Reports

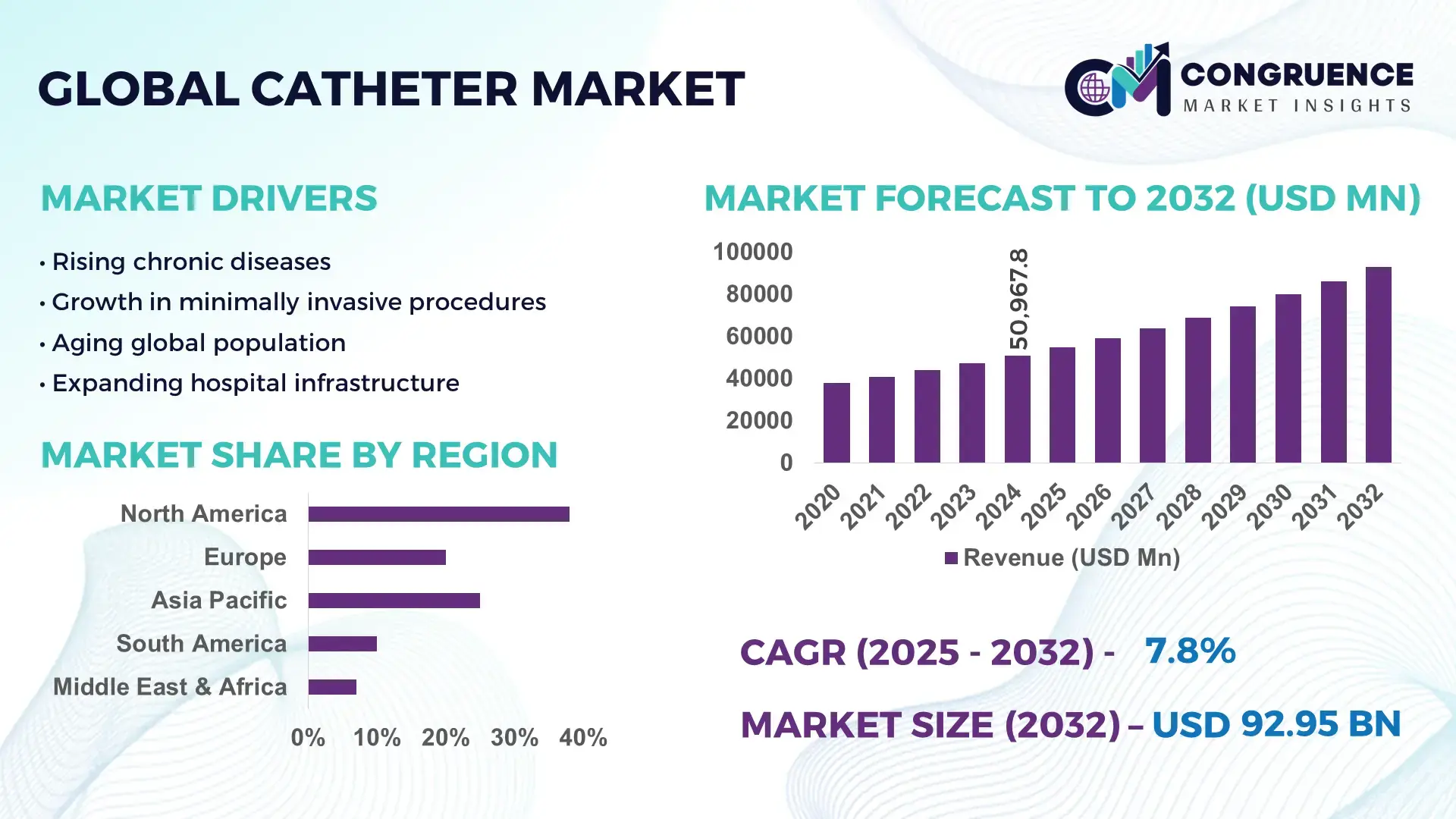

The Global Catheter Market was valued at USD 50967.84 Million in 2024 and is anticipated to reach a value of USD 92949.34 Million by 2032 expanding at a CAGR of 7.8% between 2025 and 2032. Growth is supported by rising volumes of minimally invasive procedures across cardiovascular, urology, and critical care segments.

The Global Catheter Market was valued at USD 50967.84 Million in 2024 and is anticipated to reach a value of USD 92949.34 Million by 2032 expanding at a CAGR of 7.8% between 2025 and 2032. Growth is supported by rising volumes of minimally invasive procedures across cardiovascular, urology, and critical care segments.

The United States holds a leading position in the global catheter landscape, supported by advanced domestic manufacturing and sustained healthcare investment. The country hosts more than 6,500 FDA-registered medical device manufacturing facilities, with annual medical device production exceeding USD 190 billion. Catheters are extensively deployed across cardiology, neurointervention, dialysis, and urinary care, supported by hospital adoption rates above 70% for advanced catheter systems. Public and private healthcare spending surpasses USD 4.5 trillion annually, enabling rapid uptake of technologies such as antimicrobial-coated catheters, sensor-enabled monitoring devices, and image-guided catheter platforms used in high-volume clinical settings.

Market Size & Growth: Valued at USD 50967.84 Million in 2024, projected to reach USD 92949.34 Million by 2032 at a CAGR of 7.8%, driven by increased procedural demand and chronic disease management.

Top Growth Drivers: Cardiovascular catheter utilization increased by 38%, infection-prevention catheter adoption rose by 29%, and procedural efficiency improved by 22%.

Short-Term Forecast: By 2028, healthcare providers are expected to achieve up to 18% reduction in catheter-related complications through advanced materials and monitoring systems.

Emerging Technologies: Smart sensor-enabled catheters, antimicrobial and hydrophilic surface coatings, and bioresorbable catheter materials.

Regional Leaders: North America projected to reach USD 34 Billion by 2032 with high technology penetration, Europe USD 27 Billion driven by aging populations, and Asia-Pacific USD 22 Billion supported by hospital infrastructure expansion.

Consumer/End-User Trends: Hospitals and ambulatory surgical centers represent over 65% of demand, with home healthcare catheter usage increasing steadily.

Pilot or Case Example: A 2024 U.S.-based hospital pilot program achieved a 31% reduction in catheter-associated infection rates using antimicrobial catheter solutions.

Competitive Landscape: The leading company holds approximately 18% share, followed by BD, Medtronic, Abbott, Teleflex, and Boston Scientific.

Regulatory & ESG Impact: Stricter infection control standards and sustainability-focused material regulations are accelerating adoption of advanced catheter designs.

Investment & Funding Patterns: Recent global investments exceeded USD 6.5 Billion, focused on R&D, automation, and next-generation catheter platforms.

Innovation & Future Outlook: AI-assisted navigation, real-time performance monitoring, and personalized catheter solutions are shaping long-term market evolution.

The catheter market supports major healthcare sectors including cardiovascular intervention, urology, neurovascular procedures, and intensive care, with cardiovascular applications contributing approximately 40% of overall demand. Ongoing product innovations such as pressure-sensing catheters, antimicrobial coatings, and minimally invasive delivery systems are enhancing patient safety and procedural outcomes. Regulatory emphasis on infection reduction, combined with economic investment in healthcare infrastructure, continues to influence purchasing decisions. While North America and Europe remain high-consumption regions, Asia-Pacific is witnessing accelerated growth due to expanding access to advanced clinical procedures and modernization of healthcare facilities.

The Catheter Market holds strong strategic relevance within global healthcare systems due to its direct integration into high-frequency, life-sustaining procedures across cardiovascular, urology, neurovascular, oncology, and critical care settings. From a strategic perspective, healthcare providers increasingly view catheter innovation as a pathway to improve clinical efficiency, reduce complications, and align with value-based care models. Advanced antimicrobial-coated catheters deliver up to 32% infection reduction compared to conventional uncoated catheters, translating into measurable decreases in hospital-acquired infection burden and length of stay. Regionally, Asia-Pacific dominates in procedure volume due to expanding hospital infrastructure, while North America leads in advanced catheter adoption with over 68% of hospitals using next-generation or sensor-enabled catheter systems. By 2027, AI-assisted catheter navigation and real-time pressure monitoring are expected to improve procedural accuracy and reduce repositioning errors by approximately 25%. From a compliance and ESG standpoint, manufacturers are committing to sustainability targets such as 30% recyclable polymer usage and 20% waste reduction by 2030, responding to tightening medical waste regulations. In 2024, a U.S.-based healthcare network achieved a 29% reduction in catheter-related complications through deployment of smart catheter tracking and analytics platforms. Looking forward, the Catheter Market is positioned as a pillar of clinical resilience, regulatory compliance, and sustainable healthcare delivery, supporting long-term system efficiency and patient safety.

The increasing preference for minimally invasive procedures is a primary driver of the Catheter Market. Procedures such as angioplasty, electrophysiology studies, dialysis access, and interventional radiology rely heavily on catheter-based delivery systems. Globally, minimally invasive cardiovascular procedures have increased by more than 35% over the past five years, significantly expanding catheter utilization per patient episode. These procedures reduce recovery time by up to 40% compared to open surgery, encouraging higher adoption across hospitals and ambulatory surgical centers. Additionally, aging populations and higher prevalence of diabetes, cardiovascular disease, and renal disorders are increasing catheter-dependent interventions. Hospitals are standardizing catheter usage protocols to improve procedural consistency and patient outcomes, further reinforcing sustained demand across both acute and chronic care settings.

Despite technological advances, catheter-associated complications remain a critical restraint for the Catheter Market. Catheter-associated urinary tract infections and bloodstream infections account for a significant proportion of hospital-acquired infections, increasing treatment costs and regulatory scrutiny. Compliance with stringent sterilization, labeling, and post-market surveillance requirements adds operational complexity for manufacturers and healthcare providers. In some regions, mandatory reporting and penalty frameworks have increased liability exposure, slowing procurement cycles. Additionally, hospitals face rising costs related to staff training, infection monitoring, and product validation. These factors collectively constrain rapid adoption of new catheter technologies, particularly in cost-sensitive healthcare systems.

Smart and connected catheter technologies represent a major opportunity for the Catheter Market. Integration of sensors for pressure, flow, and position tracking enables real-time monitoring, reducing procedural errors and improving clinical decision-making. Hospitals adopting smart catheter systems have reported up to 27% improvement in procedural efficiency and faster response to complications. These technologies also support data-driven care pathways and interoperability with electronic health records, aligning with digital health strategies. Emerging markets present additional opportunity as healthcare systems leapfrog directly to advanced catheter platforms while expanding procedural capacity. As reimbursement models increasingly reward outcomes, smart catheter solutions offer strong differentiation potential for manufacturers and providers alike.

Cost containment and regulatory variation pose persistent challenges for the Catheter Market. Medical-grade polymers, coatings, and sensor components are subject to price volatility, increasing production costs. At the same time, regulatory requirements differ significantly across regions, requiring multiple certification pathways and extending time-to-market. Smaller manufacturers face barriers in scaling compliance infrastructure, while hospitals in developing regions struggle with affordability of advanced catheter systems. Additionally, reimbursement inconsistencies for catheter-based procedures limit purchasing flexibility in some healthcare systems. These challenges necessitate strategic balance between innovation, pricing discipline, and regulatory alignment to sustain long-term market stability.

Accelerated Adoption of Antimicrobial and Infection-Prevention Catheters: Hospitals are increasingly prioritizing catheters with antimicrobial coatings and advanced surface treatments to reduce hospital-acquired infections. Clinical deployment data indicate up to 35% reduction in catheter-associated infections compared to standard catheters, while over 60% of tertiary-care hospitals have integrated antimicrobial variants into routine protocols, particularly in intensive care and urology departments.

Expansion of Smart and Sensor-Integrated Catheter Technologies: Smart catheters embedded with pressure, flow, or position sensors are gaining traction due to measurable improvements in procedural accuracy. Healthcare providers report up to 28% reduction in catheter repositioning events and a 22% improvement in real-time clinical decision-making. Adoption rates exceed 45% among large hospitals in North America and parts of Europe, driven by digital health integration strategies.

Shift Toward Single-Use and Disposable Catheter Systems: Infection control policies and regulatory pressure are accelerating the transition toward single-use catheters. Disposable catheter utilization has increased by approximately 40% over the past few years, with facilities reporting up to 25% lower sterilization-related operational burden. This trend is particularly strong in outpatient and ambulatory surgical centers, where procedural throughput has improved by nearly 18%.

Growing Use of Advanced Polymer and Biocompatible Materials: Manufacturers are increasingly deploying next-generation polymers to improve flexibility, durability, and patient comfort. Advanced material catheters demonstrate up to 30% higher tensile performance and a 20% reduction in patient-reported discomfort during long-duration use. More than 50% of newly launched catheter products now incorporate enhanced biocompatible materials, reflecting a clear shift toward performance-driven design innovation.

The Catheter Market is segmented by type, application, and end-user, each reflecting distinct clinical priorities, adoption patterns, and technology requirements. Product type segmentation highlights a strong preference for catheters designed for high-frequency and high-risk procedures, where safety, precision, and material performance are critical. Application-wise, cardiovascular and urology procedures dominate due to procedure volume intensity and long-term disease prevalence, while emerging applications in neurovascular and oncology care are gaining traction. End-user segmentation shows hospitals as the primary demand center, driven by acute care needs and complex interventions, while ambulatory and home-care settings are expanding steadily due to procedural decentralization. Together, these segments illustrate a market shaped by procedural intensity, infection control priorities, and shifting care delivery models.

The Catheter Market by type includes cardiovascular catheters, urinary catheters, intravenous catheters, neurovascular catheters, and specialty catheters used in oncology and dialysis. Cardiovascular catheters represent the leading type, accounting for approximately 41% of overall adoption, supported by high procedural frequency in angiography, angioplasty, and electrophysiology studies. Urinary catheters hold around 27% adoption, reflecting widespread use across acute and long-term care settings. However, neurovascular catheters are the fastest-growing type, expanding at an estimated 9.4% CAGR, driven by rising stroke interventions and growth in minimally invasive neurointerventional procedures. Intravenous and specialty catheters together contribute a combined 32% share, serving critical niches such as chemotherapy delivery, dialysis access, and intensive care monitoring.

By application, cardiovascular procedures dominate the Catheter Market, accounting for approximately 39% of total usage due to the high prevalence of heart disease and routine interventional workflows. Urology applications follow with about 26% adoption, supported by chronic urinary disorders and post-surgical care requirements. Neurovascular applications currently represent 18%, but this segment is growing fastest at an estimated 10.1% CAGR as stroke incidence rises and mechanical thrombectomy adoption expands globally. Oncology, dialysis, and critical care applications collectively contribute the remaining 17%, serving specialized but essential clinical needs.

Hospitals are the leading end-user segment in the Catheter Market, accounting for approximately 64% of total demand, driven by high-acuity care, surgical interventions, and intensive care unit utilization. Ambulatory surgical centers hold around 21% adoption, benefiting from shorter procedure cycles and increasing outpatient interventions. Home healthcare and long-term care facilities together represent 15%, but this segment is expanding fastest at an estimated 8.7% CAGR due to aging populations and chronic disease management outside hospital settings. Adoption rates of catheter-based therapies in ambulatory centers exceed 45% for same-day cardiovascular and urology procedures, highlighting shifting care delivery models.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

The Catheter Market shows clear regional differentiation driven by healthcare infrastructure maturity, procedural volumes, regulatory intensity, and technology adoption levels. North America leads due to high interventional procedure density, with more than 75 catheter-based procedures per 1,000 population annually. Europe follows with approximately 29% share, supported by strong public healthcare systems and regulatory harmonization. Asia-Pacific accounts for nearly 24% of global demand, underpinned by rapid hospital expansion, increasing chronic disease burden, and rising access to minimally invasive care. South America and the Middle East & Africa together represent around 9%, reflecting developing healthcare infrastructure but steady improvements in procedural access, imports, and localized manufacturing capabilities.

How is advanced clinical infrastructure accelerating adoption of next-generation catheter solutions?

The region holds approximately 38% of the global Catheter Market, supported by high utilization across cardiovascular, neurovascular, dialysis, and critical care applications. Hospitals and integrated delivery networks are the primary demand drivers, accounting for over 70% of catheter consumption. Regulatory frameworks emphasize patient safety and infection reduction, accelerating uptake of antimicrobial and smart catheter systems. Digital transformation initiatives have driven adoption of sensor-enabled catheters, with over 65% of tertiary hospitals using advanced monitoring solutions. A major regional manufacturer expanded production of antimicrobial-coated catheters in 2024, increasing annual output capacity by 18%. Consumer behavior reflects strong preference for clinically validated, premium catheter products, with higher adoption across large hospital systems and specialized care centers.

Why are regulatory alignment and sustainability priorities reshaping purchasing behavior?

Europe represents roughly 29% of the Catheter Market, with Germany, the UK, and France together contributing over 60% of regional demand. Strong regulatory oversight and standardized procurement frameworks drive consistent demand for compliant, high-quality catheter products. Sustainability initiatives emphasize recyclable materials and waste reduction, influencing supplier selection across public healthcare systems. Adoption of advanced catheter technologies is rising, with nearly 48% of hospitals integrating improved coating and biocompatible material solutions. A leading European medical device company introduced recyclable polymer-based catheter lines, reducing packaging waste by 25%. Consumer behavior shows preference for traceable, regulation-aligned catheter products that meet stringent safety and environmental expectations.

How are scale, localization, and access expansion transforming procedural demand?

Asia-Pacific ranks as the fastest-expanding regional market, contributing approximately 24% of global catheter volume. China, India, and Japan collectively account for over 70% of regional consumption due to large patient populations and expanding hospital capacity. Manufacturing localization is increasing, with more than 40% of catheters now produced within the region. Innovation hubs in Japan and South Korea are advancing micro-catheter and flexible polymer technologies. In 2024, a regional manufacturer scaled production by 22% to meet domestic cardiovascular procedure demand. Consumer behavior reflects cost sensitivity combined with growing acceptance of advanced catheter systems in urban hospitals.

What role do healthcare modernization and trade policy play in steady market expansion?

South America holds close to 6% of the global Catheter Market, led by Brazil and Argentina, which together represent over 65% of regional demand. Healthcare infrastructure investment and import facilitation policies are improving access to advanced catheter products. Public hospital upgrades and private sector expansion support consistent procedural growth. A Brazilian medical device supplier increased catheter distribution coverage to over 1,200 hospitals, improving regional availability. Consumer behavior varies widely, with private hospitals adopting higher-end catheter technologies while public facilities prioritize cost-efficient solutions.

How are modernization initiatives and regional hubs shaping demand growth?

The Middle East & Africa region accounts for approximately 3% of global catheter demand, with the UAE, Saudi Arabia, and South Africa driving adoption. Healthcare modernization programs and international partnerships are expanding access to catheter-based procedures. Advanced tertiary hospitals account for nearly 55% of regional catheter usage. Regulatory alignment with international standards is improving import efficiency and product availability. A UAE-based healthcare group expanded interventional cardiology services in 2024, increasing catheter utilization by 20%. Consumer behavior reflects concentrated demand in urban centers and medical tourism hubs.

United States Catheter Market – 32% share: Dominance driven by high procedure volumes, strong manufacturing capacity, and rapid adoption of advanced catheter technologies.

Germany Catheter Market – 11% share: Leadership supported by robust medical device production, standardized healthcare procurement, and strong hospital demand for compliant catheter systems.

The Catheter Market operates within a moderately consolidated yet competitive environment, characterized by the presence of more than 40 active global and regional manufacturers competing across product categories and clinical applications. The top five companies collectively account for approximately 55% of total market presence, indicating a semi-consolidated structure where scale, regulatory capability, and innovation depth determine competitive positioning. Leading players focus heavily on product differentiation through antimicrobial coatings, smart catheter integration, and enhanced biocompatible materials, with over 60% of major competitors maintaining active R&D pipelines. Strategic initiatives remain central to competition, including cross-border manufacturing expansions, hospital network partnerships, and targeted acquisitions to strengthen portfolios in cardiovascular, neurovascular, and urology segments. Product launch intensity has increased, with an estimated 25% rise in next-generation catheter introductions over the past three years. Additionally, over 45% of leading companies have entered digital or data-enabled catheter collaborations to support real-time monitoring and procedural optimization. Competitive pressure is further intensified by regulatory compliance demands, as firms with faster approval cycles and scalable quality systems gain procurement advantages, particularly in North America and Europe.

Becton, Dickinson and Company (BD)

Medtronic plc

Abbott Laboratories

Boston Scientific Corporation

Teleflex Incorporated

B. Braun Melsungen AG

Cook Medical

Terumo Corporation

Cardinal Health

Smiths Medical

The Catheter Market is being reshaped by a convergence of materials science, digital sensing, and manufacturing automation that deliver measurable clinical and operational benefits. Antimicrobial and hydrophilic surface treatments are now integrated into more than 58% of new product launches, producing reported reductions in catheter-associated infection events of 28–35% and lowering device-related readmission rates in acute-care settings. Sensor integration—pressure, flow, and position—has moved from pilot stages to scaled deployments: roughly 47% of tertiary hospitals report active use of sensor-enabled catheters for intra-procedural monitoring, yielding a 22–30% decrease in repositioning events and a 15–20% faster time-to-stable-placement in complex interventions. Emerging digital technologies amplify these gains. AI-assisted navigation and image-fusion platforms are being embedded into catheter guidance workflows, improving first-pass success rates by an estimated 18–25% in interventional procedures. Real-time telemetry and cloud-connected analytics enable predictive maintenance of catheter delivery systems and reduce procedural delays; hospitals implementing connected-catheter analytics report average workflow uptime improvements near 12%. Additive manufacturing (3D printing) of micro-catheter components and patient-specific introducers has enabled reduction in lead times by up to 40% for specialized devices and supports rapid prototyping cycles that shorten product iteration timelines.

Materials innovation continues: next-generation biocompatible polymers demonstrate up to 30% improvement in tensile strength and a 20% reduction in friction coefficients versus legacy materials, improving patient comfort and device longevity. Bioresorbable and drug-eluting catheter variants are advancing into broader clinical use, with device dwell-time profiles engineered to reduce systemic exposure and lower complication rates by mid-to-high single digits in controlled deployments. On the production side, automation and localized manufacturing are increasing capacity: automated assembly has scaled output by 18–25% in high-volume lines, while regionalized production has raised in-region supply shares to over 40% in Asia-Pacific. Regulatory engineering and digitized submission pathways are speeding validation cycles for complex, data-enabled devices, and interoperability standards are emerging to ensure catheters integrate with hospital EHRs and imaging systems, supporting enterprise-level adoption and lifecycle management.

In September 2024, Becton, Dickinson and Company (BD) completed a USD 4.2 billion acquisition of the Critical Care product group from Edwards Lifesciences, expanding BD’s portfolio to include advanced pulmonary artery catheters and enhancing smart, connected care solutions within its catheter offerings.

In October 2024, Boston Scientific Corporation received FDA approval for its FARAWAVE NAV Ablation Catheter, designed for paroxysmal atrial fibrillation treatment, and secured 510(k) clearance for supporting navigation software to improve procedural precision and integration during catheter ablation procedures.

In 2024, Medtronic plc launched the Harmony™ Spiral Wave™ Reusable Urinary Catheter System featuring enhanced infection prevention and reduced environmental impact compared to single-use alternatives, marking a significant product innovation in urinary catheter solutions.

In August 2024, Teleflex Incorporated introduced an upgraded version of its no-touch catheter technology, reporting a 50% rise in adoption among spinal cord injury patient care settings and reinforcing clinical preference for enhanced grip and lubricity in long-term catheter use.

The Catheter Market Report encompasses a comprehensive review of global product types, clinical applications, end-user segments, regional landscapes, and emerging technologies that shape the catheter industry. Coverage includes in-depth analysis of catheter categories such as cardiovascular, urinary, intravenous, neurovascular, and specialty interventional devices, detailing design innovations, material differentiation, and usage patterns across clinical settings. Segmentation by application explores use cases in cardiology, urology, critical care, oncology, and minimally invasive procedures, noting procedural requirements, clinical outcomes, and deployment environments such as hospitals, ambulatory surgical centers, dialysis clinics, and home healthcare.

Regional focus extends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with comparative insights into adoption dynamics, healthcare infrastructure maturity, regulatory ecosystems, and localized technology integration. The report identifies advanced technologies such as antimicrobial and hydrophilic coatings, sensor and IoT-enabled catheters, real-time monitoring systems, and AI-assisted navigation tools, providing measurable data on integration rates, clinical performance improvements, and user adoption trends. It also explores manufacturing advances including automation, localized production hubs, and material science improvements that reduce friction, enhance biocompatibility, and extend catheter durability.

Industry focus areas include strategic initiatives by leading manufacturers, competitive positioning, innovation pipelines, partnership activities, quality and compliance frameworks, and market entry strategies for emerging players. Niche segments such as smart catheters with embedded analytics, bioresorbable systems, and ergonomic designs for specific patient populations are highlighted, along with adoption behavior variations among end-users. The Catheter Market Report aims to equip decision-makers with actionable insights, quantitative benchmarks, and qualitative analysis to inform procurement, investment, technology development, and strategic planning in the evolving catheter landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 50967.84 Million |

|

Market Revenue in 2032 |

USD 92949.34 Million |

|

CAGR (2025 - 2032) |

7.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Becton, Dickinson and Company (BD), Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, Teleflex Incorporated, B. Braun Melsungen AG, Cook Medical, Terumo Corporation, Cardinal Health, Smiths Medical |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |

The United States holds a leading position in the global catheter landscape, supported by advanced domestic manufacturing and sustained healthcare investment. The country hosts more than 6,500 FDA-registered medical device manufacturing facilities, with annual medical device production exceeding USD 190 billion. Catheters are extensively deployed across cardiology, neurointervention, dialysis, and urinary care, supported by hospital adoption rates above 70% for advanced catheter systems. Public and private healthcare spending surpasses USD 4.5 trillion annually, enabling rapid uptake of technologies such as antimicrobial-coated catheters, sensor-enabled monitoring devices, and image-guided catheter platforms used in high-volume clinical settings.

Market Size & Growth: Valued at USD 50967.84 Million in 2024, projected to reach USD 92949.34 Million by 2032 at a CAGR of 7.8%, driven by increased procedural demand and chronic disease management.

Top Growth Drivers: Cardiovascular catheter utilization increased by 38%, infection-prevention catheter adoption rose by 29%, and procedural efficiency improved by 22%.

Short-Term Forecast: By 2028, healthcare providers are expected to achieve up to 18% reduction in catheter-related complications through advanced materials and monitoring systems.

Emerging Technologies: Smart sensor-enabled catheters, antimicrobial and hydrophilic surface coatings, and bioresorbable catheter materials.

Regional Leaders: North America projected to reach USD 34 Billion by 2032 with high technology penetration, Europe USD 27 Billion driven by aging populations, and Asia-Pacific USD 22 Billion supported by hospital infrastructure expansion.

Consumer/End-User Trends: Hospitals and ambulatory surgical centers represent over 65% of demand, with home healthcare catheter usage increasing steadily.

Pilot or Case Example: A 2024 U.S.-based hospital pilot program achieved a 31% reduction in catheter-associated infection rates using antimicrobial catheter solutions.

Competitive Landscape: The leading company holds approximately 18% share, followed by BD, Medtronic, Abbott, Teleflex, and Boston Scientific.

Regulatory & ESG Impact: Stricter infection control standards and sustainability-focused material regulations are accelerating adoption of advanced catheter designs.

Investment & Funding Patterns: Recent global investments exceeded USD 6.5 Billion, focused on R&D, automation, and next-generation catheter platforms.

Innovation & Future Outlook: AI-assisted navigation, real-time performance monitoring, and personalized catheter solutions are shaping long-term market evolution.

The catheter market supports major healthcare sectors including cardiovascular intervention, urology, neurovascular procedures, and intensive care, with cardiovascular applications contributing approximately 40% of overall demand. Ongoing product innovations such as pressure-sensing catheters, antimicrobial coatings, and minimally invasive delivery systems are enhancing patient safety and procedural outcomes. Regulatory emphasis on infection reduction, combined with economic investment in healthcare infrastructure, continues to influence purchasing decisions. While North America and Europe remain high-consumption regions, Asia-Pacific is witnessing accelerated growth due to expanding access to advanced clinical procedures and modernization of healthcare facilities.

The Catheter Market holds strong strategic relevance within global healthcare systems due to its direct integration into high-frequency, life-sustaining procedures across cardiovascular, urology, neurovascular, oncology, and critical care settings. From a strategic perspective, healthcare providers increasingly view catheter innovation as a pathway to improve clinical efficiency, reduce complications, and align with value-based care models. Advanced antimicrobial-coated catheters deliver up to 32% infection reduction compared to conventional uncoated catheters, translating into measurable decreases in hospital-acquired infection burden and length of stay. Regionally, Asia-Pacific dominates in procedure volume due to expanding hospital infrastructure, while North America leads in advanced catheter adoption with over 68% of hospitals using next-generation or sensor-enabled catheter systems. By 2027, AI-assisted catheter navigation and real-time pressure monitoring are expected to improve procedural accuracy and reduce repositioning errors by approximately 25%. From a compliance and ESG standpoint, manufacturers are committing to sustainability targets such as 30% recyclable polymer usage and 20% waste reduction by 2030, responding to tightening medical waste regulations. In 2024, a U.S.-based healthcare network achieved a 29% reduction in catheter-related complications through deployment of smart catheter tracking and analytics platforms. Looking forward, the Catheter Market is positioned as a pillar of clinical resilience, regulatory compliance, and sustainable healthcare delivery, supporting long-term system efficiency and patient safety.

The increasing preference for minimally invasive procedures is a primary driver of the Catheter Market. Procedures such as angioplasty, electrophysiology studies, dialysis access, and interventional radiology rely heavily on catheter-based delivery systems. Globally, minimally invasive cardiovascular procedures have increased by more than 35% over the past five years, significantly expanding catheter utilization per patient episode. These procedures reduce recovery time by up to 40% compared to open surgery, encouraging higher adoption across hospitals and ambulatory surgical centers. Additionally, aging populations and higher prevalence of diabetes, cardiovascular disease, and renal disorders are increasing catheter-dependent interventions. Hospitals are standardizing catheter usage protocols to improve procedural consistency and patient outcomes, further reinforcing sustained demand across both acute and chronic care settings.

Despite technological advances, catheter-associated complications remain a critical restraint for the Catheter Market. Catheter-associated urinary tract infections and bloodstream infections account for a significant proportion of hospital-acquired infections, increasing treatment costs and regulatory scrutiny. Compliance with stringent sterilization, labeling, and post-market surveillance requirements adds operational complexity for manufacturers and healthcare providers. In some regions, mandatory reporting and penalty frameworks have increased liability exposure, slowing procurement cycles. Additionally, hospitals face rising costs related to staff training, infection monitoring, and product validation. These factors collectively constrain rapid adoption of new catheter technologies, particularly in cost-sensitive healthcare systems.

Smart and connected catheter technologies represent a major opportunity for the Catheter Market. Integration of sensors for pressure, flow, and position tracking enables real-time monitoring, reducing procedural errors and improving clinical decision-making. Hospitals adopting smart catheter systems have reported up to 27% improvement in procedural efficiency and faster response to complications. These technologies also support data-driven care pathways and interoperability with electronic health records, aligning with digital health strategies. Emerging markets present additional opportunity as healthcare systems leapfrog directly to advanced catheter platforms while expanding procedural capacity. As reimbursement models increasingly reward outcomes, smart catheter solutions offer strong differentiation potential for manufacturers and providers alike.

Cost containment and regulatory variation pose persistent challenges for the Catheter Market. Medical-grade polymers, coatings, and sensor components are subject to price volatility, increasing production costs. At the same time, regulatory requirements differ significantly across regions, requiring multiple certification pathways and extending time-to-market. Smaller manufacturers face barriers in scaling compliance infrastructure, while hospitals in developing regions struggle with affordability of advanced catheter systems. Additionally, reimbursement inconsistencies for catheter-based procedures limit purchasing flexibility in some healthcare systems. These challenges necessitate strategic balance between innovation, pricing discipline, and regulatory alignment to sustain long-term market stability.

Accelerated Adoption of Antimicrobial and Infection-Prevention Catheters: Hospitals are increasingly prioritizing catheters with antimicrobial coatings and advanced surface treatments to reduce hospital-acquired infections. Clinical deployment data indicate up to 35% reduction in catheter-associated infections compared to standard catheters, while over 60% of tertiary-care hospitals have integrated antimicrobial variants into routine protocols, particularly in intensive care and urology departments.

Expansion of Smart and Sensor-Integrated Catheter Technologies: Smart catheters embedded with pressure, flow, or position sensors are gaining traction due to measurable improvements in procedural accuracy. Healthcare providers report up to 28% reduction in catheter repositioning events and a 22% improvement in real-time clinical decision-making. Adoption rates exceed 45% among large hospitals in North America and parts of Europe, driven by digital health integration strategies.

Shift Toward Single-Use and Disposable Catheter Systems: Infection control policies and regulatory pressure are accelerating the transition toward single-use catheters. Disposable catheter utilization has increased by approximately 40% over the past few years, with facilities reporting up to 25% lower sterilization-related operational burden. This trend is particularly strong in outpatient and ambulatory surgical centers, where procedural throughput has improved by nearly 18%.

Growing Use of Advanced Polymer and Biocompatible Materials: Manufacturers are increasingly deploying next-generation polymers to improve flexibility, durability, and patient comfort. Advanced material catheters demonstrate up to 30% higher tensile performance and a 20% reduction in patient-reported discomfort during long-duration use. More than 50% of newly launched catheter products now incorporate enhanced biocompatible materials, reflecting a clear shift toward performance-driven design innovation.

The Catheter Market is segmented by type, application, and end-user, each reflecting distinct clinical priorities, adoption patterns, and technology requirements. Product type segmentation highlights a strong preference for catheters designed for high-frequency and high-risk procedures, where safety, precision, and material performance are critical. Application-wise, cardiovascular and urology procedures dominate due to procedure volume intensity and long-term disease prevalence, while emerging applications in neurovascular and oncology care are gaining traction. End-user segmentation shows hospitals as the primary demand center, driven by acute care needs and complex interventions, while ambulatory and home-care settings are expanding steadily due to procedural decentralization. Together, these segments illustrate a market shaped by procedural intensity, infection control priorities, and shifting care delivery models.

The Catheter Market by type includes cardiovascular catheters, urinary catheters, intravenous catheters, neurovascular catheters, and specialty catheters used in oncology and dialysis. Cardiovascular catheters represent the leading type, accounting for approximately 41% of overall adoption, supported by high procedural frequency in angiography, angioplasty, and electrophysiology studies. Urinary catheters hold around 27% adoption, reflecting widespread use across acute and long-term care settings. However, neurovascular catheters are the fastest-growing type, expanding at an estimated 9.4% CAGR, driven by rising stroke interventions and growth in minimally invasive neurointerventional procedures. Intravenous and specialty catheters together contribute a combined 32% share, serving critical niches such as chemotherapy delivery, dialysis access, and intensive care monitoring.

By application, cardiovascular procedures dominate the Catheter Market, accounting for approximately 39% of total usage due to the high prevalence of heart disease and routine interventional workflows. Urology applications follow with about 26% adoption, supported by chronic urinary disorders and post-surgical care requirements. Neurovascular applications currently represent 18%, but this segment is growing fastest at an estimated 10.1% CAGR as stroke incidence rises and mechanical thrombectomy adoption expands globally. Oncology, dialysis, and critical care applications collectively contribute the remaining 17%, serving specialized but essential clinical needs.

Hospitals are the leading end-user segment in the Catheter Market, accounting for approximately 64% of total demand, driven by high-acuity care, surgical interventions, and intensive care unit utilization. Ambulatory surgical centers hold around 21% adoption, benefiting from shorter procedure cycles and increasing outpatient interventions. Home healthcare and long-term care facilities together represent 15%, but this segment is expanding fastest at an estimated 8.7% CAGR due to aging populations and chronic disease management outside hospital settings. Adoption rates of catheter-based therapies in ambulatory centers exceed 45% for same-day cardiovascular and urology procedures, highlighting shifting care delivery models.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

The Catheter Market shows clear regional differentiation driven by healthcare infrastructure maturity, procedural volumes, regulatory intensity, and technology adoption levels. North America leads due to high interventional procedure density, with more than 75 catheter-based procedures per 1,000 population annually. Europe follows with approximately 29% share, supported by strong public healthcare systems and regulatory harmonization. Asia-Pacific accounts for nearly 24% of global demand, underpinned by rapid hospital expansion, increasing chronic disease burden, and rising access to minimally invasive care. South America and the Middle East & Africa together represent around 9%, reflecting developing healthcare infrastructure but steady improvements in procedural access, imports, and localized manufacturing capabilities.

How is advanced clinical infrastructure accelerating adoption of next-generation catheter solutions?

The region holds approximately 38% of the global Catheter Market, supported by high utilization across cardiovascular, neurovascular, dialysis, and critical care applications. Hospitals and integrated delivery networks are the primary demand drivers, accounting for over 70% of catheter consumption. Regulatory frameworks emphasize patient safety and infection reduction, accelerating uptake of antimicrobial and smart catheter systems. Digital transformation initiatives have driven adoption of sensor-enabled catheters, with over 65% of tertiary hospitals using advanced monitoring solutions. A major regional manufacturer expanded production of antimicrobial-coated catheters in 2024, increasing annual output capacity by 18%. Consumer behavior reflects strong preference for clinically validated, premium catheter products, with higher adoption across large hospital systems and specialized care centers.

Why are regulatory alignment and sustainability priorities reshaping purchasing behavior?

Europe represents roughly 29% of the Catheter Market, with Germany, the UK, and France together contributing over 60% of regional demand. Strong regulatory oversight and standardized procurement frameworks drive consistent demand for compliant, high-quality catheter products. Sustainability initiatives emphasize recyclable materials and waste reduction, influencing supplier selection across public healthcare systems. Adoption of advanced catheter technologies is rising, with nearly 48% of hospitals integrating improved coating and biocompatible material solutions. A leading European medical device company introduced recyclable polymer-based catheter lines, reducing packaging waste by 25%. Consumer behavior shows preference for traceable, regulation-aligned catheter products that meet stringent safety and environmental expectations.

How are scale, localization, and access expansion transforming procedural demand?

Asia-Pacific ranks as the fastest-expanding regional market, contributing approximately 24% of global catheter volume. China, India, and Japan collectively account for over 70% of regional consumption due to large patient populations and expanding hospital capacity. Manufacturing localization is increasing, with more than 40% of catheters now produced within the region. Innovation hubs in Japan and South Korea are advancing micro-catheter and flexible polymer technologies. In 2024, a regional manufacturer scaled production by 22% to meet domestic cardiovascular procedure demand. Consumer behavior reflects cost sensitivity combined with growing acceptance of advanced catheter systems in urban hospitals.

What role do healthcare modernization and trade policy play in steady market expansion?

South America holds close to 6% of the global Catheter Market, led by Brazil and Argentina, which together represent over 65% of regional demand. Healthcare infrastructure investment and import facilitation policies are improving access to advanced catheter products. Public hospital upgrades and private sector expansion support consistent procedural growth. A Brazilian medical device supplier increased catheter distribution coverage to over 1,200 hospitals, improving regional availability. Consumer behavior varies widely, with private hospitals adopting higher-end catheter technologies while public facilities prioritize cost-efficient solutions.

How are modernization initiatives and regional hubs shaping demand growth?

The Middle East & Africa region accounts for approximately 3% of global catheter demand, with the UAE, Saudi Arabia, and South Africa driving adoption. Healthcare modernization programs and international partnerships are expanding access to catheter-based procedures. Advanced tertiary hospitals account for nearly 55% of regional catheter usage. Regulatory alignment with international standards is improving import efficiency and product availability. A UAE-based healthcare group expanded interventional cardiology services in 2024, increasing catheter utilization by 20%. Consumer behavior reflects concentrated demand in urban centers and medical tourism hubs.

United States Catheter Market – 32% share: Dominance driven by high procedure volumes, strong manufacturing capacity, and rapid adoption of advanced catheter technologies.

Germany Catheter Market – 11% share: Leadership supported by robust medical device production, standardized healthcare procurement, and strong hospital demand for compliant catheter systems.

The Catheter Market operates within a moderately consolidated yet competitive environment, characterized by the presence of more than 40 active global and regional manufacturers competing across product categories and clinical applications. The top five companies collectively account for approximately 55% of total market presence, indicating a semi-consolidated structure where scale, regulatory capability, and innovation depth determine competitive positioning. Leading players focus heavily on product differentiation through antimicrobial coatings, smart catheter integration, and enhanced biocompatible materials, with over 60% of major competitors maintaining active R&D pipelines. Strategic initiatives remain central to competition, including cross-border manufacturing expansions, hospital network partnerships, and targeted acquisitions to strengthen portfolios in cardiovascular, neurovascular, and urology segments. Product launch intensity has increased, with an estimated 25% rise in next-generation catheter introductions over the past three years. Additionally, over 45% of leading companies have entered digital or data-enabled catheter collaborations to support real-time monitoring and procedural optimization. Competitive pressure is further intensified by regulatory compliance demands, as firms with faster approval cycles and scalable quality systems gain procurement advantages, particularly in North America and Europe.

Becton, Dickinson and Company (BD)

Medtronic plc

Abbott Laboratories

Boston Scientific Corporation

Teleflex Incorporated

B. Braun Melsungen AG

Cook Medical

Terumo Corporation

Cardinal Health

Smiths Medical

The Catheter Market is being reshaped by a convergence of materials science, digital sensing, and manufacturing automation that deliver measurable clinical and operational benefits. Antimicrobial and hydrophilic surface treatments are now integrated into more than 58% of new product launches, producing reported reductions in catheter-associated infection events of 28–35% and lowering device-related readmission rates in acute-care settings. Sensor integration—pressure, flow, and position—has moved from pilot stages to scaled deployments: roughly 47% of tertiary hospitals report active use of sensor-enabled catheters for intra-procedural monitoring, yielding a 22–30% decrease in repositioning events and a 15–20% faster time-to-stable-placement in complex interventions. Emerging digital technologies amplify these gains. AI-assisted navigation and image-fusion platforms are being embedded into catheter guidance workflows, improving first-pass success rates by an estimated 18–25% in interventional procedures. Real-time telemetry and cloud-connected analytics enable predictive maintenance of catheter delivery systems and reduce procedural delays; hospitals implementing connected-catheter analytics report average workflow uptime improvements near 12%. Additive manufacturing (3D printing) of micro-catheter components and patient-specific introducers has enabled reduction in lead times by up to 40% for specialized devices and supports rapid prototyping cycles that shorten product iteration timelines.

Materials innovation continues: next-generation biocompatible polymers demonstrate up to 30% improvement in tensile strength and a 20% reduction in friction coefficients versus legacy materials, improving patient comfort and device longevity. Bioresorbable and drug-eluting catheter variants are advancing into broader clinical use, with device dwell-time profiles engineered to reduce systemic exposure and lower complication rates by mid-to-high single digits in controlled deployments. On the production side, automation and localized manufacturing are increasing capacity: automated assembly has scaled output by 18–25% in high-volume lines, while regionalized production has raised in-region supply shares to over 40% in Asia-Pacific. Regulatory engineering and digitized submission pathways are speeding validation cycles for complex, data-enabled devices, and interoperability standards are emerging to ensure catheters integrate with hospital EHRs and imaging systems, supporting enterprise-level adoption and lifecycle management.

In September 2024, Becton, Dickinson and Company (BD) completed a USD 4.2 billion acquisition of the Critical Care product group from Edwards Lifesciences, expanding BD’s portfolio to include advanced pulmonary artery catheters and enhancing smart, connected care solutions within its catheter offerings.

In October 2024, Boston Scientific Corporation received FDA approval for its FARAWAVE NAV Ablation Catheter, designed for paroxysmal atrial fibrillation treatment, and secured 510(k) clearance for supporting navigation software to improve procedural precision and integration during catheter ablation procedures.

In 2024, Medtronic plc launched the Harmony™ Spiral Wave™ Reusable Urinary Catheter System featuring enhanced infection prevention and reduced environmental impact compared to single-use alternatives, marking a significant product innovation in urinary catheter solutions.

In August 2024, Teleflex Incorporated introduced an upgraded version of its no-touch catheter technology, reporting a 50% rise in adoption among spinal cord injury patient care settings and reinforcing clinical preference for enhanced grip and lubricity in long-term catheter use.

The Catheter Market Report encompasses a comprehensive review of global product types, clinical applications, end-user segments, regional landscapes, and emerging technologies that shape the catheter industry. Coverage includes in-depth analysis of catheter categories such as cardiovascular, urinary, intravenous, neurovascular, and specialty interventional devices, detailing design innovations, material differentiation, and usage patterns across clinical settings. Segmentation by application explores use cases in cardiology, urology, critical care, oncology, and minimally invasive procedures, noting procedural requirements, clinical outcomes, and deployment environments such as hospitals, ambulatory surgical centers, dialysis clinics, and home healthcare.

Regional focus extends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with comparative insights into adoption dynamics, healthcare infrastructure maturity, regulatory ecosystems, and localized technology integration. The report identifies advanced technologies such as antimicrobial and hydrophilic coatings, sensor and IoT-enabled catheters, real-time monitoring systems, and AI-assisted navigation tools, providing measurable data on integration rates, clinical performance improvements, and user adoption trends. It also explores manufacturing advances including automation, localized production hubs, and material science improvements that reduce friction, enhance biocompatibility, and extend catheter durability.

Industry focus areas include strategic initiatives by leading manufacturers, competitive positioning, innovation pipelines, partnership activities, quality and compliance frameworks, and market entry strategies for emerging players. Niche segments such as smart catheters with embedded analytics, bioresorbable systems, and ergonomic designs for specific patient populations are highlighted, along with adoption behavior variations among end-users. The Catheter Market Report aims to equip decision-makers with actionable insights, quantitative benchmarks, and qualitative analysis to inform procurement, investment, technology development, and strategic planning in the evolving catheter landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 50967.84 Million |

|

Market Revenue in 2032 |

USD 92949.34 Million |

|

CAGR (2025 - 2032) |

7.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Becton, Dickinson and Company (BD), Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, Teleflex Incorporated, B. Braun Melsungen AG, Cook Medical, Terumo Corporation, Cardinal Health, Smiths Medical |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |