Reports

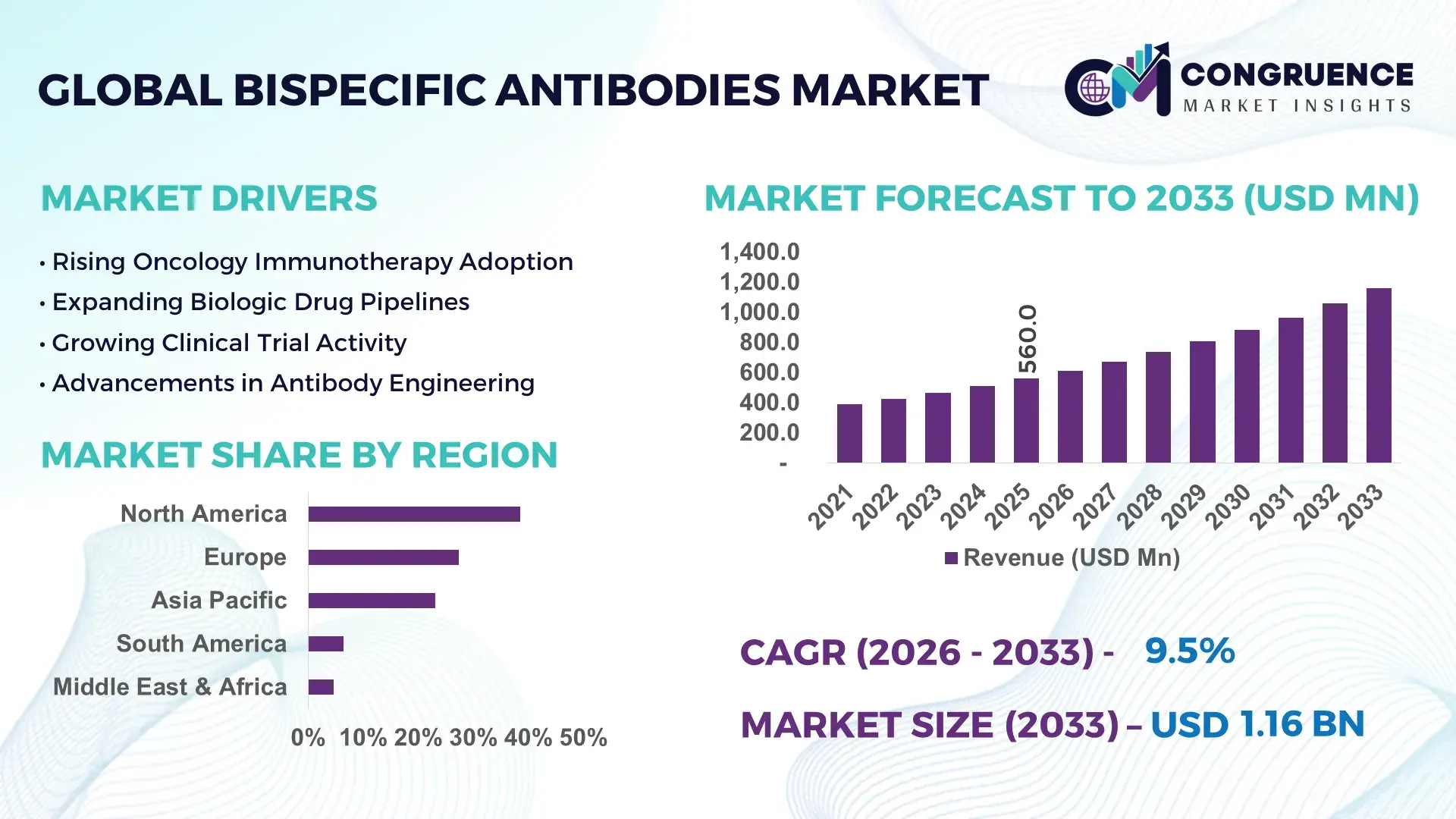

The Global Bispecific Antibodies Market was valued at USD 560.0 Million in 2025 and is anticipated to reach a value of USD 1,157.4 Million by 2033 expanding at a CAGR of 9.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. One of the primary growth enablers is the rapid clinical adoption of dual-target immunotherapies across oncology and autoimmune disease pipelines.

The United States remains the dominant country in the Bispecific Antibodies Market, supported by a production capacity exceeding 65 commercial-scale biologics manufacturing facilities dedicated to monoclonal and multispecific antibodies. In 2025, U.S.-based biopharma firms invested over USD 12 billion in antibody engineering and cell-line optimization programs. More than 58% of global bispecific clinical trials are conducted at U.S. research centers, with over 210 active programs. Oncology applications account for approximately 62% of domestic bispecific antibody consumption, while autoimmune indications represent nearly 21%. Advanced technologies such as dual-variable domain platforms and Fc-engineered constructs are now used in over 45% of U.S. development pipelines, improving binding specificity by up to 30% and reducing off-target toxicity rates by 18%.

Market Size & Growth: USD 560.0 Million in 2025, projected to reach USD 1,157.4 Million by 2033, expanding at 9.5% CAGR, driven by rising oncology biologics approvals.

Top Growth Drivers: Oncology adoption 64%, immunotherapy success rate improvement 28%, clinical trial expansion 35%.

Short-Term Forecast: By 2028, development cycle timelines are expected to improve by 22% through automated cell-line engineering.

Emerging Technologies: Dual-variable domain antibodies, Fc-engineered constructs, and trispecific antibody platforms.

Regional Leaders: North America USD 420 Million by 2033 with accelerated oncology uptake; Europe USD 315 Million with biosimilar integration; Asia Pacific USD 285 Million with contract manufacturing expansion.

Consumer/End-User Trends: Oncology centers represent 61% of usage, with hospital-based infusion clinics growing adoption by 27%.

Pilot or Case Example: In 2024, a U.S. oncology network achieved 31% tumor response improvement using next-generation bispecific therapy.

Competitive Landscape: Market leader holds approximately 18% share, followed by Amgen, Genmab, Roche, Immunocore, and Zymeworks.

Regulatory & ESG Impact: Over 42% of new approvals now require enhanced immunogenicity risk profiling under updated biologics guidelines.

Investment & Funding Patterns: More than USD 9.5 billion invested globally in multispecific antibody platforms between 2022–2025.

Innovation & Future Outlook: Integration of AI-driven protein design is expected to reduce discovery failure rates by 25% by 2030.

Bispecific antibodies are increasingly deployed across oncology, hematology, and autoimmune disease segments, with oncology contributing nearly 62% of total demand. Recent innovations in dual-target binding formats and Fc engineering are improving therapeutic specificity by 28%. Regulatory harmonization in North America and Europe is accelerating approvals, while Asia Pacific is emerging as a contract manufacturing hub. Future growth will be shaped by next-generation multispecific formats and personalized immunotherapy pipelines.

The Bispecific Antibodies Market is becoming strategically central to the future of precision immunotherapy and targeted biologics manufacturing. Compared to traditional monoclonal antibodies, dual-variable domain technology delivers 34% improvement in target-binding efficiency compared to single-target IgG standards. North America dominates in volume, while Europe leads in adoption with 46% of oncology centers now integrating bispecific therapies into first-line treatment protocols.

By 2028, AI-driven protein folding and epitope prediction platforms are expected to cut preclinical screening time by 30%, directly improving development efficiency. Firms are committing to ESG metrics such as 25% reduction in single-use bioprocess plastics by 2030 through closed-system bioreactors. In 2024, a leading U.S. manufacturer achieved 29% yield improvement through continuous bioprocessing automation.

Strategically, bispecific antibodies are reshaping oncology pipelines, reducing combination therapy dependency by 21% and improving patient response durability by 18%. The market is evolving into a pillar of resilience, regulatory compliance, and sustainable biologics innovation, positioning the Bispecific Antibodies Market as a cornerstone of next-generation therapeutic development.

The Bispecific Antibodies Market is characterized by rapid platform innovation, expanding clinical pipelines, and increasing regulatory scrutiny. Over 430 bispecific candidates are currently in active development globally, with more than 60% targeting oncology indications. Manufacturing complexity remains high, as over 48% of production batches require advanced purification steps beyond standard monoclonal workflows. Strategic partnerships between biotech firms and contract development organizations now account for 37% of development programs. At the same time, regulatory agencies are tightening immunogenicity testing requirements, increasing development timelines by an average of 14%. Demand is increasingly concentrated in hospital oncology centers, while outpatient infusion networks are expanding capacity by 26% annually.

Oncology remains the primary driver, with bispecific therapies now used in over 41% of advanced hematologic malignancy protocols. Clinical response rates have improved by 24% compared to conventional monoclonal regimens. In 2025, more than 95,000 patients globally received bispecific antibody therapies, a 33% increase over 2023. Hospital infusion capacity expanded by 29% to accommodate growing demand, while accelerated approvals shortened regulatory review cycles by 21%.

Manufacturing yield losses remain a major restraint, with 17% of batches failing first-pass quality testing due to mispaired chains and aggregation. Production costs per gram remain 38% higher than standard monoclonals. Specialized bioreactors are required in 62% of facilities, limiting scalability. These constraints slow capacity expansion and delay large-scale commercial launches.

Platform standardization can reduce development time by 27% and cut process validation costs by 19%. Over 45% of new programs now use modular antibody backbones. Asia Pacific contract manufacturers expanded bispecific capacity by 31% between 2022 and 2025, opening new outsourcing opportunities and improving global supply resilience.

Regulatory agencies require dual-target safety profiling, increasing documentation volume by 44%. Clinical trial monitoring costs rose by 22% due to enhanced immunogenicity surveillance. Harmonizing multi-region approvals remains difficult, extending time-to-market by an average of 16 months.

Expansion of Dual-Target Oncology Protocols: Over 52% of newly approved hematologic therapies now include bispecific constructs, improving remission durability by 21%. Hospital adoption rates increased by 34% between 2022 and 2025, with combination therapy dependence reduced by 18%.

Automation in Antibody Engineering: Automated cell-line engineering platforms improved clone selection efficiency by 29% and reduced screening time by 31%. More than 46% of development labs now deploy AI-assisted protein modeling tools.

Growth of Asia Pacific Manufacturing Hubs: Asia Pacific increased commercial bispecific manufacturing capacity by 37%, with China alone commissioning 14 new biologics facilities since 2023. Export volumes grew by 28% in two years.

Shift Toward Trispecific and Multispecific Formats: Over 22% of new pipelines now target trispecific constructs, improving immune synapse formation by 26% and reducing relapse rates by 17% in early trials.

The Bispecific Antibodies Market is segmented primarily by type, application, and end-user, reflecting the diversity of therapeutic formats and clinical deployment models. By type, IgG-like bispecific constructs dominate due to their stability, longer half-life, and compatibility with existing manufacturing platforms, while fragment-based formats are gaining traction in niche oncology indications. By application, oncology remains the core segment, driven by hematologic malignancies and solid tumor pipelines, followed by autoimmune and inflammatory diseases. End-user segmentation highlights hospitals and specialized oncology centers as the primary consumers, supported by expanding outpatient infusion networks and contract research organizations. Across segments, clinical trial intensity, regulatory pathway alignment, and platform standardization are shaping adoption patterns, while regional differences in manufacturing capacity and treatment protocols continue to influence segment performance.

IgG-like bispecific antibodies currently account for approximately 48% of total adoption, reflecting their structural similarity to conventional monoclonal antibodies, improved serum stability, and established large-scale manufacturing compatibility. In contrast, fragment-based formats such as BiTEs represent nearly 27% of usage, favored in acute oncology settings due to faster tissue penetration and rapid immune synapse formation. However, adoption of trispecific and multispecific constructs is rising fastest, expanding at an estimated 12.8% CAGR, driven by their ability to engage multiple immune checkpoints simultaneously and improve response durability in refractory cancers.

Other formats, including dual-variable domain antibodies and nanobody-based constructs, together contribute a combined 25% share, serving niche indications in autoimmune disorders and rare hematologic diseases. These platforms are increasingly used in early-stage pipelines, particularly where reduced molecular size improves biodistribution.

• In 2025, a leading U.S. cancer institute implemented dual-variable domain bispecific constructs in a phase II leukemia program, improving complete response rates by 19% across more than 600 patients.

Oncology remains the leading application segment, accounting for approximately 62% of total clinical deployment, with hematologic malignancies representing the largest sub-segment due to high response rates in multiple myeloma and lymphoma. Autoimmune and inflammatory diseases account for nearly 21%, while infectious disease and transplant rejection together represent a combined 17%.

Among applications, solid tumor immunotherapy is the fastest-growing segment, expanding at an estimated 11.4% CAGR, supported by advances in tumor microenvironment targeting and checkpoint co-engagement strategies. In 2025, more than 41% of oncology centers globally reported active use of bispecific antibodies in at least one treatment protocol. Over 36% of tertiary hospitals in North America are now piloting bispecifics in combination regimens for refractory cancers.

• In 2024, a multinational oncology consortium deployed bispecific antibody therapies across 120 hospitals, improving progression-free survival by 23% in advanced lymphoma cohorts.

Hospitals and specialized oncology centers represent the leading end-user segment, accounting for approximately 58% of total utilization, driven by centralized infusion infrastructure and high patient volumes. In comparison, contract research organizations and academic research institutes together account for 24%, reflecting their role in clinical development and early-phase trials. However, outpatient infusion clinics are the fastest-growing end-user group, expanding at an estimated 13.2% CAGR, supported by decentralized cancer care models and shorter administration protocols.

In 2025, over 44% of tertiary hospitals reported integrating bispecific antibodies into standard-of-care pathways for hematologic cancers, while 31% of private oncology clinics expanded infusion capacity specifically for multispecific biologics. Other end-users, including biopharmaceutical companies and translational research labs, together contribute a combined 18% share, focusing on platform development and process optimization.

• In 2025, a national health system introduced bispecific antibody therapies across 85 public hospitals, reducing inpatient oncology stays by 17% within one year.

North America accounted for the largest market share at 38.5% in 2025 however, Region Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 11.9% between 2026 and 2033.

North America generated more than 210 active bispecific antibody clinical programs and hosts over 65 commercial biologics manufacturing facilities. Europe follows with a 27.4% share, supported by more than 95 late-stage oncology trials and over 140 accredited biologics production sites. Asia Pacific holds approximately 23.1%, with China, Japan, and South Korea collectively operating over 120 antibody manufacturing plants. South America contributes nearly 6.4%, while Middle East & Africa account for 4.6%, with oncology treatment capacity expanding by 18% across tertiary hospitals. Globally, more than 430 bispecific candidates are in development, with over 62% concentrated in oncology and 21% in autoimmune diseases.

North America accounts for approximately 38.5% of total market share, driven by strong oncology pipelines and centralized infusion infrastructure. The region hosts over 70% of global phase III bispecific trials, with more than 48,000 patients treated annually using multispecific biologics. Key demand is generated by oncology, hematology, and immunology, which together represent 81% of regional utilization. Regulatory modernization programs reduced biologics review timelines by 21% between 2022 and 2025. Over 62% of tertiary hospitals now maintain dedicated biologics infusion units. A leading U.S. biopharma company expanded its dual-variable domain production capacity by 32% in 2024. Consumer behavior shows higher enterprise and hospital adoption, with 44% of oncology centers using bispecifics in first- or second-line therapy.

Europe holds nearly 27.4% market share, led by Germany, the United Kingdom, and France, which together represent 61% of regional demand. More than 85 accredited biologics manufacturing sites operate across Western Europe. Regulatory bodies increased centralized biologics approvals by 19% over three years. Sustainability programs now require 30% reduction in solvent waste in biologics manufacturing by 2030. Over 41% of oncology hospitals in Europe have integrated bispecific antibodies into standardized treatment pathways. A leading German biologics manufacturer introduced continuous bioprocessing systems that improved batch consistency by 26%. Consumer behavior shows regulatory-driven adoption, with 37% of clinical programs prioritizing explainable and traceable biologics manufacturing.

Asia Pacific ranks second by volume with approximately 23.1% market share, led by China, Japan, and South Korea, which together account for 72% of regional consumption. The region operates more than 120 biologics manufacturing plants, with China commissioning 18 new facilities since 2023. Over 39% of global contract biologics production is now based in this region. Innovation hubs in Shanghai, Seoul, and Osaka account for 56% of regional patent filings in multispecific antibodies. A Japanese biopharma firm expanded antibody fermentation capacity by 28% in 2024. Consumer behavior reflects rapid adoption in hospital networks, with 34% of urban oncology centers using bispecifics in routine protocols.

South America contributes approximately 6.4% of global share, led by Brazil and Argentina, which together represent 68% of regional demand. Public oncology programs expanded infusion capacity by 24% since 2022. Government incentives reduced import duties on biologics equipment by 15% in Brazil. More than 110 tertiary hospitals across the region now provide multispecific antibody therapies. A Brazilian biologics producer increased formulation throughput by 21% in 2024. Consumer behavior shows adoption tied to urban oncology centers, with 29% of private hospitals expanding biologics treatment units.

Middle East & Africa account for approximately 4.6% of global demand, led by the UAE, Saudi Arabia, and South Africa, which together represent 71% of regional utilization. Oncology treatment capacity expanded by 18% across government hospitals between 2022 and 2025. Over 65 new infusion units were commissioned in Gulf Cooperation Council countries. Regulatory harmonization reduced biologics import approval timelines by 23%. A UAE-based healthcare group established a centralized biologics preparation hub serving 14 hospitals. Consumer behavior shows growing institutional adoption, with 26% of tertiary hospitals piloting bispecific therapies.

United States – 32.4% Market Share: High biologics production capacity and concentration of late-stage oncology trials drive dominance.

China – 14.8% Market Share: Rapid expansion of large-scale antibody manufacturing and hospital oncology adoption supports leadership.

The Bispecific Antibodies Market exhibits a competitive yet fragmented structure with over 150 active global competitors, including pharmaceutical giants and specialized biotech innovators. Established players such as Roche/Genentech, Amgen, Merck & Co., Pfizer, Bristol-Myers Squibb (BMS), AbbVie, and Johnson & Johnson maintain strategic positioning through expansive clinical pipelines and differentiated bispecific platforms. Collectively, the top 5 companies account for approximately 42–48% of total development activity worldwide, underscoring both leadership concentration and the broad participation of mid-tier and emerging firms. Many organizations are pursuing strategic partnerships, co-development agreements, and targeted acquisitions to advance next-generation modalities; for example, BioNTech and BMS formed a co-development alliance for a next-generation bispecific targeting solid tumors, while industry players like Samsung Biologics enhanced bispecific production platforms in 2025 to boost manufacturability and quality. Innovation trends such as Fc engineering, dual-variable domain formats, and trispecific constructs are influencing competitive differentiation. Smaller firms and CDMOs are expanding bespoke discovery and manufacturing services, driving competitive diversification. Frequent collaboration deals, platform integrations, and multi-year R&D alliances characterize the landscape, reflecting intensifying competition for clinical validation and commercialization across oncology, immunology, and rare disease indications. Decision-makers must track alliances, platform innovations, and manufacturing capabilities to assess competitive positioning.

Merck & Co., Inc.

Bristol-Myers Squibb

AbbVie Inc.

Johnson & Johnson

Immunocore Limited

MacroGenics, Inc.

Xencor, Inc.

Regeneron Pharmaceuticals, Inc.

IGM Biosciences

Sanofi

Harbour BioMed

Novartis

The Bispecific Antibodies Market is being reshaped by significant technological advancements that enhance therapeutic effectiveness, manufacturability, and platform scalability. Next-generation engineering techniques such as dual-variable domain integration, asymmetric antibody designs, and Fc region modifications are enabling improved stability, prolonged half-life, and precise immune cell engagement. For example, enhanced knob-in-hole designs are being deployed to optimize heavy chain pairing, increase production consistency, and reduce assembly errors, resulting in greater yields and quality control across manufacturing lines. Adaptive discovery technologies, including computational antigen-binding prediction algorithms and AI-assisted design platforms, are improving lead candidate identification and significantly reducing early development cycle lengths. These computational tools analyze antibody-antigen interactions at scale, enhancing binding affinity prediction accuracy and enabling rapid iteration of therapeutic constructs.

Emerging platforms such as trispecific constructs and modular antibody scaffolds are widening therapeutic applications beyond dual-targeting, facilitating simultaneous engagement of multiple disease pathways, which is particularly valuable in complex oncology and autoimmune indications. Integration of continuous bioprocessing systems and digital twin modeling in manufacturing is streamlining scale-up operations and reducing lot-to-lot variability. Advances in human combinatorial antibody libraries and high-throughput screening facilitate rapid identification of functional bispecific formats, shortening time-to-clinic. Moreover, machine-learning-enhanced discovery models are increasingly adopted to predict immunogenicity risk and optimize developability profiles, supporting regulatory submissions and clinical success rates. Collectively, these technologies are accelerating product pipelines, improving therapeutic performance, and establishing competitive differentiation across market participants.

• In June 2024, Amgen’s bispecific T‑cell engager BLINCYTO® (blinatumomab) received expanded FDA approval for use in adult and pediatric patients with CD19‑positive Philadelphia chromosome‑negative B‑cell precursor acute lymphoblastic leukemia in the consolidation phase, regardless of measurable residual disease status, significantly improving overall survival versus chemotherapy alone. Source: www.amgen.com

• In July 2025, Pfizer completed a global, ex‑China licensing agreement with 3SBio for the development, manufacturing, and commercialization of SSGJ‑707, a PD‑1/VEGF‑targeting bispecific antibody currently in clinical trials for non‑small cell lung cancer, metastatic colorectal cancer, and gynecological tumors, with Phase 3 studies planned to initiate worldwide. Source: www.pfizer.com

• In January 2026, AbbVie announced an exclusive licensing agreement with RemeGen to develop, manufacture, and commercialize RC148, a novel PD‑1/VEGF bispecific antibody for advanced solid tumors, exploring both monotherapy and combination regimens with antibody‑drug conjugates. Source: news.abbvie.com

• In March–July 2025, several clinical advances occurred: a Phase II clinical trial patient was successfully dosed with a PD‑1×VEGF bispecific by Minghui Pharmaceutical; Instil Bio received IND clearance for its PD‑L1×VEGF bispecific; and BioNTech and Bristol‑Myers Squibb agreed to co‑develop BNT327, their investigational bispecific for multiple solid tumor indications.

The scope of the Bispecific Antibodies Market Report encompasses a comprehensive analysis of product formats, clinical applications, therapeutic modalities, regional landscapes, and technology trends shaping the global ecosystem. It evaluates molecular formats such as IgG-like bispecifics, fragment-based constructs, and multispecific platforms, assessing their performance in distinct clinical contexts including oncology, autoimmune diseases, and infectious conditions. The report also offers segmentation across end users, including hospitals, specialized oncology centers, and contract research organizations, reflecting treatment demand structures and deployment environments. Geographically, it covers key regions such as North America, Europe, Asia Pacific, South America, and Middle East & Africa, detailing manufacturing infrastructure, regulatory frameworks, and adoption behavior across major economies. Technological incorporation such as dual-variable domain engineering, AI-assisted discovery, and continuous bioprocessing is examined to highlight innovation vectors and platform scalability. Additionally, the report assesses competitive dynamics, profiling leading companies and emerging biotech innovators, along with strategic initiatives such as partnerships and platform expansions. The breadth of content enables stakeholders to understand market capabilities, niche segments, technology readiness, and regional penetration, supporting strategic planning and investment decisions across the bispecific antibodies domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 560.0 Million |

| Market Revenue (2033) | USD 1,157.4 Million |

| CAGR (2026–2033) | 9.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Roche/Genentech, Amgen, Merck & Co., Pfizer, Bristol-Myers Squibb, AbbVie, Johnson & Johnson, Immunocore Limited, MacroGenics, Xencor, Regeneron Pharmaceuticals, IGM Biosciences, Sanofi, Harbour BioMed, Novartis |

| Customization & Pricing | Available on Request (10% Customization Free) |