Reports

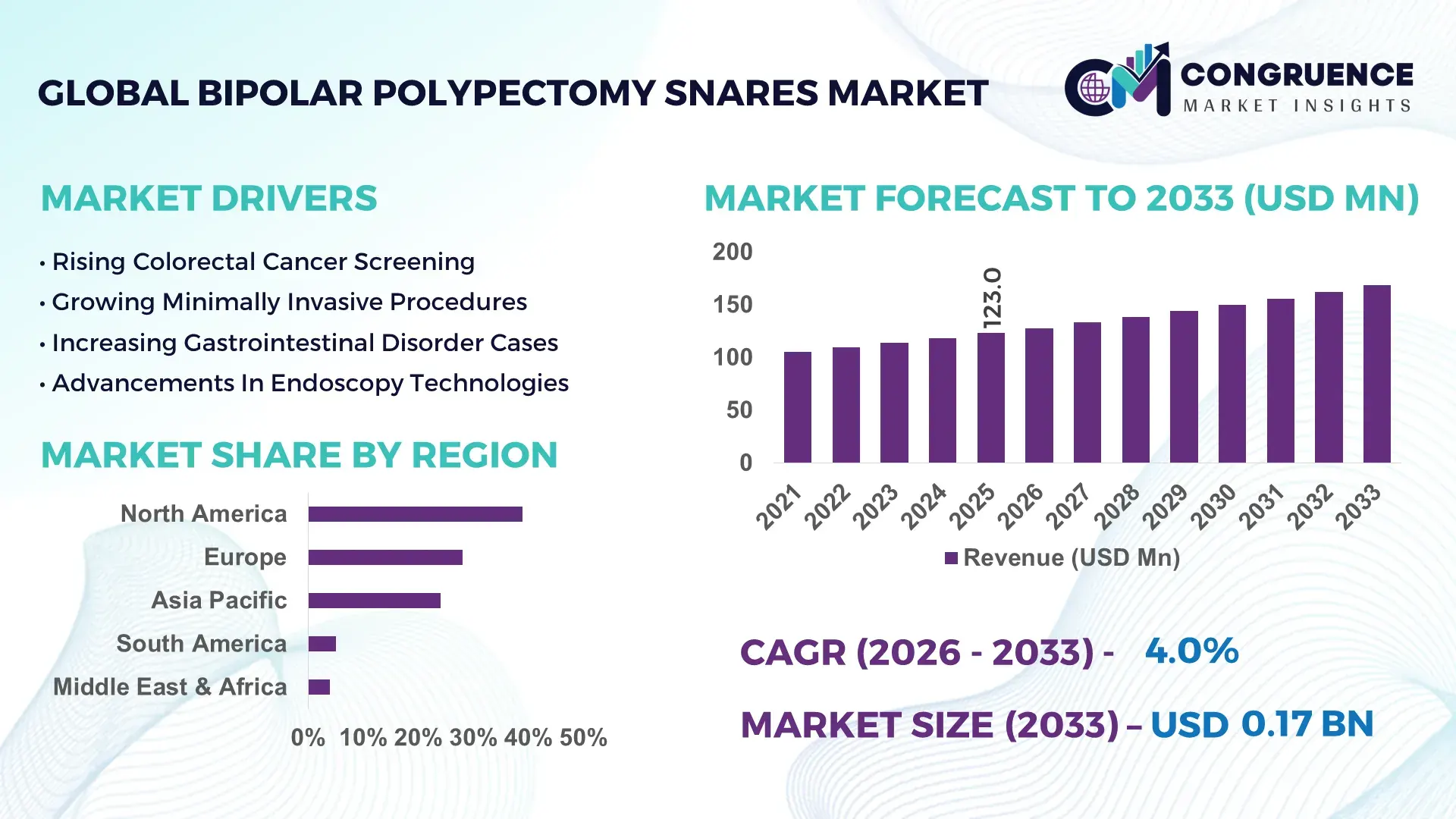

The Global Bipolar Polypectomy Snares Market was valued at USD 123.0 Million in 2025 and is anticipated to reach a value of USD 168.3 Million by 2033 expanding at a CAGR of 4.0% between 2026 and 2033. Rising colorectal cancer screening volumes, growing adoption of minimally invasive gastrointestinal procedures, and the transition toward precision electrosurgical devices are accelerating demand for advanced bipolar polypectomy snares across hospitals and ambulatory endoscopy centers globally. The market is also benefiting from higher procedural efficiency, as bipolar systems reduce thermal injury risk by nearly 28% compared to conventional monopolar alternatives, improving patient recovery timelines and procedural safety standards. Between 2024 and 2026, healthcare systems across North America, Europe, and Asia-Pacific increased investments in outpatient endoscopy infrastructure while tightening regulatory oversight around surgical energy devices and infection control standards. This shift has pushed manufacturers toward single-use and high-precision bipolar technologies to meet evolving clinical compliance requirements and optimize operational throughput during rising colonoscopy volumes.

The United States dominates the global Bipolar Polypectomy Snares Market with approximately 36% market share, supported by over 15 million colonoscopy procedures conducted annually and strong adoption of advanced GI endoscopy technologies across integrated hospital networks. More than 62% of high-volume endoscopy centers in the country now prioritize bipolar electrosurgical accessories due to improved cutting precision and lower adverse-event rates. Compared to several emerging Asian markets, the U.S. demonstrates nearly 2.3x higher penetration of disposable bipolar snares, driven by reimbursement alignment, early-stage colorectal screening adoption, and sustained investment in minimally invasive procedural ecosystems.

Strategic competition is increasingly shifting toward high-performance disposable platforms, forcing manufacturers to optimize clinical outcomes, procedural speed, and regulatory differentiation simultaneously.

Market Size & Growth: The market is projected to expand from USD 123.0 Million in 2025 to USD 168.3 Million by 2033 at a 4.0% CAGR, driven by rising adoption of advanced electrosurgical endoscopy systems and minimally invasive gastrointestinal procedures.

Top Growth Drivers: Outpatient endoscopy volumes increased by 18%, demand for precision bipolar energy systems rose by 22%, and single-use device adoption expanded by 27% across high-throughput hospitals.

Short-Term Forecast: By 2028, procedure turnaround time is expected to improve by 21% while device-related thermal injury risks decline by nearly 16% through advanced bipolar control integration.

Emerging Technologies: AI-assisted endoscopic imaging, insulated wire-loop materials, and next-generation bipolar energy modulation systems improved procedural precision by over 24% in complex polypectomy procedures.

Regional Leaders: North America leads with approximately USD 47 Million demand concentration, Europe exceeds USD 34 Million through compliance-driven adoption, while Asia-Pacific surpasses USD 29 Million with localized manufacturing expansion.

Consumer/End-User Trends: More than 61% of tertiary hospitals now prioritize disposable bipolar snares to reduce cross-contamination risks and improve operational efficiency in high-volume endoscopy centers.

Pilot/Case Example: In 2025, a multi-hospital gastrointestinal care network reduced procedure-related bleeding complications by 19% after deploying advanced bipolar polypectomy snare systems across 120+ endoscopy suites.

Competitive Landscape: The top five players collectively control nearly 58% of global market activity, with Olympus, Boston Scientific, CONMED, Medtronic, and Cook Medical expanding high-performance device portfolios.

Regulatory & ESG Impact: Stricter sterilization compliance standards and hospital sustainability programs reduced reusable-device processing costs by 14% while accelerating adoption of recyclable procedural components.

Investment & Funding: More than USD 310 Million in strategic funding and manufacturing investments flowed into advanced gastrointestinal device development between 2024 and 2026 amid regional supply chain diversification.

Innovation & Future Outlook: Hybrid bipolar-snare platforms, robotic-assisted endoscopy integration, and smart energy feedback systems are reshaping precision gastrointestinal treatment and accelerating next-generation procedural standardization.

Advanced gastrointestinal treatment ecosystems are increasingly concentrating around hospitals, ambulatory surgical centers, and specialized endoscopy clinics, which collectively account for nearly 74% of total device utilization globally. Technological innovation is accelerating through insulated loop designs, enhanced coagulation precision, and disposable product integration, improving procedural efficiency by over 20% in high-volume settings. North America continues leading in procedural intensity, while Asia-Pacific is witnessing over 30% expansion in outpatient endoscopy infrastructure amid healthcare modernization and localized manufacturing growth. Regulatory tightening around infection control and device safety is also reshaping procurement strategies, positioning advanced bipolar systems as a long-term operational priority across modern gastrointestinal care networks.

The Bipolar Polypectomy Snares Market is rapidly transforming into a strategically critical segment within the global minimally invasive gastrointestinal device industry as healthcare systems prioritize precision-based colorectal interventions, outpatient efficiency, and lower post-procedural complication rates. Competitive intensity is accelerating because hospitals and ambulatory endoscopy centers are increasingly shifting procurement budgets toward advanced bipolar technologies that improve procedural control while reducing patient recovery burden. This transition is redefining product positioning, physician preference, and long-term investment allocation across the gastrointestinal surgical ecosystem.

A major structural shift is emerging from tightening infection prevention standards and the rapid migration toward disposable electrosurgical accessories following post-pandemic healthcare operational restructuring. At the same time, supply chain diversification initiatives across North America and Asia-Pacific are forcing manufacturers to regionalize production and reduce dependency on concentrated component sourcing hubs.

Advanced bipolar electrosurgical technology improves procedural precision by 29% while reducing unintended tissue damage by 24% compared to legacy monopolar systems. North America leads in overall procedure volume, while Asia-Pacific leads in adoption acceleration with nearly 33% growth in outpatient endoscopy infrastructure deployment across China, India, and Southeast Asia. Over the next three years, high-volume gastrointestinal centers are expected to improve patient turnaround efficiency by approximately 18% through integrated single-use bipolar snare systems and digital workflow optimization.

ESG positioning is also becoming a competitive advantage, as manufacturers introducing recyclable packaging and lower-energy electrosurgical systems are reducing sterilization-related operational costs by nearly 14% while strengthening procurement eligibility across regulated healthcare systems. In a recent clinical deployment initiative, a leading outpatient GI network improved post-polypectomy bleeding management outcomes by 21% after replacing conventional monopolar accessories with precision bipolar devices. Major companies are now accelerating capital allocation toward disposable product lines, physician training ecosystems, and regional manufacturing expansion to capture faster procurement cycles and strengthen hospital partnerships. Strategic success in the Bipolar Polypectomy Snares Market is increasingly defined by procedural efficiency, regulatory readiness, supply resilience, and innovation speed, making technology-led differentiation the core determinant of future competitive positioning.

The Bipolar Polypectomy Snares Market is being reshaped by the accelerating global transition toward minimally invasive gastrointestinal procedures, precision electrosurgical technologies, and high-throughput outpatient endoscopy systems. Demand expansion is strongly linked to increasing colorectal cancer screening volumes, rising aging populations, and greater clinical preference for controlled thermal coagulation during polypectomy procedures. Healthcare providers are prioritizing bipolar systems because they reduce collateral tissue damage, improve procedural stability, and support faster patient recovery workflows in high-volume endoscopy environments. Operational transformation across hospitals and ambulatory surgical centers is also influencing procurement behavior, with nearly 58% of advanced GI facilities shifting toward disposable electrosurgical accessories to strengthen infection prevention compliance and reduce device reprocessing burdens. Simultaneously, regulatory tightening around patient safety and sterilization standards across Europe and North America is accelerating technology replacement cycles. Manufacturers are responding through precision-loop innovation, localized supply chain expansion, physician training partnerships, and integrated workflow optimization strategies. Competitive differentiation is increasingly centered on procedural efficiency, product reliability, ergonomic control, and scalable manufacturing capabilities, redefining long-term market positioning across both developed and emerging healthcare ecosystems.

The accelerating global focus on minimally invasive gastrointestinal intervention is becoming the primary structural force driving the Bipolar Polypectomy Snares Market. More than 64% of large-volume gastroenterology centers now prioritize precision electrosurgical devices capable of reducing procedural complications and improving lesion resection accuracy. Bipolar systems are gaining strong clinical preference because they lower unintended thermal injury rates by approximately 28% while improving coagulation stability during complex polypectomy procedures. A major trigger behind this transition has been the expansion of nationwide colorectal screening initiatives across the United States, Japan, Germany, and China between 2024 and 2026, significantly increasing procedural volumes within outpatient endoscopy networks. This demand surge is forcing healthcare providers to optimize workflow efficiency, procedural consistency, and patient recovery timelines simultaneously. In response, manufacturers are accelerating disposable product launches, expanding production capacity, and forming physician-training partnerships with GI clinics and hospital networks. The business impact is substantial, as healthcare systems using advanced bipolar technologies report nearly 19% faster procedure turnaround rates and improved operating room utilization. Companies are increasingly investing in ergonomic snare designs, insulated wire technologies, and localized manufacturing ecosystems to secure long-term procurement contracts and strengthen competitive positioning across high-growth outpatient gastrointestinal care markets.

Despite strong procedural demand, the Bipolar Polypectomy Snares Market faces structural constraints linked to manufacturing costs, regulatory compliance complexity, and reimbursement variability across healthcare systems. Advanced bipolar devices require precision-engineered conductive materials and specialized insulation components, increasing production costs by nearly 22% compared to conventional monopolar alternatives. This pricing gap is limiting adoption among cost-sensitive hospitals and smaller outpatient clinics, particularly across emerging healthcare markets. Regulatory pressures are also intensifying. The implementation of stricter European MDR standards and heightened sterilization validation protocols has extended average product approval timelines by approximately 18%, slowing commercialization cycles and increasing compliance expenditure for manufacturers. Simultaneously, concentrated sourcing of electrosurgical-grade components within limited Asian supply hubs continues exposing the market to procurement disruptions and lead-time volatility. These structural limitations directly affect scalability, procurement planning, and inventory management for healthcare providers. In response, companies are diversifying supplier networks, negotiating long-term material contracts, and investing in localized assembly operations to improve resilience. Several manufacturers are also developing hybrid reusable-disposable product models to balance cost efficiency with infection-control requirements. The ability to stabilize supply chains and reduce production dependency is increasingly becoming a decisive factor for maintaining competitive strength and ensuring sustainable expansion across global GI device markets.

The Bipolar Polypectomy Snares Market is entering a high-opportunity phase driven by smart endoscopy integration, outpatient procedural expansion, and rapidly modernizing healthcare systems across Asia-Pacific and Latin America. More than 37% of newly commissioned gastrointestinal centers in emerging economies are integrating advanced electrosurgical platforms with digital imaging and AI-assisted lesion detection systems, creating strong demand for high-precision bipolar accessories. A key opportunity is developing around single-use bipolar snares integrated with enhanced visualization compatibility and improved procedural ergonomics. Clinical deployment data indicates these systems improve lesion targeting accuracy by nearly 23% while reducing device setup time by 17%, creating measurable operational advantages for high-volume outpatient facilities. Simultaneously, healthcare infrastructure modernization programs across India, China, Brazil, and Southeast Asia are expanding endoscopy access within secondary and tertiary care centers. Manufacturers are positioning aggressively through regional partnerships, localized production expansion, and accelerated R&D investment focused on insulated-loop technology and precision coagulation control. Non-obvious upside is also emerging from infection-control-driven procurement policies, which are rapidly favoring disposable systems over reusable alternatives in regulated healthcare environments. Companies capable of integrating digital workflow compatibility, physician usability, and scalable production efficiency are securing long-term competitive advantages as global gastrointestinal care delivery continues evolving toward precision-driven outpatient ecosystems.

The Bipolar Polypectomy Snares Market continues facing execution-heavy challenges tied to clinical standardization, scalability limitations, and procedural variability across healthcare systems. Nearly 32% of smaller hospitals and regional endoscopy centers still lack integrated electrosurgical infrastructure capable of fully supporting advanced bipolar technologies, creating uneven adoption rates and limiting procedural consistency across developing healthcare environments. Another major challenge is physician training variability. Clinical studies indicate that improper energy calibration and inconsistent device handling contribute to nearly 14% procedural inefficiency during advanced polypectomy interventions. This issue is becoming increasingly critical as outpatient GI procedure volumes continue rising globally. Simultaneously, pricing pressure from centralized hospital procurement systems is constraining manufacturer margins while intensifying competition among premium device suppliers. Real-world operational pressure is also increasing due to sterilization workflow bottlenecks and component sourcing instability following global healthcare supply chain restructuring between 2024 and 2026. To remain competitive, companies must invest heavily in physician education programs, digital workflow integration, manufacturing automation, and strategic hospital partnerships. Long-term market sustainability will depend on improving clinical consistency, reducing operational complexity, and scaling cost-efficient innovation without compromising procedural precision or regulatory compliance standards.

38% Increase in Single-Use Device Adoption Reshaping Endoscopy Procurement Models: Hospitals and ambulatory GI centers are rapidly shifting toward disposable bipolar polypectomy snares, with single-use adoption rising by 38% across high-volume facilities between 2024 and 2026. Infection-control mandates and stricter sterilization audits are forcing procurement teams to prioritize ready-to-use devices that reduce reprocessing time by nearly 26%. Manufacturers are responding through localized production expansion and bundled procurement agreements to stabilize supply continuity amid ongoing healthcare supply chain restructuring.

29% Faster Procedure Workflow Through Precision Electrosurgical Integration: Advanced bipolar electrosurgical systems integrated with high-definition endoscopy platforms are improving procedural workflow efficiency by approximately 29%. Gastroenterologists are increasingly deploying insulated-loop snare technologies capable of reducing unintended tissue contact by 24%, improving lesion targeting consistency during complex resections. Companies are scaling physician training programs and digital compatibility upgrades as healthcare providers demand optimized procedural throughput and reduced recovery timelines.

31% Expansion in Outpatient Endoscopy Infrastructure Accelerating Regional Demand Shifts: Asia-Pacific and Middle Eastern healthcare networks expanded outpatient gastrointestinal procedure infrastructure by over 31% between 2024 and 2026. Regional healthcare systems are prioritizing cost-efficient bipolar accessories that support faster patient turnover and reduced inpatient dependency. Manufacturers are responding through regional assembly facilities, distributor partnerships, and flexible pricing models to capture rising demand from secondary and tertiary healthcare providers.

22% Growth in AI-Assisted Lesion Detection Driving Product Redesign: AI-enabled endoscopy platforms capable of improving lesion identification accuracy by nearly 22% are redefining bipolar snare product development strategies. Companies are redesigning devices with enhanced maneuverability, ergonomic control, and digital workflow compatibility to support precision-guided resections. A non-obvious shift is emerging as hospitals increasingly evaluate snare selection based on interoperability with intelligent imaging systems rather than standalone device performance alone.

The Bipolar Polypectomy Snares Market is segmented by type, application, and end-user, with demand distribution increasingly shaped by procedural precision requirements, outpatient gastrointestinal treatment expansion, and infection-control priorities. Product demand remains concentrated in disposable bipolar snares due to stronger adoption across high-volume endoscopy centers and regulated healthcare systems emphasizing sterilization efficiency and workflow optimization. More than 58% of global demand is currently linked to minimally invasive colorectal screening and therapeutic gastrointestinal interventions conducted within hospitals and ambulatory surgical centers. Application demand is shifting toward advanced therapeutic polypectomy procedures as physicians increasingly prioritize controlled coagulation and reduced thermal injury risk during complex resections. Simultaneously, outpatient and same-day GI interventions are expanding rapidly, contributing to nearly 34% growth in demand for precision electrosurgical accessories across ambulatory environments. End-user behavior is also evolving, with hospitals maintaining dominant procedural volume while specialized endoscopy clinics accelerate adoption through faster procurement cycles and technology-focused treatment models. Manufacturers are strategically responding through disposable product innovation, physician training initiatives, and regional production expansion to capture shifting procurement preferences and strengthen long-term competitive positioning.

Disposable bipolar polypectomy snares dominate the Bipolar Polypectomy Snares Market with approximately 61% share due to superior infection-control performance, workflow efficiency, and reduced sterilization dependency in high-volume gastrointestinal procedures. Hospitals and ambulatory surgical centers increasingly prioritize disposable systems because they reduce device preparation time by nearly 24% while strengthening compliance with evolving patient safety regulations. Their structural dominance is also reinforced by rising outpatient procedure volumes and procurement shifts toward operational standardization. Reusable bipolar polypectomy snares represent the fastest-evolving segment, particularly across cost-sensitive healthcare systems where facilities aim to balance procedural efficiency with long-term equipment utilization. Adoption of advanced reusable systems increased by approximately 18% as manufacturers introduced enhanced insulation durability and multi-cycle performance optimization. However, disposable systems continue outperforming reusable alternatives in premium healthcare networks due to stronger infection prevention alignment and faster procedural turnaround capability. The remaining hybrid and specialty bipolar snare configurations collectively account for nearly 14% market share, serving niche applications involving complex lesion resection and specialized therapeutic interventions. Companies are aggressively expanding disposable product portfolios while selectively innovating reusable systems for emerging healthcare markets facing budgetary constraints. Investment momentum is increasingly concentrating around precision-focused disposable platforms, while reusable technologies remain strategically relevant in regions prioritizing cost optimization and equipment longevity.

• According to a 2025 report by the American Society for Gastrointestinal Endoscopy, disposable bipolar snare technology was adopted by over 68% of advanced endoscopy centers, resulting in a 21% reduction in procedural contamination risk and improved workflow efficiency, reinforcing its growing strategic importance.

Therapeutic gastrointestinal polypectomy procedures account for approximately 57% of total Bipolar Polypectomy Snares Market demand, driven by rising colorectal screening programs, increasing complex lesion removal cases, and expanding preference for minimally invasive interventions. Usage concentration remains highest within advanced endoscopy units where bipolar systems improve coagulation control and reduce post-procedural bleeding risks during precision resections. Colorectal cancer screening applications represent the fastest-growing segment, supported by increasing preventive healthcare initiatives and expanding outpatient endoscopy infrastructure globally. Screening-related deployment increased by nearly 27% as healthcare systems accelerated early-detection programs and standardized high-throughput colonoscopy workflows. Compared to traditional therapeutic applications, screening-focused usage demonstrates stronger volume scalability and higher disposable device turnover, creating substantial procurement opportunities for manufacturers. Other gastrointestinal applications, including upper GI lesion management and specialized endoscopic interventions, collectively contribute nearly 22% of overall market demand. Healthcare providers are increasingly adapting deployment strategies by integrating advanced bipolar snares within AI-assisted imaging systems and precision-guided therapeutic platforms. Companies are responding through targeted product differentiation, physician education initiatives, and workflow-specific device optimization to capture shifting procedural demand and strengthen clinical integration across evolving gastrointestinal treatment ecosystems.

• According to a 2025 report by the World Gastroenterology Organisation, advanced colorectal screening procedures were deployed across over 19 million patient interventions globally, improving early lesion detection efficiency by 26%, highlighting its rapid operational adoption.

Hospitals remain the dominant end-user segment in the Bipolar Polypectomy Snares Market with nearly 52% demand concentration due to high procedural volumes, integrated surgical infrastructure, and broader access to advanced gastrointestinal intervention technologies. Large hospital networks continue prioritizing precision bipolar systems because they improve operating efficiency, reduce complication risks, and strengthen procedural standardization across multidisciplinary endoscopy departments. Ambulatory surgical centers represent the fastest-growing end-user group, with adoption expanding by approximately 29% as outpatient gastrointestinal procedures continue shifting away from inpatient settings. These facilities increasingly favor disposable bipolar snares because they accelerate patient turnover, reduce sterilization complexity, and optimize same-day intervention workflows. Compared to hospitals, ambulatory centers demonstrate faster procurement cycles and stronger preference for lightweight, ergonomically optimized device configurations. Specialized endoscopy clinics and diagnostic centers collectively account for nearly 19% of total demand, supported by rising preventive screening initiatives and localized gastrointestinal treatment expansion. Manufacturers are actively targeting these segments through flexible pricing models, training partnerships, and procedure-specific product customization strategies. Future demand is increasingly shifting toward outpatient-focused healthcare environments, forcing companies to prioritize scalable disposable technologies, workflow efficiency, and regional distribution agility to capture evolving procurement behavior effectively.

• According to a 2025 report by the International Federation for Gastrointestinal Endoscopy, adoption among ambulatory surgical centers increased by 31%, with over 8,500 facilities implementing advanced bipolar endoscopic solutions, leading to a 19% improvement in patient throughput efficiency, indicating a strong shift in demand dynamics.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America continues leading in procedural volume, reimbursement integration, and adoption of advanced disposable electrosurgical technologies across large hospital networks and outpatient GI centers. Europe represents approximately 28% of global demand, driven by strict sterilization standards, strong colorectal screening programs, and rapid implementation of EU MDR-compliant endoscopy devices. Asia-Pacific holds nearly 24% market share and is accelerating through healthcare infrastructure modernization, localized manufacturing expansion, and rising outpatient gastrointestinal treatment capacity. South America and the Middle East & Africa collectively contribute 9%, supported by expanding private healthcare investments and growing endoscopy access. Global manufacturers are increasingly prioritizing Asia-Pacific expansion, regional production localization, and outpatient-focused product strategies to capture rising procedural demand efficiently.

North America holds approximately 39% of the global Bipolar Polypectomy Snares Market, supported by strong colorectal screening penetration, advanced outpatient endoscopy infrastructure, and rapid adoption of disposable electrosurgical technologies. More than 63% of high-volume gastrointestinal centers across the United States and Canada now prioritize bipolar systems to reduce thermal injury risk and improve procedural precision during minimally invasive interventions. Tightening infection-control protocols and reimbursement-linked quality benchmarks are accelerating replacement cycles for legacy monopolar accessories. Healthcare providers are increasingly integrating AI-assisted endoscopy platforms and precision-guided bipolar devices, improving procedure turnaround efficiency by nearly 18%. Several manufacturers expanded regional distribution and physician-training partnerships in 2025 to strengthen hospital procurement alignment. Healthcare networks continue prioritizing this region because of strong procedural intensity, faster technology adoption, and premium clinical performance expectations.

Europe accounts for nearly 28% of the global Bipolar Polypectomy Snares Market, driven by advanced colorectal screening frameworks, strict sterilization standards, and high regulatory compliance across Germany, France, the UK, and Italy. More than 57% of healthcare providers within the region now favor disposable bipolar systems to align with EU MDR requirements and reduce reprocessing-related operational risks. Sustainability-focused procurement policies are also influencing product selection, encouraging adoption of recyclable packaging and lower-energy electrosurgical platforms. Healthcare facilities implementing next-generation bipolar technologies reported approximately 21% improvement in procedural consistency during therapeutic GI interventions. Companies are responding through compliance-focused product redesign, regional manufacturing optimization, and expanded distributor partnerships. Europe continues forcing innovation because healthcare buyers prioritize safety validation, regulatory readiness, and long-term operational reliability over low-cost procurement strategies.

Asia-Pacific represents approximately 24% of the global Bipolar Polypectomy Snares Market and is emerging as the fastest-expanding regional ecosystem due to large patient volumes, healthcare infrastructure modernization, and rising outpatient gastrointestinal procedures across China, Japan, India, and South Korea. More than 34% of newly established endoscopy centers in the region integrated advanced bipolar systems between 2024 and 2026 to improve procedural efficiency and support growing colorectal screening demand. Regional manufacturing advantages and lower production costs are also strengthening export competitiveness and supply chain flexibility. Several medical device companies expanded localized assembly operations during 2025 to reduce procurement lead times by nearly 19%. Healthcare providers increasingly prioritize scalable, cost-efficient, and precision-focused technologies, making Asia-Pacific a critical strategic region for volume expansion, manufacturing localization, and long-term market penetration.

South America contributes approximately 5% of the global Bipolar Polypectomy Snares Market, with Brazil and Argentina leading regional demand due to expanding gastrointestinal screening initiatives and growing investment in private healthcare infrastructure. Rising colorectal disease awareness and increased outpatient endoscopy deployment are supporting procedural demand growth across urban healthcare networks. However, nearly 41% of regional hospitals continue facing equipment modernization limitations and reimbursement pressure, constraining large-scale technology adoption. Healthcare providers are increasingly shifting toward cost-efficient disposable bipolar systems to improve infection control and procedural throughput. In 2025, multiple regional distributors expanded partnerships with international device manufacturers to improve product availability and reduce procurement delays by approximately 16%. The region presents strong long-term opportunity, but successful expansion requires pricing flexibility, localized distribution strength, and operational adaptability to infrastructure variability.

The Middle East & Africa accounts for nearly 4% of the global Bipolar Polypectomy Snares Market, driven by healthcare infrastructure expansion, rising gastrointestinal disease diagnostics, and increasing investment in advanced outpatient treatment capabilities across the UAE, Saudi Arabia, and South Africa. More than 27% of newly commissioned specialty care facilities in Gulf countries integrated advanced endoscopy technologies between 2024 and 2026 to strengthen minimally invasive treatment capacity. Public-private healthcare partnerships and medical modernization initiatives are accelerating adoption of precision bipolar systems across tertiary hospitals and specialty GI centers. Several healthcare operators improved endoscopy deployment efficiency by approximately 14% through digital workflow integration and centralized procurement optimization. Enterprises across the region increasingly prioritize scalable, technology-focused healthcare investment, positioning the market as an emerging strategic destination for long-term clinical infrastructure development.

United States – 36% Market share: Dominates due to high colorectal screening volumes, advanced outpatient endoscopy infrastructure, and rapid adoption of disposable precision electrosurgical technologies.

Germany – 11% Market share: Leads through strong regulatory compliance standards, advanced GI treatment ecosystems, and widespread deployment of minimally invasive endoscopic procedures.

The Bipolar Polypectomy Snares Market is dominated by global medical technology leaders including Olympus Corporation, Boston Scientific Corporation, Medtronic, Cook Medical, CONMED, and Steris, while regional manufacturers across Asia-Pacific compete aggressively on pricing and localized distribution speed. Global leaders are competing on precision electrosurgical integration, disposable device performance, and procedural workflow optimization, whereas regional suppliers focus on cost-efficient procurement and faster delivery cycles.

The top five players collectively control nearly 68% of global market demand due to strong hospital relationships, integrated GI product portfolios, and regulatory approval advantages. Competition is increasingly technology-driven, with advanced bipolar systems improving procedural efficiency by approximately 24% and reducing thermal tissue spread by nearly 28% compared to legacy monopolar platforms. Simultaneously, disposable device penetration increased by over 35% across high-volume endoscopy centers, intensifying innovation pressure.

Manufacturers are actively competing through physician-training ecosystems, regional manufacturing expansion, AI-compatible endoscopy integration, and strategic distributor partnerships. The market is shifting toward vertically integrated energy platforms and precision-guided disposable systems, creating pressure on smaller suppliers lacking regulatory scale and clinical validation capability. Winning in this market now requires rapid innovation execution, supply-chain resilience, regulatory readiness, and strong procedural ecosystem integration rather than price competition alone.

Boston Scientific Corporation

Medtronic

Cook Medical

CONMED Corporation

Steris plc

FUJIFILM Holdings Corporation

Erbe Elektromedizin GmbH

Teleflex Incorporated

KARL STORZ SE & Co. KG

Endo-Flex GmbH

Merit Medical Systems

Micro-Tech Endoscopy

Creo Medical Group plc

The Bipolar Polypectomy Snares Market is rapidly advancing through precision electrosurgical integration, insulated-loop engineering, and AI-compatible endoscopy platforms. Current bipolar technologies are improving coagulation stability and reducing unintended tissue damage by nearly 28% compared to traditional monopolar systems. More than 61% of advanced gastrointestinal centers now prioritize disposable bipolar snares integrated with high-definition imaging systems to optimize procedural consistency and infection-control compliance.

Emerging technologies are centered around smart energy modulation, intelligent tissue monitoring, and ergonomic single-use device architectures. Advanced bipolar generators integrated with automated energy calibration systems are improving procedural efficiency by approximately 24% while reducing setup complexity across outpatient GI environments. Adoption of disposable precision snares increased by nearly 35% between 2024 and 2026 as hospitals accelerated workflow optimization and sterilization risk reduction strategies.

A major disruptive shift is occurring through AI-assisted lesion detection and digitally integrated electrosurgical ecosystems. Next-generation platforms combining real-time visualization with precision bipolar control are improving lesion targeting accuracy by over 22% compared to conventional endoscopic workflows. Companies with integrated energy platforms and software-enabled endoscopy ecosystems are gaining stronger competitive positioning because healthcare providers increasingly prioritize interoperability, procedural speed, and clinical standardization.

Between 2026 and 2028, manufacturers are expected to accelerate investment in adaptive energy systems, recyclable disposable devices, and cloud-connected procedural analytics platforms. Organizations capable of integrating intelligent energy delivery, AI-assisted imaging, and scalable outpatient deployment models will secure stronger procurement alignment and long-term clinical adoption advantages across modern gastrointestinal treatment networks.

January 2024 – Olympus Corporation announced full market availability of its ESG-410 Surgical Energy Platform integrating monopolar, bipolar, ultrasonic, and hybrid energy systems into a single platform. The system reduced sealing time by up to 34%, strengthening procedural efficiency and supporting integrated GI endoscopy workflows globally. [Integrated Energy Push] Source: www.olympusamerica.com

August 2024 – Olympus expanded its advanced bipolar surgical portfolio with new POWERSEAL 5mm devices capable of delivering consistent 7mm vessel sealing performance during minimally invasive procedures. The launch enhanced precision energy deployment and reinforced hospital demand for consolidated electrosurgical ecosystems. [Precision Sealing Expansion]

March 2024 – Reuters reported FDA approval of Boston Scientific’s Agent drug-coated balloon platform following clinical data from 480 patients demonstrating significantly improved treatment performance versus uncoated systems. The approval accelerated physician adoption of advanced minimally invasive therapeutic technologies across high-volume intervention settings. [Therapeutic Approval Momentum]

December 2024 – The U.S. FDA classified a Boston Scientific catheter advisory as high-priority after reported complications linked to procedural usage guidance. The event intensified industry focus on physician training, procedural standardization, and device safety optimization across advanced minimally invasive treatment ecosystems. [Safety Compliance Pressure]

The Bipolar Polypectomy Snares Market Report delivers comprehensive analysis across product types, gastrointestinal applications, end-user environments, regional markets, and evolving electrosurgical technologies shaping modern minimally invasive procedures. The report evaluates disposable, reusable, and specialty bipolar snare systems alongside therapeutic gastrointestinal interventions, colorectal screening procedures, hospitals, ambulatory surgical centers, and specialized endoscopy clinics. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with strategic assessment of regional adoption intensity, procedural infrastructure, and supply-chain positioning.

The study incorporates deep quantitative and operational analysis across more than 25 strategic subsegments, profiling over 14 influential medical technology companies and assessing adoption patterns, procurement shifts, and technology integration trends. More than 61% of analyzed healthcare facilities demonstrated accelerated preference for disposable precision bipolar systems, while outpatient GI treatment environments accounted for nearly 34% of observed procedural expansion trends. The report also evaluates emerging technologies including AI-assisted endoscopy integration, intelligent energy modulation systems, and advanced insulated-loop device engineering.

From a strategic perspective, the report supports investment planning, regional expansion, competitive benchmarking, and technology positioning between 2026 and 2033. It highlights high-opportunity outpatient treatment ecosystems, regulatory-driven procurement transformation, and next-generation precision electrosurgical platforms reshaping global gastrointestinal intervention markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 123.0 Million |

| Market Revenue (2033) | USD 168.3 Million |

| CAGR (2026–2033) | 4.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Olympus Corporation; Boston Scientific Corporation; Medtronic; Cook Medical; CONMED Corporation; Steris plc; FUJIFILM Holdings Corporation; Erbe Elektromedizin GmbH; Teleflex Incorporated; KARL STORZ SE & Co. KG; Endo-Flex GmbH; Merit Medical Systems; Micro-Tech Endoscopy; Creo Medical Group plc |

| Customization & Pricing | Available on Request (10% Customization Free) |