Reports

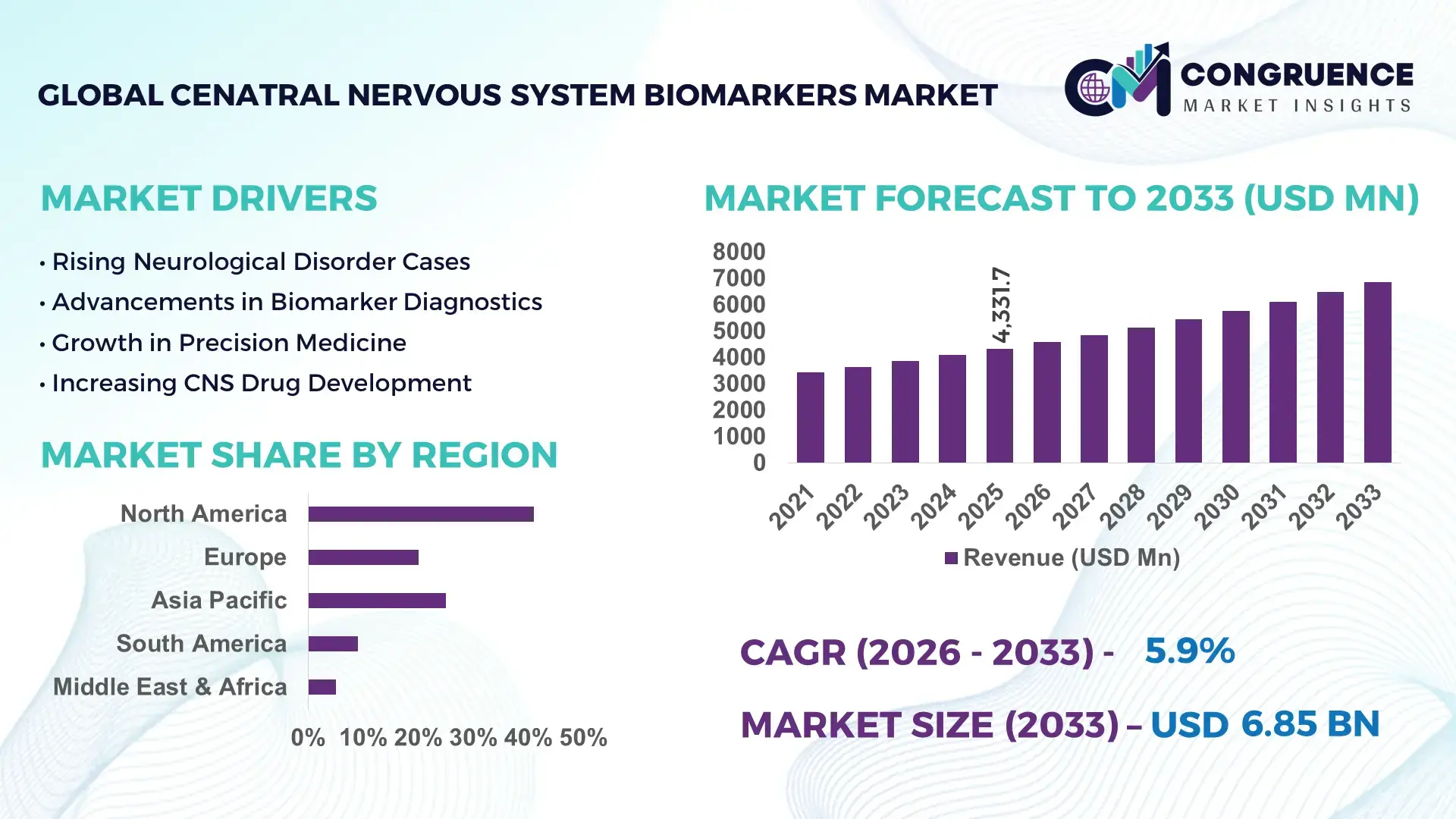

The Global Central Nervous System Biomarkers Market was valued at USD 4331.72 Million in 2025 and is anticipated to reach a value of USD 6852.16 Million by 2033 expanding at a CAGR of 5.9% between 2026 and 2033. Rising neurodegenerative disease screening programs and accelerated biomarker-based drug development pipelines are driving over 38% higher adoption of precision CNS diagnostics across tertiary healthcare networks and pharmaceutical research platforms in 2026.

The United States dominates the global central nervous system biomarkers market with approximately 41% share, supported by more than USD 2.4 billion allocated toward neuroscience and biomarker-focused research initiatives during 2025–2026. Over 58% of advanced neurology hospitals across the country integrated AI-enabled biomarker analytics into neurodegenerative disease assessment workflows, while large-scale precision medicine programs strengthened adoption of blood-based biomarker technologies. Heightened geopolitical focus on neurological healthcare resilience following global aging-related healthcare expenditure pressures has also accelerated investment in biomarker-driven clinical infrastructure and decentralized neurological testing capabilities.

Companies prioritizing scalable biomarker validation, AI-integrated neurological diagnostics, and region-specific clinical partnerships are positioned to secure stronger competitive differentiation in the high-growth central nervous system biomarkers industry.

Market Size & Growth: USD 4331.72 Million in 2025 reaching USD 6852.16 Million by 2033 at 5.9% growth, supported by 38% higher deployment of precision neurological diagnostics and biomarker-led drug discovery programs.

Top Growth Drivers: Neurodegenerative disease diagnostics contribute 34% demand growth, AI-enabled biomarker analytics add 29% operational expansion, and blood-based testing adoption increases 31% across advanced healthcare systems.

Short-Term Forecast: By 2027, automated biomarker testing platforms are projected to reduce neurological diagnostic processing costs by 22% while improving clinical workflow efficiency by 26%.

Emerging Technologies: AI-assisted neuroimaging, multiplex proteomic assays, and liquid biopsy biomarkers improve early-stage CNS disease detection accuracy by over 30% in advanced clinical settings.

Regional Leaders: North America exceeds USD 2.7 Billion with strong precision medicine adoption, Europe surpasses USD 1.8 Billion through regulatory-backed neurological programs, and Asia-Pacific approaches USD 1.5 Billion with rapid hospital digitization.

Consumer/End-User Trends: More than 52% of neurology centers increased adoption of blood-based CNS biomarker panels to accelerate minimally invasive disease monitoring.

Pilot/Case Example: In 2026, integrated biomarker analytics programs across tertiary neurology hospitals improved early Alzheimer’s detection rates by 24% and reduced repeat testing volumes by 18%.

Competitive Landscape: The top five companies collectively control nearly 46% market share through advanced assay portfolios, AI diagnostics integration, and biomarker validation partnerships.

Regulatory & ESG Impact: Neurological precision medicine frameworks improved clinical trial efficiency by 21%, while decentralized testing models reduced sample transportation requirements by 17%.

Investment & Funding: Global neuroscience and biomarker-focused investments surpassed USD 3.1 Billion during 2025–2026, supported by pharmaceutical collaborations and regional laboratory expansion initiatives.

Innovation & Future Outlook: Next-generation digital biomarkers, wearable neurological monitoring, and real-time cognitive analytics are reshaping competitive positioning amid ongoing global healthcare infrastructure modernization.

Pharmaceutical and biotechnology companies account for nearly 44% of total central nervous system biomarkers market demand, followed by diagnostic laboratories and academic research institutions with combined contributions exceeding 36%. Advanced blood-based biomarker assays, AI-driven neuroimaging platforms, and multiplex protein detection technologies are improving neurological disease classification accuracy and accelerating therapeutic trial enrollment. North America maintains the strongest demand concentration, while Asia-Pacific records faster adoption through expanding neurology infrastructure and localized biomarker manufacturing capabilities. Regulatory alignment around precision medicine frameworks and regional supply chain diversification strategies are further strengthening commercialization pathways. Digital biomarkers integrated with wearable cognitive monitoring systems are expected to redefine long-term neurological disease management and strategic clinical decision-making over the next decade.

The central nervous system biomarkers market is becoming strategically important as pharmaceutical companies, diagnostic laboratories, and healthcare systems accelerate precision neurology programs to reduce late-stage clinical failure rates and improve early disease detection efficiency. More than 46% of neurological drug pipelines in 2026 are integrating biomarker-guided patient selection frameworks, while regulatory emphasis on early Alzheimer’s diagnosis and decentralized testing infrastructure is reshaping commercialization priorities. Increased digital pathology adoption and hospital laboratory modernization are also strengthening demand for scalable biomarker analytics platforms across cognitive disorder management networks.

Advanced blood-based biomarker assays now deliver nearly 32% faster diagnostic processing compared with conventional cerebrospinal fluid testing methods while reducing invasive procedural dependency and laboratory operational costs. The United States leads high-volume deployment through AI-integrated neurology platforms and large-scale clinical validation programs, whereas Japan and Germany are prioritizing compact automated biomarker testing systems for aging population management. Over the next two to three years, more than 40% of tertiary neurology centers are expected to expand real-time biomarker monitoring capabilities through integrated digital health ecosystems.

Leading companies are strengthening partnerships with pharmaceutical developers, cloud analytics providers, and specialty diagnostic networks to improve biomarker standardization and multi-site clinical deployment efficiency. Hospitals implementing automated neurodegenerative biomarker workflows have already reported 21% lower repeat testing rates and faster therapeutic decision timelines. Companies securing scalable validation capabilities, AI-enabled neurological analytics, and localized testing infrastructure will gain stronger long-term competitive positioning across the evolving precision neuroscience landscape.

Rising adoption of precision neurology and biomarker-guided therapeutics is accelerating structural transformation across the central nervous system biomarkers market. More than 54% of advanced neurology research programs in the United States integrated biomarker-based patient stratification tools during 2026, while blood-based neurological testing adoption increased by 33% across specialty diagnostic centers. Regulatory support for early Alzheimer’s screening and faster neurodegenerative disease identification is strengthening demand for multiplex assay technologies and AI-assisted biomarker analytics. Pharmaceutical companies are responding by expanding companion diagnostic partnerships and increasing biomarker validation investments to reduce clinical trial inefficiencies. Japan and Germany are also accelerating automated neurodiagnostic infrastructure deployment to manage aging populations more effectively. Companies combining scalable assay development with real-time neurological data analytics are achieving stronger clinical integration and faster therapeutic commercialization advantages.

Inconsistent biomarker validation standards and interoperability gaps remain major structural restraints affecting large-scale deployment efficiency. Nearly 37% of neurology laboratories continue using fragmented assay interpretation frameworks, creating variability in diagnostic reproducibility and slowing multi-center clinical integration. High costs associated with advanced neuroimaging systems and proteomic testing platforms increased operational expenditure by approximately 24% for mid-sized diagnostic providers during 2025–2026. Supply dependency on specialized reagents and analytical instruments, particularly from the United States and select European manufacturing hubs, has also intensified procurement pressure amid healthcare infrastructure expansion. Companies are mitigating risk through regional manufacturing localization, long-term supplier agreements, and cloud-based data harmonization platforms. Organizations improving assay standardization and cross-platform compatibility are reducing deployment delays while strengthening laboratory scalability and operational reliability.

AI-enabled biomarker analytics and digital neurological monitoring systems are creating high-value opportunities across diagnostics, pharmaceutical development, and remote patient management. More than 42% of neurological clinical trials are expected to integrate AI-supported biomarker interpretation platforms within the next three years to improve patient selection precision and reduce trial inefficiencies. China and South Korea are accelerating investment in automated molecular diagnostics infrastructure, while wearable cognitive monitoring technologies are improving longitudinal neurological assessment accuracy by nearly 28%. Companies are also developing cloud-connected biomarker ecosystems capable of integrating imaging, genomic, and proteomic datasets into unified clinical decision frameworks. Strategic collaborations between software analytics providers and specialty diagnostics companies are expanding decentralized neurological testing capabilities. Organizations prioritizing AI-integrated biomarker ecosystems are positioned to unlock faster diagnostic scalability and differentiated precision medicine capabilities.

Long-term scalability of the central nervous system biomarkers market is challenged by complex integration requirements across imaging systems, molecular diagnostics platforms, and digital health infrastructure. Nearly 39% of healthcare providers report operational difficulty integrating biomarker datasets with existing electronic neurological record systems, slowing clinical workflow optimization. Cybersecurity exposure linked to cloud-connected neurological analytics platforms increased by approximately 18% as healthcare networks expanded remote biomarker monitoring programs. Workforce shortages in computational neurology and bioinformatics are further limiting large-scale deployment consistency across advanced testing environments. The United Kingdom and Canada are increasing investments in neurological data infrastructure modernization, yet interoperability fragmentation continues affecting cross-border research collaboration efficiency. Companies must strengthen secure analytics architecture, workforce training programs, and multi-platform integration capabilities to maintain long-term competitiveness and sustainable precision neurology deployment.

AI-Led Diagnostic Workflow Expansion Advanced neurology centers in the United States increased AI-assisted biomarker interpretation deployment by 36% during 2025–2026 to reduce diagnostic variability and accelerate clinical throughput. Automated imaging-biomarker integration platforms lowered neurological assessment turnaround time by nearly 24%, particularly across Alzheimer’s and Parkinson’s disease screening programs. Companies are restructuring laboratory workflows through cloud-based analytics partnerships and centralized data processing hubs to address specialist shortages and rising neurological case volumes.

Shift Toward Blood-Based Testing Blood-based CNS biomarker assays recorded over 31% higher clinical adoption as hospitals reduced dependence on invasive cerebrospinal fluid procedures and expanded outpatient neurological diagnostics. Germany and Japan accelerated deployment of compact automated testing systems to manage aging population burdens more efficiently. Diagnostic providers are scaling decentralized sample collection networks and reagent manufacturing partnerships to improve testing accessibility, reduce repeat procedures, and stabilize operational costs amid increasing neurology screening demand.

Clinical Trial Biomarker Standardization Pharmaceutical companies integrated standardized biomarker validation frameworks across nearly 44% of late-stage neurological drug trials to improve patient stratification consistency and regulatory readiness. Multi-site digital monitoring platforms reduced duplicate testing frequency by approximately 19%, while harmonized assay protocols improved cross-border data compatibility. Companies are expanding partnerships with specialty laboratories and analytics providers to strengthen biomarker reproducibility and accelerate precision neuroscience commercialization pipelines.

Wearable Cognitive Monitoring Integration Wearable neurological monitoring adoption increased by 28% across cognitive disorder management programs as healthcare providers expanded remote patient assessment capabilities. Real-time digital biomarkers improved longitudinal symptom tracking accuracy by nearly 22%, particularly in epilepsy and multiple sclerosis monitoring workflows. South Korea and the United Kingdom accelerated connected neurological infrastructure upgrades, while medical technology companies expanded sensor integration partnerships and edge-computing analytics platforms to strengthen continuous neurological surveillance efficiency.

Fluid biomarkers remain the leading segment within the central nervous system biomarkers market, accounting for nearly 34% of total deployment demand due to faster clinical integration, minimally invasive testing capability, and lower operational complexity compared with imaging-based diagnostics. Hospitals and diagnostic laboratories increasingly favor blood-based biomarker assays as they reduce neurological testing turnaround time by approximately 26% while improving outpatient scalability. Proteomic biomarkers are emerging as the fastest-growing segment, supported by nearly 32% higher adoption in neurodegenerative disease research and precision drug development workflows. Imaging biomarkers continue maintaining strong relevance in advanced neurological assessment programs, particularly in the United States, where AI-integrated neuroimaging infrastructure is expanding rapidly. Genomic biomarkers are strengthening therapeutic targeting capabilities, while metabolic biomarkers are gaining attention for longitudinal disease progression monitoring. Companies are prioritizing multiplex assay innovation, automated biomarker platforms, and strategic pharmaceutical collaborations to improve diagnostic accuracy and expand commercial testing capacity across high-volume neurology networks.

Alzheimer’s disease diagnosis remains the dominant application segment, contributing approximately 38% of total biomarker utilization due to expanding aging populations, earlier cognitive screening initiatives, and increasing integration of precision neurology protocols. Hospitals and specialty neurology centers are deploying blood-based Alzheimer’s biomarker assays to reduce diagnostic delays by nearly 24% and improve therapeutic intervention timelines. Drug development is emerging as the fastest-growing application as pharmaceutical companies integrate biomarker-guided patient stratification into over 42% of neurological clinical trials to improve treatment targeting efficiency. Parkinson’s disease detection and multiple sclerosis monitoring continue gaining operational importance through AI-assisted imaging and longitudinal digital biomarker programs. Epilepsy diagnosis is also expanding through wearable neurological monitoring technologies, while neurological research institutions are strengthening multi-modal biomarker validation programs. Companies are increasing automation investments, expanding decentralized testing infrastructure, and forming data analytics partnerships to improve neurological disease management scalability and accelerate clinical deployment consistency.

Hospitals remain the dominant end-user segment in the central nervous system biomarkers market, representing nearly 41% of total deployment activity due to large-scale neurology infrastructure, advanced diagnostic integration, and higher patient throughput requirements. Major hospital networks in the United States and Japan expanded automated neurological biomarker workflows by approximately 29% during 2025–2026 to accelerate cognitive disorder diagnosis and optimize specialist utilization. Pharmaceutical companies are emerging as the fastest-growing end-user group as biomarker-guided drug development and precision clinical trial programs continue expanding across neurodegenerative therapeutic pipelines. Diagnostic laboratories are strengthening market presence through centralized assay processing and decentralized sample collection models, while research institutes and academic medical centers continue driving biomarker validation and translational neuroscience innovation. Neurology clinics are also increasing adoption of portable and blood-based testing systems to improve outpatient efficiency. Companies are responding through customized assay platforms, long-term enterprise contracts, and AI-enabled analytics ecosystem development to secure larger institutional deployment volumes.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

Precision Neurology Infrastructure Accelerates Enterprise Deployment

North America maintains the highest concentration of advanced neurological biomarker deployment due to strong precision medicine infrastructure, large-scale pharmaceutical research activity, and integrated diagnostic networks. The region contributes nearly 41% of global deployment volume, with the United States driving over 68% of regional biomarker testing activity through AI-assisted neurodiagnostic platforms and automated laboratory ecosystems. More than 58% of tertiary neurology hospitals implemented blood-based biomarker testing workflows during 2025–2026 to improve early-stage cognitive disease detection efficiency. Pharmaceutical companies are also expanding biomarker-guided neurological trials through strategic partnerships with specialty laboratories and cloud analytics providers. Canada is strengthening decentralized neurological monitoring programs through digital health modernization and hospital network integration initiatives.

United States Market Outlook: The United States leads the regional market through strong neuroscience infrastructure, large-scale biomarker validation programs, and advanced clinical trial ecosystems. More than 46% of neurological drug pipelines in the country integrated biomarker-guided patient stratification frameworks during 2026. Major hospital systems expanded AI-enabled neuroimaging and fluid biomarker deployment to reduce diagnostic turnaround time and optimize specialist utilization. Federal precision medicine initiatives and growing pharmaceutical partnerships continue strengthening the country’s operational leadership in scalable neurological diagnostics.

Regulatory Alignment Strengthens Diagnostic Standardization

Europe is advancing through coordinated neurological research frameworks, standardized biomarker validation protocols, and modernization of public healthcare diagnostics infrastructure. The region represents approximately 28% of global biomarker deployment activity, supported by growing adoption of automated neurodiagnostic systems across Germany, France, and the United Kingdom. More than 34% of European neurology laboratories upgraded digital pathology and biomarker analytics systems during 2025–2026 to improve cross-border diagnostic compatibility. Regulatory emphasis on early Alzheimer’s screening and precision neurology integration is accelerating demand for multiplex biomarker assays and AI-supported imaging platforms. Regional pharmaceutical collaborations are also improving clinical trial harmonization and neurological data interoperability across multi-site research environments.

Germany Market Outlook: Germany remains the strongest operational hub within Europe due to advanced hospital infrastructure, neurological research intensity, and industrial-scale diagnostic manufacturing capabilities. Nearly 39% of major neuroscience centers in the country expanded automated biomarker testing systems during 2026 to support aging population management and neurodegenerative disease monitoring. Domestic medical technology companies are strengthening AI-integrated diagnostic platforms and reagent production partnerships, while government-supported healthcare digitization programs continue improving neurological workflow efficiency and biomarker deployment consistency.

Healthcare Modernization Expands Diagnostic Scale

Asia-Pacific is emerging as the fastest-expanding regional market due to rapid healthcare digitization, rising neurological disease burden, and large-scale investment in molecular diagnostics infrastructure. The region accounts for nearly 23% of global deployment activity, with China, Japan, and South Korea leading biomarker testing expansion through hospital modernization and automated laboratory integration. More than 31% of advanced urban healthcare facilities across Asia-Pacific increased deployment of blood-based neurological biomarker platforms during 2025–2026 to improve outpatient diagnostic efficiency. Governments are accelerating precision medicine adoption through neuroscience funding programs and localized diagnostic manufacturing strategies. Regional enterprises are also expanding cloud-connected biomarker analytics and wearable neurological monitoring ecosystems to strengthen long-term disease management capabilities.

China Market Outlook: China is rapidly strengthening its position through aggressive healthcare infrastructure investment, expanding neurological research capabilities, and localized molecular diagnostics manufacturing. Over 43% of large metropolitan hospital systems integrated AI-assisted biomarker analytics into neurodegenerative disease assessment workflows during 2026. Domestic biotechnology companies are increasing partnerships with pharmaceutical developers and cloud computing firms to improve biomarker standardization, while public healthcare modernization programs continue supporting decentralized neurological testing and precision medicine deployment across high-density population centers.

Neurology Access Expansion Drives Demand

South America is experiencing steady biomarker adoption growth as healthcare providers expand neurology diagnostics access and modernize laboratory infrastructure across major urban healthcare systems. Brazil and Argentina account for the majority of regional deployment activity, supported by rising investment in automated diagnostic laboratories and precision medicine programs. Approximately 27% of tertiary hospitals across leading metropolitan healthcare networks introduced blood-based neurological biomarker workflows during 2025–2026 to improve cognitive disorder diagnosis efficiency. Operational limitations linked to fragmented healthcare infrastructure and uneven specialist availability continue affecting deployment consistency in secondary cities. Companies are responding through regional laboratory partnerships, distributor network expansion, and localized training programs to improve diagnostic scalability and operational reliability.

Brazil Market Outlook: Brazil leads the South American market through its large hospital network, expanding private diagnostic sector, and increasing neurological disease screening programs. Nearly 33% of high-volume diagnostic laboratories upgraded automated biomarker analysis systems during 2026 to strengthen neurodegenerative disease assessment capabilities. Private healthcare providers are increasing partnerships with international diagnostics companies to improve reagent availability and workflow standardization, while medical universities are expanding neuroscience research collaboration programs to accelerate biomarker validation and clinical deployment readiness.

Healthcare Infrastructure Modernization Gains Momentum

The Middle East & Africa market is strengthening through healthcare infrastructure modernization, rising neurological disease awareness, and increasing investment in precision diagnostics capabilities. Gulf countries account for the largest concentration of biomarker deployment activity, supported by hospital digitization initiatives and expansion of advanced specialty care networks. More than 24% of tertiary healthcare facilities across the Gulf Cooperation Council integrated AI-assisted neurological diagnostic systems during 2025–2026 to improve cognitive disorder management efficiency. Governments are prioritizing neuroscience infrastructure development and strategic partnerships with international diagnostics providers to strengthen clinical capabilities. African healthcare systems are gradually expanding biomarker accessibility through centralized laboratory modernization and tele-neurology integration programs despite ongoing infrastructure constraints.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region’s strongest market due to aggressive healthcare modernization initiatives, expanding specialty hospital infrastructure, and increasing investment in precision medicine technologies. Over 29% of advanced neurology centers in the country implemented automated biomarker testing workflows during 2026 to strengthen early neurological disease detection and patient monitoring efficiency. Public-private healthcare partnerships and national digital health transformation programs are accelerating deployment of AI-enabled neurodiagnostic systems and improving long-term neurological care infrastructure across major urban healthcare hubs.

The central nervous system biomarkers market is led by Roche, Quanterix, Siemens Healthineers, Labcorp, and Thermo Fisher Scientific, with specialized diagnostics innovators competing directly against large-scale clinical testing and imaging platform providers. The top five players collectively control nearly 46% of global deployment activity through integrated assay portfolios, automated analytics systems, and enterprise hospital partnerships. Competition is increasingly shifting from standalone biomarker testing toward AI-enabled multi-modal neurological diagnostics with 28% faster processing efficiency and nearly 22% lower repeat testing rates compared with legacy workflows. Global leaders are strengthening dominance through vertical integration, reagent manufacturing expansion, and pharmaceutical collaborations, while regional laboratories compete through localized pricing and decentralized neurological testing access. Blood-based biomarker platforms are disrupting traditional cerebrospinal fluid diagnostics, accelerating consolidation across neurological diagnostics ecosystems. High regulatory validation requirements and biomarker standardization complexity remain major entry barriers. Companies capable of combining scalable clinical validation, AI-driven analytics, and rapid enterprise deployment will outperform existing competitors globally.

Thermo Fisher Scientific

Bio-Rad Laboratories

Labcorp

Abbott Laboratories

Qiagen

PerkinElmer

C2N Diagnostics

Sysmex Corporation

Beckman Coulter

Fujirebio

Danaher Corporation

Advanced blood-based biomarker assays, AI-assisted neuroimaging, and multiplex proteomic analytics are reshaping neurological diagnostics workflows across hospitals and pharmaceutical research programs. More than 52% of tertiary neurology centers integrated automated biomarker interpretation systems during 2026 to reduce diagnostic turnaround time and improve patient stratification accuracy. AI-enabled biomarker analytics improved neurological assessment efficiency by approximately 27%, while automated fluid biomarker platforms lowered laboratory processing costs by nearly 19% compared with conventional manual workflows. Companies deploying scalable cloud-connected biomarker ecosystems are achieving faster clinical integration and stronger enterprise adoption across neurodegenerative disease management programs.

Emerging technologies include digital biomarkers, wearable cognitive monitoring systems, and multi-analyte liquid biopsy platforms capable of integrating imaging, proteomic, and genomic datasets into unified neurological assessment frameworks. Blood-based biomarker testing now delivers nearly 32% faster diagnostic processing compared with cerebrospinal fluid diagnostics while reducing invasive procedural dependency. Over 41% of neurological clinical trials are integrating biomarker-guided AI analytics to improve therapeutic targeting and reduce duplicate testing inefficiencies.

Between 2026 and 2028, companies prioritizing automated biomarker validation, decentralized testing infrastructure, and edge-computing neurological monitoring platforms will secure stronger competitive positioning. Pharmaceutical developers and specialty diagnostics providers are expanding strategic partnerships to accelerate commercialization speed, strengthen assay standardization, and improve real-time neurological disease tracking capabilities across precision neuroscience ecosystems.

May 2026 – Roche received CE mark approval for Elecsys pTau217 blood-based Alzheimer’s pathology detection assay, improving diagnostic accessibility with single-assay workflow integration while targeting faster dementia identification across primary and specialty care networks.

May 2026 – Quanterix and Tempus AI partnered to integrate LucentAD Complete biomarker testing into clinical ordering workflows, expanding AI-supported neurological diagnostics and improving patient identification efficiency for Alzheimer’s screening programs nationwide.

March 2026 – Siemens Healthineers launched fully automated pTau217 and BDTau research assays, strengthening neurological biomarker standardization and supporting scalable brain health research workflows across advanced molecular diagnostics laboratories globally.

February 2026 – Labcorp introduced the first FDA-cleared Alzheimer’s blood test for primary care deployment, expanding nationwide neurological screening access and strengthening decentralized cognitive assessment capabilities for patients above 55 years.

The report delivers comprehensive analysis across imaging biomarkers, genomic biomarkers, proteomic biomarkers, metabolic biomarkers, and fluid biomarkers while evaluating operational deployment patterns across Alzheimer’s disease diagnosis, Parkinson’s disease detection, multiple sclerosis monitoring, epilepsy diagnosis, drug development, and neurological research applications. Coverage extends across hospitals, diagnostic laboratories, pharmaceutical companies, academic medical centers, research institutes, and neurology clinics, with detailed assessment of enterprise adoption trends, testing workflow modernization, and AI-integrated biomarker analytics expansion. More than 40% of advanced neurology facilities analyzed within the study have integrated automated or blood-based biomarker platforms into routine neurological assessment operations.

The report provides region-wise strategic analysis covering North America, Europe, Asia-Pacific, South America, and Middle East & Africa with emphasis on healthcare infrastructure modernization, precision medicine deployment, and decentralized neurological diagnostics expansion between 2026 and 2033. It evaluates competitive positioning, biomarker validation strategies, clinical trial integration, digital biomarker innovation, and enterprise partnership activity to support investment planning, product expansion, operational benchmarking, and long-term market entry decisions across the evolving precision neuroscience ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 4331.72 Million |

|

Market Revenue in 2033 |

USD 6852.16 Million |

|

CAGR (2026 - 2033) |

5.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Roche, Quanterix, Siemens Healthineers, Thermo Fisher Scientific, Bio-Rad Laboratories, Labcorp, Abbott Laboratories, Qiagen, PerkinElmer, C2N Diagnostics, Sysmex Corporation, Beckman Coulter, Fujirebio, Danaher Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |