Reports

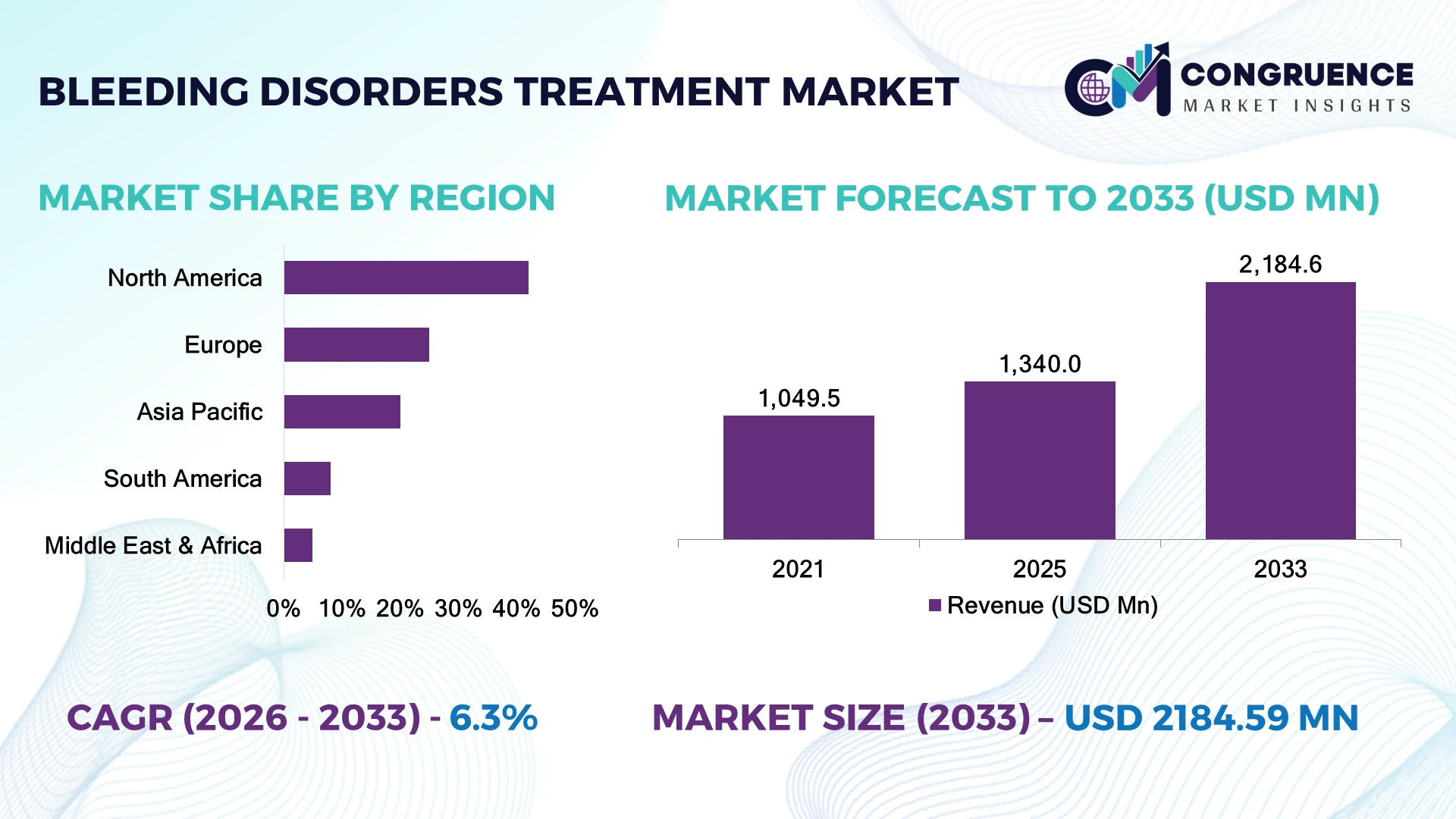

The Global Bleeding Disorders Treatment Market was valued at USD 1,340.0 Million in 2025 and is anticipated to reach a value of USD 2,184.6 Million by 2033 expanding at a CAGR of 6.3% between 2026 and 2033. Growth is driven by rising adoption of recombinant coagulation therapies, expanded gene therapy research, and increasing access to prophylactic treatments for hemophilia patients.

The United States dominates the market with nearly 40% share, supported by advanced hemophilia care infrastructure, strong biotechnology investments, and rapid adoption of extended half-life factor therapies. The country allocates billions toward rare disease innovation, while Europe follows with broader patient access programs and advanced clinical networks. Compared with emerging Asian markets, the U.S. maintains over 60% higher treatment availability through specialized centers.

Strategic focus on precision therapies and scalable manufacturing will define future competitive advantage.

Market Size & Growth: USD 1.34 Billion (2025) to USD 2.18 Billion (2033), 6.3% CAGR, driven by recombinant therapies and gene-based treatment innovation.

Top Growth Drivers: Hemophilia A treatments (45%), prophylactic therapy adoption (35%), and personalized medicine integration (25%) are accelerating market expansion.

Short-Term Forecast: By 2028, digital patient monitoring adoption increases 30%, improving therapy tracking and treatment efficiency.

Emerging Technologies: Gene therapy platforms, AI-assisted diagnosis, and extended half-life factor products are reshaping advanced bleeding disorder management.

Regional Leaders: North America reaches USD 900+ Million with specialty care adoption; Europe exceeds USD 600 Million through public healthcare programs; Asia-Pacific approaches USD 400 Million with expanding access.

Consumer/End-User Trends: Over 55% of patients in developed markets are shifting toward preventive treatment models rather than episodic care.

Pilot/Case Example: 2024 gene therapy programs demonstrated more than 80% reduction in annual bleeding episodes among eligible hemophilia patients.

Competitive Landscape: Leading companies include Takeda Pharmaceutical Company, BioMarin Pharmaceutical, CSL Limited, Bayer AG, and Novo Nordisk.

Regulatory & ESG Impact: Accelerated approvals for rare disease therapies reduce development timelines by nearly 20%, while sustainable biologics manufacturing improves resource efficiency.

Investment & Funding: More than USD 2 Billion has been directed toward rare blood disorder innovation, with partnerships expanding gene therapy pipelines and manufacturing capacity.

Innovation & Future Outlook: Next-generation therapies, decentralized care models, and precision treatment strategies are shifting competition toward long-term clinical outcomes.

The Bleeding Disorders Treatment Market is witnessing stronger demand for long-acting coagulation products, gene therapies, and home-based treatment solutions. Recent innovations in non-factor therapies have improved patient convenience, with preventive treatment adoption increasing by approximately 35% across developed healthcare systems. Supply-chain resilience initiatives following global medicine shortages are encouraging regional manufacturing expansion and diversified biologics production. The market is moving toward personalized and digitally supported care pathways.

The Bleeding Disorders Treatment Market is becoming strategically important as pharmaceutical companies compete to develop durable, patient-centric therapies that reduce treatment burden and improve clinical outcomes. Increasing investment in rare disease pipelines, regulatory acceleration for innovative therapies, and modernization of specialty healthcare infrastructure are transforming competitive priorities.

The industry is shifting from traditional replacement therapies toward advanced biologics, gene therapies, and non-factor treatments. Compared with conventional factor infusion approaches requiring frequent administration, extended half-life therapies reduce treatment frequency by nearly 50%, improving patient adherence and healthcare efficiency. North America leads in commercialization and clinical adoption, while Asia-Pacific is expanding through healthcare infrastructure upgrades and broader access programs.

Companies are strengthening partnerships, expanding manufacturing capabilities, and investing in precision medicine platforms to capture emerging opportunities. For example, integrated specialty care networks and digital monitoring solutions are improving patient management while supporting remote treatment models. Over the next few years, operational efficiency, regulatory agility, and innovation capacity will determine market leadership. Organizations that combine advanced therapies with scalable delivery systems will achieve stronger positioning in the evolving global bleeding disorders treatment landscape.

The shift toward personalized bleeding disorder management is accelerating adoption of recombinant factors, extended half-life therapies, and non-factor treatments. Prophylactic therapy penetration has exceeded 55% among treated hemophilia patients in developed healthcare systems, while recombinant product usage represents over 70% of factor replacement demand in several advanced markets. Regulatory approvals for innovative therapies in the United States and Europe are reducing treatment barriers and improving patient outcomes. Companies are expanding biologics manufacturing, forming gene therapy partnerships, and investing in next-generation coagulation platforms. A key strategic shift is the transition from episodic care models toward preventive treatment ecosystems supported by digital monitoring and specialty care networks.

High production complexity and dependence on specialized biologics manufacturing remain major constraints for market scalability. Advanced coagulation therapies can require annual treatment costs exceeding USD 100,000 per patient in developed economies, limiting accessibility across price-sensitive markets. Plasma-derived therapies still account for a significant share of global treatment supply, creating vulnerability to plasma collection disruptions and logistics challenges. Countries such as India and Brazil face infrastructure gaps, with specialized hemophilia centers concentrated in major cities rather than distributed nationwide. Companies are addressing these limitations through regional manufacturing investments, diversified plasma sourcing networks, long-term supply agreements, and development of lower-frequency treatment alternatives to improve affordability and operational stability.

Emerging gene therapies and digital healthcare platforms are creating new opportunities for long-term treatment transformation. Clinical advancements have demonstrated that certain gene therapy approaches can reduce annual bleeding episodes by more than 80% in eligible hemophilia patients, creating demand for curative treatment models. Countries including the United States, Germany, and Japan are strengthening rare disease innovation programs through accelerated regulatory pathways and advanced clinical infrastructure. Digital adherence platforms and remote monitoring tools are gaining traction, with adoption increasing by approximately 40% among specialty care providers. Companies are positioning through biotechnology partnerships, precision medicine investments, and integrated patient support ecosystems. The strongest opportunity lies in combining advanced therapies with scalable delivery models that reduce lifetime healthcare burden.

The adoption of advanced bleeding disorder treatments faces execution challenges related to specialized healthcare capacity, treatment monitoring, and regulatory complexity. Gene therapy deployment requires highly trained clinical teams, with fewer than 30% of global healthcare facilities equipped for advanced cell and gene therapy administration. Workforce shortages in hematology specialization continue to affect treatment accessibility, particularly outside major urban centers. Additionally, evolving regulatory requirements increase development complexity and commercialization timelines. Companies must strengthen physician training programs, invest in treatment-center networks, and develop standardized patient monitoring systems. Long-term competitiveness will depend on solving operational scalability issues while ensuring consistent access to innovative therapies across diverse healthcare environments.

Gene Therapy Commercialization Shift: Gene therapy adoption is accelerating as treatment centers expand advanced capabilities, with more than 80% reduction in annual bleeding episodes reported in eligible hemophilia patients and clinical screening networks growing by over 30% in developed healthcare systems. Companies are partnering with specialty hospitals and investing in manufacturing capacity to support one-time treatment models, while regulatory pathways in the United States and Europe are reshaping commercialization strategies.

Home-Based Care Expansion: Remote treatment management is changing patient workflows, with more than 50% of hemophilia patients in developed markets using preventive care approaches and digital monitoring adoption increasing approximately 35%. Healthcare providers are integrating connected platforms to improve adherence, reduce hospital visits, and optimize resource utilization. Companies are responding through patient-support programs, mobile health partnerships, and automated therapy tracking solutions.

Biologics Supply Restructuring: Global supply-chain pressure has encouraged manufacturers to diversify plasma sourcing and strengthen regional production networks. Nearly 40% of pharmaceutical companies are prioritizing supply resilience investments, while automated biologics manufacturing improves production efficiency by approximately 25%. Companies are restructuring supplier networks and expanding local facilities to reduce dependency risks exposed during pandemic-era disruptions.

Precision Treatment Integration: Advanced diagnostics and personalized treatment selection are improving clinical decision-making, with precision medicine adoption rising by nearly 30% among specialized healthcare providers. AI-assisted patient monitoring and biomarker analysis are supporting faster therapy optimization. Companies are investing in data-driven platforms and collaborative research models, creating a less visible but important shift toward outcome-based bleeding disorder management.

Recombinant coagulation factor therapies dominate the Bleeding Disorders Treatment Market, accounting for approximately 55% of overall treatment usage due to superior safety profiles, scalable manufacturing, and reduced dependency on plasma-derived inputs. Their established clinical acceptance and integration into hemophilia management protocols have maintained strong demand across the United States, Germany, and Japan. Plasma-derived therapies continue to serve critical patient groups, representing nearly 30% of treatment adoption, particularly where affordability and accessibility remain important considerations. The fastest-growing segment is gene therapy, supported by increasing investment in curative treatment approaches and advanced clinical infrastructure. Adoption of gene-based treatments is expanding as healthcare systems evaluate long-term cost benefits and improved patient quality of life. Companies are increasing research partnerships, expanding specialized treatment centers, and prioritizing next-generation coagulation platforms. Industry focus is shifting toward therapies that reduce administration frequency, with more than 40% of pipeline investments targeting longer-duration or one-time treatment solutions.

Hemophilia treatment represents the leading application segment with an estimated 65% market share, driven by the high clinical need for factor replacement therapies, prophylaxis programs, and specialized monitoring. Hemophilia A remains the largest treatment category due to a broader patient population and higher dependence on factor VIII therapies. Von Willebrand disease and other bleeding disorder applications contribute additional demand, supported by improved diagnosis and awareness programs. The fastest-growing application area is preventive and personalized treatment management, where digital monitoring and individualized dosing strategies are gaining adoption. More than 45% of specialty treatment centers are integrating patient monitoring technologies to improve therapy outcomes and reduce emergency interventions. Companies are expanding patient assistance programs, developing non-factor therapies, and strengthening partnerships with hematology networks. The market is transitioning from reactive bleeding control toward continuous disease management models, creating stronger operational value for healthcare providers.

Hospitals and specialized hematology centers represent the dominant end-user segment, accounting for approximately 60% of treatment utilization due to their advanced diagnostic infrastructure, trained specialists, and ability to administer complex therapies. Large healthcare institutions in the United States, Germany, and Japan continue to drive adoption of recombinant therapies and emerging treatment platforms. Specialty clinics are expanding their role by providing dedicated patient monitoring and long-term disease management services. The fastest-growing end-user group is specialty treatment networks and outpatient care providers, supported by the shift toward decentralized healthcare delivery. Adoption of outpatient management models is increasing by nearly 35% as patients seek convenient preventive treatment options. Research institutions and pharmaceutical companies also remain strategically important through clinical trials and innovation partnerships. Companies are developing customized support programs, expanding provider collaborations, and investing in education initiatives to improve treatment accessibility. Future demand is shifting toward integrated care ecosystems combining hospitals, digital platforms, and specialized outpatient services.

North America accounted for the largest market share at 42% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America holds the leading position in the Bleeding Disorders Treatment Market due to strong hematology networks, advanced reimbursement systems, and rapid adoption of recombinant and gene-based therapies. The region contributes nearly 42% of global treatment activity, supported by high concentration of specialty care centers and biotechnology manufacturing capabilities. The United States drives most regional demand, with more than 140 hemophilia treatment centers supporting specialized patient management. Pharmaceutical companies are expanding clinical partnerships, investing in next-generation coagulation therapies, and strengthening domestic manufacturing capabilities to improve supply reliability.

United States Market Outlook: The United States remains the strategic hub for bleeding disorder innovation due to advanced clinical infrastructure, biotechnology investment, and regulatory support for rare disease therapies. More than 30% of global clinical trials for advanced hemophilia treatments are conducted through U.S.-based research networks. Companies are focusing on gene therapy commercialization, digital patient monitoring, and specialized treatment expansion to improve long-term care delivery.

Europe maintains a strong market position through coordinated healthcare systems, advanced pharmaceutical manufacturing, and increasing adoption of personalized bleeding disorder treatments. The region contributes nearly 25% of global treatment. Countries such as Germany, France, and the United Kingdom account for a significant share of regional treatment deployment due to established hematology networks. Approximately 35% of European patients benefit from structured prophylactic care programs, supported by improved diagnosis and treatment accessibility. Regulatory initiatives supporting rare disease innovation are encouraging pharmaceutical partnerships and technology adoption. Companies are strengthening regional production capabilities, expanding specialty care collaborations, and developing patient-focused treatment pathways.

Germany Market Outlook: Germany represents a leading European market due to its advanced healthcare infrastructure, pharmaceutical manufacturing base, and strong reimbursement framework. The country operates more than 100 specialized hemophilia treatment facilities, enabling wider access to advanced therapies. Companies are increasing investments in biologics development, clinical research collaborations, and precision treatment solutions to strengthen market presence.

Asia-Pacific is emerging as the fastest-expanding market due to healthcare infrastructure development, rising diagnosis rates, and increasing investment in specialty treatment facilities. Countries including China, Japan, South Korea, and India are improving access to advanced coagulation therapies through healthcare modernization programs. The region currently represents nearly 20% of global treatment demand, with adoption concentrated in urban medical centers. China is expanding domestic biotechnology production, while Japan continues to lead in advanced therapy adoption. Companies are forming local partnerships, increasing manufacturing capacity, and introducing affordable treatment models to address accessibility challenges.

China Market Outlook: China is becoming a major growth center due to expanding biotechnology capabilities, government healthcare initiatives, and increasing investment in rare disease treatment infrastructure. The country has more than 50 specialized hemophilia care centers supporting diagnosis and treatment programs. Pharmaceutical companies are increasing local production, developing innovative therapies, and collaborating with healthcare institutions to improve treatment availability.

South America is gradually strengthening its bleeding disorder treatment ecosystem through improved healthcare programs, specialized centers, and international treatment collaborations. Brazil and Argentina represent major contributors due to larger patient populations and expanding hematology infrastructure. The region accounts for nearly 8% of global treatment activity, with adoption concentrated in major urban hospitals. Public healthcare initiatives are improving access to factor therapies, while supply-chain limitations continue to influence treatment consistency. Companies are supporting market development through partnerships with healthcare organizations, localized distribution networks, and patient education programs.

Brazil Market Outlook: Brazil leads the South American market due to its extensive public healthcare system and growing focus on rare disease management. The country has more than 30 hemophilia treatment centers supporting patient care and monitoring. Pharmaceutical companies are expanding distribution partnerships, improving therapy availability, and investing in local healthcare collaborations to strengthen long-term treatment access.

The Middle East & Africa market is developing through healthcare modernization, government investment programs, and expansion of specialized medical facilities. Adoption remains concentrated in countries with stronger healthcare infrastructure, including Saudi Arabia, the United Arab Emirates, and South Africa. The region contributes approximately 5% of global treatment demand, with increasing focus on improving diagnosis and specialist availability. Healthcare transformation initiatives are supporting advanced treatment adoption, while partnerships with international pharmaceutical companies are improving supply reliability. Companies are investing in regional distribution networks, training programs, and specialized treatment centers to address accessibility gaps.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a strategically important market due to healthcare modernization programs, investment in specialty hospitals, and increasing focus on rare disease management. The country has expanded specialized hematology services across major medical institutions, improving access to advanced therapies. Pharmaceutical companies are developing local partnerships and strengthening supply networks to support future treatment expansion.

The Bleeding Disorders Treatment Market features competition between global pharmaceutical leaders such as Takeda, CSL Behring, Bayer, Novo Nordisk, Pfizer, and Roche-backed innovators versus specialized biotechnology companies developing gene and non-factor therapies. Top five players collectively account for approximately 45% of market activity, with competition centered on technology differentiation, supply reliability, and treatment outcomes. Advanced therapies capture growing preference, with extended half-life products reducing administration frequency by nearly 50% compared with conventional approaches. Companies compete through gene therapy pipelines, strategic partnerships, manufacturing expansion, and patient-support ecosystems. Biotech innovators challenge established factor replacement suppliers through disruptive platforms, while cost-focused manufacturers strengthen accessibility in emerging markets. High regulatory barriers, complex biologics production, and specialized clinical infrastructure limit new entrants. Winning requires combining breakthrough therapy development, scalable manufacturing, strong distribution networks, and long-term patient care integration.

CSL Limited

Bayer AG

Novo Nordisk

Pfizer Inc.

Roche

BioMarin Pharmaceutical

Octapharma AG

Sanofi

Sobi

Grifols

Kedrion Biopharma

Advanced biologics, gene therapies, and non-factor treatments are reshaping bleeding disorder management by improving treatment durability and reducing administration burden. Extended half-life coagulation products deliver approximately 30–50% fewer infusion requirements compared with conventional factor therapies, improving patient adherence. Gene therapy platforms are gaining clinical adoption as specialized centers expand capabilities, with treatment models shifting from continuous replacement toward long-duration therapeutic approaches.

Digital health integration is becoming a key operational advantage through remote monitoring, patient tracking, and personalized dosing systems. Approximately 35% of specialty care providers are increasing adoption of digital management tools to improve workflow efficiency and treatment visibility. Compared with traditional manual monitoring methods, connected platforms improve data accessibility and reduce administrative workload by nearly 20%. Companies benefiting most are those combining therapies with patient-support ecosystems.

Between 2026 and 2028, AI-assisted diagnostics, biomarker analysis, and automated clinical decision tools will influence treatment optimization. Precision medicine approaches are expected to improve therapy selection accuracy and strengthen competitive positioning. Organizations investing in integrated technology platforms, manufacturing automation, and data-driven care models will gain operational advantages as the market transitions toward personalized bleeding disorder management.

March 2025 Sanofi received FDA approval for Qfitlia (fitusiran) for hemophilia A and B prophylaxis, introducing a less frequent treatment option. Clinical evaluation involved 177 participants, strengthening Sanofi’s non-factor therapy position. Source: www.fda.gov

October 2024 Pfizer Inc. gained FDA approval for Hympavzi, a non-factor prophylactic therapy for hemophilia A and B. The therapy reduced annualized bleeding rates from 38 to 3.2 in study comparisons, expanding competition beyond replacement factors. Source: www.fda.gov

April 2024 Pfizer Inc. expanded hemophilia B innovation with Beqvez gene therapy approval in the United States. Clinical results showed 60% of treated patients achieved elimination of bleeding events after one year, supporting adoption of one-time treatment models. Source: www.reuters.com

June 2025 BioMarin Pharmaceutical presented updated long-term Roctavian data at a global hematology meeting, reinforcing gene therapy research momentum. Five-year follow-up showed sustained factor activity levels in treated patients, influencing future hemophilia treatment strategies.

The Bleeding Disorders Treatment Market Report covers comprehensive analysis across treatment types, applications, end-users, regional markets, and competitive landscapes. The study evaluates recombinant therapies, plasma-derived treatments, gene therapies, and emerging non-factor solutions across hemophilia management and other bleeding disorder applications. Coverage includes hospitals, specialty treatment centers, research institutions, and pharmaceutical organizations across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report analyzes technology adoption patterns, manufacturing strategies, regulatory developments, and innovation trends shaping market direction between 2026 and 2033. It provides strategic insights into investment priorities, expansion opportunities, partnership models, and competitive positioning. The analysis supports stakeholders in identifying high-potential segments, improving operational decisions, and developing long-term strategies within the evolving global bleeding disorders treatment ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,340.0 Million |

| Market Revenue (2033) | USD 2,184.6 Million |

| CAGR (2026–2033) | 6.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Takeda Pharmaceutical Company; CSL Limited; Bayer AG; Novo Nordisk; Pfizer Inc.; Roche; BioMarin Pharmaceutical; Octapharma AG; Sanofi; Sobi; Grifols; Kedrion Biopharma |

| Customization & Pricing | Available on Request (10% Customization Free) |