Reports

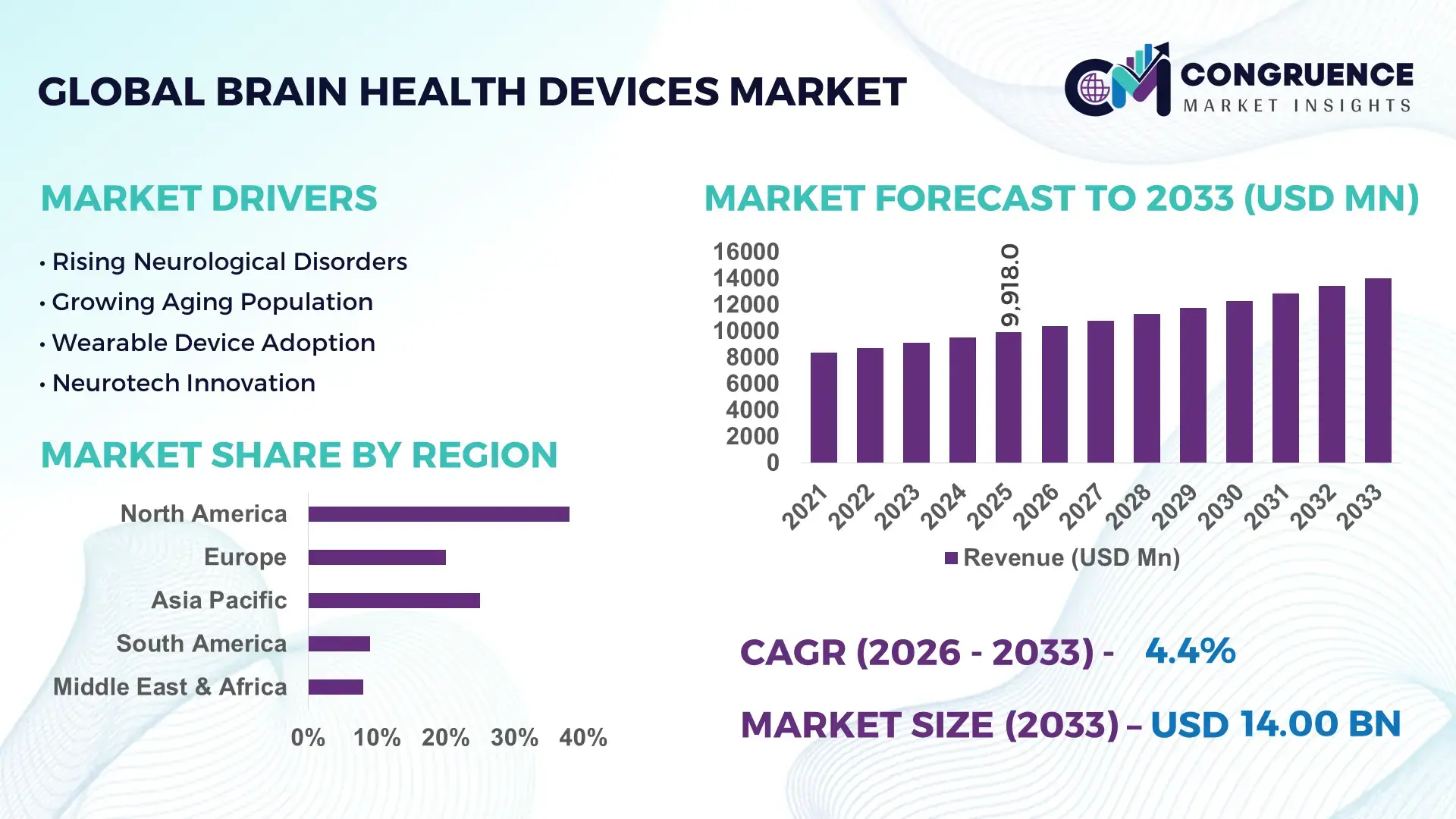

The Global Brain Health Devices Market was valued at USD 9917.99 Million in 2025 and is anticipated to reach a value of USD 13996.76 Million by 2033 expanding at a CAGR of 4.4% between 2026 and 2033. Growth is being driven by expanding deployment of neurostimulation systems, AI-enabled brain monitoring platforms, and rising clinical adoption of non-invasive neurological assessment technologies across cognitive health and neurodegenerative disease management.

The United States remains the dominant country, accounting for approximately 38% of global brain health device deployment, supported by strong neuroscience research funding, advanced healthcare infrastructure, and widespread integration of digital neurology platforms. Germany follows as a key European hub with nearly 9% market share, driven by precision medical device manufacturing and hospital-based neurodiagnostic adoption. In 2026, U.S. healthcare institutions reported over 65% utilization of advanced neurological monitoring systems in major neuroscience centers, significantly higher than several European markets. Continued investments in neurological care have accelerated technology commercialization despite ongoing healthcare budget prioritization linked to aging-population policies across developed economies.

Companies prioritizing AI-enabled diagnostics, scalable neurostimulation portfolios, and high-adoption healthcare markets are positioned to strengthen long-term competitive advantage.

Market Size & Growth: USD 9917.99 million in 2025, reaching USD 13996.76 million by 2033 at 4.4% CAGR, supported by AI-assisted neurological assessment and expanding neurostimulation adoption.

Top Growth Drivers: Neurodegenerative disorder incidence (+12%), digital neurology adoption (+18%), and non-invasive brain monitoring utilization (+15%) continue driving expansion.

Short-Term Forecast: By 2028, diagnostic workflow efficiency improves by 22% while neurological assessment turnaround times decline by 17%.

Emerging Technologies: AI analytics, wearable EEG platforms, and cloud-connected neurostimulation systems improve diagnostic accuracy by 20% and patient monitoring coverage by 25%.

Regional Leaders: North America exceeds USD 5.1 billion, Europe approaches USD 3.7 billion, and Asia-Pacific surpasses USD 3.2 billion, supported by advanced healthcare digitization.

Consumer/End-User Trends: More than 58% of major neurological centers now integrate digital brain-monitoring technologies into routine clinical workflows.

Pilot/Case Example: In 2026, an AI-enabled neurological monitoring deployment reduced diagnostic review times by 28% across participating healthcare facilities.

Competitive Landscape: Leading manufacturers collectively hold approximately 42% share, with competition centered on neurostimulation, EEG, and cognitive assessment technologies.

Regulatory & ESG Impact: Device digitalization programs improved neurological data accessibility by 19% while supporting healthcare efficiency objectives.

Investment & Funding: Global investment exceeded USD 1.4 billion, driven by strategic partnerships, neuroscience innovation programs, and regional expansion initiatives.

Innovation & Future Outlook: Next-generation wearable neurotechnology and predictive brain analytics are expected to improve early neurological risk detection by over 30%.

Brain Health Devices Market demand is increasingly concentrated in neurological diagnostics, cognitive monitoring, neurostimulation therapies, and remote patient management applications. Recent innovation focuses on AI-powered signal interpretation, wearable EEG systems, and connected therapeutic devices that improve clinical workflow efficiency by nearly 20%. An emerging trend is the integration of continuous brain-health monitoring into routine care pathways, supported by evolving neurological care standards and resilient medical technology supply networks, setting the stage for deeper strategic market evaluation.

Brain health devices are becoming strategically important as healthcare systems shift from episodic neurological treatment toward continuous monitoring, early intervention, and precision neurocare. Competition is increasingly centered on data-driven diagnostics, wearable neurotechnology, and scalable neurostimulation platforms. A notable market shift is the modernization of neurological care infrastructure, with hospitals accelerating digital integration programs and remote monitoring deployment. This transition is reshaping procurement priorities and creating new investment opportunities across device manufacturing, software analytics, and connected care ecosystems.

Technology advancement is delivering measurable operational gains. AI-assisted brain monitoring systems can reduce neurological assessment time by approximately 25% compared with conventional manual review processes while improving diagnostic workflow efficiency by nearly 20%. The United States leads large-scale deployment through advanced neuroscience networks, while Japan emphasizes aging-population-focused cognitive monitoring solutions with higher adoption across long-term care facilities. Over the next two to three years, connected neurological monitoring installations are expected to exceed 60% adoption among major specialized neuroscience centers, strengthening demand for interoperable platforms.

A practical example is the integration of wearable EEG monitoring with cloud-based analytics, enabling continuous patient observation outside traditional clinical settings. Companies are expanding strategic partnerships with healthcare providers, investing in software-enabled device portfolios, and prioritizing digital neurology capabilities. Organizations that combine clinical accuracy, scalable deployment, and data intelligence will secure stronger competitive positioning as neurological healthcare delivery continues to evolve.

The primary growth driver is the rapid adoption of digital neurology technologies that support earlier diagnosis, continuous monitoring, and personalized neurological care. More than 65% of leading neuroscience centers now utilize advanced brain-monitoring systems, while AI-assisted neurological assessment platforms improve clinical workflow efficiency by approximately 20%. In the United States, expanding reimbursement support for remote patient monitoring has accelerated deployment of connected neurodiagnostic devices. This structural shift is increasing demand for wearable EEG systems, neurostimulation technologies, and cognitive assessment platforms. Device manufacturers are responding through software integration investments, hospital partnerships, and product innovation programs. A key operational insight is that healthcare providers increasingly evaluate solutions based on long-term patient monitoring capability rather than standalone diagnostic performance, creating competitive advantages for integrated technology ecosystems.

Implementation costs remain a significant structural limitation, particularly for advanced neurostimulation and continuous brain-monitoring platforms. Initial deployment expenses can account for 20–30% of total neurological technology budgets, while system integration requirements often extend implementation timelines by more than 15%. In Germany and several other developed healthcare markets, interoperability challenges between legacy hospital information systems and next-generation neurological devices continue to constrain adoption speed. Component sourcing complexity for specialized sensors and semiconductor-based modules also creates procurement pressure. These factors affect deployment scalability and delay return-on-investment realization. Companies are mitigating risks through localized manufacturing strategies, multi-supplier sourcing agreements, and modular product architectures that reduce integration complexity. Organizations capable of lowering implementation costs gain a meaningful advantage in institutional procurement decisions.

A major opportunity lies in predictive neurological assessment supported by artificial intelligence, wearable monitoring technologies, and cloud-based analytics. Advanced algorithms can improve neurological risk identification accuracy by approximately 30%, while connected monitoring systems reduce follow-up assessment requirements by nearly 18%. Japan's aging demographics and India's expanding digital healthcare infrastructure create attractive deployment environments for next-generation brain health solutions. Policy support for digital health modernization is encouraging broader integration of remote neurological monitoring capabilities. Companies are increasing R&D investments, forming healthcare technology partnerships, and developing software-driven service models that generate recurring value beyond device sales. A notable strategic opportunity is the transition from reactive neurological treatment toward predictive intervention, creating differentiation through data intelligence rather than hardware specifications alone.

Long-term market expansion is challenged by the complexity of scaling neurological data ecosystems across diverse healthcare environments. Brain-monitoring platforms can generate over 40% more patient data than conventional neurological assessment workflows, increasing requirements for storage, analytics, and cybersecurity protection. Shortages of trained neurotechnology specialists remain a concern, with some advanced healthcare facilities reporting workforce gaps exceeding 15% in specialized neurological data interpretation roles. As connected devices become more prevalent, regulatory expectations regarding patient data governance and algorithm transparency continue to evolve. These pressures affect deployment consistency and operational sustainability. Companies must invest in workforce development, cybersecurity infrastructure, and interoperable software frameworks while strengthening partnerships with healthcare institutions. The ability to scale secure and clinically reliable neurological data platforms will become a decisive competitive differentiator.

• AI-Powered Clinical Decision Support Neurology centers are embedding AI-driven interpretation engines into EEG and brain monitoring workflows, reducing review times by nearly 25% and improving diagnostic consistency by 18%. More than 55% of newly deployed neurological monitoring platforms now include automated analytics modules. Hospitals in the United States are prioritizing integrated software-device ecosystems, prompting manufacturers to expand AI partnerships and accelerate algorithm validation programs to improve workflow throughput and clinician productivity.

• Wearable Neurotechnology Expansion Accelerates Wearable brain health devices are transitioning from research settings into routine monitoring environments, with device utilization increasing by approximately 22% and remote neurological observation programs expanding by 19%. Labor shortages in specialized neurology services are encouraging continuous patient monitoring outside traditional facilities. Companies are scaling production capacity, investing in miniaturized sensor technology, and restructuring product portfolios toward subscription-enabled monitoring models that strengthen long-term customer engagement.

• Cloud-Connected Monitoring Infrastructure Cloud-enabled neurological platforms have improved data accessibility by nearly 30% while reducing administrative processing workloads by 15%. Healthcare providers in Japan and Germany are increasingly adopting centralized neurological data architectures to support multi-site clinical operations. Device manufacturers are responding through interoperability investments and enterprise software collaborations. A less obvious shift is the growing preference for platform standardization, which is influencing procurement decisions more than hardware specifications alone.

• Precision Neurostimulation Deployment Growth Advanced neurostimulation systems are achieving treatment personalization improvements of approximately 20%, while device programming efficiency has improved by 16%. Regulatory emphasis on measurable clinical outcomes is encouraging healthcare providers to adopt data-enabled therapeutic platforms. Companies are expanding clinical partnerships, integrating predictive analytics capabilities, and enhancing patient-specific treatment optimization features, creating stronger differentiation in increasingly competitive neurological care environments.

Neurostimulation Devices represent the leading segment due to their established clinical utility, broad neurological treatment applications, and strong integration into hospital-based care pathways. These devices account for an estimated 32% of total deployment activity, supported by expanding use in movement disorders, chronic neurological conditions, and therapeutic intervention programs. Brain Monitoring Devices and EEG Devices remain essential components of diagnostic workflows, with utilization rates exceeding 60% across specialized neuroscience centers. Their operational value lies in diagnostic precision, workflow integration, and compatibility with digital neurological platforms. Manufacturers continue investing in software-enabled functionality and advanced signal processing capabilities to strengthen differentiation.

Wearable Devices are emerging as the fastest-growing segment as healthcare systems prioritize continuous monitoring and decentralized neurological care. Adoption has increased by approximately 22% over the past two years, supported by advances in miniaturization and cloud connectivity. Cognitive Assessment Devices are also gaining traction through AI-assisted screening applications and remote cognitive evaluation programs. Companies are increasing R&D spending, forming technology partnerships, and expanding product ecosystems around connected neurological care. Investment priorities are increasingly shifting from standalone hardware toward integrated monitoring and analytics solutions capable of generating long-term clinical value.

Neurological Disorders remain the dominant application segment as brain health devices are increasingly deployed for diagnosis, monitoring, and therapeutic management of complex neurological conditions. Approximately 45% of device utilization is concentrated within neurological disorder management programs, supported by rising requirements for continuous assessment and personalized intervention. Brain Research continues to represent a mature application area, particularly within specialized research institutions and clinical innovation centers. Sleep Monitoring is also expanding steadily as neurological and sleep-health evaluations become more interconnected through digital diagnostic frameworks.

Mental Health Monitoring is the fastest-growing application segment, driven by increased integration of digital biomarkers, AI-assisted assessments, and remote patient monitoring technologies. Adoption levels have risen by approximately 20%, while healthcare providers report improved patient engagement through connected monitoring tools. Cognitive Training applications are benefiting from personalized neurofeedback systems and digital therapeutic programs that enhance intervention scalability. Companies are responding through platform integration, automation investments, and deployment expansion across outpatient settings. Demand is increasingly shifting toward solutions that combine assessment, monitoring, and intervention capabilities within a unified neurological care environment.

Hospitals represent the dominant end-user segment due to their extensive neurological infrastructure, high patient volumes, and concentration of advanced diagnostic and therapeutic capabilities. Nearly 48% of brain health device deployments occur within hospital environments where integrated neurology departments require comprehensive monitoring, neurostimulation, and assessment solutions. Neurology Clinics continue to strengthen their role through specialized diagnostic services and focused neurological treatment programs. Research Institutes and Academic Institutions remain strategically important because they drive technology validation, clinical trials, and next-generation neurotechnology development.

Home Care Settings are emerging as the fastest-growing end-user category, supported by remote monitoring adoption, connected neurological care models, and wearable device proliferation. Utilization has increased by approximately 24%, while remote neurological observation programs have expanded by nearly 19%. Rehabilitation Centers are also increasing technology adoption to improve recovery monitoring and therapy optimization. Companies are targeting these segments through customized device configurations, software subscription models, healthcare partnerships, and ecosystem-based service offerings. Competitive positioning is increasingly linked to the ability to support both institutional deployment and decentralized neurological care delivery.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.8% between 2026 and 2033.

AI-Driven Neurology Infrastructure Expansion

North America maintains leadership through advanced neurological care infrastructure, high deployment density of neurodiagnostic technologies, and strong integration of AI-enabled clinical workflows. The region represents approximately 39% of global market activity, supported by extensive neuroscience networks and early adoption of connected brain monitoring systems. More than 65% of major neurological centers utilize advanced digital assessment platforms, improving diagnostic throughput and patient monitoring capabilities. Healthcare providers continue expanding remote neurological care programs, while technology developers prioritize software-enabled device ecosystems. Strategic collaborations between hospitals, neurotechnology companies, and digital health providers are accelerating deployment efficiency and strengthening long-term clinical integration across neurological care pathways.

United States Market Outlook: The United States remains the largest national market due to its concentration of neuroscience institutions, advanced reimbursement frameworks, and strong neurotechnology commercialization ecosystem. Large healthcare networks increasingly deploy wearable monitoring systems, AI-assisted diagnostics, and neurostimulation platforms across clinical settings. More than 70% of top-tier neuroscience facilities have integrated digital neurological assessment capabilities into routine workflows. Continued investment in precision neurology, remote patient management, and software-enabled medical devices reinforces the country's position as the primary innovation and deployment hub.

Digital Health Standardization Accelerates Adoption

Europe benefits from healthcare modernization initiatives, strong medical device engineering capabilities, and increasing implementation of digital neurology programs. The region accounts for approximately 28% of global market participation, supported by structured neurological care pathways and growing deployment of connected monitoring technologies. Cross-border digital health initiatives are improving interoperability, while advanced healthcare systems prioritize neurological data integration. Nearly 55% of newly installed neurological monitoring platforms now include cloud-enabled functionality. Manufacturers are expanding partnerships with healthcare providers to improve deployment consistency and support long-term neurological care transformation.

Germany Market Outlook: Germany serves as the region's most influential market due to its medical technology manufacturing strength, advanced hospital infrastructure, and strong clinical research ecosystem. The country has accelerated implementation of AI-supported neurological diagnostics and connected brain monitoring platforms across specialized healthcare facilities. More than 60% of large neurological treatment centers utilize advanced digital neurodiagnostic technologies. Strong engineering expertise and continuous healthcare modernization investments position Germany as a key center for product development, validation, and high-value neurological device deployment.

Large-Scale Deployment and Manufacturing Expansion

Asia-Pacific is emerging as the fastest-expanding market due to healthcare infrastructure investment, growing neurological disease awareness, and expanding neurotechnology manufacturing capabilities. The region contributes approximately 24% of global market activity and is rapidly increasing deployment across hospitals, specialty clinics, and community healthcare networks. Digital healthcare adoption has increased by more than 20% in several major economies, supporting broader implementation of wearable neurological monitoring solutions. Device manufacturers continue expanding regional production capacity and technology partnerships to improve supply resilience and accelerate market penetration.

China Market Outlook: China represents the largest opportunity within Asia-Pacific due to large patient volumes, expanding healthcare infrastructure, and strong domestic medical technology development. National healthcare modernization programs continue supporting adoption of AI-enabled diagnostics and connected monitoring systems. Neurological device installations across major urban healthcare networks have increased by over 18% in recent years. Local manufacturers are strengthening innovation capabilities while forming strategic collaborations with research institutions to accelerate commercialization and improve technology competitiveness.

Specialized Care Access Drives Demand

South America is experiencing increasing demand for neurological assessment and monitoring technologies as healthcare providers expand access to specialized neurological services. The region accounts for approximately 5% of global market activity and is gradually strengthening deployment capabilities through hospital modernization and digital healthcare initiatives. Investments in neurological treatment infrastructure have improved access to advanced diagnostic technologies, while telehealth adoption supports broader patient reach. Deployment growth remains moderated by infrastructure variability and procurement constraints, encouraging suppliers to focus on cost-efficient and scalable solutions.

Brazil Market Outlook: Brazil leads the regional market through its extensive healthcare network, growing neurological treatment capacity, and expanding adoption of digital medical technologies. Large urban healthcare systems are integrating advanced brain monitoring and neurodiagnostic solutions to improve patient management efficiency. More than 50% of major neurological treatment facilities have increased investment in digital diagnostic capabilities. Companies are prioritizing partnerships with healthcare institutions and distributors to improve accessibility and strengthen market penetration across both public and private healthcare environments.

Healthcare Modernization Supports Adoption

The Middle East & Africa market is advancing through healthcare infrastructure modernization, specialized treatment center expansion, and increasing investment in advanced medical technologies. The region contributes approximately 4% of global market activity and demonstrates growing interest in digital neurological assessment capabilities. Government-backed healthcare transformation programs are improving access to advanced diagnostic platforms, while hospital networks continue investing in specialized neuroscience services. Neurological technology deployments have increased by approximately 15% across major healthcare investment hubs. Companies are strengthening local partnerships and service capabilities to support long-term market development.

Saudi Arabia Market Outlook: Saudi Arabia is the most strategically significant market within the region due to large-scale healthcare transformation initiatives and expanding investment in specialized medical services. Neurological care facilities are increasingly adopting advanced monitoring systems, AI-assisted diagnostic tools, and connected healthcare platforms. More than 40% of newly commissioned specialty healthcare projects include digital neurological assessment capabilities. Continued investment in healthcare infrastructure, workforce development, and medical technology partnerships strengthens the country's position as a leading regional destination for advanced brain health device deployment.

The market is led by Medtronic, Abbott Laboratories, Nihon Kohden, Natus Medical, and NeuroPace, which collectively control approximately 48% of global activity. Competition primarily occurs between global neurostimulation leaders and neurodiagnostic specialists, while emerging digital neurology firms challenge established manufacturers through software-enabled platforms. Technology performance, clinical accuracy, deployment speed, and ecosystem integration have become more influential than price alone. AI-enabled monitoring solutions improve workflow efficiency by nearly 20%, while connected neurological platforms reduce data-processing workloads by approximately 15%, creating measurable differentiation. Leading players are expanding through hospital partnerships, product portfolio diversification, and integration of predictive analytics capabilities. Vertical integration strategies are also increasing as manufacturers seek greater control over critical software, sensor, and data-management functions. The competitive shift is moving toward platform-based neurological care rather than standalone devices. Regulatory validation requirements, clinical evidence generation, and healthcare integration complexity remain significant entry barriers. Winning requires clinical credibility, interoperable technology ecosystems, scalable deployment models, and continuous innovation.

Medtronic plc

Abbott Laboratories

Nihon Kohden Corporation

Natus Medical Incorporated

NeuroPace Inc.

Compumedics Limited

Brain Products GmbH

Neuroelectrics

EMOTIV Inc.

Cognionics Inc.

Advanced Brain Monitoring Inc.

Ceribell Inc.

Electrical Geodesics Inc.

Cadwell Industries Inc.

Current technology adoption is centered on AI-enhanced EEG systems, advanced neurostimulation platforms, and cloud-connected brain monitoring devices. AI-assisted neurological analysis improves diagnostic workflow efficiency by approximately 20% while reducing manual interpretation time by nearly 25%. More than 60% of major neuroscience centers now utilize digital brain-monitoring technologies within routine clinical operations. The business impact is significant: faster neurological assessment, improved clinician productivity, and stronger patient management capabilities. Companies with integrated software-hardware ecosystems are gaining competitive advantages over manufacturers focused solely on standalone devices.

Emerging technologies include wearable EEG systems, predictive neurological analytics, and remote cognitive monitoring platforms. Wearable solutions improve continuous monitoring coverage by nearly 22%, while cloud-enabled neurological platforms enhance data accessibility by approximately 30%. Adoption of connected neurological monitoring programs has surpassed 50% among advanced healthcare networks. Compared with conventional episodic assessments, continuous AI-supported monitoring delivers approximately 18% higher detection efficiency for neurological abnormalities. Companies are expanding partnerships with healthcare providers and digital health firms to strengthen interoperability, recurring service models, and long-term clinical integration.

Disruptive innovation is increasingly focused on closed-loop neurostimulation, brain-computer interface development, and real-time adaptive neurological therapies. Between 2026 and 2028, deployment of intelligent neurotechnology platforms is expected to accelerate as healthcare systems prioritize predictive intervention models. Advanced adaptive stimulation systems improve therapy personalization by nearly 20% compared with legacy fixed-program devices. Market leaders investing in AI-driven neurotechnology, connected infrastructure, and scalable data ecosystems will strengthen competitive positioning as neurological care becomes increasingly continuous, automated, and data-centric.

April 2024 – Medtronic received FDA approval for its Inceptiv closed-loop spinal cord stimulator featuring real-time sensing technology that automatically adjusts therapy delivery. The adaptive system enables continuous feedback-driven treatment optimization, strengthening Medtronic’s position in advanced neuromodulation and personalized neurotechnology. Source: https://news.medtronic.com

April 2025 – NeuroPace presented three-year post-approval study data for its RNS System showing an 82% median seizure reduction in adults with drug-resistant focal epilepsy. The clinical outcome reinforces long-term efficacy and supports broader physician adoption of responsive neurostimulation therapies. Source: https://investors.neuropace.com

June 2025 – NeuroPace secured a new financing facility of up to USD 75 million to support commercialization, product expansion, and operational scaling initiatives. The funding strengthens manufacturing flexibility and enhances the company’s ability to expand personalized neuromodulation deployment. Source: https://www.globenewswire.com

January 2026 – Ceribell received FDA Breakthrough Device Designation for its AI-based large vessel occlusion stroke detection solution. The technology extends the company’s EEG platform into acute stroke monitoring and supports faster neurological assessment workflows within hospital environments. Source: https://www.nasdaq.com

This report provides comprehensive coverage of the Brain Health Devices Market across device types, applications, end-users, technology platforms, and key geographic markets. The analysis evaluates EEG Devices, Neurostimulation Devices, Brain Monitoring Devices, Wearable Devices, and Cognitive Assessment Devices while examining demand across Neurological Disorders, Mental Health Monitoring, Cognitive Training, Sleep Monitoring, and Brain Research applications. The study further assesses adoption trends among Hospitals, Neurology Clinics, Research Institutes, Rehabilitation Centers, Home Care Settings, and Academic Institutions. More than 60% of current deployments remain concentrated within advanced neurological care environments, while remote monitoring adoption continues expanding across decentralized care models.

The report delivers strategic insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment concentration, technology adoption patterns, and competitive positioning. It evaluates emerging areas including AI-assisted diagnostics, wearable neurotechnology, predictive neurological analytics, and connected monitoring ecosystems. Coverage includes operational benchmarks, investment priorities, partnership activity, innovation trends, and evolving enterprise strategies, supporting expansion planning, competitive assessment, portfolio optimization, and long-term market decision-making between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 9917.99 Million |

|

Market Revenue in 2033 |

USD 13996.76 Million |

|

CAGR (2026 - 2033) |

4.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Medtronic plc, Abbott Laboratories, Nihon Kohden Corporation, Natus Medical Incorporated, NeuroPace Inc., Compumedics Limited, Brain Products GmbH, Neuroelectrics, EMOTIV Inc., Cognionics Inc., Advanced Brain Monitoring Inc., Ceribell Inc., Electrical Geodesics Inc., Cadwell Industries Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |