Reports

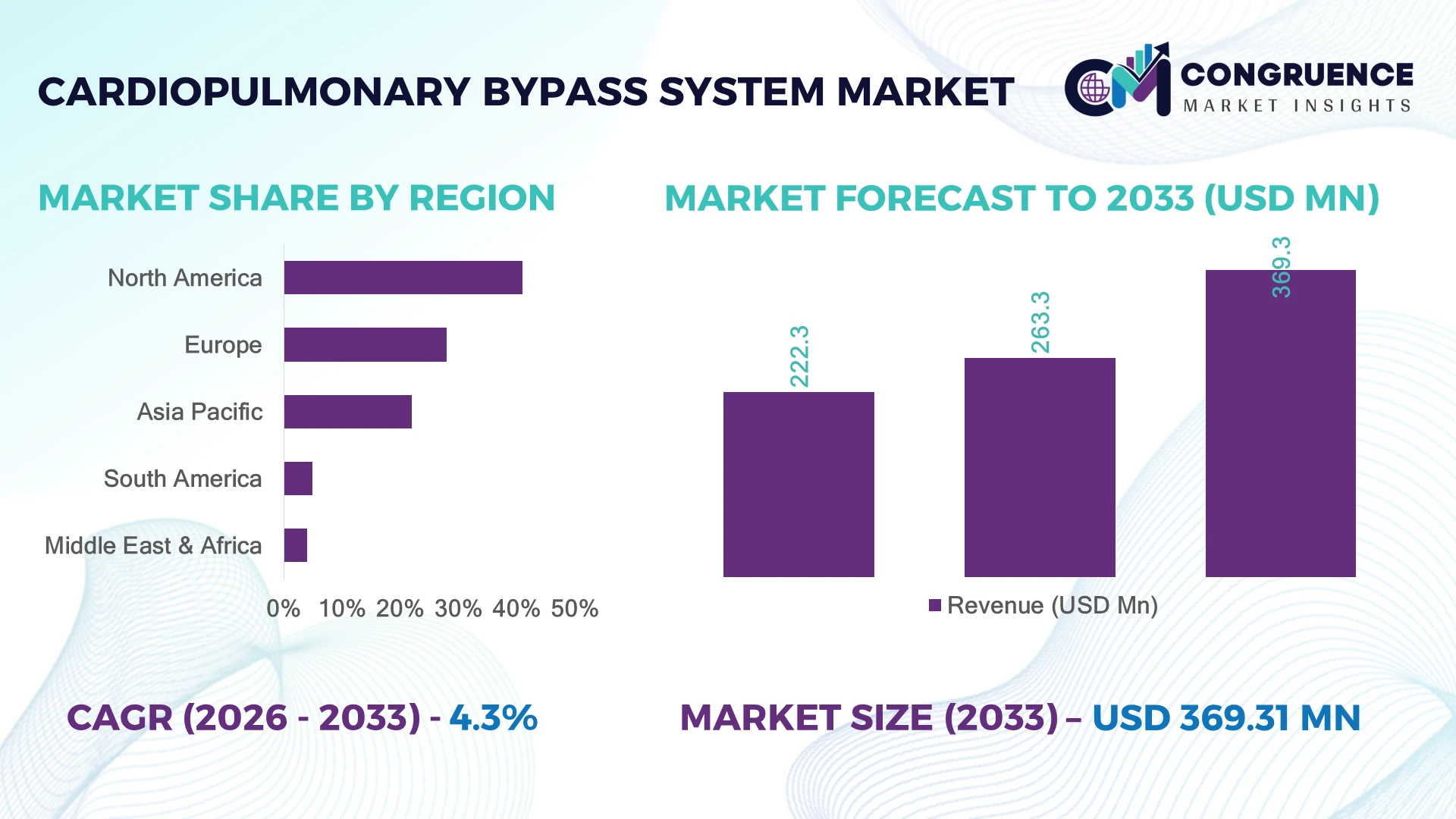

The Global Cardiopulmonary Bypass System Market was valued at USD 263.3 Million in 2025 and is anticipated to reach a value of USD 369.3 Million by 2033 expanding at a CAGR of 4.32% between 2026 and 2033. Rising cardiac surgery volumes, wider adoption of minimally invasive cardiovascular procedures, and continuous advances in oxygenators, perfusion monitoring, and patient safety technologies are accelerating global market expansion.

The United States dominates the global Cardiopulmonary Bypass System Market with approximately 39% market share, supported by advanced cardiac care networks, over 1,000 specialized heart centers, and sustained investments in cardiovascular innovation. Compared with Japan, which maintains one of the world's highest procedure rates per capita due to an aging population, the U.S. benefits from broader technology integration and hospital procurement capacity. The continued modernization of cardiac surgery infrastructure strengthens supplier positioning and long-term procurement strategies across high-value healthcare markets.

Strategic implication: Manufacturers focusing on advanced perfusion technologies, hospital partnerships, and clinical workflow optimization will strengthen competitive positioning in mature and expanding surgical markets.

Market Size & Growth: USD 263.3 Million in 2025 is projected to reach USD 369.3 Million by 2033 at 4.32% CAGR, driven by increasing adoption of advanced perfusion monitoring and cardiac surgery modernization.

Top Growth Drivers: Cardiac surgery volume +9%, elderly patient pool +7%, advanced perfusion technology adoption +12%.

Short-Term Forecast: By 2028, integrated perfusion workflows improve operating efficiency by nearly 15% while reducing setup time by approximately 10%.

Emerging Technologies: AI-assisted perfusion monitoring, smart oxygenators, real-time hemodynamic analytics, and automated safety alarms enhance surgical precision.

Regional Leaders: North America (~USD 145 Million), Europe (~USD 96 Million), and Asia-Pacific (~USD 79 Million) lead through digital operating rooms, hospital upgrades, and expanding cardiac centers.

Consumer/End-User Trends: More than 68% of tertiary cardiac hospitals prioritize integrated heart-lung systems with advanced monitoring capabilities.

Pilot/Case Example: In 2024, digital perfusion implementation at leading cardiac centers reduced perfusion-related workflow variation by approximately 18%.

Competitive Landscape: LivaNova holds roughly 24% market share alongside Medtronic, Terumo Corporation, Getinge, and Xenios AG amid global manufacturing expansion.

Regulatory & ESG Impact: Enhanced device safety standards and quality compliance improved clinical traceability by nearly 20% across advanced healthcare systems.

Investment & Funding: More than USD 450 Million has supported cardiovascular technology expansion through strategic partnerships, manufacturing upgrades, and hospital modernization.

Innovation & Future Outlook: Next-generation minimally invasive perfusion platforms, digital connectivity, and intelligent monitoring strengthen global surgical efficiency and competitive differentiation.

Cardiopulmonary bypass systems remain essential across complex cardiac procedures, with demand increasing in adult, pediatric, and minimally invasive heart surgery programs. Manufacturers continue introducing intelligent monitoring platforms, compact oxygenators, and digitally connected perfusion systems that improve clinical workflow. More than 35% of newly installed systems now feature advanced data integration capabilities, while evolving medical device compliance requirements continue influencing product development and hospital procurement strategies, setting the stage for broader strategic market evolution.

The Cardiopulmonary Bypass System Market has become strategically important as healthcare providers expand advanced cardiac surgery capacity while prioritizing patient safety, procedural consistency, and operating room efficiency. Hospital infrastructure modernization, digital operating room integration, and stronger medical device quality regulations are reshaping procurement priorities. Companies increasingly compete through intelligent monitoring capabilities, clinical interoperability, and comprehensive service support rather than hardware performance alone.

Modern perfusion platforms equipped with automated monitoring and digital data management reduce manual workflow steps by approximately 20% compared with conventional standalone systems while improving intraoperative decision support. North America continues leading large-scale deployment through established cardiovascular centers, whereas Asia-Pacific records faster adoption as new specialty hospitals and surgical facilities expand. Over the next two to three years, integrated perfusion information systems are expected to become standard across high-volume cardiac surgery programs.

Healthcare providers are increasingly deploying connected cardiopulmonary bypass platforms that integrate directly with hospital information systems, reducing documentation time and improving procedural standardization. Manufacturers are expanding regional production, strengthening distributor partnerships, and investing in clinician training to support wider adoption. Organizations that combine technological innovation with strong clinical support and supply resilience will secure lasting competitive advantages in the evolving global cardiovascular care ecosystem.

Increasing cardiovascular disease prevalence and the expansion of complex cardiac procedures are strengthening demand for advanced cardiopulmonary bypass systems. More than 70% of open-heart surgeries continue to require extracorporeal circulation, while adoption of integrated perfusion monitoring platforms has increased by nearly 18% across leading cardiac hospitals. In the United States, updated hospital infrastructure and stricter patient safety protocols are accelerating replacement of aging heart-lung machines with digitally connected systems. This transition improves procedural consistency, reduces manual intervention, and enhances clinical decision-making. Manufacturers are responding through product innovation, software-enabled perfusion platforms, and strategic collaborations with hospital networks to improve interoperability and strengthen long-term service contracts. The combination of digital integration and clinical standardization is becoming a decisive competitive differentiator.

The market continues to face structural pressure from high equipment acquisition costs, lengthy certification processes, and dependence on specialized clinical infrastructure. Nearly 45% of hospitals in developing healthcare systems postpone advanced perfusion equipment procurement due to budget limitations, while regulatory approval timelines can extend product commercialization by 12–18 months. Dependence on precision components and medical-grade polymers also exposes manufacturers to supply-chain disruptions, particularly during periods of logistics instability. These factors slow installation cycles and increase operational costs for healthcare providers. Companies are mitigating risks through localized manufacturing, multi-source component procurement, and long-term supplier agreements while simplifying product platforms to reduce maintenance complexity and improve procurement flexibility across cost-sensitive healthcare systems.

The integration of artificial intelligence, predictive analytics, and cloud-connected perfusion management is creating new opportunities beyond conventional heart-lung support. More than 40% of newly introduced premium systems incorporate advanced digital monitoring, while automated perfusion documentation can reduce clinician administrative workload by approximately 25%. Japan is accelerating digital operating room adoption through hospital modernization initiatives that encourage connected surgical technologies. Manufacturers are investing in intelligent software ecosystems, remote diagnostics, and data-driven clinical support to improve procedural efficiency and equipment lifecycle management. An emerging opportunity lies in subscription-based software upgrades and predictive maintenance services, enabling vendors to establish recurring customer engagement while helping hospitals optimize equipment utilization and clinical performance.

Successful deployment increasingly depends on highly trained perfusionists, seamless interoperability, and standardized digital infrastructure rather than equipment availability alone. Approximately 30% of healthcare facilities report shortages of experienced perfusion professionals, while integration of connected operating room technologies can require 20% longer implementation timelines than conventional standalone systems. In Germany, hospitals expanding digital surgical workflows must ensure compatibility between perfusion devices, anesthesia systems, and electronic medical records without disrupting clinical operations. Failure to achieve seamless integration affects procedural consistency, cybersecurity readiness, and long-term operational efficiency. Companies must strengthen clinician training programs, cybersecurity investment, and interoperability partnerships while developing intuitive software architectures that simplify implementation and accelerate adoption across diverse hospital environments.

Digital Perfusion Workflow Integration: Cardiac hospitals are increasingly integrating cardiopulmonary bypass systems with electronic health records and surgical analytics platforms, with nearly 42% of newly installed systems supporting digital connectivity and approximately 18% faster clinical documentation. Updated medical device traceability requirements in the United States are accelerating adoption. Manufacturers are expanding software capabilities, strengthening interoperability partnerships, and offering lifecycle support contracts to improve workflow efficiency and equipment utilization.

Compact System Design Evolution: Demand is shifting toward compact heart-lung machines and modular perfusion platforms that reduce operating room footprint by nearly 20% while lowering setup time by approximately 15%. High-volume cardiac centers in Japan are adopting space-efficient systems to optimize procedural throughput. Suppliers are redesigning product architectures with modular components, improving transportability, simplifying maintenance, and enabling faster deployment across diverse surgical environments.

Supply Chain Localization Strategies: Medical device manufacturers are restructuring sourcing networks after recent logistics disruptions, with over 35% increasing regional component procurement and inventory buffers improving delivery consistency by nearly 22%. European regulatory compliance and geopolitical supply uncertainty have accelerated localized manufacturing initiatives. Companies are expanding supplier ecosystems, qualifying multiple component vendors, and strengthening regional assembly operations to enhance production resilience and shorten lead times.

Advanced Clinical Monitoring Expansion: Intelligent perfusion monitoring with predictive alerts and automated data capture is becoming standard in premium systems, improving intraoperative parameter visibility by approximately 25% and reducing manual monitoring tasks by nearly 17%. A non-obvious shift is the growing use of procedure data for hospital quality benchmarking rather than solely patient monitoring. Manufacturers are investing in AI-enabled analytics, clinician training, and cloud-based performance platforms to strengthen long-term customer engagement.

Heart-Lung Machines remain the leading segment, accounting for nearly 36% of overall demand due to their central role in maintaining circulation and oxygenation during complex cardiac procedures. Their reliability, integration with advanced monitoring platforms, and compatibility with modern operating room workflows make them indispensable in high-volume hospitals. Oxygenators represent the fastest-growing segment as healthcare providers increasingly adopt biocompatible membrane technologies that improve gas exchange efficiency and reduce inflammatory response. Manufacturers continue enhancing oxygenator performance through material innovation and improved flow dynamics, supporting safer long-duration procedures. Cannulas, perfusion pumps, arterial filters, tubing sets, and accessories collectively strengthen the ecosystem by improving procedural safety, infection control, and operational flexibility. Perfusion pumps equipped with digital control modules are gaining traction, with adoption increasing by nearly 16%, while integrated tubing systems have reduced setup complexity by approximately 14%. Companies are expanding comprehensive product portfolios, investing in compatible system architectures, and forming clinical partnerships to deliver complete perfusion solutions rather than standalone components, reflecting shifting procurement priorities toward integrated surgical platforms.

Coronary Artery Bypass Grafting (CABG) remains the dominant application, representing approximately 48% of cardiopulmonary bypass procedures because of the continued global burden of coronary artery disease and the need for dependable extracorporeal circulation during complex bypass operations. Heart Valve Surgery follows as a mature segment supported by increasing treatment of degenerative valve disorders. Congenital Heart Defect Repair is the fastest-growing application as improvements in pediatric cardiac care and earlier diagnosis expand surgical intervention across specialized healthcare facilities. Lung transplantation and other complex cardiac surgeries continue generating specialized demand for advanced perfusion technologies capable of supporting extended procedures and critical physiological management. More than 30% of tertiary cardiac centers have expanded hybrid operating room capabilities, while digital perfusion planning has improved procedural coordination by nearly 18%. Manufacturers are responding through procedure-specific system configurations, advanced oxygenation technologies, and clinician education programs that improve workflow efficiency and broaden application-specific clinical adoption.

Hospitals represent the largest end-user segment, contributing roughly 68% of equipment deployment owing to extensive cardiac surgery infrastructure, multidisciplinary clinical teams, and continuous investment in advanced operating room technologies. Large tertiary hospitals perform the highest procedure volumes and increasingly procure integrated perfusion platforms with long-term service agreements. Cardiac Centers are the fastest-growing end-user group as dedicated cardiovascular facilities expand specialized surgical capacity and adopt next-generation perfusion technologies to improve procedural efficiency and patient outcomes. Ambulatory Surgical Centers remain limited to selected cardiovascular interventions because highly complex open-heart procedures continue requiring comprehensive hospital infrastructure. Specialty Clinics primarily support preoperative evaluation, postoperative follow-up, and referral pathways rather than direct cardiopulmonary bypass deployment. Nearly 41% of advanced cardiac centers have upgraded digital perfusion infrastructure over the past two years, while integrated service contracts have increased by approximately 20%. Manufacturers are tailoring pricing models, expanding clinical training programs, and strengthening partnerships with specialized cardiac institutions to reinforce customer retention and accelerate technology adoption.

North America accounted for the largest market share at 41.0% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.61% between 2026 and 2033.

North America remains the largest market due to its dense concentration of tertiary cardiac hospitals, established reimbursement systems, and rapid replacement of legacy perfusion equipment with digitally integrated platforms. The region contributes approximately 41% of global demand, supported by widespread adoption of minimally invasive cardiac procedures and advanced operating room technologies. More than 75% of high-volume cardiac centers have incorporated digital perfusion monitoring into routine surgical workflows, improving procedural standardization and patient safety. Manufacturers continue expanding clinical service capabilities, software integration, and long-term maintenance partnerships while strengthening domestic supply resilience through regional production and distribution networks.

United States Market Outlook: The United States leads the regional market through its extensive cardiovascular care infrastructure, strong medical technology ecosystem, and continuous investment in advanced surgical equipment. More than 1,000 specialized cardiac centers perform high volumes of open-heart procedures each year, creating sustained demand for next-generation cardiopulmonary bypass systems. Hospitals continue prioritizing integrated perfusion platforms, cybersecurity-enabled connectivity, and clinician training programs, while manufacturers strengthen domestic manufacturing capabilities and expand strategic collaborations with leading healthcare systems to accelerate technology deployment.

Europe maintains a strong market position through advanced cardiac surgery programs, harmonized medical device regulations, and continuous modernization of hospital infrastructure. The region represents nearly 28% of global market activity, supported by widespread adoption of intelligent perfusion systems and integrated operating room technologies. More than 60% of newly procured cardiopulmonary bypass platforms include digital monitoring functionality to enhance procedural traceability and patient safety. Medical device manufacturers continue investing in regional production facilities, regulatory compliance, and clinical partnerships to strengthen product availability while supporting hospitals transitioning toward standardized digital surgical workflows.

Germany Market Outlook: Germany serves as Europe's primary market owing to its highly developed healthcare infrastructure, advanced medical device manufacturing base, and extensive network of specialized cardiac hospitals. Large university hospitals continue replacing conventional perfusion equipment with digitally connected systems that improve operational efficiency and data management. Approximately 30% of leading cardiovascular centers have expanded hybrid operating room capabilities over recent years, encouraging suppliers to increase local technical support, clinician education, and collaborative product development initiatives.

Asia-Pacific is experiencing the fastest market expansion as governments increase investment in advanced cardiovascular care, specialty hospitals, and surgical infrastructure. The region accounts for approximately 22% of global demand while demonstrating the strongest momentum in equipment deployment across emerging healthcare systems. More than 20% of newly commissioned tertiary hospitals now include dedicated cardiac surgery departments equipped with modern perfusion technologies. Manufacturers are expanding localized production, establishing distribution partnerships, and increasing clinical education programs to support growing procedure volumes and improve technology accessibility across rapidly developing healthcare markets.

China Market Outlook: China is strengthening its position through large-scale healthcare infrastructure expansion, domestic medical device manufacturing, and increasing investment in cardiovascular specialty care. Hundreds of tertiary hospitals continue upgrading cardiac surgery capabilities with intelligent operating room technologies and advanced perfusion equipment. Digital hospital initiatives and expanding procurement of domestically manufactured medical devices are encouraging suppliers to localize production, strengthen research collaborations, and accelerate product certification while improving nationwide equipment availability.

South America continues progressing through targeted investment in cardiovascular treatment capacity, modernization of public healthcare institutions, and increasing availability of specialized cardiac services. The region contributes nearly 5% of the global market, with procurement focused primarily on tertiary hospitals and reference cardiac centers. Approximately 18% of major cardiac institutions have upgraded perfusion systems during recent modernization programs, improving procedural efficiency and patient management. Although budget constraints and import dependence remain operational considerations, manufacturers are strengthening distributor partnerships, expanding after-sales services, and improving local technical support to enhance long-term market presence.

Brazil Market Outlook: Brazil represents the largest national market in South America due to its extensive hospital network, growing cardiovascular disease burden, and concentration of specialized cardiac surgery centers. Major metropolitan hospitals continue investing in advanced heart-lung systems and digital operating room technologies while expanding surgeon and perfusionist training. Public-private healthcare partnerships are supporting modernization initiatives, encouraging suppliers to broaden regional distribution networks and improve maintenance capabilities for high-utilization cardiac facilities.

The Middle East & Africa market is advancing through sustained healthcare infrastructure investment, expansion of specialized cardiovascular centers, and modernization of tertiary hospitals. The region accounts for approximately 4% of global demand, with adoption concentrated in countries prioritizing advanced surgical capabilities. More than 15% of newly developed tertiary healthcare projects now include dedicated cardiac surgery facilities equipped with modern perfusion technologies. Manufacturers are strengthening regional distribution partnerships, establishing clinical training programs, and supporting technology transfer initiatives to improve deployment consistency across rapidly evolving healthcare systems.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through extensive hospital expansion programs, strong government healthcare investment, and accelerated adoption of advanced medical technologies under national healthcare transformation initiatives. New cardiovascular centers continue integrating intelligent operating room infrastructure and modern perfusion equipment to support complex cardiac procedures. Growing investment in specialized clinical workforce development and digital healthcare systems is encouraging global manufacturers to establish strategic partnerships, expand technical support capabilities, and reinforce long-term market participation.

The market is led by LivaNova, Terumo Corporation, Medtronic, Xenios AG, and Senko Medical Instrument, with global technology leaders competing against regional manufacturers and cost-focused OEM suppliers. The top five players collectively control approximately 72% of global market activity through integrated cardiopulmonary bypass portfolios and long-term hospital relationships. Competition centers on digital perfusion technology, clinical reliability, and supply resilience rather than pricing alone. Premium systems improve workflow efficiency by nearly 20%, while integrated monitoring reduces manual documentation by approximately 18%, encouraging hospitals to prioritize technology over acquisition cost. Companies are expanding manufacturing capacity, strengthening distributor partnerships, launching intelligent perfusion platforms, and increasing software-enabled service offerings through vertical integration. Competitive momentum is shifting toward digitally connected ecosystems and consumable-driven recurring business, while industry consolidation reinforces established brands. Stringent regulatory approvals, extensive clinical validation, and hospital procurement cycles remain major entry barriers. Success increasingly depends on combining innovation, dependable supply, comprehensive service support, and interoperable digital solutions that outperform established market leaders.

Terumo Corporation

Medtronic plc

Senko Medical Instrument Mfg. Co., Ltd.

Xenios AG

Braile Biomédica S.A.

Nipro Corporation

EUROSETS S.r.l.

Chalice Medical Ltd.

Spectrum Medical Ltd.

Meril Life Sciences Pvt. Ltd.

Gen World Medical Devices

Digital perfusion technologies are redefining cardiopulmonary bypass procedures through integrated patient monitoring, automated documentation, and intelligent workflow management. More than 45% of newly installed premium systems now include real-time hemodynamic analytics and centralized data integration, reducing documentation time by approximately 20%. Hospitals increasingly favor connected platforms because they improve procedural consistency while supporting regulatory compliance and quality reporting.

Emerging technologies include AI-assisted perfusion guidance, predictive alarm algorithms, biocompatible membrane oxygenators, and cloud-enabled service diagnostics. Compared with conventional standalone heart-lung machines, next-generation integrated systems improve workflow efficiency by nearly 18% while reducing manual parameter adjustments by approximately 25%. Adoption has exceeded 40% among leading tertiary cardiac centers, providing manufacturers with stronger service revenues and deeper customer retention. Companies investing in digital ecosystems, software upgrades, and remote diagnostics gain a clear competitive advantage over suppliers focused solely on hardware.

Between 2026 and 2028, intelligent automation, interoperable operating room platforms, and predictive maintenance capabilities will become key procurement criteria. Hospitals will increasingly prioritize complete digital perfusion ecosystems that reduce downtime, optimize asset utilization, and standardize clinical performance. Organizations acting early on connected technologies will strengthen operational efficiency, improve clinician productivity, and secure long-term competitive differentiation.

May 2024 – Terumo Cardiovascular received U.S. FDA 510(k) clearance for the CDI OneView™ Monitoring System, enabling display of 22 real-time patient parameters during cardiopulmonary bypass procedures, strengthening perfusion monitoring capabilities and expanding digital operating room adoption. Source: www.terumo.com

February 2025 – LivaNova PLC reported strong global adoption of its Essenz™ Perfusion System, with cardiopulmonary business recording 11.2% constant-currency quarterly growth, driven by consumables demand and increased capital placements, reinforcing its competitive leadership in advanced perfusion technologies. Source: www.investor.livanova.com

March 2025 – LivaNova PLC confirmed continued expansion of Essenz installations and announced plans to increase oxygenator manufacturing capacity by 60% while targeting broader global deployment of next-generation perfusion technologies, strengthening long-term supply resilience and hospital support. Source: www.livanova.com

February 2025 – Getinge AB announced its strategic exit from the surgical perfusion business, allowing competitors to strengthen cardiopulmonary bypass equipment positioning while redirecting resources toward ECMO technologies, reshaping competitive dynamics across advanced cardiovascular device markets.

This report delivers comprehensive analysis of the cardiopulmonary bypass system industry across seven product types, five major applications, and four end-user categories, providing detailed assessment of demand patterns, technology adoption, procurement strategies, and competitive positioning. Regional evaluation spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment trends, healthcare infrastructure development, manufacturing capabilities, and evolving clinical requirements. More than 70% of demand remains concentrated within hospital-based cardiac surgery programs, while digital perfusion adoption continues expanding across specialized cardiovascular centers.

The study evaluates intelligent perfusion platforms, advanced oxygenators, integrated monitoring technologies, and workflow automation while examining emerging opportunities in connected operating rooms and data-driven perfusion management. Strategic insights support investment prioritization, product portfolio planning, market entry evaluation, partnership development, competitive benchmarking, and geographic expansion decisions. Coverage between 2026 and 2033 enables stakeholders to identify evolving procurement priorities, technology transitions, operational risks, and long-term competitive opportunities across both mature and emerging healthcare markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 263.3 Million |

| Market Revenue (2033) | USD 369.3 Million |

| CAGR (2026–2033) | 4.32% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | LivaNova PLC; Terumo Corporation; Medtronic plc; Senko Medical Instrument Mfg. Co., Ltd.; Xenios AG; Braile Biomédica S.A.; Nipro Corporation; EUROSETS S.r.l.; Chalice Medical Ltd.; Spectrum Medical Ltd.; Meril Life Sciences Pvt. Ltd.; Gen World Medical Devices |

| Customization & Pricing | Available on Request (10% Customization Free) |