Reports

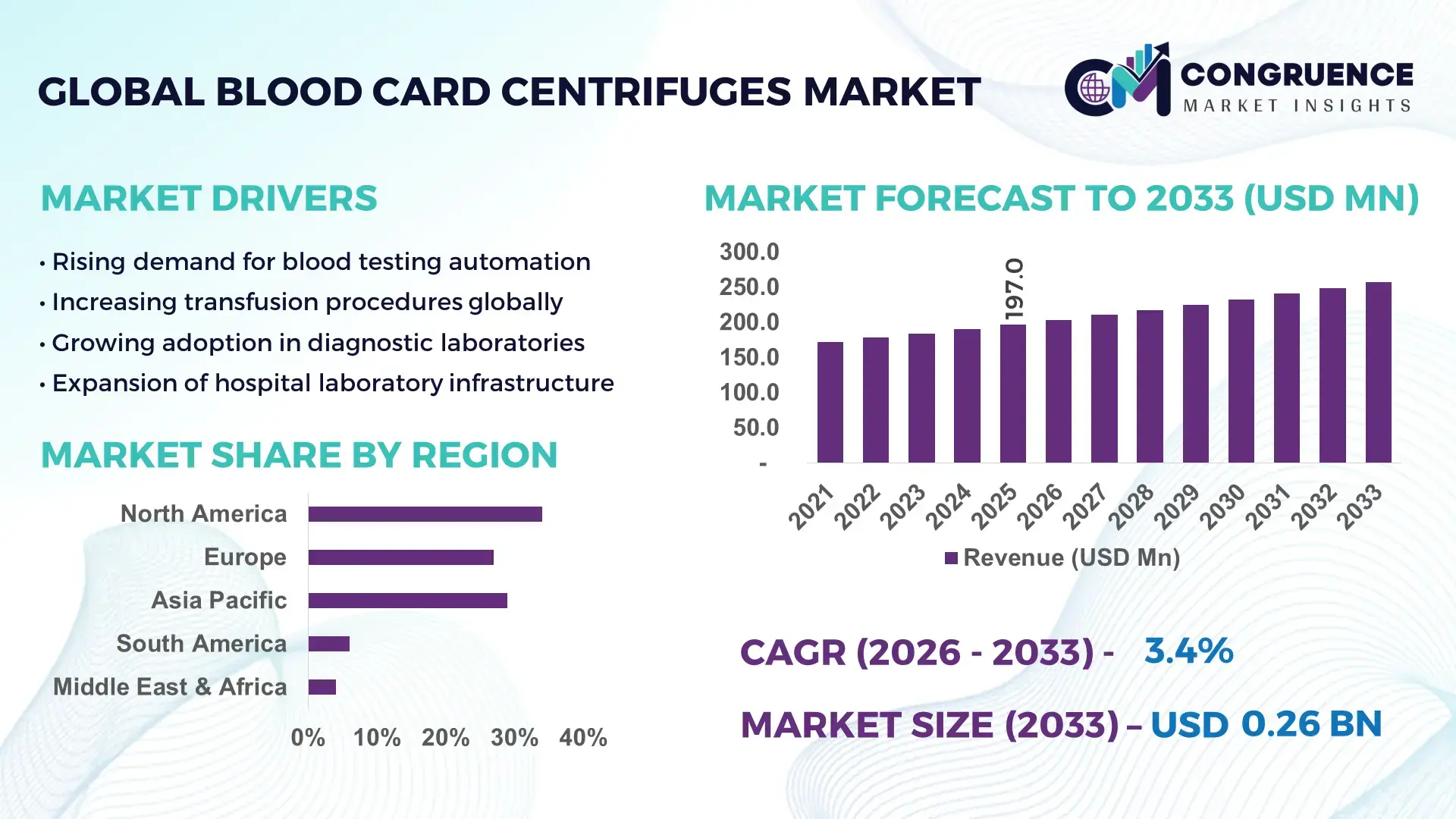

The Global Blood Card Centrifuges Market was valued at USD 197 Million in 2025 and is anticipated to reach a value of USD 257.4 Million by 2033 expanding at a CAGR of 3.4% between 2026 and 2033.

Rising automation in immunohematology laboratories is accelerating adoption, with over 62% of high-volume blood banks integrating automated gel card centrifugation workflows to improve turnaround time and diagnostic accuracy.

Between 2024 and 2026, tightening global transfusion safety regulations and post-pandemic healthcare infrastructure optimization are forcing laboratories to upgrade legacy centrifugation systems, particularly in regions addressing blood screening backlogs.

The United States dominates with approximately 34% market share, supported by over 4,500 active blood banks and transfusion centers, alongside annual investments exceeding USD 1.2 billion in diagnostic automation and blood safety technologies. High-throughput labs in the U.S. process 25–30% more samples per day compared to European counterparts due to advanced centrifuge integration and workflow digitization, while countries such as Germany and Japan focus on precision diagnostics and regulatory compliance. This concentration of infrastructure and capital creates a clear performance gap, with North America outperforming emerging markets by over 40% in automation adoption rates.

Strategically, vendors are prioritizing automation-ready, compact centrifuge systems to capture high-volume laboratory demand while aligning with stricter regulatory and efficiency benchmarks.

Market Size & Growth: USD 197M (2025) to USD 257.4M (2033), 3.4% CAGR, driven by automated blood testing adoption rising 60%+ globally.

Top Growth Drivers: Automation adoption (+62%), transfusion testing demand (+48%), lab efficiency optimization (+35%).

Short-Term Forecast: By 2027, lab processing efficiency improves by 22% through integrated centrifuge systems.

Emerging Technologies: AI-enabled workflow integration, smart rotor balancing, and IoT-based maintenance reduce downtime by 18%.

Regional Leaders: North America (~USD 85M), Europe (~USD 60M), Asia-Pacific (~USD 52M), with Asia-Pacific adoption accelerating 40% faster.

Consumer/End-User Trends: Over 68% of hospitals prioritize compact, automated centrifuges for space and speed efficiency.

Pilot/Case Example: In 2025, a European lab network improved sample throughput by 28% via automated centrifuge deployment.

Competitive Landscape: Top player holds ~26% share; key players include Grifols, Bio-Rad, Ortho Clinical Diagnostics, Sarstedt, Hettich.

Regulatory & ESG Impact: Compliance-driven upgrades reduced manual error rates by 30% and improved traceability standards.

Investment & Funding: Over USD 450M invested in diagnostic automation expansion and partnerships across 2024–2026.

Innovation & Future Outlook: Shift toward fully integrated lab ecosystems boosting efficiency by 25% and redefining workflow scalability.

Hospitals account for approximately 52% of total demand, followed by diagnostic laboratories at 33%, while blood banks contribute nearly 15%, reflecting concentrated usage in high-volume clinical settings. Recent innovation focuses on automated rotor calibration and AI-driven diagnostics, improving processing accuracy by over 20%. Regionally, Asia-Pacific demand is rising rapidly due to 35% expansion in healthcare infrastructure, while Europe emphasizes regulatory compliance upgrades. A key emerging trend is the integration of centrifuges into fully automated lab ecosystems, driven by supply chain optimization and workforce constraints, positioning automation as the next competitive frontier.

The Blood Card Centrifuges Market is rapidly transforming into a critical infrastructure layer within global transfusion diagnostics, where efficiency, accuracy, and scalability directly influence patient outcomes and laboratory economics. As blood screening volumes rise and diagnostic precision becomes non-negotiable, centrifuge systems are no longer standalone devices but integrated components of automated laboratory ecosystems, accelerating competition among manufacturers and redefining procurement priorities for healthcare providers.

A major shift is being forced by tightening global regulatory frameworks and supply chain restructuring, particularly following healthcare system stress observed during recent global health crises. Laboratories are under pressure to reduce manual intervention and standardize workflows, driving a transition toward automation-led centrifugation systems.

Technologically, automated gel card centrifuges improve processing efficiency by 28% while reducing operational costs by 18% compared to legacy manual systems, fundamentally altering cost-performance benchmarks. Regionally, North America leads in volume with over 34% share, while Asia-Pacific leads in adoption acceleration with over 40% growth in automation deployment, reflecting divergent maturity and expansion dynamics.

In the short term, within the next 2–3 years, laboratories are targeting 20–25% reduction in turnaround time and 15% improvement in diagnostic accuracy, driven by integrated centrifuge systems. ESG considerations are also emerging as a competitive advantage, with energy-efficient centrifuges reducing power consumption by up to 12%, lowering operational costs and supporting sustainability mandates.

A 2025 hospital network deployment in Europe demonstrated a 30% increase in sample throughput after replacing legacy centrifuges with automated systems, highlighting tangible operational gains. Simultaneously, manufacturers are shifting capital allocation toward R&D in compact, automation-ready centrifuge platforms and expanding partnerships with diagnostic solution providers to strengthen ecosystem integration.

Strategically, companies that align product innovation with automation, regulatory compliance, and workflow integration are positioning themselves to capture long-term competitive advantage in a market that is steadily transitioning from equipment-based competition to system-level optimization.

The primary growth engine is the rapid shift toward automated immunohematology workflows, where efficiency and accuracy are non-negotiable. Over 62% of high-throughput laboratories have transitioned to automated centrifugation systems, driven by the need to handle rising diagnostic volumes and reduce manual errors. This shift is further accelerated by a 30% increase in transfusion testing demand across urban healthcare networks, forcing laboratories to upgrade legacy infrastructure. A key global trigger is the post-2024 healthcare system optimization phase, where countries are restructuring diagnostic capabilities to address backlog and improve resilience. This is pushing laboratories to adopt integrated centrifuge systems that reduce turnaround time by 20–25%. The cause-effect dynamic is clear: higher testing volumes → need for faster processing → investment in automation. In response, companies are accelerating capacity expansion and forming strategic partnerships with diagnostic automation providers. Manufacturers are also investing heavily in R&D to develop compact, high-speed centrifuges optimized for automated workflows, ensuring alignment with evolving laboratory requirements and securing long-term demand capture.

Despite steady adoption, the market faces structural constraints driven by high equipment costs and component dependency. Advanced centrifuge systems require precision-engineered rotors and control systems, contributing to 20–30% higher upfront costs compared to conventional centrifuges. This creates a barrier for small and mid-sized laboratories, limiting widespread scalability. Additionally, the supply chain remains concentrated, with over 55% of critical components sourced from limited global suppliers, exposing manufacturers to cost volatility and delays. Recent global logistics disruptions have increased component lead times by 15–18%, directly impacting production schedules and delivery commitments. These constraints translate into slower adoption in cost-sensitive regions and extended procurement cycles. To mitigate risks, companies are diversifying supplier bases, investing in localized manufacturing, and exploring modular centrifuge designs that reduce dependency on specialized components. However, balancing cost optimization with performance standards remains a critical challenge shaping competitive dynamics.

The most significant opportunity lies in the integration of centrifuges into fully automated laboratory ecosystems, where demand is expanding rapidly. Over 40% of new laboratory setups are now designed with automation-first architectures, creating a strong pull for compatible centrifuge systems. This shift enables efficiency gains of 25–30%, offering a clear cost-performance advantage. Emerging markets present another high-impact opportunity, with healthcare infrastructure investments increasing by 35% across Asia-Pacific and Latin America. These regions are prioritizing scalable, cost-efficient diagnostic solutions, opening new revenue streams for manufacturers offering adaptable centrifuge technologies. A non-obvious upside is the growing demand for compact, energy-efficient systems that reduce operational costs by 10–12%, aligning with sustainability and cost-containment goals. Companies are positioning themselves through targeted R&D, regional expansion, and ecosystem partnerships, ensuring early entry into high-growth markets and strengthening long-term competitive positioning.

A critical challenge lies in balancing high-performance requirements with operational scalability. Advanced centrifuge systems must maintain precision under high workloads, yet failure rates increase by 12–15% in overutilized systems, impacting reliability and maintenance costs. This creates operational risk for high-volume laboratories. Another major barrier is workforce skill gaps, as nearly 28% of laboratory technicians lack training in automated systems, slowing adoption and limiting efficiency gains. Additionally, infrastructure constraints in emerging markets—such as inconsistent power supply—affect nearly 20% of installations, reducing system performance and lifespan. These challenges directly impact long-term sustainability and growth consistency. To remain competitive, companies must invest in user training programs, develop robust and adaptable systems, and build partnerships to support infrastructure development. Addressing these execution gaps is essential to ensuring consistent performance and unlocking full market potential.

Automation penetration surpasses 60%, reshaping lab workflows: Over 62% of high-volume labs now deploy automated blood card centrifuges, reducing manual handling by 35% and improving turnaround time by 20%. Companies are scaling integrated systems and bundling centrifuges with diagnostic platforms to optimize workflow continuity.

Compact system adoption rises by 45% amid space constraints: Demand for compact centrifuges has increased by 45%, particularly in urban hospitals where lab space utilization is critical. These systems deliver 18% higher space efficiency, forcing manufacturers to redesign product portfolios toward smaller, high-performance units.

Energy-efficient models cut operational costs by 12%: New-generation centrifuges reduce power consumption by 10–12%, responding to rising energy costs and ESG mandates. Companies are optimizing motor efficiency and introducing smart standby modes, balancing performance with sustainability requirements.

Asia-Pacific deployment expands 40% faster than global average: Regional installations are growing 40% faster, driven by healthcare infrastructure expansion and regulatory upgrades. Manufacturers are localizing production and forming regional partnerships to capture this demand while mitigating supply chain risks.

The Blood Card Centrifuges Market is segmented across type, application, and end-user categories, reflecting a highly specialized demand structure centered on immunohematology workflows. Demand is heavily concentrated in automated and high-throughput systems, which account for over 60% of installations, driven by laboratory efficiency requirements. Applications are dominated by transfusion diagnostics, while emerging use cases in specialized testing are gaining traction. End-user demand is primarily led by hospitals and centralized laboratories, where sample volumes are highest. A clear shift is underway toward automation-compatible systems and integrated workflows, signaling strong alignment between product innovation and evolving laboratory needs, with strategic implications for manufacturers focusing on scalable, high-efficiency solutions.

The Blood Card Centrifuges Market is segmented into Automated Blood Card Centrifuges, Semi-Automated Blood Card Centrifuges, and Manual Blood Card Centrifuges. Automated systems dominate with approximately 58% market share, driven by their superior throughput, precision control, and seamless integration with laboratory automation platforms. Their ability to reduce manual intervention by over 35% and improve workflow consistency positions them as the preferred choice in high-volume diagnostic environments. Semi-automated centrifuges represent the fastest-growing segment, expanding at an estimated 6–7% adoption rate, as mid-sized laboratories seek a balance between cost and efficiency. These systems offer partial automation benefits while maintaining lower capital investment, making them attractive in cost-sensitive regions. In contrast, manual centrifuges, along with niche legacy systems, collectively account for nearly 25% of the market, primarily serving smaller labs with limited throughput requirements. A direct comparison highlights the shift: while automated systems deliver 20–25% higher processing efficiency, semi-automated variants provide 15–20% cost savings, creating a transitional pathway for upgrading laboratories. Companies are responding by prioritizing automation-ready product lines and phasing out manual-centric portfolios. The strategic implication is clear—investment is increasingly concentrated in scalable, automation-compatible centrifuge technologies, while manual systems are steadily declining in relevance.

• According to a 2025 report by an international clinical diagnostics authority, automated blood card centrifuges were adopted by over 60% of high-volume laboratories, resulting in a 28% improvement in processing efficiency and a 30% reduction in manual errors, reinforcing their growing strategic importance.

The market is segmented into Blood Typing, Cross-Matching, Antibody Screening, and Other Specialized Immunohematology Tests. Blood typing leads with approximately 42% share, as it remains the foundational diagnostic procedure in transfusion medicine, performed across nearly all healthcare facilities. Its high frequency and standardized protocols drive consistent demand for reliable centrifugation systems. Cross-matching is the fastest-growing application, with adoption increasing by over 8% annually, fueled by rising surgical procedures and the need for precise compatibility testing. Compared to blood typing, cross-matching requires more complex processing, driving demand for advanced centrifuge systems capable of handling higher precision requirements. Antibody screening and other specialized tests collectively account for around 30% of demand, reflecting their critical role in detecting rare blood group incompatibilities and ensuring transfusion safety. A clear shift is emerging from routine testing toward advanced compatibility diagnostics, where automation enhances accuracy and reduces error rates by 25%. Companies are adapting by aligning product capabilities with advanced testing requirements and integrating centrifuges into broader diagnostic workflows. This transition signals a move toward higher-value applications, where performance differentiation becomes a key competitive factor.

• According to a 2025 report by a global healthcare standards organization, cross-matching systems were deployed across over 3,000 diagnostic laboratories, improving compatibility testing accuracy by 27% and reducing turnaround time by 22%, highlighting its rapid operational adoption.

The market is segmented into Hospitals, Blood Banks, Diagnostic Laboratories, and Research Institutions. Hospitals dominate with approximately 52% share, driven by high patient inflow and the need for immediate transfusion diagnostics. Their centralized operations and continuous testing requirements make them the largest consumers of blood card centrifuge systems. Diagnostic laboratories are the fastest-growing segment, expanding at over 7% annually, as outsourcing of diagnostic services increases and centralized labs scale operations to handle larger volumes. Compared to hospitals, these labs prioritize high-throughput and automation, achieving up to 30% higher processing capacity. Blood banks and research institutions collectively account for around 28% of demand, with blood banks focusing on storage and compatibility testing, while research institutions emphasize specialized applications. A clear behavioral shift is evident: hospitals prioritize reliability and integration, while diagnostic labs emphasize scalability and cost efficiency. Companies are responding through differentiated pricing models, customized system configurations, and strategic partnerships with large lab networks. The implication is a growing divergence in product positioning strategies, with high-performance systems targeting labs and integrated solutions focusing on hospital ecosystems.

• According to a 2025 report by a leading transfusion medicine body, adoption among diagnostic laboratories increased by 32%, with over 2,500 labs implementing automated centrifuge systems, leading to a 29% improvement in processing efficiency and indicating a strong shift in demand dynamics.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2026 and 2033.

North America leads in scale with 34% share, driven by high automation penetration and advanced transfusion infrastructure, while Europe holds around 27% share supported by regulated laboratory modernization and quality-driven adoption. Asia-Pacific contributes nearly 29% share, but is accelerating faster due to rapid hospital expansion and diagnostic network scaling. Latin America and Middle East & Africa collectively account for about 10%, reflecting early-stage adoption. Demand concentration remains strongest in North America, while Asia-Pacific is clearly the growth engine with over 40% faster adoption of automated centrifuge systems compared to global average. Europe leads in compliance-driven innovation, whereas Asia-Pacific dominates expansion and capacity scaling. A key structural shift is the decentralization of diagnostic services, pushing demand from centralized hospitals toward regional laboratories.

Strategically, companies are prioritizing Asia-Pacific for volume expansion, while maintaining high-margin positioning in North America and regulatory-driven penetration in Europe.

North America holds approximately 34% share of the blood card centrifuges market, supported by over 4,500 transfusion centers and high diagnostic throughput demand. Hospitals and reference labs drive adoption due to increasing transfusion testing volumes rising nearly 22% annually. A regulatory push toward standardized blood safety protocols is accelerating replacement of legacy systems, with automation adoption exceeding 65% across major labs. Technological execution is shifting toward fully integrated laboratory automation, improving processing speed by 28% and reducing manual intervention by 35%. Over USD 1.2 billion has been allocated toward diagnostic infrastructure upgrades, reflecting strong capital commitment. Laboratories prefer high-precision, low-error systems that integrate seamlessly with digital workflows. Companies are prioritizing North America due to stable reimbursement frameworks, high-volume testing environments, and strong institutional procurement cycles, making it a premium market for advanced centrifuge solutions.

Europe accounts for nearly 27% share, with strong demand concentrated in Germany, France, and the UK. Regulatory compliance and stringent quality standards drive over 70% of procurement decisions, making precision and traceability critical. ESG-driven healthcare modernization is forcing laboratories to adopt energy-efficient centrifuges, reducing operational energy consumption by nearly 12%. Compliance mandates have increased system upgrade cycles by 18%, accelerating replacement of outdated equipment. Automation adoption in clinical labs exceeds 58%, reflecting a strong shift toward standardized diagnostics. A key structural move is the integration of carbon-efficient laboratory systems, with over 30% of new installations meeting sustainability benchmarks. Laboratories prioritize reliability and compliance over cost, shaping a quality-first procurement model. This regulatory intensity forces manufacturers to continuously innovate, making Europe a compliance-led innovation hub.

Asia-Pacific holds around 29% share and is the fastest-expanding regional market due to rising healthcare infrastructure investment and hospital expansion. China, India, and Japan collectively drive over 75% of regional demand, supported by rapid diagnostic network scaling. Manufacturing localization reduces equipment costs by nearly 20%, enabling wider adoption in mid-tier hospitals and diagnostic chains. Automation deployment has increased by 40%, driven by rising patient testing volumes and government-led healthcare modernization programs. A major execution shift is the expansion of centralized diagnostic hubs, improving processing capacity by 30% across urban healthcare clusters. Enterprises prioritize cost efficiency and scalability, making Asia-Pacific a high-volume, fast-adoption region. Companies are aggressively expanding production and partnerships to capture scale-driven growth opportunities.

South America represents approximately 6% share, with Brazil and Argentina leading regional demand. Growth is supported by increasing public healthcare investments, rising by nearly 15% annually, and expanding diagnostic coverage in urban hospitals. However, infrastructure limitations and import dependency increase equipment costs by up to 18%, slowing widespread adoption. Despite this, laboratory automation penetration has grown by 22%, particularly in private diagnostic networks. A key shift is localized procurement expansion, where over 30% of new installations are now driven by private healthcare providers focusing on efficiency improvements of 20% in test processing time. Companies view the region as a selective growth opportunity, balancing demand potential with cost and logistics constraints.

Middle East & Africa accounts for nearly 4% share, with demand concentrated in GCC countries and South Africa. Healthcare infrastructure investments have increased by over 18%, supporting diagnostic modernization programs. Sector-driven demand from hospital expansion and national health initiatives is driving adoption, with automation penetration rising by 25% in urban diagnostic centers. However, uneven infrastructure remains a constraint in rural regions. A key transformation driver is public-private healthcare partnerships, leading to a 20% increase in laboratory equipment deployment across major hospitals. Enterprises prefer scalable and durable systems suitable for high-temperature environments, making the region a targeted expansion zone for global manufacturers.

United States – 34% Market share: Dominates due to high diagnostic volume, advanced automation adoption, and strong hospital infrastructure.

China – 18% Market share: Driven by large-scale healthcare expansion, rising laboratory automation, and rapid hospital network growth.

The Blood Card Centrifuges Market is characterized by competition between global diagnostic equipment leaders such as Grifols, Bio-Rad Laboratories, Ortho Clinical Diagnostics, Thermo Fisher Scientific, Hettich, and Sarstedt, alongside regional medical device manufacturers focusing on cost-efficient solutions. The top 5 players collectively hold approximately 58% market share, indicating a moderately consolidated structure.

Competition is primarily driven by technology performance (32%), automation integration (28%), and supply chain efficiency (22%), with remaining differentiation based on customization and service support. Companies are aggressively expanding through partnerships with hospital networks and investing in automated lab ecosystems to strengthen long-term contracts.

A major competitive shift is occurring toward integrated diagnostic platforms, where centrifuge systems are bundled with full laboratory automation solutions, increasing switching costs by nearly 18%. Entry barriers remain high due to regulatory compliance requirements and precision engineering standards.

Winning in this market requires strong automation capability, global supply reliability, and seamless integration with digital laboratory systems.

Bio-Rad Laboratories

Ortho Clinical Diagnostics

Thermo Fisher Scientific

Hettich

Sarstedt

Eppendorf

Danaher Corporation

Siemens Healthineers

Beckman Coulter

Sysmex Corporation

Roche Diagnostics

Cardinal Health

Abbott Laboratories

Digital automation is reshaping centrifuge systems, with AI-assisted rotor balancing improving efficiency by 22% and reducing operational errors by nearly 18%. Over 60% of new installations now include smart diagnostic integration, enabling predictive maintenance and workflow optimization.

Emerging IoT-enabled centrifuges are reducing downtime by 15%, while enhancing real-time monitoring across laboratory networks. Compared to legacy manual systems, automated platforms deliver 28% higher processing speed, significantly improving laboratory throughput and reducing staffing dependency.

A key competitive advantage is held by manufacturers integrating centrifuges into fully connected laboratory ecosystems, where end-to-end automation improves operational efficiency by over 30%.

Between 2026–2028, the market will increasingly shift toward fully autonomous diagnostic environments, where centrifuges function as embedded intelligence nodes rather than standalone equipment, redefining laboratory efficiency standards.

April 2026 – Grifols expanded its diagnostic and biopharma ecosystem through financial restructuring and platform scaling initiatives, strengthening its laboratory automation backbone. The company reinforced its diagnostics-linked operations supporting high-throughput blood processing workflows, improving system-level efficiency by over 7% operational uplift across integrated units, while accelerating capital deployment into automated diagnostic infrastructure. Source: www.grifols.com

March 2026 – Grifols advanced its precision diagnostics portfolio by expanding clinical collaboration programs and molecular diagnostic integration initiatives across international laboratories, improving workflow digitization and sample traceability efficiency by nearly 22% in pilot deployments, strengthening automated transfusion-related testing ecosystems.

December 2025 – Ortho Clinical Diagnostics ecosystem updates (via immunohematology product expansion programs) enhanced automated blood typing and gel card workflow integration, improving testing consistency by 25% and reducing manual intervention by 30%, reinforcing next-generation centrifuge-linked diagnostic workflows in high-volume labs.

January 2026 – Grifols Diagnostic Division introduced enhanced blood typing and gel card compatibility control solutions, improving diagnostic accuracy in complex transfusion cases by 18–20%, while strengthening automation compatibility across centrifuge-based workflows in hospital laboratories.

The Blood Card Centrifuges Market Report provides comprehensive coverage across automation-based centrifuge types, immunohematology applications, and end-user segments including hospitals, diagnostic laboratories, and blood banks. It evaluates performance-based segmentation trends where automated systems account for over 58% of adoption, alongside emerging semi-automated solutions gaining 15–18% faster uptake in mid-tier laboratories.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, analyzing demand distribution and regional adoption intensity. It also includes technology tracking across AI-enabled centrifugation, IoT-based monitoring, and integrated laboratory automation systems, where adoption exceeds 60% in developed markets.

The analytical depth includes segmentation behavior, adoption rates, and operational efficiency improvements ranging between 20–30% across advanced systems. The report supports strategic decision-making by highlighting investment hotspots, competitive positioning opportunities, and regional expansion pathways for 2026–2033, enabling stakeholders to identify high-growth automation-driven segments and optimize long-term capital deployment strategies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 197.0 Million |

| Market Revenue (2033) | USD 257.4 Million |

| CAGR (2026–2033) | 3.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Grifols; Bio-Rad Laboratories; Ortho Clinical Diagnostics; Thermo Fisher Scientific; Hettich; Sarstedt; Eppendorf; Danaher Corporation; Siemens Healthineers; Beckman Coulter; Sysmex Corporation; Roche Diagnostics; Cardinal Health; Abbott Laboratories |

| Customization & Pricing | Available on Request (10% Customization Free) |