Reports

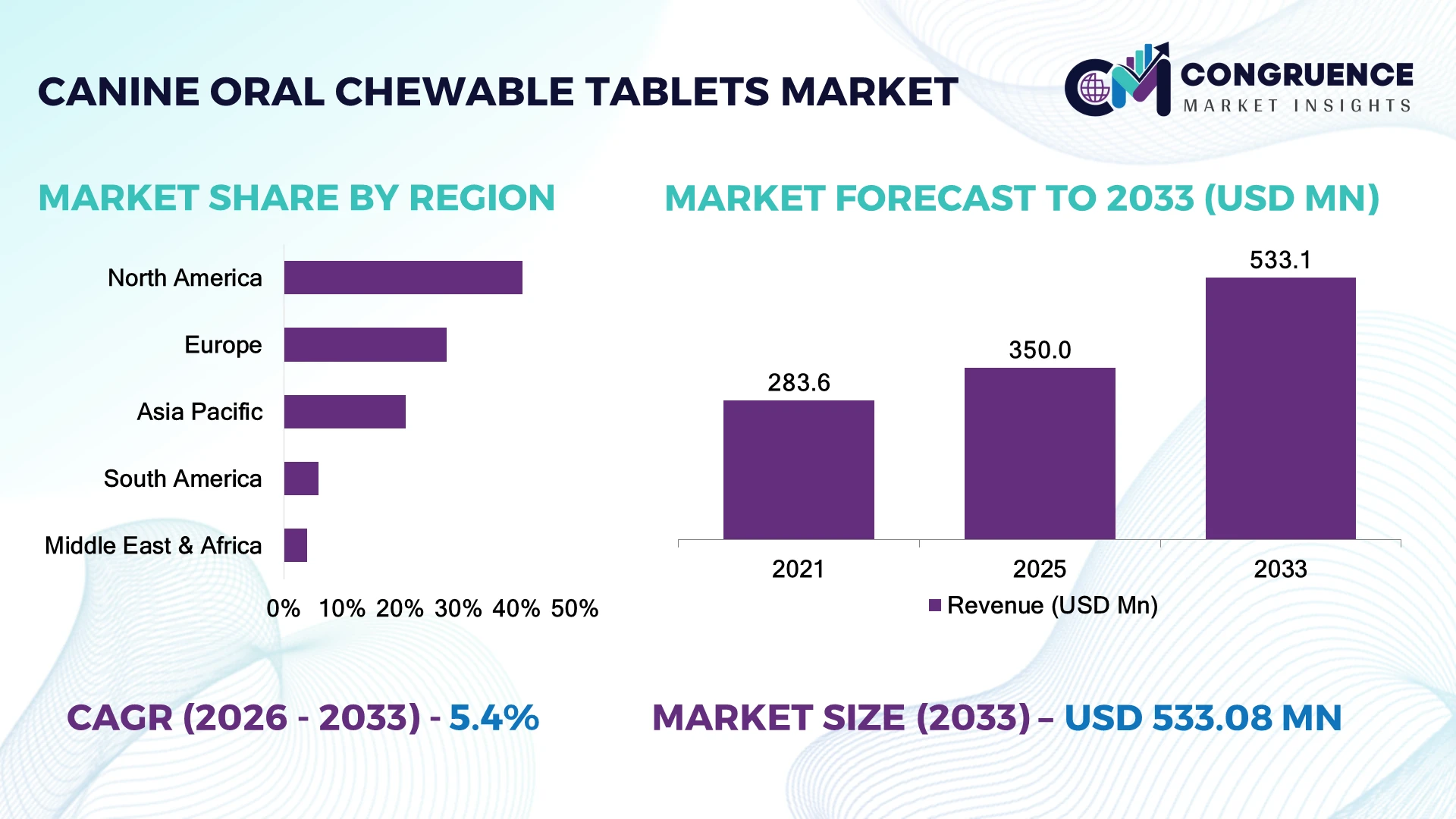

The Global Canine Oral Chewable Tablets Market was valued at USD 350.0 Million in 2025 and is anticipated to reach a value of USD 533.1 Million by 2033 expanding at a CAGR of 5.4% between 2026 and 2033. Growth is driven by rising preventive veterinary care, increasing preference for palatable oral dosage forms, and expanding approvals for advanced parasiticides and chronic disease therapies in companion animals.

The United States dominates the global market with an estimated 39% share, supported by one of the world's largest companion animal healthcare industries, robust veterinary infrastructure, and annual pet healthcare spending exceeding USD 38 billion. Compared with Germany, where preventive treatment adoption remains below 30% in several routine care segments, U.S. veterinary clinics report preventive medication compliance above 65%, reinforced by continuous pharmaceutical innovation and strong regulatory oversight through the FDA Center for Veterinary Medicine.

This leadership reinforces North America as the primary commercialization hub, making regulatory readiness, product differentiation, and veterinary partnerships essential for long-term competitive success.

Market Size & Growth: USD 350.0 Million in 2025, projected to reach USD 533.1 Million by 2033 at 5.4% CAGR, supported by advanced companion animal therapeutics and expanded preventive healthcare.

Top Growth Drivers: Preventive parasite control adoption (+22%), pet insurance expansion (+18%), veterinary clinic digitalization (+15%).

Short-Term Forecast: By 2028, manufacturing efficiency improves by 14% through automated tablet production and digital quality monitoring.

Emerging Technologies: AI-assisted formulation, precision flavor masking, and controlled-release chewable technologies accelerate product performance.

Regional Leaders: North America (~USD 205 Million), Europe (~USD 102 Million), Asia-Pacific (~USD 73 Million), driven by premium pet healthcare and regional veterinary expansion.

Consumer/End-User Trends: More than 68% of pet owners prefer flavored chewable tablets over conventional oral dosage forms for improved compliance.

Pilot/Case Example: In 2024, veterinary digital prescription programs improved treatment adherence by approximately 19% across participating clinics.

Competitive Landscape: Leading companies collectively account for nearly 52% of the market, including Zoetis, Elanco Animal Health, Merck Animal Health, Boehringer Ingelheim, and Virbac.

Regulatory & ESG Impact: Sustainable pharmaceutical packaging initiatives reduce packaging waste by nearly 20% while supporting evolving veterinary compliance standards.

Investment & Funding: More than USD 900 Million has been directed toward veterinary pharmaceutical expansion, manufacturing upgrades, and strategic partnerships.

Innovation & Future Outlook: Next-generation multifunctional chewable formulations and digital veterinary ecosystems strengthen global product differentiation and regional market expansion.

Canine Oral Chewable Tablets Market demand is expanding across parasite prevention, pain management, dermatology, and chronic disease treatment for companion dogs. Advanced taste-enhancement technologies and extended-release formulations continue improving treatment compliance, with flavored dosage acceptance exceeding 70% in veterinary practices. Growing localization of pharmaceutical manufacturing and evolving veterinary quality standards are strengthening supply resilience while supporting broader commercialization and strategic product innovation.

The Canine Oral Chewable Tablets Market has become strategically important as veterinary healthcare providers increasingly prioritize treatment adherence, premium therapeutics, and preventive care programs. Companies are strengthening regional manufacturing networks and diversifying ingredient sourcing to improve supply continuity while adapting to evolving veterinary regulatory requirements. Digital prescription management and connected veterinary services are also reshaping commercial strategies across developed healthcare markets.

Modern chewable tablet manufacturing systems deliver approximately 18% higher production efficiency than conventional batch processing while reducing formulation variability and product waste. North America continues to lead commercialization through established veterinary infrastructure and premium pet healthcare spending, whereas Asia-Pacific is rapidly expanding through increasing pet ownership, wider veterinary clinic networks, and local pharmaceutical manufacturing capabilities. Industry adoption of automated packaging and digital quality assurance continues to improve operational consistency.

Manufacturers are introducing multifunctional chewable products combining parasite protection with broader therapeutic benefits while expanding partnerships with veterinary hospitals, distributors, and animal health providers. Investment priorities increasingly focus on formulation innovation, localized production, and digital veterinary engagement platforms. These strategic initiatives strengthen competitive positioning, improve treatment accessibility, and establish long-term operational resilience across the evolving global companion animal healthcare industry.

Rising preventive healthcare for companion animals and greater acceptance of palatable oral formulations are reshaping veterinary pharmaceutical strategies. More than 68% of dog owners now prefer flavored chewable medications because they improve treatment compliance, while preventive parasite protection exceeds 70% among insured pets in the United States. Updated veterinary treatment guidelines continue encouraging routine preventive medication over reactive care, accelerating prescription volumes. This shift has increased demand for combination therapies that simplify dosing schedules and strengthen adherence. In response, companies are investing in advanced flavor-masking technologies, expanding manufacturing capacity, and partnering with veterinary clinic networks to improve product accessibility. A key strategic advantage lies in integrating multiple therapeutic indications into a single chewable formulation, reducing administration complexity while improving long-term patient outcomes.

Stringent veterinary pharmaceutical approval requirements and dependence on specialized active pharmaceutical ingredients continue limiting production flexibility. Regulatory documentation and product validation account for nearly 20% of total development timelines, while approximately 35% of veterinary pharmaceutical manufacturers rely on imported active ingredients for critical formulations. Global logistics disruptions and tighter quality compliance have increased procurement uncertainty, particularly for manufacturers sourcing ingredients from multiple countries. These pressures extend product launch schedules and reduce manufacturing responsiveness. Companies are addressing these constraints by localizing API sourcing, establishing long-term procurement agreements, and qualifying multiple suppliers to improve supply continuity. Strengthening domestic manufacturing ecosystems has become an important operational strategy for reducing exposure to cross-border disruptions and maintaining consistent product availability.

Next-generation chewable formulations supported by digital veterinary platforms are creating differentiated value across companion animal healthcare. More than 45% of veterinary clinics in developed markets now utilize digital prescription management, while automated adherence reminders improve treatment completion by approximately 18%. In Japan, increased investment in precision veterinary medicine is accelerating development of breed-specific therapeutic formulations with enhanced bioavailability. Companies are combining controlled-release technologies, personalized dosing approaches, and connected veterinary software to strengthen long-term treatment outcomes. Strategic collaborations between pharmaceutical developers and veterinary technology providers are expanding integrated care ecosystems. An emerging opportunity lies in combining therapeutic monitoring with digital compliance tools, enabling more effective chronic disease management while improving clinical decision-making and operational efficiency.

Maintaining manufacturing consistency across multiple production sites remains a significant execution challenge as veterinary pharmaceutical portfolios become increasingly specialized. Quality assurance activities account for nearly 25% of production operations, while regulatory inspections have increased by approximately 15% across several major pharmaceutical manufacturing jurisdictions. In Germany, stricter validation requirements for veterinary medicinal products require manufacturers to maintain harmonized production documentation across facilities. These evolving compliance expectations increase operational complexity, workforce training requirements, and technology integration demands. Companies must continue investing in advanced manufacturing automation, digital quality management systems, and standardized validation protocols to sustain consistent product performance. Building globally aligned production infrastructure will remain essential for protecting competitiveness, accelerating product deployment, and supporting long-term operational resilience.

Combination Therapy Expansion Companion animal healthcare providers are rapidly shifting toward multi-action chewable tablets that combine parasite control with dermatological or gastrointestinal support. Combination prescriptions have increased by nearly 24% over the past two years, while treatment adherence has improved by approximately 18% due to simplified dosing. Companies are expanding integrated product portfolios, optimizing formulation platforms, and streamlining manufacturing workflows to reduce inventory complexity and improve veterinary prescribing efficiency amid evolving preventive healthcare protocols.

Advanced Palatability Engineering Veterinary pharmaceutical manufacturers are accelerating investments in flavor-masking technologies and protein-based excipient systems to improve canine acceptance. Palatable chewable formulations now achieve acceptance rates above 72%, reducing incomplete treatment cycles by nearly 16%. Automated formulation optimization and digital quality-control systems are shortening development timelines while improving production consistency. Manufacturers are strengthening R&D partnerships and expanding specialized formulation capabilities to differentiate products within increasingly competitive companion animal therapeutic portfolios.

Localized Manufacturing Strategies Pharmaceutical companies are restructuring supply chains by expanding regional manufacturing and secondary packaging operations closer to high-demand veterinary markets. Local sourcing of selected pharmaceutical ingredients has increased by approximately 20%, while inventory lead times have declined by nearly 14%. This operational transition strengthens procurement resilience against global logistics disruptions and regulatory inspection delays. Companies are increasing contract manufacturing partnerships and upgrading production facilities to improve continuity, flexibility, and market responsiveness.

Digital Veterinary Integration Veterinary clinics are increasingly integrating electronic prescribing, treatment reminders, and digital patient records into routine companion animal care. Digital prescription workflows have expanded by nearly 28%, while automated follow-up programs improve medication compliance by around 17%. Pharmaceutical companies are collaborating with veterinary software providers to connect products with digital healthcare ecosystems, enabling better prescription tracking, inventory forecasting, and long-term treatment management while supporting more efficient clinical operations.

Parasiticide chewable tablets remain the dominant product category, accounting for approximately 48% of the global market due to routine preventive treatment against fleas, ticks, heartworm, and intestinal parasites. Their broad clinical application, convenient administration, and high compliance among pet owners continue to strengthen market penetration. Pain management chewables represent the fastest-growing segment as veterinary practices increasingly adopt long-term osteoarthritis and post-surgical care protocols. Anti-inflammatory, nutritional supplement, and dermatology-focused chewables continue expanding their strategic relevance through specialized treatment pathways and personalized veterinary care. Manufacturers are broadening product portfolios by introducing multi-benefit formulations and improving flavor technologies to increase treatment acceptance. Nearly 70% of newly introduced chewable veterinary products emphasize enhanced palatability or simplified dosing, while combination formulations continue gaining traction across veterinary clinics. Investment priorities increasingly focus on differentiated therapeutic indications, lifecycle management, and premium prescription products that improve treatment adherence and strengthen competitive positioning.

Parasite prevention represents the largest application segment with an estimated 46% market share, supported by routine veterinary recommendations and year-round preventive healthcare protocols. Consistent prescription frequency, broad disease coverage, and growing awareness among pet owners reinforce its leadership. Chronic disease management is emerging as the fastest-growing application as longer canine life expectancy increases demand for sustained therapies addressing osteoarthritis, dermatological disorders, endocrine diseases, and cardiac conditions. Pain management, nutritional supplementation, and gastrointestinal care continue expanding through integrated wellness programs and individualized treatment strategies. Veterinary pharmaceutical companies are strengthening application-specific product development by combining therapeutic efficacy with improved dosing convenience. Approximately 65% of veterinary clinics increasingly recommend preventive oral medications during annual wellness examinations, while digital patient monitoring supports better long-term treatment adherence. Companies continue expanding clinical education programs and veterinary partnerships to strengthen prescription confidence across both mature preventive applications and specialized chronic care segments.

Veterinary clinics account for approximately 58% of total market demand, supported by prescription authority, diagnostic capabilities, and direct patient management. Their established infrastructure enables routine preventive treatment, chronic disease monitoring, and post-treatment evaluation, making them the primary distribution channel for prescription chewable tablets. Veterinary hospitals represent the fastest-growing end-user segment as advanced surgical procedures, specialist care, and referral services continue expanding. Animal shelters, research institutions, and rehabilitation centers also contribute through preventive treatment programs and disease management initiatives. Manufacturers are strengthening relationships with veterinary professionals through clinical education, customized pricing programs, digital ordering platforms, and technical support. Nearly 62% of prescription chewable products are dispensed directly through veterinary practices, while integrated procurement systems continue improving inventory planning and operational efficiency. Companies are expanding enterprise partnerships, distributor networks, and professional engagement initiatives to strengthen market coverage and improve long-term customer retention across institutional buyers.

North America accounted for the largest market share at 41.0% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.7% between 2026 and 2033.

North America remains the largest regional market, supported by mature veterinary healthcare infrastructure, high companion animal ownership, and strong prescription compliance. The region contributes approximately 41% of global demand, with veterinary clinics serving as the primary dispensing channel for preventive and therapeutic chewable medications. Preventive parasite management programs exceed 70% adoption among insured companion dogs, while digital prescription workflows continue improving treatment continuity. Pharmaceutical companies are expanding domestic manufacturing, strengthening veterinary distribution partnerships, and increasing investment in advanced formulation technologies. Automated packaging lines and electronic inventory management have reduced order processing times by nearly 16%, improving supply responsiveness across veterinary networks. Premium therapeutic portfolios and integrated veterinary care models continue reinforcing the region's operational leadership.

United States Market Outlook: The United States represents the largest national market owing to its extensive veterinary hospital network, advanced companion animal healthcare ecosystem, and robust pharmaceutical innovation capabilities. More than 32,000 veterinary practices support widespread deployment of prescription chewable therapies, while preventive healthcare adoption continues increasing among insured pet populations. Companies are expanding manufacturing capacity, investing in digital veterinary platforms, and strengthening distribution partnerships to accelerate product availability and improve prescription adherence across both urban and suburban veterinary care networks.

Europe accounts for approximately 28% of the global market, supported by stringent veterinary pharmaceutical standards, strong companion animal welfare policies, and established prescription-based treatment practices. Veterinary professionals increasingly recommend chewable formulations for chronic disease management and parasite prevention due to improved treatment compliance. Pharmaceutical manufacturers continue modernizing production facilities with automated quality systems and expanding specialized veterinary product portfolios. More than 60% of new veterinary pharmaceutical manufacturing investments emphasize advanced quality assurance technologies and sustainable production processes. Strategic collaborations between manufacturers and veterinary organizations continue improving clinical adoption while supporting consistent regulatory compliance across European markets.

Germany Market Outlook: Germany leads the European market through its advanced pharmaceutical manufacturing capabilities, well-established veterinary healthcare infrastructure, and strong regulatory framework. Veterinary prescription compliance remains among the highest in Europe, supported by widespread preventive healthcare practices and continuous pharmaceutical innovation. Manufacturers continue investing in formulation research, automated production technologies, and high-quality manufacturing standards while strengthening collaborations with veterinary professionals to support next-generation companion animal therapeutics.

Asia-Pacific represents approximately 21% of the global market and continues strengthening its position through rapid companion animal adoption, expanding veterinary infrastructure, and growing pharmaceutical manufacturing capacity. Increasing disposable income and greater awareness of preventive veterinary care are driving prescription demand across urban markets. Regional manufacturers are increasing localized production while multinational companies continue expanding commercial operations and distribution networks. Pharmaceutical manufacturing investments have increased by nearly 22% across major production hubs, supporting improved product availability and shorter delivery timelines. The combination of expanding veterinary services and localized manufacturing is creating a highly competitive operating environment.

China Market Outlook: China is the largest market within Asia-Pacific due to its expanding companion animal population, increasing veterinary clinic density, and rapidly developing animal healthcare industry. Domestic pharmaceutical manufacturers continue investing in modern production facilities, quality certification programs, and research capabilities to support premium veterinary medicines. Digital pet healthcare platforms and expanding veterinary hospital chains are improving prescription accessibility, while localized manufacturing strengthens supply continuity and competitive pricing.

South America accounts for approximately 6% of the global market, supported by improving veterinary services, rising companion animal ownership, and greater awareness of preventive healthcare. Veterinary clinic expansion across metropolitan areas is increasing prescription accessibility for chewable therapeutics, particularly for parasite prevention and chronic disease management. Distribution modernization and regional pharmaceutical partnerships continue strengthening product availability despite periodic logistics constraints. Approximately 18% of veterinary distributors have expanded cold-chain and pharmaceutical storage capacity to improve inventory management. Companies are increasing localized commercial partnerships while optimizing distribution strategies to improve operational efficiency and strengthen market penetration.

Brazil Market Outlook: Brazil represents the largest market in South America due to its substantial companion animal population and expanding veterinary healthcare sector. Veterinary pharmaceutical companies continue strengthening regional distribution networks, investing in professional education initiatives, and expanding access to premium preventive medications. Growing veterinary clinic networks and improved pharmaceutical logistics continue supporting higher prescription volumes while encouraging wider adoption of advanced chewable formulations throughout the country's companion animal healthcare ecosystem.

The Middle East & Africa contributes approximately 4% of the global market, supported by expanding veterinary infrastructure, increasing investment in companion animal healthcare, and improving pharmaceutical distribution capabilities. Urban veterinary hospitals are adopting more advanced diagnostic and prescription practices, encouraging wider use of premium chewable therapies. Governments and private healthcare providers continue investing in veterinary modernization, while pharmaceutical companies strengthen regional partnerships to improve product availability. Distribution capacity has expanded by nearly 15% across major urban healthcare networks, improving supply consistency and reducing procurement delays. Strategic investment remains focused on expanding veterinary service accessibility and strengthening pharmaceutical supply chains.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through continued investment in veterinary healthcare infrastructure, expanding private veterinary hospital networks, and modernization of pharmaceutical distribution systems. Companion animal healthcare services continue developing rapidly across major cities, supported by stronger regulatory oversight and increasing demand for premium veterinary medicines. Companies are expanding commercial partnerships, improving logistics capabilities, and introducing specialized prescription products to strengthen long-term market presence and operational efficiency.

The Canine Oral Chewable Tablets Market is characterized by competition between global animal health leaders such as Zoetis, Elanco Animal Health, Merck Animal Health, Boehringer Ingelheim, and Virbac, and regional veterinary pharmaceutical manufacturers competing through localized distribution and pricing. The top five companies collectively account for approximately 58% of the global market, reflecting a moderately consolidated structure. Competition centers on formulation innovation, palatability, regulatory approvals, manufacturing reliability, and veterinary channel penetration rather than price alone. Premium chewable formulations improve treatment compliance by nearly 18%, while automated manufacturing reduces batch variability by around 15% and digital supply-chain platforms shorten fulfillment cycles by approximately 12%. Companies are strengthening positions through manufacturing expansion, strategic acquisitions, veterinary partnerships, and vertically integrated supply networks. Competitive momentum is shifting toward multifunctional parasite-control products, localized production, and digital veterinary ecosystems. Regulatory expertise, clinical validation, and established veterinary distribution remain the primary entry barriers. Winning requires continuous product innovation, resilient manufacturing, rapid regulatory execution, and trusted veterinary relationships.

Elanco Animal Health Incorporated

Merck Animal Health

Boehringer Ingelheim Animal Health

Virbac S.A.

Dechra Pharmaceuticals PLC

Ceva Santé Animale

Vetoquinol S.A.

Chanelle Pharma

Norbrook Laboratories Ltd.

Krka d.d.

Ourofino Saúde Animal

Advanced palatability engineering, precision granulation, and continuous manufacturing technologies are transforming canine oral chewable tablet production. Modern flavor-masking systems improve medication acceptance by approximately 20%, while precision blending enhances dosage consistency by nearly 16%. Around 60% of newly launched premium veterinary chewables incorporate advanced taste-enhancement platforms, allowing manufacturers to improve treatment adherence and reduce product rejection during routine administration.

Artificial intelligence is increasingly integrated into formulation optimization, process monitoring, and automated visual inspection. Compared with conventional manual quality control, AI-enabled inspection reduces packaging defects by nearly 22% while shortening batch-release timelines by approximately 15%. Cloud-based manufacturing execution systems are being deployed across large veterinary pharmaceutical facilities, improving production traceability and supply-chain visibility. Companies with integrated digital manufacturing capabilities benefit from faster product commercialization and improved operational consistency.

Between 2026 and 2028, predictive manufacturing analytics, personalized veterinary therapeutics, and connected veterinary prescription platforms will become major competitive differentiators. Digital prescription integration is expected to exceed 40% among advanced veterinary hospital networks, enabling better inventory planning and treatment monitoring. Early adopters investing in intelligent manufacturing, automated quality management, and next-generation chewable delivery technologies will strengthen operational efficiency, accelerate regulatory readiness, and reinforce long-term competitive positioning.

October 2024 – Elanco Animal Health received U.S. FDA approval for Credelio Quattro™ (lotilaner, moxidectin, praziquantel, and pyrantel chewable tablets), the first monthly canine oral chewable providing protection against six major parasite groups in a single dose. Commercial launch was scheduled for Q1 2025, strengthening Elanco's companion animal portfolio. Source: www.elanco.com

April 2025 – Zoetis Inc. secured U.S. FDA approval for a new Simparica Trio® indication preventing flea tapeworm infections by eliminating vector fleas before transmission. The approval marked the company's fourth parasiticide label expansion within six months, reinforcing leadership in preventive canine therapeutics. Source: www.zoetisus.com

May 2025 – Elanco Animal Health received an additional U.S. FDA approval expanding the Credelio Quattro™ label to include treatment and control of hookworm infections in dogs and puppies aged eight weeks and older, broadening therapeutic coverage and strengthening veterinary prescribing flexibility. Source: www.fda.gov

October 2025 – Elanco Animal Health obtained another U.S. FDA label expansion for Credelio® and Credelio Quattro™, adding protection against longhorned tick infestations and prevention of Borrelia burgdorferi infections through vector tick control, significantly expanding tick-borne disease protection for companion dogs.

The report provides comprehensive analysis of the global Canine Oral Chewable Tablets Market across product types, therapeutic applications, end-user categories, and major geographic markets. It evaluates preventive and therapeutic chewable formulations, prescribing trends, manufacturing developments, veterinary distribution channels, regulatory evolution, and technology adoption. The assessment covers companion animal healthcare demand patterns, formulation innovation, production capabilities, competitive positioning, and deployment trends across established and emerging veterinary pharmaceutical markets.

The study delivers strategic intelligence covering North America, Europe, Asia-Pacific, South America, and the Middle East & Africa while evaluating more than 12 leading market participants. It analyzes product innovation, digital veterinary integration, manufacturing modernization, supply-chain optimization, and evolving treatment preferences. The report supports business expansion, investment prioritization, competitive benchmarking, partnership evaluation, portfolio development, and long-term strategic planning by identifying high-potential market segments, operational trends, and emerging commercial opportunities through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 350.0 Million |

| Market Revenue (2033) | USD 533.1 Million |

| CAGR (2026–2033) | 5.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Zoetis Inc.; Elanco Animal Health Incorporated; Merck Animal Health; Boehringer Ingelheim Animal Health; Virbac S.A.; Dechra Pharmaceuticals PLC; Ceva Santé Animale; Vetoquinol S.A.; Chanelle Pharma; Norbrook Laboratories Ltd.; Krka d.d.; Ourofino Saúde Animal |

| Customization & Pricing | Available on Request (10% Customization Free) |