Reports

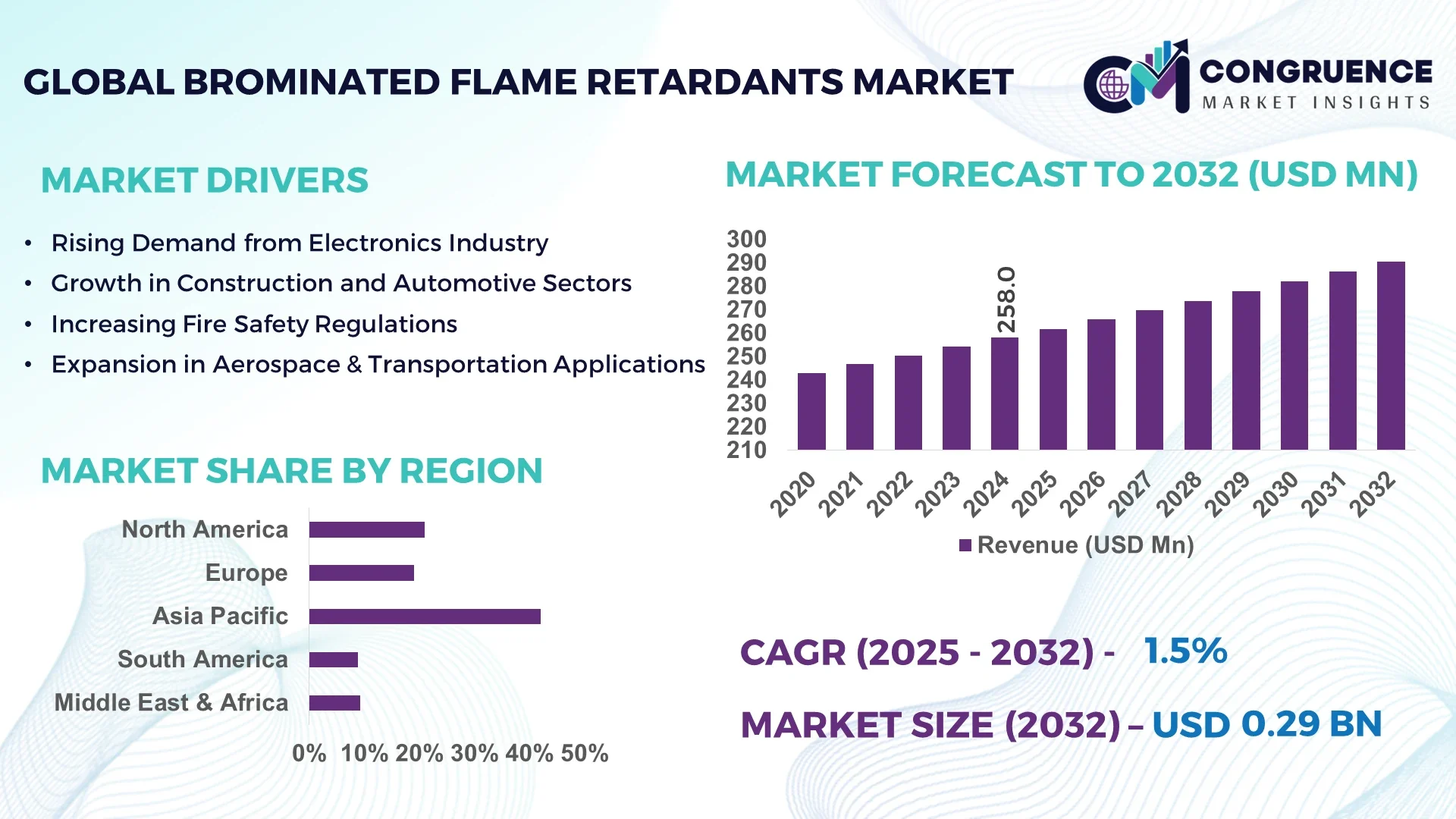

The Global Brominated Flame Retardants Market was valued at USD 258.0 Million in 2024 and is anticipated to reach a value of USD 290.6 Million by 2032 expanding at a CAGR of 1.5% between 2025 and 2032.

China hosts significant production infrastructure for brominated flame retardants, featuring advanced compounding and polymer integration facilities. Investments have focused on high-capacity reactors and automated dosing systems. This supports applications in electronics housings, automotive components, and building insulation products, with ongoing enhancements in precision mixing and thermal stability technologies.

The Brominated Flame Retardants Market encompasses industries such as electronics, construction, textiles, automotive, and aerospace. Electron-device housings and circuit board encapsulation remain primary application sectors, while flame-retardant fabrics and building materials are steadily gaining traction. Technological innovations include development of synergistic blends combining brominated compounds with phosphorus-based retardants for enhanced fire performance and reduced environmental load. Regulatory pressure—particularly from chemical safety agencies—pushes manufacturers toward safer and lower-toxicity formulations, prompting reformulation initiatives and adoption of reactive flame retardants. Environmental concerns are leading to R&D on low-bromine-content and bio-based alternatives. Regional consumption indicates high demand in electronics hubs and emerging infrastructure markets. Emerging trends suggest shifts towards sustainable formulation practices, integration into lightweight composites for EVs, and expansion in Asia-Pacific and Latin American markets, offering strategic prospects for decision-makers in formulation optimization and regulatory adaptation.

Artificial Intelligence (AI) is increasingly playing a pivotal role in enhancing operational excellence and product innovation in the Brominated Flame Retardants Market. AI-powered simulation platforms enable formulators to model the interaction of flame-retardant compounds with polymers under various thermal conditions, accelerating R&D cycles and reducing physical trial-and-error by up to 30%. In production facilities, AI-driven process control systems continuously analyze sensor inputs—temperature, viscosity, mixing torque—and autonomously adjust dosing parameters to maintain consistent dispersion quality, reducing batch rejection rates by approximately 15%. Moreover, predictive maintenance systems leveraging AI analytics flag equipment wear or deviations in reactor performance before failure occurs, which helps minimize downtime and uphold production schedules. Supply chain optimization models in the market track raw-material availability, forecast demand for specific formulation grades, and coordinate logistic scheduling, significantly improving throughput. In product innovation, AI-assisted design tools analyze regulatory toxicology data and guide development toward lower-toxicity formulations while ensuring fire safety standards. Collectively, these AI applications elevate efficiency, consistency, and agility in the Brominated Flame Retardants Market.

“In 2024, a resin additive manufacturer implemented an AI-based mixing control system that reduced batch viscosity variation by 18% and decreased energy consumption in blending operations by 12%.”

The Brominated Flame Retardants Market is shaped by an interplay of technological progress, regulatory pressure, and end-use industry demand. Innovations in reactive and synergistic flame retardant formulations are refining product effectiveness while addressing environmental concerns. Strict fire-safety regulations across electronics and construction sectors require compliance through performance testing and standardized approvals, influencing formulation choices. Supply-chain constraints—such as availability of specific brominated intermediates—can disrupt production schedules. Simultaneously, investments in automation, process control, and sustainable chemistry are modernizing manufacturing capabilities. Demand trends are influenced by the electronics sector’s miniaturization needs and the automotive industry's shift toward lightweight, flame-resistant composites. Manufacturers strategically balance regulatory adaptation with innovation to maintain market relevance.

Strict fire safety standards in electronics, construction, and transportation sectors are driving steady demand for effective flame retardants. These regulations mandate specific fire-performance metrics—such as UL 94 ratings for electronics and ASTM E-84 classifications for building materials—necessitating reliable brominated formulations. Compliance initiatives in major manufacturing economies have also prompted industry consolidation around high-performance standards. As a result, manufacturers are investing in robust testing infrastructure, consistent product scoping, and advanced quality-control systems to meet fire safety specifications in key verticals.

Environmental persistence and toxicity concerns remain a significant restraint on the Brominated Flame Retardants Market. Certain brominated compounds are known to be bioaccumulative and have been linked to developmental and hormonal disruptions. These issues have triggered increasingly strict regulations and consumer skepticism, especially in regions with active chemical safety oversight. Producing lower-toxicity formulations while maintaining efficacy remains a technical and regulatory challenge, requiring deeper investment in R&D and specialized testing protocols.

Growing demand for lower-bromine content and bio-based alternatives presents a strategic opportunity. Companies are exploring synergistic blends that use reduced bromine levels in conjunction with phosphorus- or nitrogen-based co-agents, providing compliance with safety standards while improving environmental profiles. Some manufacturers are piloting plant-derived flame retardant precursors or reactive compounds that chemically bind to polymer matrices, reducing leachability and environmental impact. These innovations open niche applications in consumer electronics and construction where sustainability credentials are increasingly valued.

Balancing regulatory compliance with cost-efficient formulation poses an escalating challenge. Testing requirements for flame resistance, toxicity, and environmental impact vary widely across jurisdictions—requiring multiple rounds of validation and documentation. Specialized analytical equipment, certified testing facilities, and reformulation efforts increase operational complexity. At the same time, raw material price volatility for brominated intermediates and additives can pressure margins, compelling manufacturers to optimize supply chains and invest in cost-management measures without sacrificing safety or compliance.

Rise in Modular and Prefabricated Construction: The rise of modular, prefabricated construction is increasing demand for flame-retardant materials that can be integrated during off-site assembly. These components require consistent flame-resistance across modules, fueling demand for precision-grade, brominated retardants—especially in Europe and North America where off-site efficiency is critical.

Expansion in Electric Vehicle Composite Use: Brominated flame retardants are increasingly incorporated in lightweight composite panels and battery housing for electric vehicles. These applications require high thermal stability and thermal runaway protection—leading to rising adoption of advanced brominated additives compatible with composite polymer systems.

Adoption of Reactive Flame Retardant Systems: Manufacturers are launching reactive BFRs that chemically bond during polymer curing. These systems reduce additive migration, enhance long-term stability, and align with regulatory expectations for low-emission materials in consumer electronics and indoor construction products.

Growth in Flame-Retardant Textiles: Textile applications (including upholstery, draperies, and protective workwear) are expanding in use of brominated flame retardants. Explicit performance benchmarks, such as NFPA 701 certification for fabrics, are steering demand toward tailored formulations with enhanced durability and wash-resistance.

The Brominated Flame Retardants Market is segmented based on type, application, and end-user, reflecting the diverse industrial demand for fire protection solutions. By type, the market includes tetrabromobisphenol A (TBBPA), decabromodiphenyl ether (Deca-BDE), hexabromocyclododecane (HBCD), and other derivatives, each offering distinct properties for polymer integration. Applications span electronics, construction, automotive, textiles, and aerospace, with electronics retaining a dominant role due to extensive use in circuit boards and casings. From an end-user perspective, manufacturers catering to consumer electronics and automotive components hold a strong influence on demand, while construction and industrial users are expanding rapidly in alignment with stringent safety codes. Collectively, these segments illustrate how material characteristics and regulatory frameworks guide usage, while evolving preferences for safer and more sustainable solutions are shaping the future adoption of brominated flame retardants.

Tetrabromobisphenol A (TBBPA) holds the largest share within the brominated flame retardants segment, driven by its widespread use in printed circuit boards and electrical housings. Its strong thermal stability and compatibility with epoxy and polycarbonate resins make it a preferred choice in high-volume electronic applications. Decabromodiphenyl ether (Deca-BDE), while facing restrictions in several regions due to environmental concerns, still retains relevance in markets with less stringent regulations, particularly in textiles and plastics where cost-effectiveness is critical. Hexabromocyclododecane (HBCD), traditionally important in insulation foams, has seen declining demand owing to regulatory scrutiny but continues to serve niche construction applications. The fastest-growing type is emerging alternatives and reactive brominated compounds, designed to chemically bind with polymer matrices, thus reducing leaching and addressing regulatory challenges. These innovations not only meet safety standards but also align with sustainability goals, positioning them as the most dynamic category in the type segmentation.

Electronics represent the leading application segment for brominated flame retardants, accounting for extensive use in housings, connectors, and circuit boards. The requirement for reliable flame resistance in compact and heat-sensitive devices underscores their indispensability in this sector. Construction follows closely, where insulation materials, cables, and coatings depend on flame retardants to meet building safety standards. The fastest-growing application is in automotive, particularly electric vehicles, where lightweight composites, battery enclosures, and interior components demand materials with superior fire protection. Textiles, including furnishings and protective workwear, also contribute steadily, benefiting from enhanced wash durability and compliance with fire safety certifications. Aerospace and transportation sectors, though smaller in scale, leverage brominated flame retardants in specialized components where high-performance fire resistance is mandatory. Together, these applications highlight the critical role of flame-retardant integration across diverse industries, driven by technological advancement and regulatory requirements.

