Reports

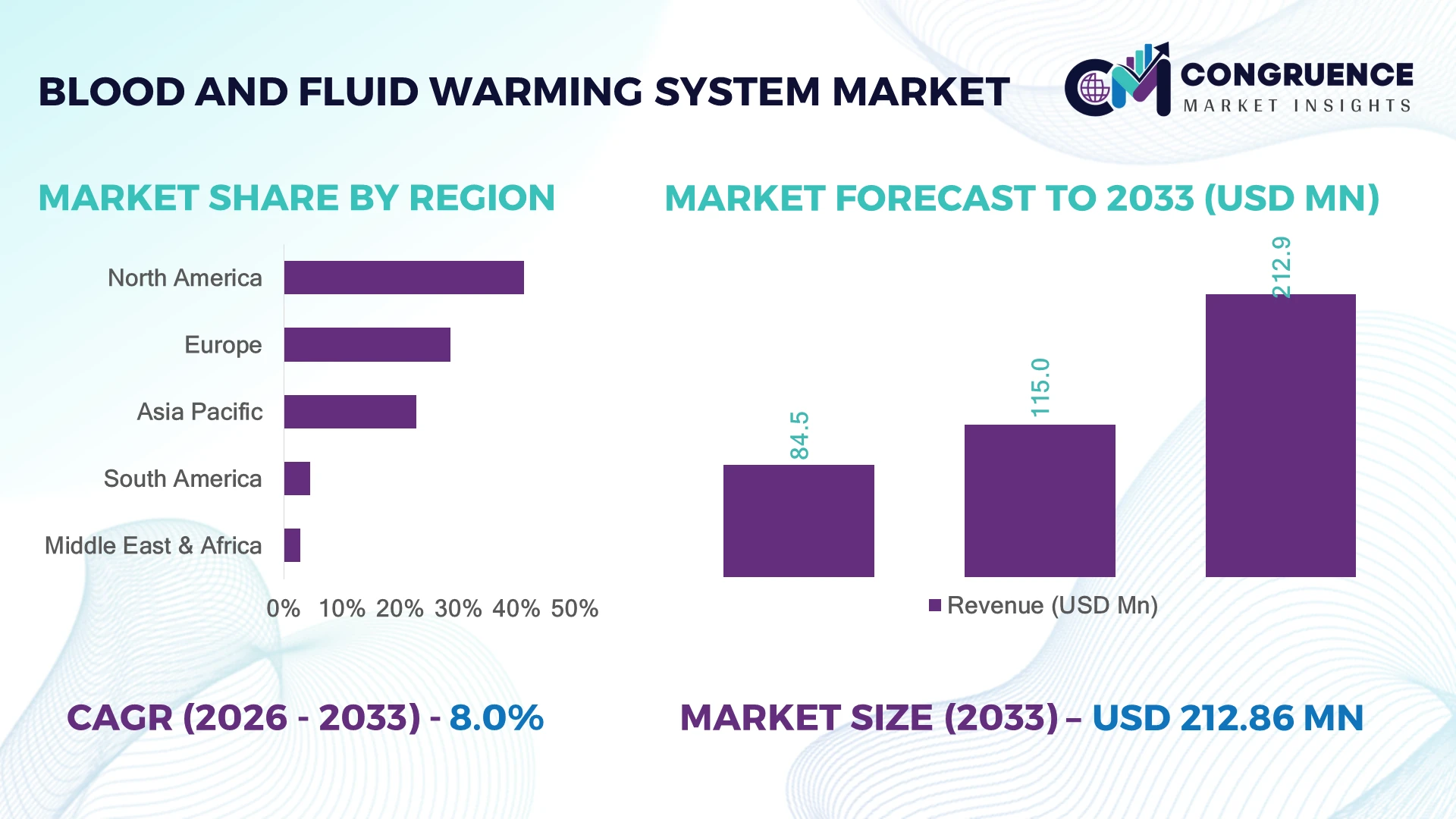

The Global Blood and Fluid Warming System Market was valued at USD 115.0 Million in 2025 and is anticipated to reach a value of USD 212.9 Million by 2033 expanding at a CAGR of 8.0% between 2026 and 2033. Growth is driven by rising trauma care procedures, expanding surgical volumes, stricter perioperative temperature management protocols, and rapid adoption of advanced portable warming technologies across emergency, military, and critical care environments.

The United States dominates the global Blood and Fluid Warming System Market with approximately 39% market share, supported by over 6,000 hospitals, high adoption of advanced operating room technologies, and sustained investments in trauma and emergency care infrastructure. Compared with Germany, which emphasizes standardized perioperative care across public healthcare systems, the U.S. demonstrates broader deployment of portable warming devices in military medicine and air medical transport, strengthening clinical readiness and accelerating technology adoption.

Healthcare providers prioritizing intelligent warming technologies, portable platforms, and integrated patient temperature management solutions are positioned to strengthen clinical outcomes and long-term competitive differentiation.

Market Size & Growth: USD 115.0 Million (2025) is projected to reach USD 212.9 Million by 2033 at 8.0% CAGR, driven by advanced perioperative care protocols and expanding trauma treatment capacity.

Top Growth Drivers: Surgical procedures (+18%), emergency care demand (+22%), and portable device adoption (+27%) continue accelerating market expansion.

Short-Term Forecast: By 2028, automated temperature management systems are expected to improve workflow efficiency by nearly 20% across advanced healthcare facilities.

Emerging Technologies: AI-enabled monitoring, compact battery-powered warming systems, and smart temperature sensors improve precision and patient safety.

Regional Leaders: North America (~USD 82 Million), Europe (~USD 58 Million), and Asia-Pacific (~USD 46 Million by 2033) lead through hospital modernization and critical care expansion.

Consumer/End-User Trends: More than 65% of tertiary hospitals prioritize integrated blood and fluid warming solutions within surgical workflows.

Pilot/Case Example: A 2024 trauma-center deployment reduced unintended perioperative hypothermia by approximately 30% through continuous warming technology.

Competitive Landscape: Baxter holds roughly 20% market share alongside 3M, Belmont Medical Technologies, Smiths Medical, and Stryker.

Regulatory & ESG Impact: Updated perioperative care guidelines contributed to over 25% higher compliance with patient temperature management standards.

Investment & Funding: More than USD 350 Million supports manufacturing expansion, strategic partnerships, and next-generation critical care technologies amid global supply-chain diversification.

Innovation & Future Outlook: Connected warming platforms, digital monitoring, and lightweight portable systems are redefining competitive positioning across high-growth healthcare markets.

Blood and Fluid Warming System Market demand continues expanding across trauma centers, operating rooms, intensive care units, and emergency transport services where rapid temperature stabilization directly improves clinical outcomes. Compact portable devices, intelligent temperature monitoring, and disposable warming accessories are reshaping product development, while nearly 45% of new hospital equipment upgrades emphasize integrated patient warming solutions. Healthcare supply-chain resilience and evolving perioperative quality standards further support adoption, setting the stage for broader strategic investments.

The Blood and Fluid Warming System Market has become strategically important as healthcare providers prioritize patient safety, operating room efficiency, and standardized perioperative care. Competition increasingly centers on integrated temperature management platforms that improve clinical consistency while supporting hospital modernization initiatives. Regulatory emphasis on preventing inadvertent hypothermia and healthcare infrastructure upgrades continues to influence procurement strategies, particularly across tertiary hospitals and emergency care networks.

Modern microprocessor-controlled warming systems deliver temperature accuracy within narrow clinical ranges while reducing setup time by approximately 25% compared with conventional manual warming approaches. North America leads in large-scale deployment through advanced trauma and surgical facilities, whereas Asia-Pacific is expanding rapidly through hospital construction, emergency medical service upgrades, and greater investment in critical care technology. Over the next two to three years, digital connectivity and remote equipment monitoring are expected to become standard features across premium systems.

Manufacturers are strengthening regional manufacturing capabilities, expanding distributor partnerships, and investing in portable platforms designed for ambulances, military medicine, and air medical transport. A growing number of hospitals are standardizing warming devices across surgical departments to simplify clinical workflows and maintenance. Organizations that combine technological innovation, reliable product availability, and comprehensive clinical support will strengthen competitive positioning while delivering measurable operational advantages in increasingly performance-focused healthcare environments.

Rising adoption of evidence-based perioperative temperature management protocols is accelerating deployment of blood and fluid warming systems across surgical, trauma, and emergency care settings. More than 70% of major surgical procedures involve active patient temperature monitoring, while perioperative hypothermia affects up to 50% of unwarmed surgical patients. The United States continues expanding Level I trauma centers and emergency transport capabilities, increasing demand for portable warming platforms with digital controls. This structural shift improves patient recovery, reduces transfusion-related complications, and standardizes clinical workflows. Manufacturers are responding through intelligent warming technologies, battery-powered transport systems, strategic hospital partnerships, and expanded manufacturing capacity. A key strategic trend is the integration of warming devices into hospital-wide perioperative protocols, transforming them from standalone equipment into essential components of standardized surgical care.

High acquisition costs and uneven hospital infrastructure remain significant barriers to widespread deployment, particularly across middle-income healthcare systems. Advanced warming platforms typically cost 30–45% more than conventional warming methods, while nearly 40% of secondary hospitals continue relying on legacy manual temperature management practices. In countries such as India, procurement cycles are frequently influenced by public tender budgets and imported component availability, creating delays in equipment replacement. These constraints reduce deployment scalability and increase maintenance complexity across multi-site healthcare networks. Companies are mitigating risk through localized assembly, long-term procurement agreements, service-based contracts, and modular product portfolios tailored to different healthcare budgets. Organizations offering flexible ownership models gain stronger access to resource-constrained hospital systems.

Digital healthcare transformation is creating new opportunities for connected blood and fluid warming technologies beyond traditional operating rooms. More than 55% of newly procured critical care devices now emphasize interoperability, while connected medical equipment adoption has increased by approximately 35% across advanced hospitals. Japan is investing heavily in smart emergency medical infrastructure, supporting demand for portable warming systems integrated with patient monitoring platforms. Manufacturers are expanding R&D around wireless temperature tracking, predictive maintenance, and cloud-enabled asset management that improves equipment utilization and service efficiency. An emerging strategic opportunity lies in military medicine, disaster response, and ambulance fleets, where compact intelligent warming systems provide operational advantages while supporting broader digital healthcare ecosystems.

Long-term market expansion depends on seamless integration with evolving hospital ecosystems and consistent clinical adoption. Nearly 28% of healthcare facilities report interoperability challenges when connecting specialized medical devices with digital hospital platforms, while approximately 32% identify workforce training as a major barrier to advanced equipment utilization. In Germany, hospitals increasingly require standardized digital documentation and interoperability before approving new medical technologies, extending implementation timelines. These operational pressures affect deployment consistency, maintenance efficiency, and technology utilization rates rather than procurement alone. Companies must strengthen clinical education programs, software integration capabilities, cybersecurity resilience, and post-installation technical support through strategic partnerships with healthcare providers. Organizations that simplify implementation while enhancing digital compatibility will secure stronger long-term competitive positioning.

Portable Systems Gain Momentum: Portable blood and fluid warming systems are being deployed across ambulance fleets, military transport units, and emergency response networks, with adoption increasing by nearly 28% over the past two years. Battery-powered operation and compact designs reduce treatment delays by approximately 20% during patient transfer. Updated emergency preparedness initiatives in the United States are encouraging healthcare providers to expand mobile critical care capabilities, prompting manufacturers to scale production and strengthen partnerships with emergency medical service providers.

Digital Workflow Integration Expands: Hospitals are integrating warming devices with electronic medical records and centralized equipment management platforms, improving device utilization by nearly 24% while reducing maintenance response times by 18%. Digital hospital transformation in Japan is accelerating demand for connected clinical equipment. Manufacturers are introducing intelligent monitoring features, automated calibration, and predictive maintenance capabilities to streamline perioperative workflows and reduce equipment downtime.

Disposable Components See Growth: Single-use warming accessories now account for more than 40% of newly procured consumables in advanced surgical facilities, helping lower cross-contamination risks by approximately 30%. Enhanced infection prevention protocols and stricter sterilization standards are reshaping procurement strategies. Companies are expanding disposable product portfolios, localizing manufacturing, and improving supply-chain resilience to ensure uninterrupted product availability.

Localized Manufacturing Strengthens Supply: Healthcare suppliers are restructuring production networks, reducing dependence on single-country sourcing by nearly 25% while shortening procurement lead times by around 15%. Enterprise buyers increasingly prioritize supply continuity alongside product performance—a non-obvious purchasing shift. Manufacturers are expanding regional assembly facilities, diversifying component suppliers, and forming strategic logistics partnerships to improve operational reliability under evolving healthcare procurement policies.

Portable Blood and Fluid Warming Systems represent the leading segment, accounting for approximately 52% of total market deployment due to their flexibility across operating rooms, emergency transport, trauma care, and military medicine. Their lightweight design, rapid temperature stabilization, and battery-powered operation enable consistent performance in both hospital and field environments. Healthcare providers increasingly standardize portable platforms to simplify patient transfer while maintaining uninterrupted warming therapy. Accessories & Consumables remain strategically important because recurring replacement supports continuous clinical operations and infection prevention requirements. Stationary Blood and Fluid Warming Systems are emerging as the fastest-growing segment within large tertiary hospitals undergoing operating room modernization. Nearly 35% of newly installed surgical suites now integrate fixed warming platforms with centralized monitoring systems, while enterprise procurement of integrated warming equipment has increased by approximately 22%. Manufacturers are investing in intelligent control interfaces, modular product architectures, and strategic hospital collaborations to strengthen long-term product portfolios. This investment shift reflects growing demand for scalable, digitally integrated warming infrastructure across high-acuity clinical environments.

Surgery continues to dominate application demand, representing nearly 58% of total equipment utilization because temperature management directly supports perioperative safety, blood transfusion efficiency, and improved patient recovery. Growing procedural complexity and standardized warming protocols have reinforced investment in integrated operating room equipment. Acute Care is the fastest-growing application as emergency departments expand trauma capabilities and intensive care capacity. Hospitals report approximately 26% greater utilization of warming devices within emergency workflows compared with pre-pandemic operating practices. Preoperative Care is gaining importance as hospitals implement standardized patient preparation protocols to reduce unintended hypothermia before surgery. Obstetrics is also expanding steadily, particularly in cesarean deliveries where neonatal and maternal temperature management has become more standardized. Home Care and Others remain comparatively smaller but benefit from portable technologies supporting specialized treatment pathways. Manufacturers are responding through workflow integration, automated temperature controls, and application-specific product configurations that improve operational efficiency while addressing diverse clinical environments.

Hospitals remain the dominant end-user segment, accounting for approximately 68% of overall installations due to high surgical volumes, trauma care infrastructure, and advanced critical care capabilities. Continuous equipment utilization across operating rooms, emergency departments, and intensive care units supports sustained procurement activity. Ambulatory Surgical Centers represent the fastest-growing buyer group as same-day procedures expand and facilities prioritize compact, cost-efficient warming technologies. Procurement among outpatient surgical facilities has increased by approximately 24% alongside broader adoption of minimally invasive procedures. Military & Emergency Medical Services continue strengthening demand for highly portable systems capable of operating in transport environments, while Blood Banks utilize warming devices to support safe transfusion practices. Clinics and Other healthcare facilities increasingly adopt compact platforms as outpatient procedural capacity expands. Manufacturers are tailoring pricing models, service agreements, and product configurations for each customer segment while expanding partnerships with hospital networks and surgical center operators to strengthen competitive positioning across institutional healthcare markets.

North America accounted for the largest market share at 41.3% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

North America maintains the leading position through its mature healthcare infrastructure, widespread adoption of perioperative temperature management protocols, and extensive network of trauma and transplant centers. The region contributes approximately 41.3% of global demand, supported by high utilization across operating rooms, emergency departments, and critical care units. More than 70% of tertiary hospitals have standardized active patient warming protocols within surgical pathways. Ongoing investments in digital operating rooms and connected medical equipment continue to strengthen deployment of intelligent warming systems. Manufacturers are expanding service networks, strengthening hospital partnerships, and introducing interoperable platforms that improve clinical workflow efficiency and equipment utilization.

United States Market Outlook: The United States represents the largest national market owing to its extensive surgical volume, advanced trauma systems, and technology-focused hospital procurement strategies. More than 6,000 hospitals and a well-established network of Level I trauma centers support continuous demand for blood and fluid warming systems. Healthcare providers increasingly integrate warming technologies with perioperative monitoring platforms, while domestic manufacturers continue expanding production capacity and product innovation to support emergency medicine, military healthcare, and high-acuity surgical environments.

Europe remains a highly established market, accounting for approximately 28.6% of global demand, driven by evidence-based perioperative care guidelines and continuous hospital modernization. Healthcare systems increasingly prioritize standardized patient temperature management, resulting in broader deployment across surgical specialties and intensive care units. Nearly 65% of large university hospitals have integrated advanced warming technologies into enhanced recovery protocols. Public healthcare investments and medical device quality standards continue supporting replacement of conventional warming methods with digitally controlled systems. Companies are expanding regional distribution, strengthening regulatory compliance capabilities, and introducing energy-efficient equipment tailored to institutional procurement requirements.

Germany Market Outlook: Germany leads the European market through its advanced hospital infrastructure, strong medical device manufacturing ecosystem, and high surgical procedure volumes. The country continues investing in digital hospital modernization under national healthcare transformation initiatives, encouraging greater adoption of intelligent perioperative equipment. Large university medical centers increasingly standardize warming technologies across operating theatres, while domestic engineering expertise supports continuous product innovation and reliable clinical deployment throughout the healthcare system.

Asia-Pacific is the fastest-growing regional market as governments continue expanding tertiary healthcare infrastructure, emergency medical services, and surgical capacity. The region represents approximately 22.8% of global market activity, with demand supported by increasing hospital construction and broader access to advanced surgical care. More than 35% of newly commissioned tertiary hospitals across major Asian economies include upgraded perioperative equipment specifications. Manufacturers are strengthening localized production, expanding distribution partnerships, and increasing regional assembly operations to improve delivery efficiency and reduce procurement timelines.

China Market Outlook: China is the largest contributor within Asia-Pacific due to rapid healthcare infrastructure expansion, domestic medical device manufacturing, and rising adoption of advanced surgical technologies. Continuous investment in high-level public hospitals and emergency medical facilities has strengthened demand for intelligent blood and fluid warming systems. Local manufacturers are increasing production capacity while international companies expand strategic partnerships to improve technology access, product localization, and nationwide distribution across both urban and provincial healthcare institutions.

South America accounts for approximately 4.5% of the global market, supported by ongoing investment in hospital modernization, trauma care capacity, and public healthcare improvement programs. Demand is concentrated within major metropolitan healthcare networks where surgical activity and emergency services continue expanding. Around 30% of recently upgraded tertiary hospitals have incorporated modern perioperative warming equipment into operating room refurbishment projects. Procurement remains influenced by public funding cycles and imported medical equipment availability, encouraging suppliers to strengthen regional distribution and technical support capabilities.

Brazil Market Outlook: Brazil dominates the regional market through its extensive public and private hospital network, growing surgical procedure volumes, and expanding critical care infrastructure. Large healthcare providers continue investing in operating room modernization and patient safety initiatives that support active warming technology deployment. International manufacturers are collaborating with local distributors to improve after-sales service, product availability, and clinician training, strengthening long-term adoption across major urban healthcare centers.

The Middle East & Africa region represents approximately 2.8% of the global market, supported by sustained healthcare infrastructure investments, specialized hospital development, and modernization of emergency medical services. Government-backed healthcare transformation programs are increasing procurement of advanced operating room technologies, particularly within tertiary referral hospitals. More than 25% of newly developed specialist hospitals across Gulf Cooperation Council countries include integrated perioperative warming systems during initial equipment procurement. Suppliers are expanding regional partnerships, technical service capabilities, and localized training programs to strengthen long-term market penetration.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through large-scale healthcare infrastructure projects, expanding specialist hospital capacity, and continued implementation of national healthcare transformation initiatives. Major public hospital developments increasingly prioritize advanced surgical equipment and digital operating room integration. International medical device manufacturers are strengthening local partnerships, expanding clinical education programs, and supporting healthcare workforce development to improve deployment consistency and technology utilization across the Kingdom's rapidly modernizing healthcare sector.

The market is led by 3M, Belmont Medical Technologies, Baxter International, Smiths Medical, and Stryker, while specialized warming device manufacturers compete against diversified critical care OEMs and cost-focused regional suppliers. The top five players collectively account for approximately 64% of the global market, reflecting moderate consolidation with strong technology differentiation. Competition is driven by temperature precision, portability, workflow integration, and disposable compatibility rather than price alone. Premium systems reduce setup time by nearly 25%, while integrated digital monitoring improves equipment utilization by around 20% and disposable product attachment rates exceed 60% in advanced hospitals. Companies compete through manufacturing expansion, hospital purchasing agreements, product innovation, and broader distribution partnerships. The competitive landscape is shifting toward intelligent connected platforms and stronger supply-chain resilience, increasing pressure on manufacturers lacking clinical integration capabilities. Regulatory compliance, clinical validation, and established hospital relationships remain key entry barriers. Winning requires reliable technology, rapid service support, scalable manufacturing, and continuous innovation.

Belmont Medical Technologies

Baxter International Inc.

Smiths Medical

Stryker Corporation

Barkey GmbH & Co. KG

ICU Medical, Inc.

The 37Company

QinFlow Ltd.

Biegler GmbH

Emit Corporation

Stihler Electronic GmbH

Geratherm Medical AG

Modern blood and fluid warming systems increasingly utilize microprocessor-controlled heating, dry-heat technology, precision temperature sensors, and intelligent alarm management to improve clinical safety. More than 65% of newly installed premium systems incorporate digital temperature monitoring, while automated calibration reduces maintenance interventions by approximately 18%. Integration with hospital information systems and perioperative monitoring platforms enables real-time equipment status visibility, improving workflow efficiency and reducing manual documentation requirements.

Emerging technologies include battery-powered portable warmers, wireless asset tracking, predictive maintenance software, and cloud-enabled fleet management. Compared with conventional resistance-based warming devices, advanced induction and closed-loop temperature control technologies improve temperature accuracy by nearly 30% while reducing warm-up time by approximately 25%. Hospitals operating high-volume trauma centers and emergency transport services benefit most from these innovations because portable intelligent platforms improve deployment flexibility without compromising temperature consistency during patient transfer.

Between 2026 and 2028, manufacturers are expected to accelerate development of AI-assisted diagnostics, self-monitoring electronics, and interoperable warming platforms capable of seamless integration with connected operating rooms. Deployment of smart medical equipment is projected to exceed 55% among newly equipped tertiary hospitals. Companies investing early in cybersecurity, software interoperability, and predictive service capabilities will strengthen competitive positioning, improve equipment utilization, reduce lifecycle operating costs, and establish long-term differentiation as healthcare providers increasingly prioritize connected perioperative ecosystems.

October 2024 – Belmont Medical Technologies secured a national patient warming agreement with Premier Inc., expanding access to the Belmont® Rapid Infuser RI-2 across approximately 4,350 U.S. hospitals, strengthening institutional procurement and market penetration. Source: www.belmontmedtech.com

2025 – Belmont Medical Technologies announced a Blood/Fluid Warming Equipment & Supplies agreement with HealthTrust, broadening contracted availability across participating healthcare providers and reinforcing commercial distribution through major U.S. group purchasing networks.

April 2025 – 3M issued updated operating instructions for the Ranger Blood/Fluid Warming System after validating warming performance of up to 333 mL/min under specified conditions, improving clinical labeling accuracy and reinforcing safe device utilization. Source: www.fda.gov

February 2026 – Belmont Medical Technologies appointed Brian Larkin as Chief Executive Officer to accelerate strategic expansion, operational execution, and product innovation across critical care temperature management technologies. Source: www.prnewswire.com

The report delivers comprehensive analysis of the Blood and Fluid Warming System Market across three product types, six application areas, and six end-user categories, providing detailed evaluation of deployment patterns, purchasing priorities, and technology adoption. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by country-level operational insights. The study also evaluates portable warming technologies, stationary platforms, disposable accessories, intelligent monitoring systems, and emerging digital integration trends shaping clinical practice.

The report profiles 13 major industry participants and examines competitive positioning, product innovation, supply-chain developments, regulatory influences, and enterprise deployment strategies. Quantitative assessment includes market share distribution, adoption intensity, procurement behavior, and healthcare infrastructure trends. Strategic insights support investment prioritization, product portfolio expansion, partnership evaluation, geographic growth planning, and competitive benchmarking while identifying high-potential clinical applications and evolving technology adoption patterns expected to influence market direction between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 115.0 Million |

| Market Revenue (2033) | USD 212.9 Million |

| CAGR (2026–2033) | 8.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | 3M; Belmont Medical Technologies; Baxter International Inc.; Smiths Medical; Stryker Corporation; Barkey GmbH & Co. KG; ICU Medical, Inc.; The 37Company; QinFlow Ltd.; Biegler GmbH; Emit Corporation; Geratherm Medical AG |

| Customization & Pricing | Available on Request (10% Customization Free) |