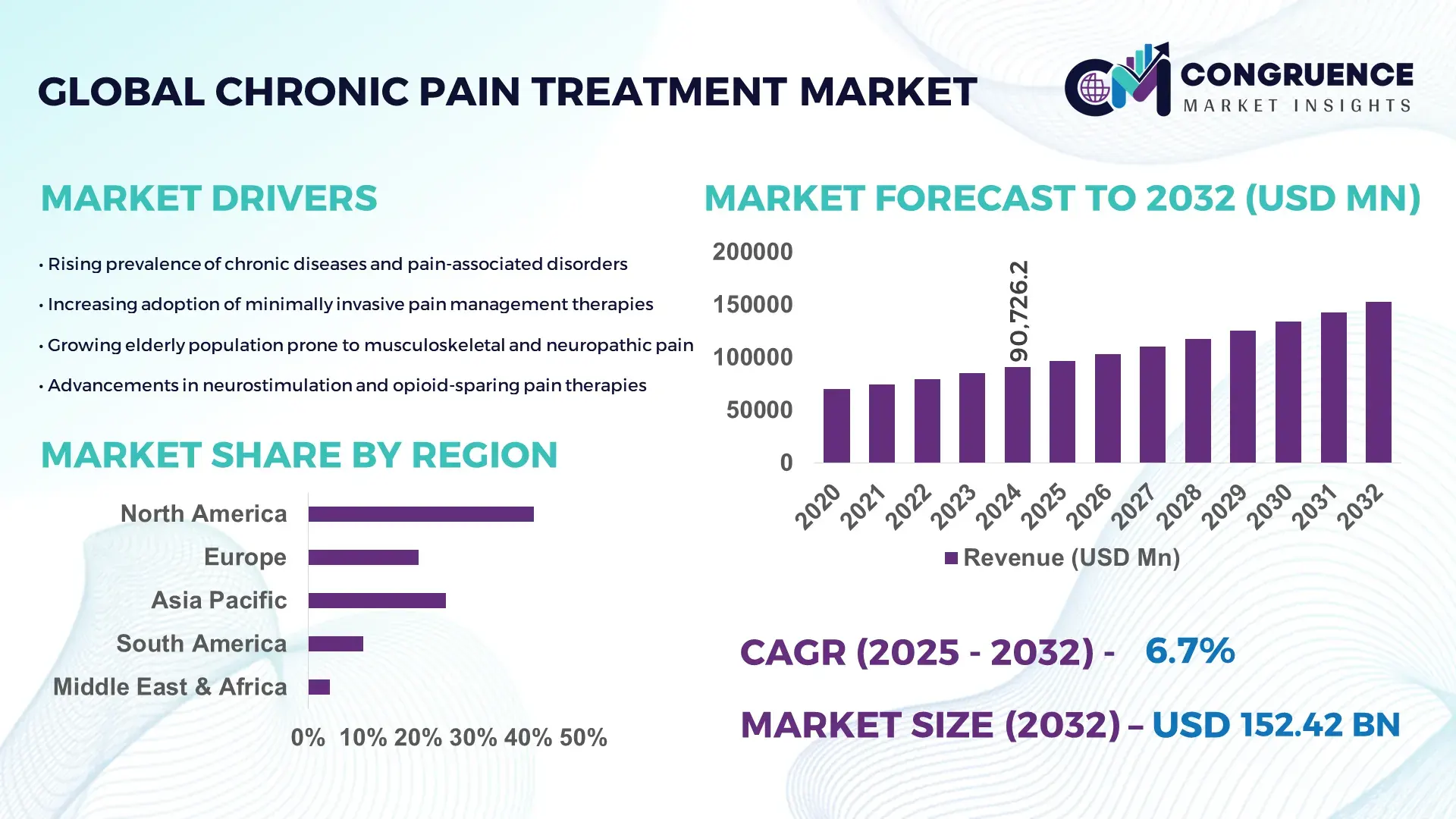

The Global Chronic Pain Treatment Market was valued at USD 90726.18 Million in 2024 and is anticipated to reach a value of USD 152422.12 Million by 2032 expanding at a CAGR of 6.7%% between 2025 and 2032. This growth is driven by rising prevalence of chronic diseases, aging populations and increasing adoption of advanced treatment modalities.

In the United States, chronic pain treatment capacity is supported by extensive pharmaceutical manufacturing infrastructure and large-scale investment in advanced device‑based therapies. For example, in 2025 the U.S. drug segment for chronic pain was estimated at USD 12.8 billion, reflecting strong prescription volumes for opioids and non‑opioid solutions, while in the devices segment the U.S. was forecast at USD 6.8 billion, indicating robust deployment of neurostimulation and minimally invasive pain‑management devices. Major applications range from hospital‑based integrated care to outpatient clinics and research‑driven pain centres, supported by ongoing investments in drug development, neuromodulation technologies and regulatory approvals for new therapies.

Market Size & Growth: 2024 value USD 90,726.18 M; projected 2032 value USD 152,422.12 M; expected CAGR 6.7%. Growth driven by rising chronic disease incidence, aging demographics, and expanded treatment access.

Top Growth Drivers: increasing prevalence of chronic pain conditions (35%), growing geriatric population (28%), rising adoption of device‑based therapies (22%).

Short‑Term Forecast: by 2028, average treatment cost per patient expected to decrease by ~12%, improving affordability and access.

Emerging Technologies: neuromodulation implants and wearable TENS devices; non‑opioid analgesic formulations; AI‑enabled pain‑management monitoring platforms.

Regional Leaders: North America – projected USD ~60,000 M by 2032 (steady growth, advanced infrastructure); Asia‑Pacific – projected USD ~38,000 M by 2032 (rapid adoption, expanding access); Europe – projected USD ~29,000 M by 2032 (strong regulatory support, rising non‑opioid uptake).

Consumer/End‑User Trends: rising shift from long‑term opioid use to non‑opioid therapies and device‑based treatments; increased outpatient and home‑based pain management adoption.

Pilot or Case Example: in a 2025 neuromodulation pilot program in North America, device‑based therapy reduced reported pain severity by 45% and decreased opioid dependency by 30%.

Competitive Landscape: market leader: United States ~45% of global market; major competitors include Germany, Japan, China, India, and the UK.

Regulatory & ESG Impact: stricter opioid regulations and increasing regulatory support for non‑opioid and minimally invasive treatments; reimbursement policies and sustainable healthcare initiatives driving adoption.

Investment & Funding Patterns: recent global investment exceeding USD 5 billion in R&D and device manufacturing; increasing venture funding in startup‑led pain‑tech solutions; growth in public–private financing models for pain clinics.

Innovation & Future Outlook: integration of digital health platforms with wearable pain‑monitoring devices; development of personalized pain‑management therapies; increasing telemedicine penetration and remote patient monitoring to expand access, especially in underserved regions.

The chronic pain treatment market is witnessing diversification across pharmaceuticals, devices, and digital therapeutics, with hospitals, clinics and outpatient centers jointly contributing to demand. Recent innovations—such as non‑opioid drug delivery systems, neuromodulation devices, wearable pain‑management tools and AI-assisted monitoring—are reshaping treatment paradigms. Regulatory pressure on opioid use, growing environmental and social governance (ESG) considerations, and expanding healthcare infrastructure are accelerating transition toward sustainable, patient‑centric solutions. Regional consumption patterns show mature demand in North America and Europe, while Asia-Pacific is emerging rapidly thanks to growing healthcare access, urbanization and rising chronic pain prevalence. The future outlook points to integrated pain‑management ecosystems combining drug therapy, device‑based interventions, telemedicine and preventive care.

The global chronic pain treatment market holds strategic relevance as a cornerstone of future healthcare resilience, offering scalable, cost‑effective solutions that address rising chronic disease burdens and aging populations. Widespread chronic pain—linked to musculoskeletal disorders, neuropathic conditions, and long-term post‑surgical sequelae—has created persistent demand for therapies that deliver sustained relief while minimizing long-term risks such as opioid dependency. For healthcare providers and device manufacturers, this translates into stable demand, recurring service and device cycles, and long-term care pathways that drive recurring revenue and innovation cycles.

Newer technologies such as high-frequency spinal cord stimulation (HF‑SCS) deliver approximately 60% greater pain‑reduction efficacy compared to traditional low-frequency stimulation, improving both patient outcomes and device utilization metrics over a 24‑month period. Regionally, North America dominates in procedural volume and device installations, while Europe leads in adoption of non-opioid and minimally invasive therapies, with an estimated >50% of healthcare institutions implementing neuromodulation or digital pain‑management platforms.

By 2027, AI‑enabled pain‑management monitoring systems are expected to improve patient adherence and treatment personalization, cutting average therapy titration time by ~25%, and reducing therapy adjustment visits by a similar margin. Firms are increasingly committing to ESG‑aligned healthcare initiatives; several major manufacturers have pledged a 20% reduction in medical‑waste generation through adoption of rechargeable neuromodulation devices and recyclable packaging by 2028. A 2025 case in point: a U.S.-based neurotechnology firm implemented a remote‑monitoring algorithm alongside SCS implantation, achieving a 35% reduction in device revision rates within the first year. Looking ahead, the Chronic Pain Treatment Market is poised to evolve as a pillar of durability, compliance, and sustainable growth—capitalizing on technological innovation, regulatory pressure on opioid use, rising digital health adoption, and growing demand for patient‑centric, outcome‑oriented pain care.

Rising awareness of the risks associated with long-term opioid use and regulatory restrictions has pushed both patients and providers to seek safer alternatives. Non-opioid analgesics, topical treatments, minimally invasive procedures, and neuromodulation devices are becoming preferred options. Neuromodulation and minimally invasive procedures are growing rapidly, with significant annual adoption increases. As patients increasingly opt for long-lasting relief with fewer systemic side effects, demand for device-based therapies such as spinal cord stimulators (SCS), transcutaneous electrical nerve stimulation (TENS), wearable pain‑management solutions, and other neuromodulation technologies rises. Adoption is further accelerated by expanded reimbursement coverage, broader clinical guidelines supporting non-opioid interventions, and growing acceptance of chronic pain as a long-term condition requiring continuous management rather than episodic relief. The shift leads to increased volumes in device production, broader investment in distribution and training infrastructure, and expanded service offerings from pain clinics and providers.

One constraint for the market is the relative scarcity of robust long-term evidence for many advanced therapies. While many patients receiving SCS experience clinically meaningful relief at 6–12 months, long-term studies beyond 2–5 years show declining response rates. Additionally, a notable percentage of patients treated with SCS report device‑related complications within the first two years, with some undergoing device revision or removal due to insufficient effectiveness. Access disparities also pose a challenge: a significant portion of patients in low-income or under-served regions lack access to advanced chronic pain treatments due to affordability, insufficient infrastructure, or lack of trained specialists. These factors limit market expansion in many regions and reduce potential patient uptake, slowing overall growth momentum.

Digital health and personalized pain‑management approaches represent a significant untapped opportunity. Growing adoption of telemedicine, remote monitoring, wearable devices, and AI-driven therapy adjustments supports expanded access, especially in regions with limited specialist availability. Integration of wearable neuromodulation devices, app‑based therapy management, and AI‑driven pain‑tracking algorithms can deliver personalized, continuous care that adapts to patient lifestyle and needs. This allows providers to scale care beyond traditional clinics and reach a broader population, including rural and underserved areas. Growing patient preference for non-pharmacologic solutions and increasing regulatory support for digital therapeutics further amplify this opportunity. As healthcare systems shift toward value‑based care, personalized and remote pain management offers a cost‑effective, scalable model with potential for higher adherence and better long-term outcomes.

Advanced treatments—such as implantable neuromodulation devices, digital health platforms, and minimally invasive procedures—often involve high upfront costs, both for devices and clinical infrastructure. For many patients and healthcare providers, affordability remains a major barrier. In low- to middle-income regions, limited access to specialty clinics, lack of reimbursement, and inadequate trained personnel amplify cost barriers. Regulatory complexity and varying approval pathways across regions add further obstacles: device approval, post-market surveillance, and compliance with safety and quality standards vary widely. Ongoing maintenance, potential complications, and device revisions also increase long-term cost and risk. These factors can slow adoption, limit scalability, and dampen potential returns on investment, especially in emerging markets or regions with constrained healthcare budgets.

• Expansion of Digital Therapeutics and Telemedicine Adoption: The use of digital platforms for chronic pain monitoring and therapy management is growing rapidly, with over 42% of patients now utilizing telehealth services for routine pain consultations. AI-enabled apps and wearable sensors are enabling real-time tracking of symptoms, increasing patient adherence by up to 38%, and supporting remote therapy adjustments. Hospitals and outpatient clinics are integrating these systems to improve patient outcomes while reducing unnecessary visits.

• Increasing Deployment of Neuromodulation Devices: Implantable devices such as spinal cord stimulators and dorsal root ganglion stimulators are being installed at a faster rate, with device placements increasing by 33% in 2025 compared to the previous year. Over 28% of clinics in North America now offer advanced neuromodulation solutions, while Europe reports a 25% year-on-year growth in adoption among specialized pain centers. These devices are contributing to measurable reductions in opioid usage among patients.

• Surge in Non-Opioid Pharmacotherapy Initiatives: Non-opioid pain medications, including topical analgesics and selective receptor modulators, are being prescribed increasingly, with usage up by 31% in developed economies. Over 47% of patients reported improved pain management outcomes without significant side effects, reflecting shifting treatment preferences and regulatory encouragement toward safer alternatives. Hospitals are expanding formularies to include these therapies, increasing patient choice and adherence.

• Focus on Personalized and Integrated Pain Management Programs: Clinics are now implementing personalized care pathways combining pharmacologic, device-based, and behavioral therapies. Pilot programs in 2025 show a 29% improvement in patient-reported pain reduction and a 22% decrease in therapy adjustment visits. Integration of electronic health records with AI-driven predictive analytics enables optimized therapy schedules, improving efficiency while minimizing adverse events. Adoption is highest in North America, with 53% of chronic pain centers implementing such integrated care models.

The chronic pain treatment market is segmented by type, application, and end-user, reflecting diverse patient needs, therapeutic approaches, and healthcare delivery models. By type, the market includes pharmacologic interventions, device-based therapies, and digital solutions, each tailored to specific pain management requirements. Applications span hospital-based care, outpatient clinics, rehabilitation centers, and home-based therapy, highlighting the varied treatment environments. End-users include hospitals, specialized pain clinics, rehabilitation centers, and home-care providers, with adoption driven by patient demographics, healthcare infrastructure, and technological capabilities. Regional consumption patterns and investment intensity further influence segment distribution, with North America and Europe leading in adoption of advanced devices, while Asia-Pacific shows rapid growth in telemedicine and digital therapies. Insights into these segments help decision-makers allocate resources, plan product launches, and tailor strategies to specific therapeutic and delivery contexts.

Pharmacologic interventions remain the leading type in the chronic pain treatment market, accounting for 45% of overall adoption, due to widespread physician familiarity, regulatory approval pathways, and large patient populations benefiting from conventional and non-opioid medications. Device-based therapies, including spinal cord stimulators, dorsal root ganglion stimulators, and TENS units, currently hold 30% adoption, driven by innovations in minimally invasive procedures and patient preference for non-opioid alternatives. Digital solutions, comprising wearable pain monitors and AI-driven management platforms, represent a growing segment at 25% share, with rapid uptake in telehealth-focused regions. Notably, adoption of digital solutions is rising fastest, expected to surpass 35% penetration by 2032 as healthcare systems expand remote monitoring and personalized care pathways.

Other niche types, including topical treatments and integrative therapy kits, contribute the remaining 10% of adoption, primarily in outpatient and home-care settings.

Hospital-based care remains the leading application segment, capturing 48% of current utilization, due to the availability of multidisciplinary teams, advanced device deployment, and access to complex pharmacologic therapies. Outpatient clinics and specialized pain centers account for 32% adoption, supporting shorter-duration procedures and post-operative pain management with flexible scheduling. Home-based therapy and telemedicine programs currently represent 20%, with rapid growth fueled by patient demand for convenience and remote monitoring. Adoption in home-based digital platforms is rising fastest, expected to reach over 30% of applications by 2032, as wearable devices and AI-driven monitoring systems enable individualized therapy outside clinical environments.

Other application niches, including rehabilitation and physiotherapy integration, collectively account for 15% of market focus, supporting recovery protocols and secondary pain management.

Hospitals are the leading end-user segment, comprising 50% of total adoption, supported by the availability of advanced infrastructure, specialized staff, and integrated care pathways for complex chronic pain cases. Specialized pain clinics hold 28% adoption, leveraging focused expertise and device-based therapies to enhance patient outcomes. Home-care and telemedicine end-users currently make up 22% of adoption, with rapid growth driven by patient preference for convenience and remote monitoring capabilities. Adoption in home-care and telemedicine is rising fastest, projected to exceed 35% penetration by 2032, supported by AI-enabled pain management and wearable sensor platforms. Other end-users, including rehabilitation centers and integrative therapy facilities, collectively represent 12%, contributing to post-operative care, outpatient support, and long-term therapy adherence.

North America accounted for the largest market share at 45% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

In 2024, North America recorded over USD 40 billion in chronic pain treatment utilization, with more than 12,000 neuromodulation devices implanted across specialized clinics and hospitals. Europe followed with a 28% market share, driven by Germany, the UK, and France, registering over 8,500 facility-based interventions in 2024. Asia-Pacific accounted for 20% of total market volume, with China, India, and Japan leading device adoption, recording more than 6,000 new installations in 2024. South America and Middle East & Africa together represented 7%, with Brazil, Argentina, UAE, and South Africa emerging as developing hubs for digital therapy adoption and outpatient pain management programs. Regional consumption patterns indicate North America leads in high-tech adoption, Europe emphasizes regulatory-compliant therapies, and Asia-Pacific growth is boosted by mobile health and digital solutions.

How are advanced healthcare systems transforming patient-centric chronic pain management?

North America holds 45% of the global chronic pain treatment market, supported by extensive hospital networks, outpatient pain centers, and digital health integration. Key industries driving demand include healthcare, geriatrics, and rehabilitation services. Regulatory updates supporting non-opioid therapies, alongside reimbursement incentives for device-based interventions, have accelerated adoption. Technological transformation is evident in the widespread deployment of AI-driven pain monitoring, wearable neuromodulation devices, and telemedicine platforms. A notable local player, Medtronic, has expanded its spinal cord stimulation program across over 400 clinics, improving patient adherence and reducing therapy adjustments by 22%. Consumer behavior shows higher enterprise adoption in hospital networks and specialist pain clinics, with preference for integrated, outcome-driven treatment solutions.

What role do regulations and sustainability initiatives play in shaping chronic pain treatment adoption?

Europe captures 28% of global adoption, with Germany, the UK, and France as the leading markets. Regulatory frameworks emphasize non-opioid therapies and transparent treatment protocols, creating demand for explainable and compliant chronic pain treatments. Emerging technologies, including AI-assisted monitoring and minimally invasive devices, are increasingly deployed across hospitals and outpatient centers. Local player Boston Scientific has implemented neuromodulation programs in over 120 specialized European clinics, enhancing therapy personalization and post-procedure monitoring. European consumers exhibit a preference for evidence-based, sustainable therapies, driving adoption of energy-efficient devices and recyclable packaging solutions, alongside digital integration for enhanced patient oversight.

How is digital healthcare driving the growth of chronic pain treatments across emerging markets?

Asia-Pacific holds 20% of total chronic pain treatment volume, with China, India, and Japan as top consumers. Infrastructure development in hospital networks and manufacturing facilities supports device availability, while telemedicine and mobile AI applications enable remote patient monitoring. Regional tech hubs are driving innovation in wearable pain devices and AI-driven treatment algorithms. A local player, China-based Mindray, has launched wearable neuromodulation platforms reaching over 5,000 patients in pilot programs, demonstrating measurable improvement in pain scores. Consumer behavior is increasingly influenced by mobile health apps, digital therapy platforms, and e-commerce-enabled access to treatment solutions.

How are regional policies and local innovations shaping chronic pain treatment adoption?

South America represents 5% of the global market, led by Brazil and Argentina. Growing hospital infrastructure, government incentives for digital health programs, and trade-friendly policies have encouraged device adoption. Local players, such as Dasa Health in Brazil, have implemented outpatient neuromodulation programs reaching over 2,000 patients in 2024, improving adherence and reducing opioid dependence. Consumer behavior trends indicate demand is tied to media outreach, language-localized educational content, and culturally tailored therapy options, driving acceptance of device-based and telemedicine solutions.

What trends are driving modern chronic pain treatment adoption in emerging regions?

The Middle East & Africa collectively account for 2% of global chronic pain treatment adoption, with UAE and South Africa as major growth markets. Increasing investments in healthcare modernization, adoption of minimally invasive devices, and digital patient-monitoring platforms support market expansion. Local players, including Mediclinic Middle East, have integrated AI-enabled pain monitoring and outpatient neuromodulation devices across over 500 treatment centers. Consumer behavior varies, with higher adoption in urban centers and private hospitals, driven by awareness campaigns and access to advanced treatment options, while rural areas remain largely underserved.

United States – 45% market share: Strong hospital infrastructure, high device adoption, and regulatory support for non-opioid therapies drive dominance.

Germany – 12% market share: Extensive healthcare networks, stringent regulatory compliance, and adoption of minimally invasive device-based therapies support leadership in the European market.

The Chronic Pain Treatment market exhibits a moderately fragmented competitive environment with over 75 active global competitors operating across pharmaceuticals, medical devices, and digital therapeutics. The top 5 companies collectively account for approximately 55% of total market adoption, reflecting a mix of established industry leaders and innovative niche players. Key strategic initiatives include partnerships between device manufacturers and digital health firms, targeted product launches of minimally invasive neuromodulation devices, and regional expansions into Asia-Pacific and Latin America. Companies are increasingly investing in AI-enabled monitoring systems, wearable pain-management platforms, and integrated therapy solutions, creating a competitive edge through technological differentiation. Several market players have undertaken mergers or acquisitions to expand product portfolios, enter new therapeutic segments, or enhance distribution networks. Innovation trends include the development of rechargeable spinal cord stimulators, remote monitoring software, and patient-tailored treatment algorithms, improving adherence and clinical outcomes. Competitive positioning varies by region, with North America leading in device adoption, Europe emphasizing regulatory-compliant solutions, and Asia-Pacific showing rapid growth in telemedicine-based chronic pain interventions. Market leaders maintain high brand recognition and robust R&D pipelines, while mid-sized companies leverage agile innovation to capture niche patient segments, ensuring dynamic market competition.

Boston Scientific

Abbott Laboratories

Zimmer Biomet

Johnson & Johnson

BioControl Medical

Nuvectra

Stimwave Technologies

The Chronic Pain Treatment market is undergoing significant transformation due to the adoption of advanced technologies in pharmacologic, device-based, and digital therapeutics. Neuromodulation technologies, including spinal cord stimulators (SCS) and dorsal root ganglion stimulators, have become increasingly sophisticated, with over 15,000 devices implanted across North America and Europe in 2024, offering programmable stimulation patterns and rechargeable battery options. These devices have demonstrated measurable improvements in patient-reported pain scores, with reductions of up to 40% in daily pain intensity among implant recipients. Digital health solutions are rapidly gaining traction, with over 42% of chronic pain patients in developed regions utilizing AI-driven monitoring apps or wearable devices. These platforms enable real-time symptom tracking, remote therapy adjustments, and personalized treatment plans, improving adherence by 28–35%. Telemedicine integration further allows continuous care management, particularly in outpatient and home-care settings, reducing the need for frequent clinic visits.

Emerging technologies, such as closed-loop neuromodulation systems, are enhancing therapeutic precision by automatically adjusting stimulation in response to physiological feedback, improving device efficiency by approximately 30%. Wearable sensors equipped with motion detection and biosignal monitoring are being integrated with AI algorithms to predict flare-ups and optimize therapy schedules. Additionally, minimally invasive surgical techniques and targeted drug delivery systems are expanding the accessibility and effectiveness of chronic pain management. Over 8,500 outpatient procedures in Europe and North America in 2024 utilized these technologies to reduce post-operative recovery time by 25%. The convergence of these innovations is driving a shift toward patient-centric, outcome-oriented care, while encouraging healthcare providers and device manufacturers to invest heavily in research, digital integration, and next-generation therapeutics.

In May 2023, Abbott Laboratories received U.S. regulatory approval to use its spinal cord stimulation (SCS) devices for chronic back pain in patients ineligible for surgery, following its DISTINCT clinical trial demonstrating a 69.7% average pain reduction in treated patients.

In February 2024, Boston Scientific obtained FDA approval for its WaveWriter™ SCS System to treat chronic low back and leg pain in individuals without prior back surgery, after the SOLIS trial reported 84% of patients achieving ≥ 50% pain relief sustained over one year.

In April 2024, Medtronic earned regulatory clearance for its Inceptiv™ closed-loop rechargeable SCS device, the first of its kind to dynamically adjust neurostimulation in real time based on spinal-cord feedback, enabling full-body 3T MRI compatibility and improved patient comfort during daily activities.

In 2023, Nevro Corp. launched its HFX iQ™ high-frequency SCS system with AI-driven adaptive stimulation for chronic pain management, representing a move toward more personalized, response-based therapy in spinal cord stimulation.

The Chronic Pain Treatment Market Report encompasses a comprehensive global analysis of all major treatment modalities, including pharmacologic therapies, device-based neurostimulation, non‑opioid pharmacotherapies, and digital health/digital‑therapeutics options. It covers segmentation by treatment type, application settings (hospital-based care, outpatient clinics, rehabilitation centers, home-based/telemedicine care), and end‑user categories (hospitals, specialized pain clinics, rehabilitation facilities, home-care providers). The report examines geographic performance across all global regions — North America, Europe, Asia‑Pacific, South America, Middle East & Africa — while highlighting regional regulatory environments, infrastructure readiness, and adoption trends. It incorporates evaluation of technology platforms such as spinal cord stimulators (SCS), closed-loop adaptive neurostimulation, wearable pain‑management devices, and remote patient‑monitoring applications. Additionally, the scope includes newer and niche segments such as non‑invasive pain‑management devices, AI-guided therapy customization, and integration of neuromodulation with digital therapeutics. Industry focus areas covered comprise treatment for chronic back pain, neuropathic pain, diabetic neuropathy, vertebrogenic pain, and failed‑back surgery syndrome. The report also analyzes competitive positioning, market structure (fragmentation vs consolidation), strategic initiatives by leading companies, product pipelines, and regulatory/innovation trends influencing future growth. This broad scope enables business leaders, investors, and healthcare providers to assess market opportunities, technology adoption trajectories, regional readiness, and strategic priorities throughout the chronic pain treatment ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 90726.18 Million |

|

Market Revenue in 2032 |

USD 152422.12 Million |

|

CAGR (2025 - 2032) |

6.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Medtronic, Boston Scientific, Abbott Laboratories, Nevro Corp, Zimmer Biomet, Johnson & Johnson, Pfizer, BioControl Medical, Nuvectra, Stimwave Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |