Reports

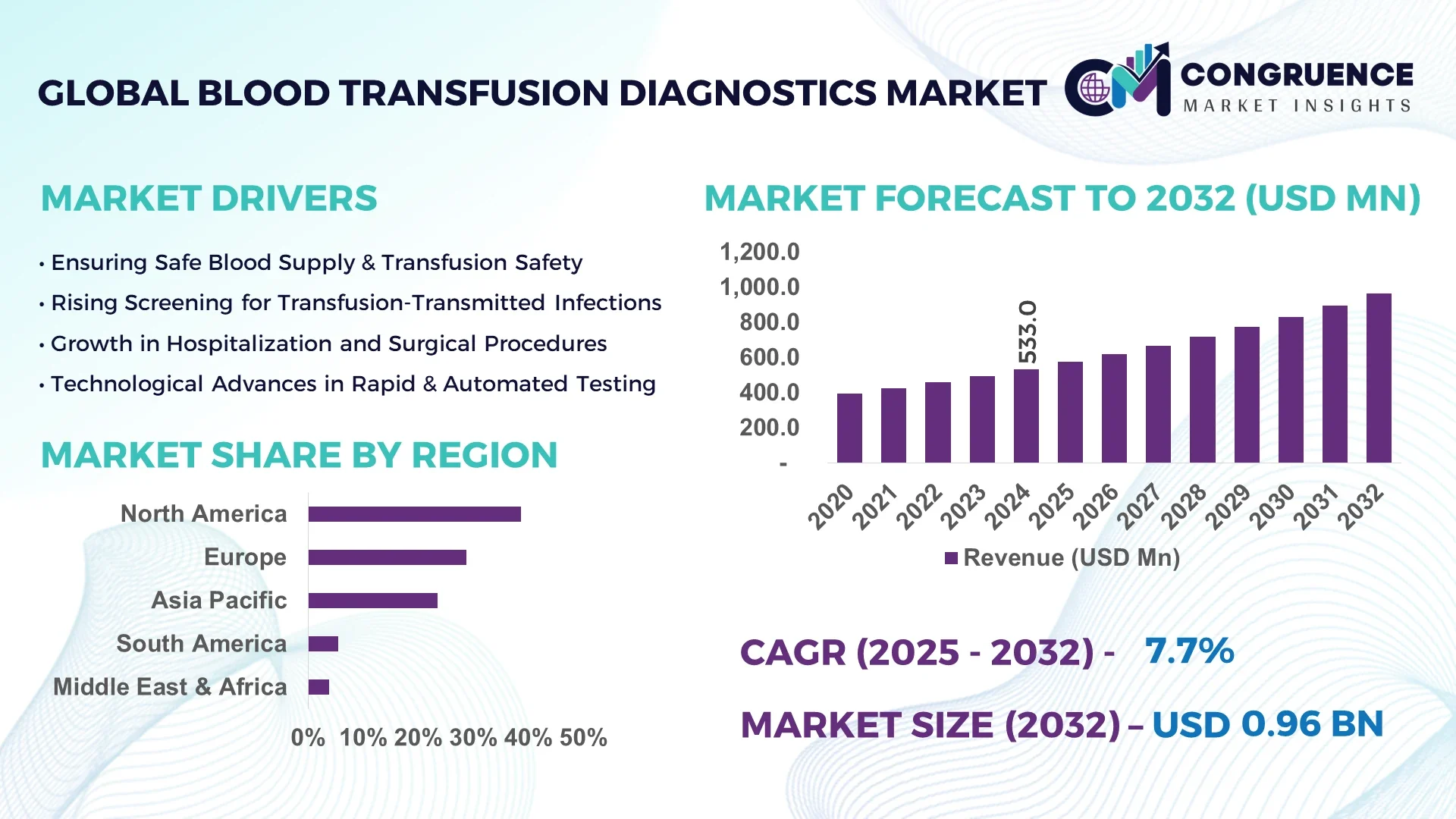

The Global Blood Transfusion Diagnostics Market was valued at USD 533.0 Million in 2024 and is anticipated to reach a value of USD 964.8 Million by 2032, expanding at a CAGR of 7.7% between 2025 and 2032.

The United States holds a leading role in the Blood Transfusion Diagnostics Market. The country maintains high production standards in diagnostic instruments, substantial investment in automated blood screening platforms in large hospital networks, and frequent deployment of nucleic acid and serology-based testing across blood banks. Major diagnostic centers in the U.S. have integrated state-of-the-art workflows for donor management and compatibility testing.

Globally, the Blood Transfusion Diagnostics Market is showing consistent momentum across hospital laboratories, blood banks, and national screening programs. Reagents and kits account for a substantial portion of usage, particularly in ABO/Rh grouping, antibody screening, and extended phenotyping. Molecular testing platforms are advancing rapidly, offering high sensitivity for infectious markers. Regulatory mandates for transfusion safety and growing disease awareness are driving standardized testing protocols. Economic drivers include rising surgical volumes and trauma care needs in aging populations. Regionally, adoption rates are higher in North America and Europe due to established infrastructure, while Asia-Pacific and Latin America are increasing diagnostics uptake with expanding health budgets. Emerging trends involve automation of serological platforms, deployment of microfluidic point-of-care devices, and adoption of pathogen-reduction technologies to ensure safe blood components. Looking ahead, integration of multiplex molecular panels and connected diagnostic suites is expected to strengthen workflow efficiency and patient safety.

Artificial intelligence is fundamentally transforming the Blood Transfusion Diagnostics Market, enhancing accuracy, speed, and decision support across critical domains. AI-driven models now power predictive diagnostics, enabling blood banks and hospital laboratories to forecast transfusion needs in advance based on patient clinical data. For instance, a meta-model trained on over 72,000 ICU patient records demonstrated an AUROC of 0.97 and an accuracy of 0.93 in predicting 24-hour transfusion requirements—delivering operational efficiencies and better resource alignment. Additionally, AI is automating quality control for reagent kits and instrument calibration, reducing human error and improving batch consistency. Automated image-based analysis platforms are reading serological slides and blood smear tests with advanced pattern recognition, cutting result turnaround time by up to 40%.

In donor screening operations, AI-powered systems are optimizing donor selection and scheduling by analyzing historical donation records, infection risk, and demographic trends. This approach helps reduce shortages and improve engagement during high-demand periods. AI also supports transcription and compatibility validation workflows in cross-matching tests, detecting potential mismatches earlier. As a result, the Blood Transfusion Diagnostics Market is evolving toward intelligent, automated operations—reducing staffing load, improving safety, and enhancing throughput without compromising diagnostic integrity. Suppliers that adopt AI-enabled instrumentation and software platforms can differentiate their offerings and build deeper traction with healthcare institutions prioritizing precision transfusion medicine.

“In January 2025, Emory University researchers deployed a machine learning-based meta-model on ICU data comprising 72,072 patients, achieving AUROC of 0.97, accuracy of 0.93 and F1-score of 0.89 in predicting necessity for blood transfusion within 24 hours.”

The Blood Transfusion Diagnostics Market is driven by increasing demand for safe transfusion practices, particularly in acute care, surgical procedures, and chronic disease management. Hospitals and blood banks prioritize compatibility testing and infectious disease screening to mitigate transfusion-transmitted reactions, driving continuous procurement of assays, reagents, and automated instruments. Innovations in multiplex molecular platforms, microfluidic diagnostics, and high-throughput serology systems are enhancing operational efficiency and sample accuracy. At the same time, regulatory frameworks in regions like North America and Europe enforce robust standards for pre-transfusion testing, influencing vendor requirements and product design. Supply chain resilience, instrument maintenance, and cost of consumables remain critical influences on purchasing decisions.

Rising global incidence of surgeries, trauma cases, maternal health interventions, and chronic blood disorders is fueling the demand for reliable blood transfusion diagnostics. Hospitals conduct millions of ABO/Rh typing and antibody screening tests annually to ensure compatibility. With blood donation and transfusion rates increasing in aging and urbanizing regions, laboratories are procuring more test kits and upgrading instrumentation. This continuous volume requirement reinforces the demand for durable reagents, rapid cross-matching tools, and efficient workflows to manage higher throughput without compromising safety.

Advanced diagnostic instruments and consumables for blood transfusion testing require significant capital investment, limiting adoption in resource-constrained settings. Automated molecular platforms and high-sensitivity kits incur higher operating expenses and maintenance overhead. Smaller clinics and rural blood banks often rely on manual serological methods due to budget limitations. Additionally, regulatory certification and quality assurance measures for instruments add compliance costs. Fluctuating reagent pricing further impacts affordability, especially where procurement needs exceed local financing capacity.

Emerging opportunities in the Blood Transfusion Diagnostics Market revolve around point-of-care testing platforms and pathogen-reduction systems. Compact molecular and microfluidics-based devices offer rapid compatibility testing in remote or emergency settings. Simultaneously, pathogen reduction technologies—such as UV and riboflavin-based treatment for blood components—are gaining traction to eliminate transfusion-transmissible infections like HIV, Zika, and malaria. As healthcare systems seek safer blood workflows, suppliers offering integrated testing and pathogen-reduction solutions can address unmet needs in both developed and emerging markets.

Blood transfusion diagnostics are subject to stringent regulatory oversight, particularly for assays used in infectious disease screening and donor compatibility testing. In the U.S., the FDA mandates full quality system compliance and reporting for many laboratory-developed assays. Similar oversight exists in Europe under IVDR. Obtaining approvals for NAT-based tests, automated platforms, and novel diagnostic methods requires substantial validation and documentation. In addition, variations in testing protocols across regions create fragmentation, complicating global product launches. The burden of regulatory compliance can delay time-to-market and increase development costs for diagnostic manufacturers.

Rise in Automated Molecular and Serology Platforms: Laboratories worldwide are installing integrated systems capable of performing both serological and NAT-based screening simultaneously. In 2024, several centralized blood banks processed over 1 million sample tests monthly using fully automated platforms that reduced manual intervention by 60%.

Growth in Predictive Transfusion Modeling with AI: Healthcare systems are deploying AI models based on large clinical datasets to forecast ICU transfusion needs. In early adopter hospitals, blood order accuracy improved by 35%, reducing emergency stock wastage and optimizing logistics.

Expansion of Portable, Point-of-Care Diagnostics: Compact testing devices for blood typing and infectious markers designed for mobile clinics and emergency triage have improved on-site decision-making. In field trials, these platforms produced results in under 25 minutes, aiding rapid compatibility assessments.

Implementation of Pathogen-Reduction Technologies: Blood banks in Europe and North America are increasingly using pathogen-reduction systems that treat plasma and platelets using riboflavin-UV technology. This innovation reduced instances of transfusion-transmitted infections by nearly 85% in facilities adopting the method mid-2024.

The Blood Transfusion Diagnostics Market is segmented based on type, application, and end-user. These segments play a crucial role in determining diagnostic approaches, technology preferences, and operational priorities across healthcare settings. The type segment comprises various diagnostic methods such as serological assays, nucleic acid testing (NAT), and pathogen reduction technologies—each aligned with safety and accuracy imperatives. Applications are diverse, covering disease screening, blood group typing, cross-matching, and transfusion monitoring. These address both routine and high-risk transfusion scenarios. In terms of end-users, hospitals dominate due to high patient volumes and urgent care needs, while standalone blood banks and diagnostic laboratories contribute significantly by managing centralized testing operations. Each of these segments is shaped by technological innovation, regulatory demands, and healthcare infrastructure developments. Notably, automation, precision, and turnaround time are emerging as key decision-making parameters across all segments, influencing procurement behavior and long-term investment strategies in blood diagnostics.

Serological assays currently dominate the Blood Transfusion Diagnostics Market due to their widespread adoption, ease of implementation, and compatibility with legacy infrastructure in hospitals and blood banks. These tests are foundational in determining ABO/Rh blood grouping and performing antibody screening for transfusion compatibility. Their established reliability and lower operational cost have secured their leading position across both developed and emerging regions. However, nucleic acid testing (NAT) is emerging as the fastest-growing type. NAT offers superior sensitivity in detecting transfusion-transmissible infections such as HIV, HCV, and HBV during the early window period, thus enhancing transfusion safety. As regulatory bodies and national health programs push for zero-risk blood supplies, NAT platforms are being adopted more widely, particularly in urban and high-volume settings. Other types, including microarray-based diagnostics and pathogen reduction technologies, are gaining niche relevance. These are being integrated into specialized workflows, particularly where rapid molecular profiling or contamination mitigation is critical. Their uptake is expected to grow steadily with increasing emphasis on blood component safety and diagnostic precision.

Among the various applications, infectious disease screening holds the largest share in the Blood Transfusion Diagnostics Market, owing to its central role in ensuring the safety of transfused blood. Hospitals and blood banks must comply with strict mandates to screen for multiple viral, bacterial, and parasitic infections before releasing blood products. The rising incidence of transfusion-transmissible diseases across regions has reinforced this application as a core function of diagnostic workflows. In contrast, compatibility testing is the fastest-growing application area. This includes cross-matching, extended phenotyping, and antibody identification procedures critical for surgical, trauma, and chronic care patients. Demand for these tests is increasing as healthcare providers adopt personalized transfusion strategies, especially in oncology and transplant units. Blood grouping, while a mature application, remains essential across all transfusion centers and often forms the first line of testing in both manual and automated environments. Monitoring post-transfusion reactions, although a smaller application segment, is gaining importance in quality control and adverse event management programs.

Hospitals represent the leading end-user segment in the Blood Transfusion Diagnostics Market, driven by high patient volumes, diverse clinical requirements, and the need for rapid turnaround in emergency and surgical departments. These facilities operate on-site transfusion laboratories or collaborate with centralized diagnostic networks to manage large-scale compatibility testing and infection screening. The fastest-growing end-user category is standalone blood banks. With the expansion of voluntary blood donation programs and the consolidation of blood screening operations, these institutions are rapidly upgrading their testing capabilities. Investments in automation and NAT-based systems are particularly high in this segment to improve throughput and safety. Diagnostic laboratories also contribute to market demand, especially in outsourced testing environments where blood banks or clinics lack in-house diagnostic capacity. Military healthcare units, maternal care centers, and organ transplant programs represent additional end-users that influence demand trends by requiring highly accurate and rapid diagnostic support for critical care transfusions.

North America accounted for the largest market share at 38.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

The dominance of North America is attributed to its robust healthcare infrastructure, high blood donation rates, and the presence of leading diagnostic technology providers. Meanwhile, Asia-Pacific’s rapid market expansion is driven by rising healthcare investments, growing awareness around transfusion safety, and a burgeoning population with increased access to advanced diagnostics. Europe held a strong secondary position, owing to stringent safety regulations and nationalized healthcare systems. Other regions like South America and the Middle East & Africa are also showing stable growth due to improvements in healthcare access and supportive government initiatives. Regional dynamics are further influenced by public-private partnerships, diagnostic technology adoption rates, and the expansion of blood banks and transfusion centers in both urban and semi-urban areas.

The North America Blood Transfusion Diagnostics Market held a market share of 38.6% in 2024, making it the leading regional contributor globally. The region benefits from highly developed healthcare systems and a well-organized network of blood banks and hospitals, particularly in the United States and Canada. A major driver of demand comes from the high volume of surgeries, trauma care, and chronic disease management requiring transfusion diagnostics. Government bodies such as the FDA have implemented rigorous regulatory frameworks to ensure transfusion safety, further boosting demand for advanced testing platforms. Additionally, the adoption of next-generation technologies like nucleic acid amplification testing and automated blood screening systems is prevalent across large hospitals and diagnostic laboratories. Digital transformation in diagnostics, including AI-integrated workflows and electronic blood bank management systems, is also accelerating the efficiency and reliability of transfusion diagnostics in the region.

Europe accounted for approximately 28.7% of the global market share in 2024, maintaining its position as a significant player in the Blood Transfusion Diagnostics Market. Germany, the UK, and France are the key countries contributing to regional market strength due to their sophisticated healthcare systems and advanced laboratory networks. Regulatory bodies such as the European Medicines Agency (EMA) and national health services have implemented strict quality control standards for blood safety, fostering higher adoption of reliable diagnostic solutions. The region also promotes sustainability through eco-friendly diagnostic technologies and circular economy initiatives within healthcare. Furthermore, Europe is witnessing increased deployment of molecular diagnostics and multiplex platforms in transfusion settings, supported by innovation clusters in biomedical research. The integration of automation and smart diagnostics into hospital systems is helping streamline operations and reduce human error, positioning Europe as a technologically advanced market.

Asia-Pacific is the fastest-growing region in the global Blood Transfusion Diagnostics Market and ranked third in terms of overall volume in 2024. Key countries such as China, India, and Japan are driving significant demand due to expanding healthcare infrastructure, rising disease burden, and increasing public awareness around safe transfusion practices. The region is also experiencing rapid urbanization and economic development, which is translating into better access to healthcare services and diagnostic technologies. Governments in China and India are investing heavily in hospital networks and blood banking capabilities, enhancing the availability and safety of transfusion services. Local manufacturers are scaling production to meet regional needs, while international companies are also entering strategic partnerships to expand their market footprint. Technological advancements such as point-of-care diagnostics, AI-based analyzers, and mobile blood screening units are becoming prominent across both rural and urban settings.

South America’s Blood Transfusion Diagnostics Market is gaining traction with Brazil and Argentina leading the region in terms of market share in 2024. The region is seeing a growing emphasis on public healthcare development and donor recruitment campaigns aimed at improving blood availability and safety. Brazil, in particular, has made significant progress in establishing a national transfusion system supported by government initiatives and international collaborations. Argentina follows with considerable investments in diagnostic automation and screening infrastructure. Despite some infrastructural limitations, the region is adopting advanced diagnostic technologies, including NAT and automated serological testing, especially in urban centers. Trade agreements and healthcare reform policies across the continent are fostering market growth. Additionally, the growing burden of infectious diseases and road traffic accidents in the region is creating sustained demand for reliable and timely transfusion diagnostics.

The Middle East & Africa Blood Transfusion Diagnostics Market is witnessing steady growth, with countries such as the UAE and South Africa leading regional adoption. In 2024, the region’s growing demand is supported by the expansion of tertiary healthcare facilities and the introduction of national blood safety regulations. Economic diversification strategies in Gulf nations have resulted in significant investments in the healthcare sector, particularly in diagnostics and laboratory services. South Africa has developed a strong network of blood banks and is focusing on eliminating transfusion-transmissible infections through stringent testing. Technological modernization, including automated immunoassay systems and digital data integration for donor tracking, is being gradually implemented. Furthermore, trade partnerships and international aid programs are helping less developed parts of the region improve diagnostic capacity. Increasing public-private collaborations are also contributing to the adoption of advanced transfusion diagnostics across both urban and remote areas.

United States – 32.5% Market Share

High demand from hospital networks and leadership in diagnostic technology innovation position the United States as the global market leader in blood transfusion diagnostics.

China – 14.8% Market Share

China's expanding healthcare infrastructure, government-led blood safety initiatives, and rising patient population contribute to its dominant presence in the Asia-Pacific market.

The Blood Transfusion Diagnostics Market features a highly dynamic ecosystem with over 45 active global competitors ranging from multinational diagnostics firms to niche biotech companies. Market leaders differentiate themselves with strong instrument portfolios, reagent kits, and integrated diagnostic solutions for blood typing, infectious disease detection, and donor screening.

Key strategic initiatives include recent launches of automated, high-throughput screening platforms capable of processing over 10,000 samples per day. Several firms have entered into joint ventures with hospital networks and national blood services to expand diagnostic outreach. Mergers have also reshaped the landscape, combining molecular diagnostics specialists with established serology providers to offer end-to-end solutions.

Innovation trends are central to competition. Top companies are investing in multiplex molecular assays, microfluidic and point-of-care devices, and pathogen-reduction integration. Suppliers are embedding digital dashboards and AI-enabled analytics in their platforms to improve batch consistency and traceability. Industry positioning varies: some focus on high-end platform sales to large hospitals, while others target volume reagent kits for blood banks. Overall, competitive pressure is high, with differentiation hinging on technology integration, regulatory compliance, and tailored service support for healthcare systems globally.

Abbott Laboratories

Bio‑Rad Laboratories

Danaher Corporation

Grifols, S.A.

Immucor, Inc.

Ortho Clinical Diagnostics

Roche Diagnostics

Siemens Healthineers

Thermo Fisher Scientific

Terumo Corporation

Technological advancements are redefining capabilities within the Blood Transfusion Diagnostics Market, driven by innovation in automation, molecular testing, and digital integration. One of the most transformative shifts is the adoption of multiplex nucleic acid testing (NAT) platforms capable of simultaneously screening multiple pathogens, reducing test cycles by up to 50% in centralized laboratories.

Another game-changing development is the expansion of microfluidic point-of-care (POC) diagnostic devices, delivering rapid results—often within 20 minutes—in hospital triage, mobile clinics, or rural settings. These systems support testing for ABO/Rh, antibody screening, and select infectious agents in compact, benchtop formats.

Leading vendors are also integrating pathogen-reduction technologies into their offerings. These systems use treatments such as ultraviolet light or riboflavin-based illumination to deactivate viruses and bacteria in blood components, enhancing safety protocols.

Automated serological workstations now feature robotic handling of sample tubes, integrated barcoding, and digital result management, enabling technicians to scale up throughput with minimal manual intervention. Some organizations report processing over 1 million tests monthly with centralized automation, reducing labor needs by more than half.

Digital dashboards and AI-driven analytics have begun to complement hardware solutions. These capabilities enable anomaly detection, reagent batch tracking, and predictive maintenance of instrumentation. Additionally, the adoption of biosensor-based screening modules for blood group antigens and antibodies is expanding personalized compatibility testing. Together, these technology trends are raising diagnostic standards and redefining efficiency and safety expectations across the sector.

In February 2024, Ortho Clinical Diagnostics launched a fully automated serology platform with integrated barcode tracking, improving sample traceability by 90% in high-volume blood banks.

In August 2023, Danaher enhanced its NAT testing suite by introducing a cartridge-based system capable of detecting five transfusion-transmissible infections in a single run with under 45-minute turnaround.

In April 2024, Siemens Healthineers unveiled a portable pathogen-reduction unit designed for on-site treatment of plasma and platelets in mobile blood donation camps.

In November 2023, Grifols introduced a biosensor-enabled blood grouping system with real-time digital readouts and automated result logging for rapid compatibility assessment.

The Blood Transfusion Diagnostics Market Report provides comprehensive coverage of diagnostic technologies and operational practices in the global transfusion safety landscape. It evaluates main product types, including serological assays, nucleic acid tests (NAT), pathogen-reduction technologies, point-of-care devices, and multiplex platforms across testing workflows.

Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed country-level analysis for markets like the United States, China, Germany, India, and Brazil. The report explores applications such as disease screening, blood grouping, cross-matching, antibody identification, and emergency triage testing.

End-user segments covered in the report include hospitals, blood banks, standalone diagnostic laboratories, maternal care centers, transplant units, and military healthcare. The study assesses coverage of automation and calibration platforms, reagent kits, biosensor modules, digital analytics tools, and instrument service ecosystems.

Moreover, the scope highlights trends in AI-integrated analytics, laboratory information systems (LIMS), mobile diagnostic units, and partnerships with national blood authorities. It also includes emerging niche segments such as pathogen-reduction workflows, wellness-focused blood testing, and rapid compatibility kits. Designed for decision-makers, the report delivers strategic insights on procurement, deployment, technology integration, and market expansion opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 533.0 Million |

| Market Revenue (2032) | USD 964.8 Million |

| CAGR (2025–2032) | 7.7 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Abbott Laboratories, Bio‑Rad Laboratories, Danaher Corporation, Grifols, S.A., Immucor, Inc., Ortho Clinical Diagnostics, Roche Diagnostics, Siemens Healthineers, Thermo Fisher Scientific, Terumo Corporation |

| Customization & Pricing | Available on Request (10 % Customization is Free) |