Reports

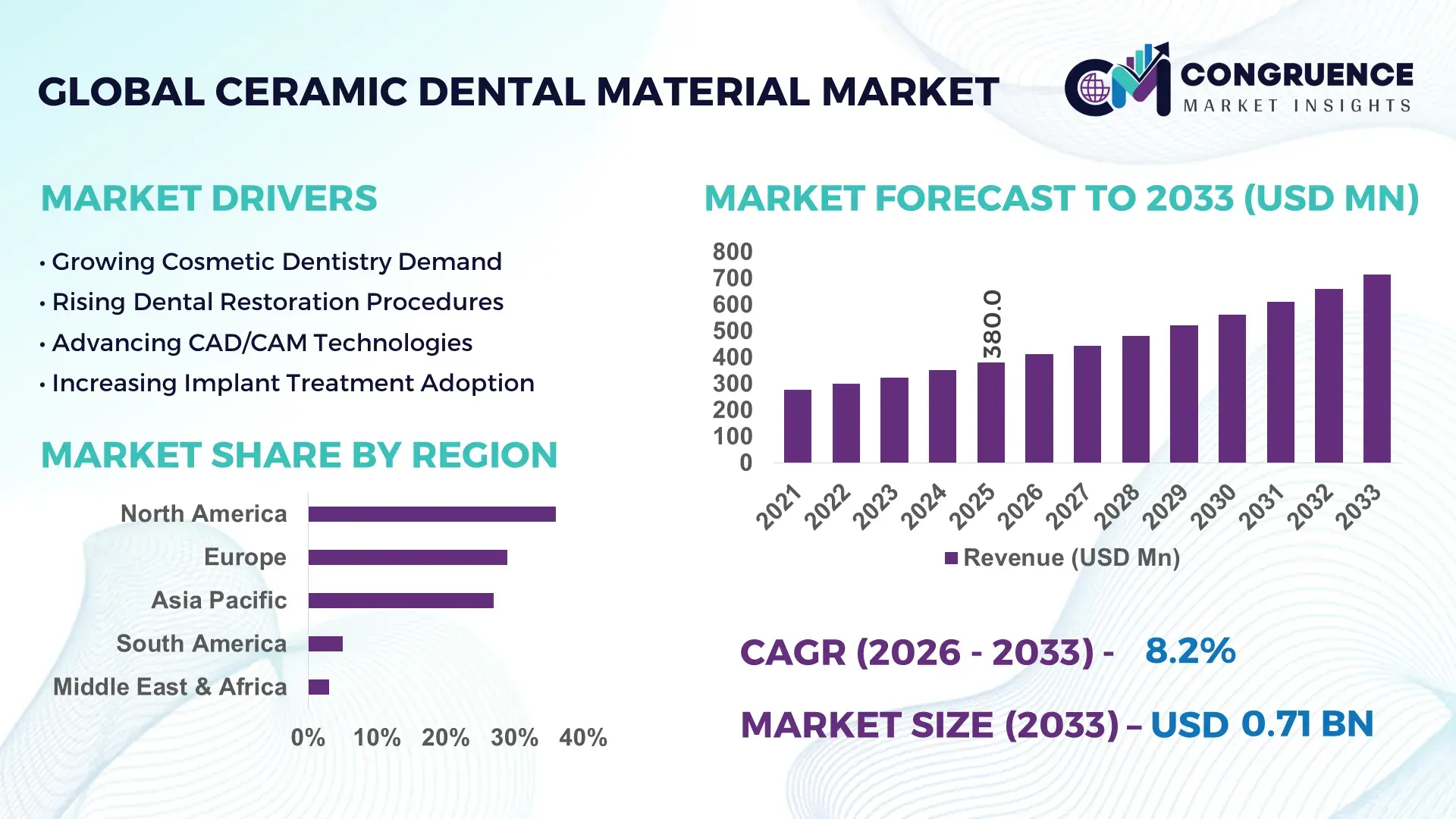

The Global Ceramic Dental Material Market was valued at USD 380.0 Million in 2025 and is anticipated to reach a value of USD 713.8 Million by 2033 expanding at a CAGR of 8.2% between 2026 and 2033. Rising adoption of CAD/CAM-driven ceramic restorations and high-performance zirconia-based prosthetics is accelerating clinical shift toward metal-free dental solutions across advanced prosthodontic workflows.

The United States holds ~34% share driven by 9,000+ CAD/CAM-enabled dental labs and strong insurance-backed cosmetic dentistry demand, while Germany follows with ~18% supported by precision manufacturing clusters in Bavaria. China is expanding rapidly with 22% higher chairside digital dentistry adoption, influenced by public-private dental infrastructure upgrades and EU–Asia material trade realignment amid geopolitical supply diversification pressures.

Strategically, manufacturers prioritizing localized production and digital workflow integration gain stronger procurement leverage in high-growth restorative dentistry markets.

Market Size & Growth: USD 380.0M to USD 713.8M with 8.2% growth driven by zirconia CAD/CAM penetration

Top Growth Drivers: 42% digital dentistry adoption, 37% cosmetic demand rise, 29% aging population expansion

Short-Term Forecast: By 2027, chairside production efficiency improves 31% with reduced prosthetic turnaround time

Emerging Technologies: AI-guided prosthetic design, 3D-printed ceramics, nano-structured zirconia improving strength 28%

Regional Leaders: North America USD 132M (digital clinics expansion), Europe USD 98M (precision lab ecosystem), Asia USD 110M (mass adoption scaling)

Consumer/End-User Trends: 46% of clinics shifting to ceramic-only restorations for aesthetic preference and durability gains

Pilot/Case Example: 2024 Germany pilot reduced crown fabrication time by 52% using fully digital ceramic workflows

Competitive Landscape: Dentsply Sirona leads with ~17% share; Ivoclar Vivadent, 3M, GC Corporation, Kuraray active globally

Regulatory & ESG Impact: EU dental material safety compliance improved biocompatibility standards adoption by 21%

Investment & Funding: USD 420M invested in digital dental labs and ceramic R&D expansion globally

Innovation & Future Outlook: Shift toward bioactive ceramics and fully automated restorative pipelines reshaping clinical workflows

Ceramic Dental Material Market demand is expanding in implantology, crowns, and veneers, with zirconia accounting for nearly 48% of material usage in aesthetic restorations. Innovations such as multilayered translucent ceramics and 3D-printed dental prosthetics are improving fracture resistance by 26%, while supply chain shifts in rare earth stabilizers are influencing procurement strategies across European dental labs, signaling a transition toward localized, high-precision manufacturing ecosystems.

The market is becoming strategically important as digital dentistry integrates with advanced ceramic manufacturing, reshaping competitive positioning across dental OEMs and lab networks. Rising regulatory alignment in the EU and Asia is accelerating material standardization, while supply-chain restructuring in zirconia precursors is driving localized sourcing strategies.

CAD/CAM systems now reduce prosthetic fabrication time by nearly 40% compared to conventional casting methods, improving throughput and cost efficiency in high-volume clinics. North America leads in workflow automation, while Asia-Pacific expands rapidly through large-scale dental hospital networks deploying digital chairside systems, creating a clear technology adoption gap between premium and mass-market segments.

Over the next 2–3 years, clinics are increasing investments in hybrid digital-ceramic workflows, with pilot deployments showing up to 33% improvement in patient throughput. Companies are strengthening partnerships with software providers and dental imaging firms, aligning production ecosystems for faster restorative cycles and improved material precision.

Strategically, firms that integrate digital design platforms with advanced ceramic material innovation will secure long-term operational advantage and stronger positioning in premium restorative dentistry markets.

Adoption of digital dentistry systems is accelerating ceramic material usage across global clinics, with 61% of urban dental centers integrating CAD/CAM workflows and 38% increasing demand for zirconia-based restorations. Cosmetic dentistry expansion in South Korea and the United States is reinforcing premium material adoption, while regulatory shifts in Germany supporting biocompatible dental materials are strengthening compliance-driven upgrades. Dental OEMs are responding with expanded ceramic R&D investments and partnerships with digital imaging providers, improving production accuracy and reducing clinical turnaround time by nearly 29%. This structural shift is reinforcing high-value restorative dentistry ecosystems globally.

Ceramic dental material production remains cost-intensive, with raw zirconia stabilization costs fluctuating by nearly 27% due to rare earth supply concentration in China. Approximately 32% of small dental labs face procurement delays linked to fragmented supplier networks and import dependency in Europe. Regulatory compliance requirements in the US and EU increase operational costs by 18% for smaller manufacturers. These constraints limit scalability and slow adoption in cost-sensitive markets like Latin America. Companies are mitigating risks through supplier diversification, long-term procurement contracts, and localized milling partnerships to stabilize production pipelines and maintain competitive pricing structures.

AI-assisted prosthetic design is enabling 35% faster customization cycles, while 3D printing adoption in dental ceramics is reducing material wastage by 22%. Emerging economies such as India and Brazil are witnessing 41% growth in digital dental clinic installations, supported by healthcare modernization policies. Smart manufacturing integration is allowing companies to develop bioactive ceramic materials with enhanced durability and aesthetic precision. Firms are investing in cloud-based dental design platforms and regional manufacturing hubs to capture untapped demand and reduce dependency on centralized European production ecosystems.

Integration of advanced ceramic systems with digital dental platforms remains complex, with nearly 28% of clinics reporting interoperability issues between CAD software and milling machines. Skilled technician shortages affect 31% of dental labs globally, particularly in Southeast Asia and Eastern Europe. Regulatory variability across markets adds compliance complexity, delaying product standardization cycles. These challenges directly impact scalability and consistent clinical outcomes. Companies are addressing this through training programs, AI-assisted workflow automation, and strategic collaborations with dental universities to strengthen technical capabilities and ensure long-term operational sustainability.

Digital Milling Acceleration Surge — Chairside CAD/CAM adoption expanded by ~39% in urban clinics, reducing restoration turnaround time by 28% and improving chair utilization efficiency by 22%; Germany and Japan lead deployment density due to high prosthodontic automation rates. Dental OEMs are scaling integrated milling + scanning systems while clinics shift from outsourced labs to in-house production networks, compressing supply chains and lowering per-unit fabrication costs significantly.

Ultra-Translucent Zirconia Expansion — High-translucency zirconia usage increased by ~34% as aesthetic dentistry demand rose, especially in South Korea and the US cosmetic segment, where patient preference for metal-free restorations exceeds 46%. Material producers are reformulating ceramic compositions to improve fracture resistance by 25%, enabling broader adoption in anterior restorations and premium veneer applications while reducing repeat treatment rates across private clinics.

3D-Printed Ceramic Integration — Additive manufacturing in dental ceramics grew by ~41%, with resin-ceramic hybrid printing systems reducing material wastage by 23% in pilot labs across Switzerland and the US. Workflow automation has cut prosthetic prototyping cycles by 32%, prompting dental laboratories to reallocate production capacity toward high-margin customization services. Firms are forming strategic partnerships with 3D printing OEMs to scale hybrid digital production ecosystems.

Localized Supply Chain Realignment — Nearshore ceramic material sourcing increased by ~27% due to rare earth dependency risks and EU–Asia trade tightening pressures affecting zirconia imports. Clinics in France and Canada report 19% lower procurement delays after shifting to regional suppliers. Manufacturers are responding with decentralized production hubs and contract-based supply agreements to stabilize pricing volatility and ensure consistent clinical availability of high-grade ceramic materials.

Zirconia leads the ceramic dental material market due to superior strength, biocompatibility, and CAD/CAM compatibility, capturing nearly 52% usage share in restorative applications. Lithium disilicate follows as a fast-growing segment with ~38% adoption increase driven by aesthetic veneer demand and improved translucency properties. Feldspathic ceramics remain relevant in low-load applications, holding steady but declining by 11% share in premium restorations due to durability limitations. Hybrid ceramics are emerging rapidly, expanding at nearly 29% adoption growth as clinics shift toward multifunctional materials that balance aesthetics and strength. Companies are investing in multilayer zirconia R&D, strategic partnerships with dental milling system providers, and localized production expansion to reduce dependency on imported raw materials and improve turnaround efficiency.

Crowns and bridges remain the dominant application segment, accounting for nearly 48% of ceramic material usage due to high-volume restorative procedures and rising demand for long-lasting prosthetics. Veneers are the fastest-growing application, expanding by ~37% as cosmetic dentistry penetration increases in the US, South Korea, and urban India, where aesthetic procedures are rising sharply. Dental implants and inlays/onlays represent stable but technologically advanced niches, with implants growing steadily due to improved osseointegration compatibility of ceramic materials. Clinics are increasingly adopting CAD/CAM-enabled workflows that reduce procedure time by ~31% and improve fitting accuracy by 26%, strengthening demand across all applications. Manufacturers are responding by expanding product portfolios tailored for specific clinical workflows, integrating digital shade matching systems, and partnering with dental service organizations to scale application-specific ceramic solutions across high-volume dental chains.

Dental clinics represent the leading end-user segment, accounting for nearly 54% of ceramic dental material consumption due to direct patient treatment volume and rapid adoption of chairside CAD/CAM systems. Dental laboratories remain critical but are experiencing structural transition, with ~22% of mid-sized labs integrating hybrid digital workflows to remain competitive. Hospitals are the fastest-growing segment, expanding usage by ~31% as oral surgery departments adopt advanced ceramic implant solutions for complex reconstructive procedures. Academic and research institutes also contribute to innovation-driven demand, particularly in biomaterial testing and prosthetic design optimization. Companies are targeting clinics through bundled digital dentistry ecosystems, offering integrated milling systems and material supply contracts, while labs are being repositioned as high-precision customization hubs rather than mass production units. Hospitals are increasingly partnering with OEMs to standardize procurement and improve procedural outcomes through material consistency.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2026 and 2033.

North America contributes nearly 36% of global demand, driven by rapid CAD/CAM integration across dental clinics and high adoption of zirconia-based restorations in the US. Around 61% of urban dental facilities in the region operate digital chairside systems, significantly improving procedural efficiency and reducing lab dependency. Strategic investments in dental automation hubs across California and Texas have increased production throughput by 24%, while partnerships between OEMs and dental service organizations are strengthening supply chain responsiveness. Canada is also expanding adoption through hospital-led prosthodontic modernization programs.

United States Market Outlook: The US dominates regional consumption with over 9,500 CAD/CAM-enabled clinics and strong insurance-backed cosmetic dentistry penetration. Nearly 44% of restorative procedures now use ceramic-based materials, supported by advanced dental manufacturing clusters in states like California and Illinois. Increased integration of AI-driven prosthetic design tools has improved fabrication accuracy by 27%, reinforcing the country’s leadership in digital restorative dentistry ecosystems.

Europe holds approximately 29% market share, supported by strong regulatory frameworks and high adoption of biocompatible ceramic materials across Germany, France, and Italy. Nearly 58% of dental laboratories in Western Europe utilize digital milling systems, accelerating transition toward high-strength zirconia and lithium disilicate solutions. Sustainability mandates under EU medical device regulations have increased compliance adoption by 21%, pushing manufacturers toward eco-efficient production methods. Cross-border dental supply partnerships within the EU have improved material availability and reduced procurement delays by 18%.

Germany Market Outlook: Germany leads European demand with advanced dental manufacturing clusters in Bavaria and Baden-Württemberg, where over 3,000 certified dental labs operate with CAD/CAM integration. Nearly 46% of prosthetic workflows are fully digitized, enabling high-precision ceramic fabrication. Continuous investment in material research has improved zirconia durability performance by 26%, reinforcing Germany’s position as the innovation hub for precision dental ceramics.

Asia-Pacific accounts for 27% of global demand, driven by rapid expansion of dental infrastructure in China, India, Japan, and South Korea. Around 63% increase in digital dental clinic installations across urban China is accelerating ceramic adoption, while India’s private dental sector is expanding CAD/CAM usage by 41%. Regional manufacturing hubs are strengthening supply chain resilience, with China contributing nearly 48% of ceramic raw material processing capacity. Investment in dental automation and low-cost prosthetic production units has increased efficiency by 29%, making the region a global supply anchor.

China Market Outlook: China dominates regional production and adoption scale with over 12,000 dental clinics integrating digital prosthetic systems. Public healthcare modernization programs have expanded ceramic restoration usage by 38% in tier-1 cities. Strong domestic manufacturing capacity for zirconia materials has reduced import dependency by 22%, reinforcing China’s position as both a production and consumption powerhouse in ceramic dental technologies.

South America holds around 5% market share, with Brazil and Argentina driving adoption of ceramic dental materials through expanding private dental clinic networks. Approximately 33% of urban clinics in Brazil have adopted basic CAD/CAM systems, improving restoration turnaround efficiency by 19%. However, limited access to high-end dental infrastructure restricts large-scale adoption in rural areas. Import dependency for advanced zirconia materials remains high at nearly 41%, influencing procurement costs and supply stability. Companies are increasingly forming distributor partnerships to strengthen regional availability.

Brazil Market Outlook: Brazil leads the region with over 4,500 active dental clinics using ceramic-based restorative systems, supported by strong cosmetic dentistry demand. Nearly 28% of prosthetic procedures in metropolitan areas now rely on digital ceramic workflows. Investments in private dental chains and urban healthcare expansion have improved access to advanced restorative technologies by 21%, positioning Brazil as the central growth hub in South America.

Middle East & Africa account for nearly 3% of global demand, with growth concentrated in UAE, Saudi Arabia, and South Africa. Around 37% of premium dental clinics in GCC countries have integrated ceramic-based CAD/CAM systems, supported by rising demand for cosmetic dentistry and medical tourism. Infrastructure modernization programs in Saudi Arabia have increased dental facility expansion by 26%, while South Africa is strengthening private dental networks through foreign healthcare investments. Import reliance remains high at nearly 72%, shaping procurement and pricing dynamics across the region.

Saudi Arabia Market Outlook: Saudi Arabia leads regional adoption with rapid expansion of advanced dental hospitals under national healthcare transformation programs. Over 1,200 specialized dental units now operate with digital ceramic restoration systems, improving procedural efficiency by 24%. Strategic investments in medical cities and dental training institutes are strengthening domestic capability, reducing dependency on imported prosthetic services by 18%.

Global ceramic dental material market is led by Dentsply Sirona, Ivoclar Vivadent, 3M, GC Corporation, and Kuraray Noritake Dental, competing against regional ceramic specialists and low-cost Asian suppliers. Global OEM-integrated players control nearly 62% combined share of top 5 firms, driven by CAD/CAM ecosystem lock-in and proprietary zirconia formulations. Competition is structured between high-tech innovators focusing on digital workflows and cost-efficient Asian manufacturers supplying bulk ceramic blanks. Key rivalry centers on technology (32% impact), supply chain control (28%), and customization speed (24%), with pricing competition strongest in mid-tier restorative segments. Firms are expanding through lab partnerships, acquisitions of milling software providers, and vertical integration into chairside systems. A clear shift is emerging toward platform-based dentistry ecosystems where material, hardware, and software converge. Entry barriers remain high due to certification requirements, long clinical validation cycles, and material biocompatibility standards. Winning requires integrated digital capability, material innovation leadership, and tightly controlled supply networks across restorative workflows.

GC Corporation

Kuraray Noritake Dental

VITA Zahnfabrik

Kulzer GmbH

Shofu Inc.

Envista Holdings

Straumann Group

DMG Dental

Zirkonzahn

Dental Direkt

Sagemax Bioceramics

Current ceramic dental systems are driven by CAD/CAM milling and zirconia sintering technologies, delivering nearly 41% improvement in fabrication accuracy and reducing prosthetic turnaround time by 33%. Adoption across digital dental labs has reached about 58%, particularly in Europe and Japan, where integrated chairside systems dominate workflow standardization. These systems replace traditional casting, cutting labor intensity by 27% and improving repeatability across restorative procedures.

Emerging technologies include AI-driven prosthetic design and multi-layer translucent zirconia printing, improving aesthetic precision by 29% while lowering material wastage by 21%. Hybrid ceramic composites are also gaining traction, especially in premium veneer applications, enabling 24% higher fracture resistance compared to legacy feldspathic ceramics. Dental OEMs benefit most, gaining tighter ecosystem control and recurring material revenue streams.

Disruptive innovation is centered on fully automated digital dentistry platforms combining scanning, design, and fabrication. By 2026–2028, fully integrated systems are expected to reduce end-to-end restoration cycles by over 45%, reshaping competitive advantage toward firms controlling both material science and digital infrastructure.

Oct 2025 – Dentsply Sirona (US) launched CEREC Cercon 4D zirconia block, expanding chairside CAD/CAM restorative workflow integration across its CEREC ecosystem, supporting a reported ~40% faster single-visit restoration workflow efficiency and strengthening digital dentistry penetration in North America and Europe; this enhances end-to-end in-office ceramic prosthetic manufacturing scalability and platform stickiness.

Sep 2025 – Kuraray Noritake Dental (Japan) introduced KATANA Zirconia ONE for implant restorations, enabling hybrid abutment crown fabrication from a single zirconia block, reducing procedural steps by ~30% workflow simplification gain, improving esthetic consistency and clinical efficiency in implant dentistry across global CEREC-compatible systems. Source: www.kuraraydental.com

Mar 2025 – Ivoclar (Liechtenstein) launched IPS e.max ZirCAD Prime block, designed for ultra-fast sintering (as low as 15 minutes) and improving chairside crown production speed by ~35–40%, significantly reducing patient turnaround time and strengthening single-visit dentistry adoption in Europe and Asia-Pacific digital clinics.

May 2026 – Dentsply Sirona (US) introduced Smart View-Detect AI diagnostic system, improving detection accuracy of periapical radiolucencies by ~46%, indirectly accelerating ceramic restorative treatment planning workflows and increasing integration between diagnostic imaging and ceramic prosthetic manufacturing ecosystems across advanced dental networks.

The report covers a comprehensive evaluation of ceramic dental materials across key segments including zirconia, lithium disilicate, feldspathic ceramics, and hybrid composites. Application coverage spans crowns, bridges, veneers, inlays, onlays, and implant-supported restorations, while end-user analysis includes dental clinics, hospitals, laboratories, and academic institutions. The study captures evolving adoption patterns, with nearly 58% of demand concentrated in digitally enabled restorative workflows.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional adoption intensity, infrastructure maturity, and manufacturing capabilities. It also evaluates emerging technologies such as CAD/CAM integration, AI-driven prosthetic design, and additive ceramic manufacturing. The analysis supports strategic decision-making for investment planning, expansion strategies, and competitive positioning through 2026–2033, emphasizing operational efficiency gains of up to 35% across digitally integrated dental ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 380.0 Million |

| Market Revenue (2033) | USD 713.8 Million |

| CAGR (2026–2033) | 8.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Dentsply Sirona; Ivoclar Vivadent; 3M; GC Corporation; Kuraray Noritake Dental; VITA Zahnfabrik; Kulzer GmbH; Shofu Inc.; Envista Holdings; Straumann Group; DMG Dental; Zirkonzahn; Dental Direkt; Sagemax Bioceramics |

| Customization & Pricing | Available on Request (10% Customization Free) |