Consumer electronics manufacturers are the leading end-users of brominated flame retardants, reflecting the global proliferation of smartphones, laptops, household appliances, and communication systems. Their reliance on TBBPA and related compounds for printed circuit boards and housings reinforces this dominance. The fastest-growing end-user group is the automotive sector, driven by the rapid adoption of electric vehicles that require fire-resistant materials in battery systems and lightweight structural composites. Construction companies represent another major contributor, particularly in insulation, cabling, and prefabricated modules where safety compliance is non-negotiable. The textile industry also plays a niche role, supplying flame-resistant fabrics for both industrial and residential use. Aerospace manufacturers, while a smaller segment, demand highly specialized, high-performance formulations to meet stringent international standards. Collectively, these end-user dynamics illustrate how safety regulations, material innovation, and industry-specific performance needs dictate the adoption of brominated flame retardants across global markets.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, the Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

The dominance of Asia-Pacific is primarily attributed to the high consumption of brominated flame retardants in electronics, automotive, and construction sectors, particularly in China, India, and Japan. Meanwhile, the Middle East & Africa region is witnessing rapid infrastructure development and industrial expansion, creating strong demand for flame retardant solutions. This dual dynamic positions Asia-Pacific as the core hub while signaling emerging opportunities in the Middle East & Africa.

North America held around 21% of the global market share in 2024, with the United States driving most of the demand. The region’s growth is fueled by widespread use of flame retardants in consumer electronics, automotive interiors, and building materials. Regulatory frameworks that promote fire safety compliance are supporting market stability. Additionally, U.S. manufacturers are adopting digital technologies to improve flame retardant formulations, enhancing efficiency and sustainability. Canada is also emerging as a contributor, with its strong construction activities and government support for safer fire protection materials.

Europe accounted for 18% of the global share in 2024, with Germany, the UK, and France being the leading markets. Stringent regulatory bodies, including REACH compliance, are shaping the adoption of brominated flame retardants across the region. Germany is a key player due to its robust automotive and electronics manufacturing base, while France and the UK are seeing demand growth in construction and aerospace. Europe is also adopting advanced manufacturing technologies, driving the production of safer and more efficient flame retardant materials while aligning with sustainability goals.

Asia-Pacific dominated with 42% market share in 2024, making it the largest regional market. China leads the region due to its strong electronics and manufacturing ecosystem, supported by rapid industrialization and construction activities. India is witnessing accelerated adoption in the automotive and building sectors, while Japan maintains a steady demand driven by high-quality electronics production. The region’s large-scale infrastructure expansion and innovation hubs continue to boost market opportunities, making Asia-Pacific the global center for brominated flame retardant consumption.

South America captured around 8% of the global share in 2024, with Brazil and Argentina being the key contributors. Brazil dominates the regional market, supported by large-scale construction and infrastructure development. Argentina is contributing steadily, particularly in the automotive industry. The region benefits from favorable trade policies and increasing demand for safety-compliant materials in urban projects. While its share is comparatively smaller, South America presents opportunities for expansion in fire safety across construction and consumer goods sectors.

The Middle East & Africa accounted for 11% of the global share in 2024 and is projected to be the fastest-growing region. The UAE and Saudi Arabia are driving demand with massive construction projects, while South Africa shows consistent uptake in industrial and residential developments. The oil and gas sector also contributes significantly due to the need for enhanced fire safety standards. Government initiatives supporting infrastructure modernization and regional trade partnerships are further accelerating adoption, making this region an attractive growth hotspot.

China – 28% Market Share

China dominates the brominated flame retardants market due to its strong production base in electronics and large-scale infrastructure development.

United States – 15% Market Share

The U.S. holds a major share driven by high demand from consumer electronics, automotive interiors, and strict fire safety regulations.

The brominated flame retardants market is characterized by a moderately consolidated competitive landscape, with more than 35 active global and regional players operating across diverse industries such as electronics, construction, automotive, and textiles. Leading companies are positioned strongly due to their broad product portfolios, established supply chains, and strong R&D capabilities, enabling them to maintain dominance in key regions. Competitive strategies include product innovation to align with environmental regulations, strategic mergers and acquisitions to expand geographic reach, and joint ventures with downstream manufacturers to secure long-term contracts. Recent years have witnessed an increase in sustainability-driven innovation, with several players introducing eco-friendlier formulations to meet evolving safety standards. In addition, technological advancements in polymer integration and material compatibility have created new opportunities for differentiation. The market remains highly competitive, with top-tier companies competing on quality, compliance, and performance, while regional firms focus on cost efficiency and serving niche applications. Overall, the industry is shaped by continuous innovation, regulatory adaptation, and strategic collaborations aimed at reinforcing global market positioning.

Albemarle Corporation

ICL Group Ltd.

LANXESS AG

Chemtura Corporation

Tosoh Corporation

Nabaltec AG

Shandong Brother Technology Co., Ltd.

Jordan Bromine Company Limited

Weidmann Holding AG

Gulf Resources Inc.

The brominated flame retardants market is experiencing notable advancements in technology, driven by the need to balance fire safety performance with environmental compliance. One of the most significant developments is the improvement of polymer compatibility, enabling brominated flame retardants to be effectively integrated into plastics, textiles, and electronic components without compromising material integrity. Advanced encapsulation technologies are being adopted to enhance dispersion and reduce leaching, extending the product’s functional lifespan. Additionally, there is a growing trend toward synergistic formulations where brominated flame retardants are combined with other additives, such as antimony trioxide or phosphorus-based agents, to deliver superior flame suppression while minimizing total loading levels.

Another key area of technological innovation is the development of low-migration and reactive flame retardants that chemically bond with the polymer matrix, reducing the risk of emissions and improving stability under thermal stress. This is especially critical in applications such as electronics housings and automotive interiors, where durability and regulatory compliance are paramount. Research is also focusing on high-performance brominated epoxy oligomers and polymers, which provide enhanced resistance to ignition and contribute to lightweight material design. Emerging technologies emphasize recyclability and reduced toxicity, with manufacturers increasingly investing in bio-based formulations and advanced material science approaches. Collectively, these innovations are setting new standards for efficiency, safety, and sustainability across industries.

• In February 2023, Albemarle Corporation expanded its bromine production capacity in Jordan to support the rising demand for brominated flame retardants in electronics and building materials, strengthening its position as a leading global supplier.

• In August 2023, ICL Group introduced an advanced range of polymer-compatible brominated flame retardants, designed to reduce migration and improve recyclability, catering to stricter environmental compliance standards in Europe and North America.

• In March 2024, LANXESS AG partnered with a major Asian electronics manufacturer to co-develop high-performance brominated flame retardant solutions optimized for miniaturized consumer electronics and 5G-enabled devices.

• In July 2024, Tosoh Corporation launched a new brominated epoxy oligomer for automotive and aerospace applications, offering superior heat resistance and flame suppression while reducing halogen emissions compared to traditional formulations.

The Brominated Flame Retardants Market Report provides a comprehensive assessment of the industry, covering product types, application areas, end-user segments, regional dynamics, and technological innovations. It evaluates the full spectrum of flame retardant types, including tetrabromobisphenol A (TBBPA), decabromodiphenyl ethane (DBDPE), and brominated epoxy oligomers, analyzing their relevance across consumer electronics, automotive, construction, textiles, and industrial equipment. The report highlights application-specific trends, ranging from printed circuit boards and electrical enclosures to insulation materials and upholstery, illustrating the diverse role of brominated flame retardants in enhancing fire safety standards.

From a geographic perspective, the report covers established markets such as North America and Europe while emphasizing high-growth regions like Asia-Pacific and the Middle East & Africa. Each regional analysis outlines the industrial base, regulatory frameworks, and infrastructure development fueling demand. The study also examines the competitive strategies of leading companies, mapping their positioning in both mature and emerging markets.

In addition, the report addresses ongoing technological transitions, including the adoption of low-migration formulations, encapsulation methods, and reactive compounds that improve safety and sustainability. Insights into supply chain developments, raw material sourcing, and environmental regulations further broaden the report’s scope. By presenting an integrated view of products, applications, technologies, and regional opportunities, the report offers a valuable resource for decision-makers seeking to align strategies with the evolving brominated flame retardants market landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 258.0 Million |

| Market Revenue (2032) | USD 290.6 Million |

| CAGR (2025–2032) | 1.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Albemarle Corporation, ICL Group Ltd., LANXESS AG, Chemtura Corporation, Tosoh Corporation, Nabaltec AG, Shandong Brother Technology Co., Ltd., Jordan Bromine Company Limited, Weidmann Holding AG, Gulf Resources Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |