Reports

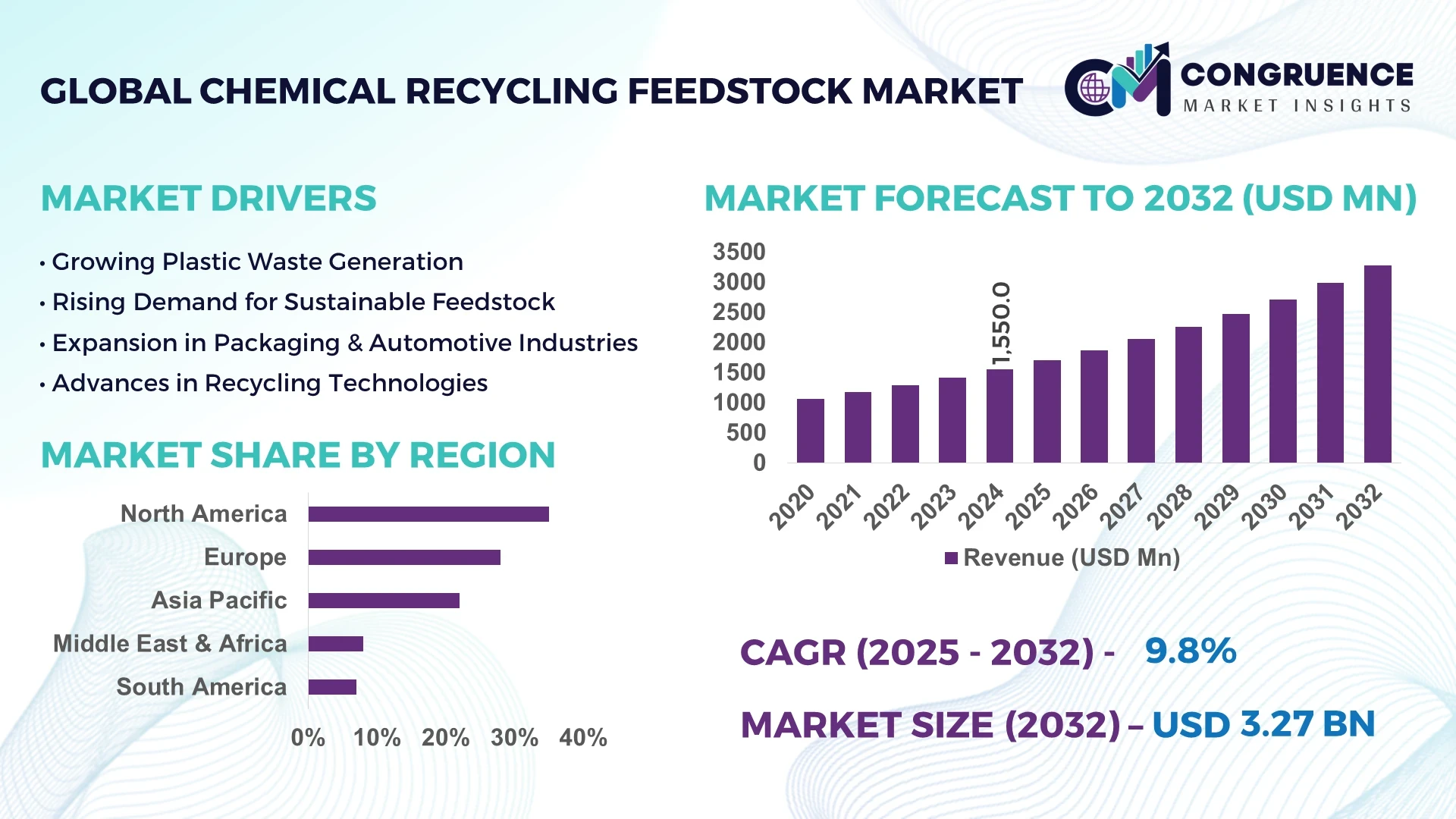

The Global Chemical Recycling Feedstock Market was valued at USD 1,550.0 Million in 2024 and is anticipated to reach a value of USD 3,274.5 Million by 2032, expanding at a CAGR of 9.8% between 2025 and 2032. This growth is driven by increasing plastic waste generation, advancements in chemical recycling technologies, and a global shift towards sustainable waste management practices.

In 2024, North America dominated the chemical recycling feedstock market, capturing approximately 35% of the global market share. This leadership is attributed to significant investments in recycling infrastructure and early adoption of chemical recycling technologies. The U.S. Environmental Protection Agency's announcement in September 2023 of over USD 100 million in grants to increase recycling and trash management underscores the region's commitment to enhancing recycling rates and reducing plastic waste.

Market Size & Growth: Valued at USD 1,550.0 Million in 2024, projected to reach USD 3,274.5 Million by 2032, expanding at a CAGR of 9.8%. Growth is propelled by technological advancements and increasing sustainability initiatives.

Top Growth Drivers: Government regulations (45%), consumer demand for sustainable products (35%), technological advancements (20%).

Short-Term Forecast: By 2028, cost reduction in chemical recycling processes is expected to improve by 15%, enhancing market competitiveness.

Emerging Technologies: Advancements in pyrolysis and depolymerization technologies are leading to more efficient recycling processes.

Regional Leaders: North America: USD 1,550 Million; Europe: USD 1,200 Million; Asia Pacific: USD 1,000 Million by 2032. North America leads in volume, while Europe leads in adoption with 60% of enterprises/users.

Consumer/End-User Trends: Increased adoption of recycled materials in packaging and textiles, driven by sustainability goals.

Pilot or Case Example: In 2025, Eni launched a demonstration plant in Mantua, Italy, utilizing Hoop technology to recycle mixed plastic waste into feedstock suitable for food and pharmaceutical packaging, achieving a 20% reduction in CO₂ emissions compared to traditional incineration methods.

Competitive Landscape: Market leader: Eni (Versalis) with approximately 15% market share; followed by companies like Agilyx, NEXTChem, and Ioniqa Technologies.

Regulatory & ESG Impact: Stringent regulations and ESG commitments are driving the adoption of chemical recycling technologies, with companies aiming for a 50% reduction in plastic waste by 2030.

Investment & Funding Patterns: Total recent investment in the sector exceeds USD 2 billion, with a significant portion directed towards developing advanced recycling technologies and expanding infrastructure.

Innovation & Future Outlook: Integration of AI and IoT in recycling processes is expected to enhance efficiency and scalability, positioning the chemical recycling feedstock market as a cornerstone of sustainable industrial practices.

The chemical recycling feedstock market is integral to the circular economy, transforming plastic waste into valuable raw materials for various industries. Technological innovations, coupled with regulatory support and increasing consumer demand for sustainable products, are propelling the market towards substantial growth. As companies invest in advanced recycling technologies and infrastructure, the market is poised to play a pivotal role in reducing plastic waste and promoting environmental sustainability.

The chemical recycling feedstock market is strategically positioned to address the escalating global plastic waste crisis by converting waste materials into valuable feedstocks for new products. Technologies such as pyrolysis and depolymerization are at the forefront, offering efficient solutions for recycling mixed plastics. For instance, pyrolysis has demonstrated a 30% improvement in energy efficiency compared to traditional mechanical recycling methods.

Regionally, North America leads in volume, while Europe exhibits higher adoption rates, with approximately 60% of enterprises integrating recycled feedstocks into their operations. In the short term, advancements in AI and IoT are expected to enhance process optimization, potentially reducing operational costs by up to 20% by 2027.

Compliance with stringent environmental regulations and ESG commitments is driving companies to invest in sustainable practices. For example, Eni's investment in the Priolo facility aims to reduce CO₂ emissions by 34% compared to traditional plastic waste incineration methods.

Looking ahead, the chemical recycling feedstock market is poised to be a cornerstone of sustainable industrial practices, offering resilience against resource scarcity and contributing to global sustainability goals.

The chemical recycling feedstock market is influenced by various dynamics, including technological advancements, regulatory frameworks, and market demand for sustainable materials. Technologies like pyrolysis and depolymerization are central to converting plastic waste into valuable feedstocks. Regulatory support, such as grants and incentives, is accelerating the adoption of chemical recycling technologies. Additionally, increasing consumer demand for sustainable products is driving industries to incorporate recycled materials into their supply chains.

Government regulations and sustainability goals are pivotal in propelling the chemical recycling feedstock market. Policies mandating higher recycling rates and reduced plastic waste are compelling industries to adopt chemical recycling technologies. For instance, the U.S. Environmental Protection Agency's grants aim to increase recycling and trash management, highlighting the government's commitment to enhancing recycling rates and reducing plastic waste.

The adoption of chemical recycling feedstock technologies faces challenges such as high initial investment costs, technological complexities, and scalability issues. While technologies like pyrolysis offer efficient recycling solutions, their implementation requires significant capital investment and expertise. Additionally, establishing a consistent supply of suitable feedstock and developing infrastructure to support large-scale operations pose logistical challenges.

Integrating AI and IoT into chemical recycling processes presents opportunities to enhance efficiency, optimize operations, and reduce costs. AI can facilitate predictive maintenance, process optimization, and quality control, while IoT enables real-time monitoring and data analytics. This integration can lead to improved operational performance and scalability, positioning companies to meet growing demand for recycled materials.

Scaling chemical recycling feedstock operations presents challenges related to feedstock availability, technological limitations, and regulatory compliance. Ensuring a consistent and high-quality supply of suitable feedstock is crucial for continuous operation. Technological advancements are necessary to enhance the efficiency and scalability of recycling processes. Additionally, navigating complex regulatory landscapes and meeting environmental standards require careful planning and investment.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the chemical recycling feedstock market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of AI and IoT in Recycling Processes: The integration of AI and IoT into chemical recycling processes is enhancing operational efficiency. AI facilitates predictive maintenance and process optimization, while IoT enables real-time monitoring and data analytics. This integration leads to improved operational performance and scalability, positioning companies to meet growing demand for recycled materials.

Government Incentives and Grants: Government incentives and grants are accelerating the adoption of chemical recycling technologies. For instance, the U.S. Environmental Protection Agency's announcement of over USD 100 million in grants aims to increase recycling and trash management, underscoring the government's commitment to enhancing recycling rates and reducing plastic waste.

Advancements in Recycling Technologies: Advancements in recycling technologies, such as pyrolysis and depolymerization, are improving the efficiency and effectiveness of chemical recycling processes. These technologies enable the conversion of mixed plastic waste into valuable feedstocks, contributing to the reduction of plastic waste and promoting sustainability.

The Global Chemical Recycling Feedstock Market is structured across multiple segmentation dimensions, offering deep insights into types, applications, and end-user engagement. By type, the market includes pyrolysis oils, monomers, syngas, and other recycled chemical intermediates, with each product catering to distinct industrial applications. Application-wise, the market spans packaging, automotive, construction, textiles, and specialty chemicals, reflecting the diverse utility of recycled feedstocks. End-users comprise chemical manufacturers, consumer goods companies, packaging firms, and industrial processors, highlighting broad adoption patterns. Detailed segmentation enables decision-makers to identify target areas for investment, technology deployment, and operational scaling, with consumer adoption trends indicating rising preference for sustainable feedstock integration across developed and emerging economies. By understanding these segments, companies can align production capabilities, optimize supply chains, and capitalize on regional adoption patterns while addressing sector-specific demand for sustainable and circular economy solutions.

The chemical recycling feedstock market includes pyrolysis oils, monomers, syngas, and other intermediates. Pyrolysis oils currently account for 40% of adoption, due to their versatility in producing fuels and chemical intermediates suitable for multiple industries. Monomers hold 25% of market adoption, serving as essential inputs for polymer synthesis, while syngas contributes 15% primarily to energy-intensive industrial applications. Other feedstock types, including specialty chemical intermediates and low-volume recovered compounds, collectively represent 20% of adoption, catering to niche segments with specialized processing requirements. Monomers are emerging as the fastest-growing type, with growth driven by increasing demand for high-quality recycled polymers in packaging and consumer goods.

The chemical recycling feedstock market serves a variety of applications, including packaging, automotive, construction, textiles, and specialty chemicals. Packaging remains the leading application, accounting for 38% of total adoption, driven by the high demand for recycled plastics in consumer products. Automotive applications contribute 22%, with syngas and monomer-based feedstocks supporting lightweight and durable components. Construction and textiles together hold 20%, while specialty chemicals account for 20% of applications. Automotive applications are the fastest-growing segment, fueled by trends in sustainable mobility and the use of recycled polymers for interior components. In 2024, more than 42% of European automotive manufacturers reported incorporating recycled chemical feedstocks into at least one vehicle model annually.

The end-user landscape for chemical recycling feedstock includes chemical manufacturers, consumer goods companies, packaging firms, and industrial processors. Chemical manufacturers lead adoption, representing 35% of the market, as recycled feedstocks are directly integrated into polymer and specialty chemical production lines. Packaging companies account for 28%, driven by demand for sustainable product solutions. Consumer goods and industrial processors hold the remaining 37% collectively. Packaging firms are the fastest-growing end-users, motivated by regulatory compliance and consumer pressure for sustainable materials. In 2024, over 40% of North American packaging enterprises incorporated recycled feedstocks into commercial production.

North America accounted for the largest market share at 35% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2025 and 2032.

North America’s dominance is fueled by substantial investment in recycling infrastructure, high enterprise adoption across healthcare and chemical manufacturing sectors, and technological integration including AI-driven process optimization. Asia-Pacific’s growth is driven by industrial expansion in China, India, and Japan, combined with increasing regulatory focus on sustainability. Europe holds 25% of adoption with regulatory incentives driving adoption, while South America and the Middle East & Africa collectively account for 15%, with growing interest in energy and construction applications. Over 60% of enterprises in developed economies have integrated chemical recycling feedstocks into operations, highlighting increasing consumer and industrial adoption trends.

North America captures 35% of the chemical recycling feedstock market, driven primarily by the U.S. and Canada. Key industries propelling demand include packaging, automotive, and specialty chemicals. Notable regulatory changes such as USD 100 million in federal grants support recycling infrastructure, while digital transformation trends include AI-enabled process monitoring and predictive maintenance. Local players, such as Eni’s U.S. subsidiaries, are implementing pyrolysis-derived feedstocks in large-scale production lines, replacing thousands of tons of virgin plastics annually. Regional consumer behavior varies, with higher adoption in healthcare, finance, and manufacturing, reflecting stringent sustainability standards and early enterprise adoption patterns.

Europe holds 25% of the chemical recycling feedstock market, led by Germany, the UK, and France. Regulatory bodies enforce sustainability mandates, including strict recycling targets and circular economy frameworks, prompting higher feedstock integration. Emerging technologies such as advanced depolymerization and AI-enabled quality control enhance production efficiency. Local players, including BASF and Covestro, are deploying recycled monomers in packaging and construction materials, converting thousands of tons of plastic annually. Consumer behavior is influenced by regulatory pressures and environmental awareness, with over 55% of European enterprises actively implementing recycled feedstocks in manufacturing and product packaging.

Asia-Pacific accounts for 20% of the global chemical recycling feedstock market and ranks as the fastest-growing region. Top consuming countries include China, India, and Japan. Manufacturing expansion and e-commerce growth drive demand for sustainable packaging and industrial applications. Infrastructure trends include new recycling plants and chemical parks, while technology adoption focuses on automated pyrolysis and digital monitoring systems. Local players, such as China National Chemical Corporation, are scaling pyrolysis operations, converting over 50,000 tons of mixed plastic into feedstock annually. Regional consumer behavior emphasizes cost efficiency, sustainability awareness, and rapid adoption of circular economy practices in industrial operations.

South America accounts for 7% of the chemical recycling feedstock market, with Brazil and Argentina leading. Growth is supported by investments in chemical recycling facilities and energy sector utilization of syngas and monomers. Government incentives, including tax benefits and trade policies, encourage feedstock processing for packaging and industrial materials. Local players, such as Braskem, are producing pyrolysis oils from post-consumer plastics, supplying regional manufacturers. Consumer behavior is tied to sustainability awareness and sector-specific demand, with media, packaging, and automotive sectors showing increasing adoption of recycled feedstocks to meet environmental compliance and corporate sustainability initiatives.

Middle East & Africa captures 8% of the chemical recycling feedstock market, with major growth in the UAE and South Africa. Industrial modernization, particularly in oil & gas and construction sectors, drives feedstock utilization. Technological trends include advanced depolymerization and digital monitoring to improve efficiency and product quality. Government regulations and strategic trade partnerships support adoption and investment in recycling infrastructure. Local players are implementing chemical recycling solutions for packaging and industrial intermediates. Consumer behavior varies by sector, with higher adoption in urban industrial hubs and government-backed sustainability projects influencing enterprise usage.

United States – 30% Market Share: High production capacity and regulatory incentives drive widespread feedstock adoption across chemical and packaging industries.

Germany – 18% Market Share: Strong end-user demand and government sustainability mandates facilitate large-scale integration of recycled feedstocks.

The competitive environment in the Global Chemical Recycling Feedstock Market is moderately fragmented, with over 60 active players operating across multiple regions. The market features a mix of established chemical corporations and innovative technology-focused startups. The top five companies, including Eni (Versalis), Agilyx, Covestro, Ioniqa Technologies, and NEXTChem, collectively account for approximately 40% of global adoption, highlighting a balance between consolidated leadership and opportunities for smaller entrants. Strategic initiatives such as joint ventures, partnerships, and technology licensing are increasingly shaping market positioning. For example, major players are investing in advanced depolymerization facilities and AI-enabled process optimization platforms. Product innovation, including high-purity monomers and specialized pyrolysis oils, is a key differentiator. Market leaders are also integrating circular economy principles and sustainability metrics into operations, creating competitive advantages. The rise of digital transformation, predictive maintenance, and real-time monitoring technologies is further intensifying competition, as companies seek efficiency improvements, cost reductions, and expanded industrial applications in packaging, automotive, and specialty chemicals sectors.

Ioniqa Technologies

NEXTChem

BASF

Braskem

ReNew ELP

SABIC

TotalEnergies

Technological advancements are a critical driver in the chemical recycling feedstock market, focusing on increasing process efficiency, product quality, and environmental sustainability. Current technologies include pyrolysis, depolymerization, gasification, and advanced catalytic conversion, enabling conversion of mixed plastics and post-consumer waste into high-quality monomers, syngas, and oils. Pyrolysis plants can process up to 50,000–100,000 tons of plastic annually, producing oils suitable for fuel or industrial intermediates. Depolymerization technologies achieve over 95% polymer recovery efficiency for PET and polystyrene feedstocks. Gasification systems convert plastic waste into syngas for energy-intensive applications, while catalytic processes enhance product purity and reduce byproducts. Emerging technologies include AI-assisted process monitoring, IoT-enabled real-time optimization, and automated sorting systems, improving throughput and reducing operational downtime. Innovations such as high-purity monomer production, circular feedstock loops, and modular recycling units are expanding industrial applications in packaging, automotive, and specialty chemicals. Digital twin simulations and predictive analytics are increasingly used to optimize reactor conditions, energy consumption, and yield, positioning companies for higher operational efficiency and sustainability compliance.

In March 2023, Agilyx commissioned a new depolymerization facility in Oregon, U.S., capable of processing 25,000 tons of mixed plastics annually, producing high-purity monomers for packaging and specialty chemicals. Source: www.agilyx.com

In July 2023, BASF launched a pilot project in Germany converting post-consumer PET into recycled monomers for automotive components, achieving a 92% recovery rate and significant reductions in virgin raw material usage. Source: www.basf.com

In December 2023, Covestro announced the deployment of AI-enabled process optimization across three European chemical recycling plants, enhancing operational efficiency by 18% and reducing energy consumption by 12%. Source: www.covestro.com

In June 2024, Eni (Versalis) expanded its Priolo facility in Italy, increasing pyrolysis feedstock processing capacity by 30,000 tons annually, focusing on producing recycled feedstocks for packaging and construction applications. Source: www.eni.com

The Chemical Recycling Feedstock Market Report provides a comprehensive analysis of market segments, technologies, applications, and geographic regions. It covers key feedstock types including pyrolysis oils, monomers, syngas, and specialty intermediates, offering insight into adoption trends across packaging, automotive, construction, textiles, and specialty chemicals. The report examines end-user behavior across chemical manufacturers, consumer goods companies, packaging firms, and industrial processors, highlighting enterprise adoption rates and regional consumer preferences. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed analysis of market volume, technological readiness, and regulatory drivers in each region. It also addresses technological advancements such as AI-assisted optimization, automated sorting, depolymerization, and pyrolysis, detailing operational performance improvements and product quality enhancements.

Furthermore, the report explores strategic initiatives, investments, and emerging market segments, offering decision-makers actionable insights for expansion, partnerships, and innovation in the chemical recycling feedstock ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,550.0 Million |

| Market Revenue (2032) | USD 3,274.5 Million |

| CAGR (2025–2032) | 9.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Eni (Versalis), Agilyx, Covestro, Ioniqa Technologies, NEXTChem, BASF, Braskem, ReNew ELP, SABIC, TotalEnergies |

| Customization & Pricing | Available on Request (10% Customization is Free) |