Reports

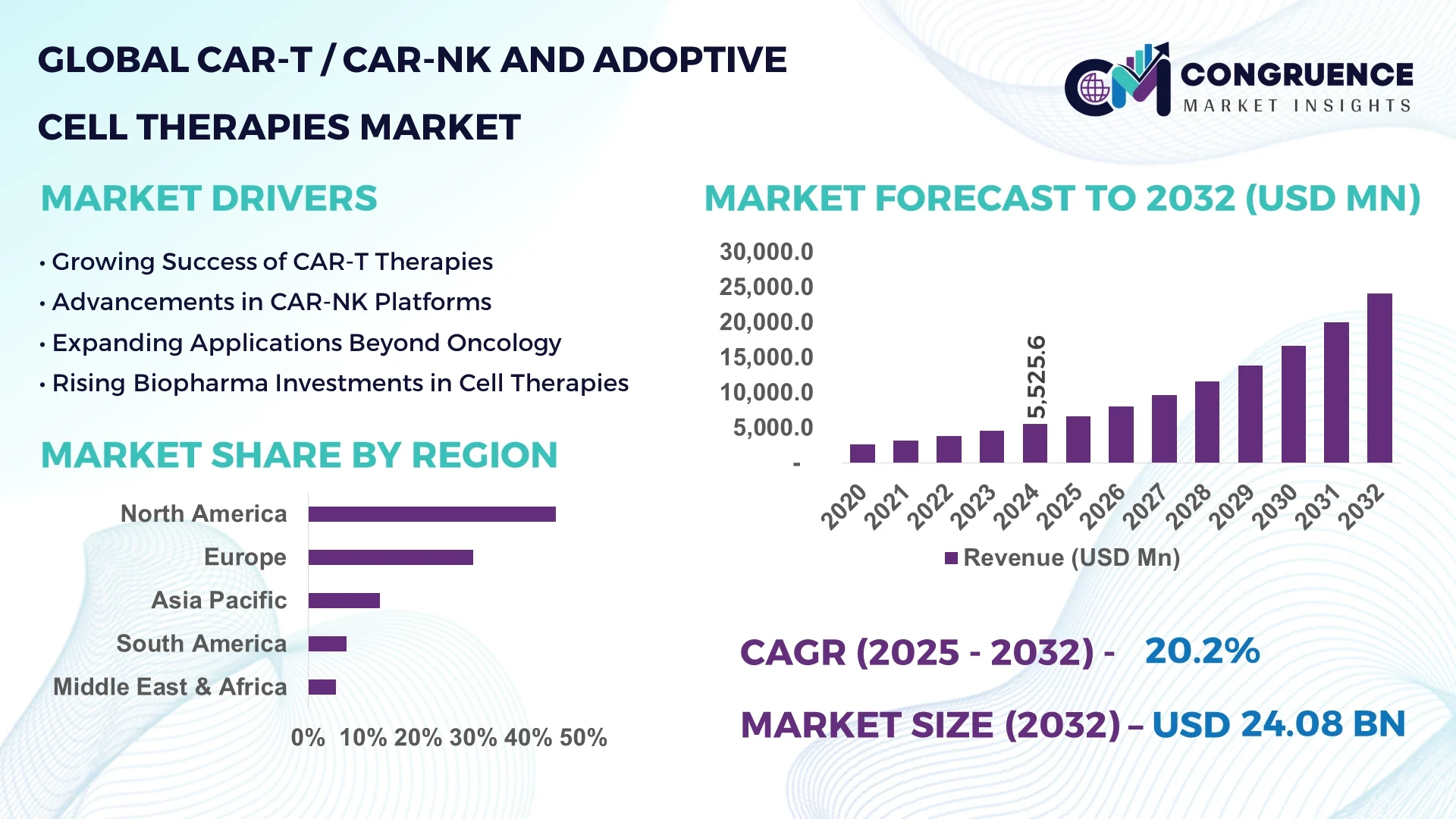

The Global CAR-T / CAR-NK And Adoptive Cell Therapies Market was valued at USD 5,525.60 Million in 2024 and is anticipated to reach a value of USD 24,077.7 Million by 2032 expanding at a CAGR of 20.2% between 2025 and 2032.

In the United States, CAR-T and CAR-NK manufacturing is supported by advanced cell therapy facilities, multi-million-dollar funding in next-generation adoptive platforms, and strong integration within oncology treatment networks—especially for hematologic indications.

Across the broader CAR-T / CAR-NK and Adoptive Cell Therapies market, leading product categories include autologous CAR-T constructs, off-the-shelf CAR-NK therapies, tumor-infiltrating lymphocytes (TILs), and next-gen multi-specific cellular platforms. Notable innovations include closed-system manufacturing modules, bispecific CAR constructs, and streamlined vector delivery systems. Regulatory landscapes are evolving with expedited pathways for breakthrough therapies; meanwhile, growing emphasis on precision medicine and cancer survival outcomes is driving payer willingness to reimburse high-complexity treatment modalities. Geographic consumption patterns show North American and European leadership in therapy adoption, while Asia-Pacific is leveraging scaling manufacturing hubs and clinical trial infrastructure. Emerging trends feature modular decentralized production units, combinatorial adoptive regimens, enhanced safety switch incorporation, and early-stage development of CAR-NK and CAR-M (macrophage) therapies, signaling a robust future outlook for adoptive immunotherapies.

AI is playing a pivotal role in optimizing operational performance, throughput, and safety across the CAR-T / CAR-NK And Adoptive Cell Therapies Market. Machine learning tools now predict optimal antigen targets and refine construct design, reducing preclinical lead times by approximately 25%. AI-powered image processing during manufacturing identifies cell phenotype deviations in real-time, improving batch yield consistency and significantly reducing product failure rates. Within clinical manufacturing sites, AI-driven process analytics monitor cytokine levels and cell viability in bioreactors, enabling proactive interventions that minimize contamination risk and enhance regulatory compliance. These tools also facilitate efficient patient-to-product matching by processing clinical and genomic datasets, streamlining trial enrollment in the adoptive therapy space. Furthermore, natural language processing (NLP) algorithms aid protocol optimization by summarizing trial eligibility from literature, expediting study setup. AI is enabling adaptive dosing models based on early immune response metrics, enhancing therapeutic precision and safety. In effect, AI integration is not only accelerating development cycles but also improving consistency, accuracy, and operational efficiency throughout the CAR-T / CAR-NK And Adoptive Cell Therapies Market.

“In July 2024, a collaboration between a leading CAR-T developer and an AI biotech firm implemented deep-learning models that predicted optimal CAR-T antigen combinations, increasing in-vitro cytotoxicity by 18%.”

The CAR-T / CAR-NK And Adoptive Cell Therapies Market is shaped by rapid therapeutic innovation, evolving manufacturing strategies, and dynamic clinical uptake. With increasing approvals for CAR-T therapies and growing preclinical interest in CAR-NK platforms, development activity is intensifying. Manufacturing is transitioning from centralized suites to modular, cGMP-compliant units, supporting faster turnover and decentralized access. Healthcare policies are adjusting to value-based reimbursement aligned with long-term remission outcomes. Strategic R&D and academic-industry alliances are expanding adoptive platform pipelines. Regulatory agencies continue adapting frameworks to expedite access for breakthrough cellular therapies. Simultaneously, emerging economies are investing in adoptive manufacturing infrastructure and registration pathways. Together, these forces are reshaping strategy, investment, and delivery across the CAR-T / CAR-NK And Adoptive Cell Therapies Market.

The emergence of allogeneic CAR-NK products and plug-and-play modular manufacturing units is accelerating scalable therapy production. Early adopters report cutting delivery timelines by up to two weeks and reducing operating footprint in clinical sites—advancing both supply and access in adoptive cell therapy deployment.

Manufacturing complexity, cryogenic transport requirements, and coordination across collection, engineering, and infusion steps remain limiting factors. A significant number of centers—particularly outside tier-1 academic sites—still rely on centralized manufacturing, which can extend lead times and constrain therapy reach.

Ongoing Phase I/II trials are exploring CAR-T or CAR-NK modalities in solid tumors, often in combination with checkpoint inhibitors or modulatory biologics. Early signals of infiltration and partial responses are prompting sponsors to scale early-phase programs—unlocking new therapeutic use-cases beyond hematologic malignancies.

Cytokine release syndrome and neurotoxicity risks demand specialized care infrastructure, limiting adoption in centers without ICU backup. Moreover, regulatory requirements diverge significantly across regions—some demand full DPR validation for viral vector use, while others lack defined standards—posing challenges for global rollout of adoptive therapies.

** Surge in CAR-NK Research and Pilot Deployments: CAR-NK constructs are entering clinical settings, with early-stage trials demonstrating reduced off-target toxicity and reporting expanded safety margins relative to CAR-T in preclinical models.

** Introduction of Modular On-Site Manufacturing Pods: Multiple therapy centers have deployed mobile, closed-system CAR manufacturing units enabling same-site production of autologous and allogeneic products, significantly reducing logistical complexity.

** Adoption of AI-Driven Quality Assurance: AI-enabled monitoring systems now track bioreactor parameters and cell viability in real-time, alerting operators to process drift and improving batch consistency across adoptive therapy facilities.

** Advancement of CAR-M and Multi-Cell Platforms: Early preclinical studies of CAR-macrophage and hybrid adoptive platforms are gaining visibility, with proof-of-concept data showing enhanced tumor infiltration and antigen presentation characteristics.

The CAR-T / CAR-NK And Adoptive Cell Therapies market is segmented by therapy type (autologous CAR-T, allogeneic CAR-NK, TCR-engineered cells, TILs), application (hematologic malignancies, solid tumors, combination regimens, autoimmune indications), and end-user (academic hospitals, specialty therapy centers, commercial cell therapy CDMOs, biopharma). These segments reflect distinct clinical applicability, infrastructure requirements, and adoption dynamics. This structure offers decision-makers clarity in aligning strategic priorities, capacity planning, and investment pathways within the rapidly evolving adoptive immunotherapy domain.

Autologous CAR-T remains the leading type, anchored by multiple regulatory approvals and deep clinical evidence in hematologic cancers. The fastest-growing type is allogeneic CAR-NK, driven by off-the-shelf potential and notably improved safety profiles. TCR-engineered and TIL-based therapies maintain niche relevance, especially in research centers focused on solid tumors and personalized neoantigen approaches.

Hematologic cancers constitute the dominant application—attributable to existing approvals and therapy familiarity. The fastest-growing application is solid tumors, sustained by expanding trial portfolios and new delivery constructs such as armored CAR-T or CAR-NK. Combination strategies—such as adoptive cell therapy plus checkpoint inhibitors—are emerging, particularly in resistant or late-stage indications, solidifying their role in future therapy regimens.

Academic and research hospitals are the leading end-users, with established manufacturing and trial infrastructure. The fastest-growing end-user segment is commercial CDMOs and specialty therapy centers, capitalizing on modular manufacturing and serving growing service-based therapy needs. Biopharma sponsors complement the landscape through licensing partnerships and pipeline development, contributing upstream through therapeutic innovation rather than direct delivery.

North America accounted for the largest market share at 45% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 23% between 2025 and 2032.

North America benefits from well-established biopharma infrastructure, advanced clinical trial networks, and strong regulatory support for innovative therapies. Europe follows with robust R&D investments and expanding adoption in oncology centers, particularly in Germany, the UK, and France. Asia-Pacific is emerging as a critical growth hub, driven by large patient populations in China and India, combined with increasing government support for cell therapy manufacturing. South America and the Middle East & Africa are gaining traction through public–private partnerships and infrastructure improvements, opening new pathways for adoptive immunotherapies. These regional variations highlight a globally competitive yet fragmented market landscape.

Innovative Cell-Based Therapies Driving Cancer Immunology

North America accounted for nearly 45% of the CAR-T / CAR-NK and Adoptive Cell Therapies market in 2024, underscoring its leadership in advanced oncology treatments. The demand is fueled by industries spanning biopharmaceuticals, research hospitals, and precision medicine companies. Regulatory bodies have accelerated approval timelines through expedited review programs, encouraging rapid commercialization. Federal and state-level funding has significantly boosted R&D, particularly in expanding GMP-compliant facilities. Technological advances include digital twin applications in manufacturing and AI-driven quality control systems. These advancements are improving consistency and scalability of adoptive therapies, strengthening the region’s dominance in high-complexity cellular immunotherapies.

Advancing Immunotherapy with Collaborative Research Models

Europe accounted for close to 30% of the CAR-T / CAR-NK and Adoptive Cell Therapies market in 2024, supported by strong activity in Germany, the UK, and France. The European Medicines Agency (EMA) continues to refine regulatory pathways for advanced therapies, ensuring higher compliance and patient safety standards. Sustainability initiatives are also emerging, particularly in manufacturing, as facilities adopt greener supply chains for biopharma operations. Adoption of digital platforms and automation within research laboratories is accelerating therapy development. Widespread academic-industry collaboration is reinforcing Europe’s competitive advantage, making it a pivotal market in shaping global immunotherapy pipelines.

Scaling Manufacturing Hubs for Next-Gen Therapies

Asia-Pacific ranked second in market volume in 2024 and is positioned as the fastest-growing region, with China, India, and Japan representing the top consuming countries. China’s expansion in GMP facilities and India’s focus on contract development and manufacturing are reshaping the supply chain landscape. Japan continues to lead in clinical translation through its advanced regulatory framework for regenerative medicine. Regional innovation hubs are integrating robotics and AI in production systems, creating faster turnaround times and higher cell therapy yields. This region is becoming an essential contributor to global expansion, with its infrastructure positioning it as a future leader in adoptive cell therapy manufacturing.

Emerging Access Pathways through Government Incentives

South America accounted for nearly 7% of the CAR-T / CAR-NK and Adoptive Cell Therapies market in 2024, with Brazil and Argentina as the leading contributors. Market expansion is supported by government trade policies and incentives that encourage biopharma investment. Infrastructure development, particularly in advanced healthcare facilities, is enabling adoption of complex therapies. Key energy and logistics improvements are reducing barriers to importing critical biopharma materials. With increasing patient enrollment in clinical trials, South America is steadily emerging as a promising region for adoptive immunotherapies.

Modernizing Healthcare Systems to Enable Advanced Therapies

The Middle East & Africa represented around 5% of the CAR-T / CAR-NK and Adoptive Cell Therapies market in 2024, led by countries such as the UAE, Saudi Arabia, and South Africa. Regional demand is driven by healthcare diversification beyond oil & gas economies and increasing investment in cancer treatment infrastructure. Modernization of laboratories, adoption of AI-based diagnostic tools, and digital hospital networks are creating a supportive environment for advanced therapies. Local regulatory partnerships and trade agreements are improving market access, ensuring that adoptive therapies gradually penetrate this developing healthcare market.

United States – 40% Market Share

Strong clinical trial networks, advanced manufacturing capabilities, and consistent regulatory support sustain its leadership in the CAR-T / CAR-NK and Adoptive Cell Therapies market.

China – 20% Market Share

Rapid expansion of GMP manufacturing facilities and high patient enrollment in early-stage clinical trials drive its fast-growing presence in adoptive therapies.

The CAR-T / CAR-NK And Adoptive Cell Therapies market is highly competitive, with more than 70 active players globally ranging from multinational biopharmaceutical corporations to emerging biotech startups. Market leaders hold strong positions due to their diverse pipelines and proven track records in commercializing CAR-T products. Strategic partnerships with CDMOs and academic institutions remain a critical component for expanding global reach. Companies are engaging in mergers and acquisitions to strengthen technology platforms and broaden clinical portfolios. Continuous product launches, especially in CAR-NK and dual-targeted CAR constructs, are reshaping the competitive dynamics. Innovation trends focus on decentralized manufacturing, AI-driven quality monitoring, and next-generation safety switches. This environment fosters rapid therapeutic development but also intensifies pressure on smaller players to differentiate through niche applications or specialized expertise.

Novartis AG

Gilead Sciences (Kite Pharma)

Bristol Myers Squibb

Johnson & Johnson (Janssen Biotech)

Fate Therapeutics

Nkarta Therapeutics

Allogene Therapeutics

Cellectis

Autolus Therapeutics

Legend Biotech

Adaptimmune Therapeutics

The CAR-T / CAR-NK and Adoptive Cell Therapies market is undergoing a technological transformation, with advances in manufacturing, vector design, and digitalization driving greater scalability and precision. Closed-system bioreactors now enable continuous monitoring of cell expansion, reducing contamination risks and improving yields by up to 30%. The development of non-viral gene editing platforms such as CRISPR and transposon systems is lowering costs while enhancing safety by minimizing insertional mutagenesis. AI and machine learning are streamlining design of antigen-specific constructs and predicting off-target effects with high accuracy. Automation in cell processing, including robotic liquid handling and digital quality assurance, has reduced batch variability. Emerging trends also highlight point-of-care manufacturing pods, which can decentralize therapy production and increase accessibility. Furthermore, integration of multi-omic data into therapy design is supporting highly personalized treatment strategies, offering new opportunities in solid tumor applications. Collectively, these technologies are setting the foundation for broader adoption, higher efficiency, and improved patient safety in next-generation adoptive immunotherapies.

In March 2023, Bristol Myers Squibb received regulatory approval for a new CAR-T therapy targeting relapsed large B-cell lymphoma, expanding treatment options for patients resistant to standard regimens.

In October 2023, Novartis announced the launch of a decentralized CAR-T manufacturing program, deploying automated units in clinical centers to reduce vein-to-vein time and increase patient access.

In May 2024, Fate Therapeutics initiated clinical trials for its off-the-shelf CAR-NK therapy, showing promising safety results and highlighting the shift toward allogeneic adoptive cell therapies.

In July 2024, Allogene Therapeutics reported successful results from an early-phase trial of its dual-targeted CAR-T construct, demonstrating enhanced tumor control and reduced relapse rates.

The scope of the CAR-T / CAR-NK And Adoptive Cell Therapies Market Report covers a comprehensive analysis of therapy types, applications, end-users, and geographic regions, providing insights into both established and emerging segments. It examines autologous CAR-T therapies, allogeneic CAR-NK platforms, TCR-engineered approaches, and TIL-based treatments, each contributing to distinct market opportunities. Applications are explored across hematologic malignancies, solid tumors, autoimmune disorders, and combination regimens, reflecting the diverse clinical potential of adoptive immunotherapies. The report includes regional insights spanning North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting unique growth drivers and adoption challenges. Attention is also given to technological trends such as automation, AI integration, non-viral vector delivery, and decentralized manufacturing. Industry coverage encompasses biopharma leaders, clinical research organizations, and contract development partners. By addressing therapeutic innovation, infrastructure expansion, and regulatory evolution, the report provides stakeholders with actionable intelligence to identify investment opportunities, assess competitive positioning, and plan strategic roadmaps in the rapidly evolving landscape of adoptive cell therapies.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 5,525.6 Million |

|

Market Revenue in 2032 |

USD 24,077.7 Million |

|

CAGR (2025 - 2032) |

20.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Novartis AG, Gilead Sciences (Kite Pharma), Bristol Myers Squibb, Johnson & Johnson (Janssen Biotech), Fate Therapeutics, Nkarta Therapeutics, Allogene Therapeutics, Cellectis, Autolus Therapeutics, Legend Biotech, Adaptimmune Therapeutics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |