Reports

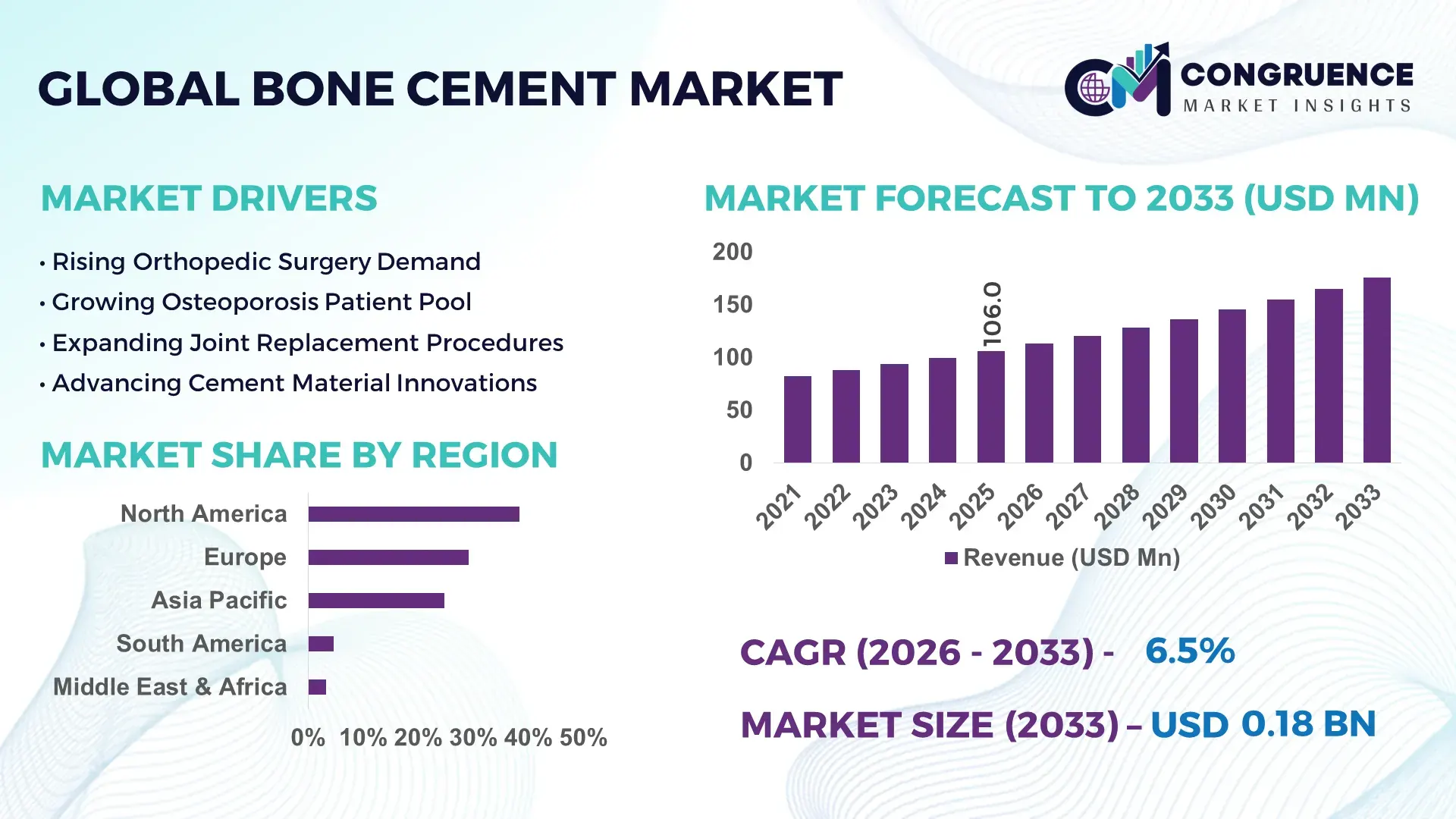

The Global Bone Cement Market was valued at USD 106.0 Million in 2025 and is anticipated to reach a value of USD 175.4 Million by 2033 expanding at a CAGR of 6.5% between 2026 and 2033. Growth is being driven by rising hip and knee arthroplasty volumes, increasing use of antibiotic-loaded bone cement in infection prevention protocols, and expanding orthopedic reconstruction procedures among aging populations.

The United States dominates the global Bone Cement Market with an estimated 32% share, supported by more than 1.3 million annual joint replacement procedures and sustained investments in advanced orthopedic care infrastructure. Compared with Germany, which accounts for nearly 8% of global orthopedic implant demand, the U.S. demonstrates broader adoption of antibiotic-loaded cement technologies and robotic-assisted surgical systems. Post-pandemic surgical backlog recovery and healthcare modernization initiatives have further accelerated procedural volumes, reinforcing the country's leadership position in high-value orthopedic interventions.

Strategically, manufacturers should prioritize advanced infection-resistant formulations, surgeon-focused product differentiation, and partnerships with implant providers to strengthen competitive positioning in high-volume orthopedic markets.

Market Size & Growth: USD 106.0 Million in 2025 reaching USD 175.4 Million by 2033 at 6.5% CAGR, supported by rising joint replacement procedures and advanced orthopedic implant integration.

Top Growth Drivers: Knee arthroplasty volumes up 18%, antibiotic-loaded cement adoption above 25%, and orthopedic surgery center expansion exceeding 12% globally.

Short-Term Forecast: By 2028, operating room efficiency is expected to improve by nearly 15% through standardized cement preparation and delivery systems.

Emerging Technologies: Smart mixing systems, antibiotic-enhanced formulations, and digital surgical planning platforms are improving procedural precision and consistency.

Regional Leaders: North America projected at USD 63 Million, Europe at USD 48 Million, and Asia-Pacific at USD 42 Million, driven by orthopedic modernization and procedure expansion.

Consumer/End-User Trends: More than 60% of cement demand originates from hip and knee replacement procedures in advanced healthcare systems.

Pilot/Case Example: A 2024 orthopedic center deployment of vacuum-mixing technology reduced cement porosity by approximately 20%, improving implant fixation outcomes.

Competitive Landscape: Leading suppliers collectively control about 55% of market activity, with key participants including Zimmer Biomet, Stryker, Heraeus, Smith & Nephew, and DJO.

Regulatory & ESG Impact: Enhanced infection-control protocols contributed to post-surgical complication reductions of nearly 10% across several developed healthcare markets.

Investment & Funding: More than USD 450 Million has been directed toward orthopedic manufacturing upgrades, regional expansion, and biomaterial innovation initiatives.

Innovation & Future Outlook: Next-generation bioactive and antimicrobial cement technologies are reshaping product development amid ongoing global healthcare infrastructure expansion.

Bone Cement Market demand remains concentrated in joint reconstruction, trauma fixation, and revision surgery applications where implant stability is critical. Recent innovations include low-porosity formulations, advanced vacuum-mixing technologies, and enhanced antibiotic-loaded products that improve procedural outcomes. Nearly 25% of newly introduced orthopedic cement products now emphasize infection-mitigation capabilities. Supply-chain localization efforts and stricter surgical quality standards are also influencing procurement strategies, setting the stage for broader strategic market developments.

The Bone Cement Market is becoming strategically important as healthcare providers focus on improving implant longevity, reducing revision procedures, and optimizing surgical efficiency. Rising orthopedic procedure volumes, combined with increasing regulatory emphasis on infection prevention, are pushing hospitals and device manufacturers toward higher-performance cement technologies. At the same time, healthcare supply-chain restructuring is encouraging regional production capabilities to reduce dependency on imported medical materials and improve procurement resilience.

Technology adoption is creating measurable operational advantages. Modern vacuum-mixing systems can reduce cement porosity by up to 20% compared with conventional manual preparation methods, resulting in stronger implant fixation and greater procedural consistency. North America continues to lead in robotic-assisted orthopedic surgery integration, while Asia-Pacific is expanding procedure capacity through hospital modernization programs and growing orthopedic specialist networks. This regional contrast highlights differences in technology maturity and deployment scale.

A practical example is the increasing use of antibiotic-loaded bone cement in revision arthroplasty procedures, where infection-control requirements are particularly stringent. Manufacturers are expanding collaborations with implant producers, increasing localized manufacturing investments, and strengthening distribution networks. Over the next two to three years, wider adoption of advanced cement formulations and digital surgical workflows will reinforce competitive differentiation, improve clinical outcomes, and strengthen long-term positioning across orthopedic care ecosystems.

The increasing volume of joint replacement procedures is accelerating demand for advanced bone cement products across orthopedic care pathways. More than 60% of bone cement consumption is linked to hip and knee arthroplasty applications, while revision surgeries account for nearly 15% of total procedural demand. In the United States, annual joint replacement volumes continue to expand as the population aged over 65 grows and osteoarthritis prevalence rises. Simultaneously, infection-prevention protocols have increased adoption of antibiotic-loaded formulations by over 25% in major orthopedic centers. This procedural shift is improving demand visibility for manufacturers, prompting investments in specialized formulations, surgeon-training programs, and strategic partnerships with implant companies. A key operational insight is that hospitals increasingly prioritize outcome-based procurement rather than product cost alone.

Growing utilization of cementless fixation systems is creating structural pressure on traditional bone cement demand, particularly among younger and more active patient populations. In several developed healthcare markets, cementless knee and hip implant penetration has exceeded 40%, while porous implant technology adoption has increased by nearly 20% over the past five years. Germany and Japan have witnessed increasing surgeon preference for biologic fixation methods supported by long-term osseointegration benefits. This trend directly impacts product volumes in selected orthopedic procedures and intensifies competition among suppliers. To mitigate exposure, manufacturers are diversifying portfolios toward hybrid fixation solutions and advanced antibiotic-loaded products. A critical strategic insight is that product differentiation is increasingly determined by clinical outcomes rather than fixation material alone.

The emergence of bioactive and next-generation antimicrobial bone cement technologies presents a significant opportunity for market participants seeking premium clinical positioning. Research programs indicate that infection-related revision procedures can represent up to 12% of orthopedic revision cases, creating strong demand for enhanced protective formulations. More than 30% of new orthopedic biomaterial development projects now focus on antibacterial performance, drug-eluting technologies, or improved osteointegration characteristics. In the United Kingdom and the United States, healthcare systems are increasingly emphasizing infection-reduction strategies through value-based care models. Companies are responding through R&D collaborations, university partnerships, and biomaterial innovation programs. A notable strategic opportunity lies in combining infection prevention and implant longevity within a single formulation platform, creating differentiated long-term clinical value.

Long-term clinical validation requirements remain a major challenge for bone cement manufacturers seeking sustainable market expansion. Regulatory authorities increasingly require extensive post-market surveillance, while clinical performance monitoring programs have expanded by approximately 20% across several advanced healthcare systems. Product qualification timelines can extend beyond 24 months due to mechanical testing, biocompatibility verification, and infection-control assessments. In the United States, evolving regulatory expectations for orthopedic biomaterials are increasing compliance costs and development complexity. These factors can delay commercialization, constrain innovation cycles, and reduce deployment consistency across healthcare providers. To address these pressures, companies are investing in digital quality systems, clinical research partnerships, and advanced testing infrastructure. The strongest competitive advantage increasingly belongs to manufacturers capable of accelerating evidence generation without compromising regulatory compliance.

• Antibiotic-Loaded Product Expansion Adoption of antibiotic-loaded bone cement has increased by more than 25% in major orthopedic centers as hospitals intensify infection-prevention strategies. Revision arthroplasty programs are driving particularly strong utilization, with infection-management protocols becoming more standardized across surgical networks. Manufacturers are expanding production capacity and strengthening partnerships with healthcare providers to align product portfolios with outcome-focused procurement requirements.

• Vacuum Mixing Standardization Vacuum-mixing systems are becoming standard practice in advanced orthopedic facilities, reducing cement porosity by nearly 20% while improving fixation consistency. Surgical workflow optimization initiatives have shortened preparation times by approximately 10% in high-volume operating environments. In response, suppliers are integrating automated mixing technologies and procedural support services to improve efficiency and strengthen hospital relationships beyond product sales.

• Localized Manufacturing Strategies Supply-chain resilience has become a priority following global logistics disruptions and raw-material availability concerns. Several orthopedic material suppliers have increased regional manufacturing footprints, while procurement teams seek to reduce dependency on single-source suppliers. Localization initiatives have improved delivery reliability by approximately 15% in selected markets. Companies are restructuring distribution networks and expanding inventory management capabilities to enhance operational continuity.

• Smart Orthopedic Integration Digital surgical planning platforms and data-driven orthopedic workflows are increasingly influencing bone cement selection decisions. More than 35% of advanced orthopedic centers now incorporate digital preoperative planning into implant procedures, improving procedural predictability and material utilization. Manufacturers are responding through software partnerships, surgeon education programs, and integrated solution offerings. A notable emerging trend is the convergence of implant, cement, and surgical-planning ecosystems to create more standardized procedural outcomes and stronger provider loyalty.

Polymethyl Methacrylate (PMMA) Cement remains the leading segment, accounting for approximately 62% of global bone cement demand due to its superior fixation strength, predictable handling characteristics, and widespread compatibility with orthopedic implant systems. The segment continues to benefit from extensive use in hip and knee arthroplasty procedures, where immediate mechanical stability remains a critical clinical requirement. Manufacturers are investing in low-porosity formulations and advanced antibiotic-loaded PMMA products to improve implant performance and reduce post-operative complications. Its established regulatory profile and strong surgeon familiarity further reinforce its dominant market position. Calcium Phosphate Cement represents the fastest-growing segment, supported by increasing demand for bioactive materials capable of promoting bone regeneration. Adoption has expanded by nearly 18% over the past three years in trauma and vertebral augmentation procedures. While Glass Polyalkenoate Cement and other specialty formulations occupy smaller shares, they are attracting attention in niche orthopedic applications requiring enhanced biological integration. Companies are expanding biomaterial research partnerships and accelerating innovation programs, reflecting a gradual shift toward next-generation bone repair technologies and value-added clinical outcomes.

Arthroplasty is the largest application segment, representing approximately 68% of total bone cement utilization worldwide. The segment benefits from rising volumes of hip and knee replacement procedures, increasing life expectancy, and growing demand for mobility-restoration treatments. Cemented fixation remains particularly important in elderly patient populations where immediate implant stabilization is required. Healthcare providers continue to prioritize advanced cement formulations that improve fixation durability and support long-term implant performance. As procedure complexity increases, suppliers are expanding product portfolios focused on infection prevention and optimized surgical handling characteristics. Vertebroplasty and kyphoplasty are emerging as the fastest-growing applications, with procedure adoption increasing by nearly 15% in several developed healthcare systems due to the growing incidence of osteoporosis-related vertebral fractures. Trauma procedures also contribute steadily as hospitals seek efficient fixation solutions for complex orthopedic injuries. Manufacturers are responding by developing specialized formulations tailored to minimally invasive procedures, while expanding training initiatives to improve deployment consistency. Demand is increasingly shifting toward application-specific products that deliver measurable procedural and clinical advantages.

Hospitals represent the dominant end-user segment, accounting for approximately 72% of global bone cement consumption. Their leadership stems from high surgical volumes, advanced orthopedic infrastructure, and access to specialized surgical teams capable of performing complex joint reconstruction procedures. Large hospital networks continue to consolidate procurement activities, increasingly favoring suppliers that offer integrated product support, surgeon training, and infection-management solutions. This concentration of purchasing power is encouraging manufacturers to strengthen long-term institutional partnerships and expand clinical support capabilities. Specialty orthopedic centers are emerging as the fastest-growing end-user category, with procedure volumes increasing by nearly 16% as healthcare systems seek greater efficiency and shorter patient recovery pathways. Ambulatory surgical centers are also gaining traction for selected orthopedic procedures due to lower operating costs and streamlined care delivery models. Companies are targeting these facilities through customized product offerings, flexible pricing strategies, and dedicated service programs. The evolving buyer landscape indicates that future competitive success will depend on the ability to address both large-scale hospital demand and rapidly expanding specialized care networks.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2026 and 2033.

North America maintains its leading position through high orthopedic procedure volumes, widespread adoption of cemented joint replacement techniques, and strong integration of advanced surgical technologies. The region accounts for nearly 38.4% of global bone cement demand, supported by a mature healthcare infrastructure and increasing use of antibiotic-loaded formulations. More than 1.3 million hip and knee replacement procedures are performed annually across the United States, creating consistent demand for fixation materials. Hospitals are increasingly implementing robotic-assisted orthopedic surgery platforms and digital surgical planning tools, improving procedural accuracy and material utilization. Manufacturers continue expanding clinical support programs and surgeon training partnerships to strengthen market penetration and product differentiation.

United States Market Outlook: The United States represents the largest national market due to its extensive orthopedic care network, high surgical throughput, and strong reimbursement framework. More than 70% of orthopedic procedures involving bone cement are conducted in large hospital systems and specialized orthopedic centers. The country also leads in the adoption of antibiotic-loaded bone cement and robotic-assisted arthroplasty technologies. Continued investment in outpatient orthopedic surgery infrastructure and advanced implant systems is reinforcing long-term demand for premium bone cement formulations and value-added clinical solutions.

Europe accounts for approximately 29.1% of global market activity and benefits from established orthopedic care systems, high procedural quality standards, and widespread access to joint replacement surgery. The region's market is shaped by increasing revision arthroplasty volumes and growing emphasis on infection prevention protocols. Healthcare providers are prioritizing evidence-based procurement, driving demand for clinically validated bone cement products. Advanced hospital networks across Germany, France, and the United Kingdom continue investing in surgical modernization programs. In addition, the adoption of vacuum-mixing systems and low-porosity formulations has increased by nearly 20% within major orthopedic institutions, improving implant fixation consistency and procedural outcomes.

Germany Market Outlook: Germany serves as the region's most influential market due to its strong orthopedic manufacturing ecosystem and high concentration of specialized surgical facilities. The country performs hundreds of thousands of joint replacement procedures annually and maintains one of Europe's largest orthopedic implant markets. Strong collaboration between hospitals, implant manufacturers, and biomaterial developers supports continuous innovation. German healthcare providers are also among the earliest adopters of advanced infection-control technologies, creating favorable conditions for premium bone cement solutions.

Asia-Pacific is emerging as the fastest-growing regional market, supported by expanding healthcare infrastructure, rising orthopedic procedure volumes, and increasing access to advanced surgical treatments. The region contributes approximately 24.7% of global demand, with significant growth driven by aging populations and increasing healthcare expenditure. Hospital modernization initiatives across China, India, and South Korea are improving access to joint reconstruction procedures. Orthopedic surgery volumes have expanded by more than 15% in several major urban healthcare systems over the past few years. Manufacturers are increasing local production capabilities, strengthening distribution networks, and forming strategic partnerships to support growing procedural demand and improve supply-chain responsiveness.

China Market Outlook: China remains the region's largest market due to its substantial patient base, rapidly expanding healthcare infrastructure, and growing orthopedic implant industry. The country continues to increase investments in tertiary hospitals and advanced surgical facilities. More than 35% of newly established orthopedic specialty centers in Asia-Pacific are located in China, reinforcing procedural capacity growth. Domestic manufacturers are also accelerating biomaterial innovation and production expansion, improving local availability while reducing dependence on imported orthopedic products.

South America represents approximately 4.6% of global market demand and is experiencing steady growth as healthcare systems improve access to orthopedic care. Rising rates of osteoarthritis and musculoskeletal disorders are contributing to increased procedure volumes, particularly in major urban centers. Public and private healthcare providers are expanding orthopedic surgery capacity while investing in modern surgical equipment and implant technologies. However, procurement budget constraints and uneven healthcare infrastructure continue to influence adoption rates across several countries. Manufacturers are responding through distributor partnerships, localized supply strategies, and cost-optimized product offerings designed for value-conscious healthcare environments.

Brazil Market Outlook: Brazil is the region's largest and most strategically important market due to its extensive hospital network and growing orthopedic procedure base. The country accounts for more than 45% of South America's orthopedic surgery activity and continues to invest in healthcare modernization initiatives. Large metropolitan healthcare systems are increasingly adopting advanced arthroplasty techniques and infection-control protocols. Market participants are strengthening local distribution networks and expanding physician education programs to improve procedural consistency and support broader product adoption.

The Middle East & Africa region accounts for approximately 3.2% of global market activity and is increasingly influenced by healthcare infrastructure expansion and specialist care development. Governments and private healthcare operators are investing in advanced hospital facilities, orthopedic centers, and surgical technology upgrades. Growing medical tourism activity in selected countries is further supporting demand for high-quality orthopedic procedures. Several healthcare modernization projects have increased orthopedic treatment capacity by more than 10% in leading healthcare hubs. Manufacturers are leveraging regional partnerships and distributor networks to improve market access and strengthen supply reliability.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through substantial healthcare investment, hospital expansion programs, and ongoing healthcare transformation initiatives. The country continues to develop specialized orthopedic care facilities as part of broader healthcare modernization efforts. Advanced tertiary hospitals are expanding joint replacement capabilities and adopting internationally recognized surgical standards. Increasing orthopedic specialist availability and investment in digital healthcare infrastructure are strengthening procedural efficiency while creating favorable conditions for the adoption of advanced bone cement technologies.

The Bone Cement Market is characterized by competition between global orthopedic biomaterial leaders such as Heraeus Medical, Zimmer Biomet, Stryker, Smith & Nephew, and Arthrex, alongside regional biomaterial suppliers competing primarily on pricing and distribution reach. The top five players collectively control approximately 55–60% of global market activity, creating a moderately consolidated structure. Competition centers on clinical performance, infection-prevention capability, surgeon preference, and supply reliability rather than price alone. Antibiotic-loaded formulations command adoption rates nearly 25% higher in revision procedures, while advanced vacuum-mixing technologies reduce porosity by up to 20%, creating measurable differentiation. Companies are strengthening positions through acquisitions, biomaterial innovation, manufacturing expansion, and strategic hospital partnerships. The competitive landscape is shifting toward bioactive and infection-management technologies, while regulatory approvals and long-term clinical validation remain major entry barriers. Winning requires proven clinical evidence, surgeon loyalty, robust supply chains, and differentiated biomaterial innovation.

Smith & Nephew

Arthrex

Enovis

Tecres S.p.A.

Teknimed

Meril Life Sciences

Aesculap

Medtronic

Exactech

Bone cement technology is evolving from conventional fixation materials toward multifunctional biomaterial platforms that improve implant longevity and infection management. Antibiotic-loaded bone cement has become a standard technology in many revision procedures, with adoption exceeding 30% in advanced orthopedic centers. Compared with traditional non-antibiotic formulations, dual-antibiotic systems have demonstrated infection-risk reductions exceeding 20% in selected high-risk applications. This shift is providing hospitals with measurable reductions in revision burdens while improving long-term clinical outcomes.

Advanced vacuum-mixing systems represent another major technological transition. Modern mixing platforms reduce cement porosity by approximately 15–20% compared with manual preparation methods, resulting in stronger mechanical fixation and improved consistency. Digital surgical planning tools are also increasingly integrated into arthroplasty workflows, with more than 35% of high-volume orthopedic centers incorporating preoperative digital planning. Companies that combine implant systems, cement technologies, and workflow optimization tools gain stronger competitive positioning through procedural standardization and surgeon adoption.

Between 2026 and 2028, bioactive calcium phosphate technologies, drug-eluting biomaterials, and 3D-printed bone substitute solutions are expected to reshape orthopedic reconstruction strategies. Manufacturers investing in regenerative biomaterials and infection-prevention technologies will benefit most from the transition toward outcome-focused orthopedic care. Early adopters are positioned to secure stronger clinical differentiation, broader procurement acceptance, and enhanced long-term market relevance.

October 2025 – Heraeus Medical expanded its orthopedic biomaterials portfolio through the integration of INNOTERE and launched the heracure product line featuring calcium-phosphate bone regeneration solutions and proprietary 3D-printed biomaterials. The move broadened its regenerative orthopedics footprint beyond traditional fixation products. Source: www.heraeus-medical.com

September 2025 – Heraeus Medical LLC acquired Synthecure®, a fully synthetic calcium sulfate bone void filler platform focused on infection management applications. The acquisition expanded its bioresorbable portfolio and strengthened positioning in trauma surgery and bone defect treatment markets.

July 2025 – Heraeus Medical announced new long-term registry findings showing PALACOS® R+G bone cement achieved a 1.8% revision rate versus 3.9% for comparable products in knee arthroplasty. The data reinforced its clinical differentiation strategy and evidence-based market positioning.

November 2024 – Zimmer Biomet received FDA approval for the Oxford® Cementless Partial Knee, reporting improved fixation and operating-room efficiency versus cemented alternatives. The approval accelerated the industry's transition toward cementless orthopedic solutions and intensified competitive pressure on conventional bone cement suppliers.

The Bone Cement Market Report provides comprehensive coverage of orthopedic fixation materials used across arthroplasty, vertebroplasty, kyphoplasty, trauma management, and related reconstruction procedures. The analysis evaluates major product categories including PMMA cement, calcium phosphate cement, antibiotic-loaded formulations, and emerging biomaterial alternatives. More than 60% of current demand remains concentrated in joint replacement procedures, while increasing adoption of advanced infection-management technologies is reshaping product development priorities. The report assesses hospitals, orthopedic centers, and ambulatory surgical facilities as key end-user groups influencing procurement and deployment trends.

The study further examines market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment intensity, technology adoption, and competitive positioning. Coverage includes biomaterial innovation, vacuum-mixing systems, infection-prevention technologies, regenerative bone substitutes, and digital orthopedic workflow integration. Strategic insights support investment evaluation, product expansion planning, competitive benchmarking, partnership development, and long-term market positioning through 2033, enabling stakeholders to identify high-priority growth opportunities and evolving industry requirements.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 106.0 Million |

| Market Revenue (2033) | USD 175.4 Million |

| CAGR (2026–2033) | 6.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Heraeus Medical; Zimmer Biomet; Stryker; Smith & Nephew; Arthrex; Enovis; Tecres S.p.A.; Teknimed; Meril Life Sciences; Aesculap; Medtronic; Exactech |

| Customization & Pricing | Available on Request (10% Customization Free) |