Reports

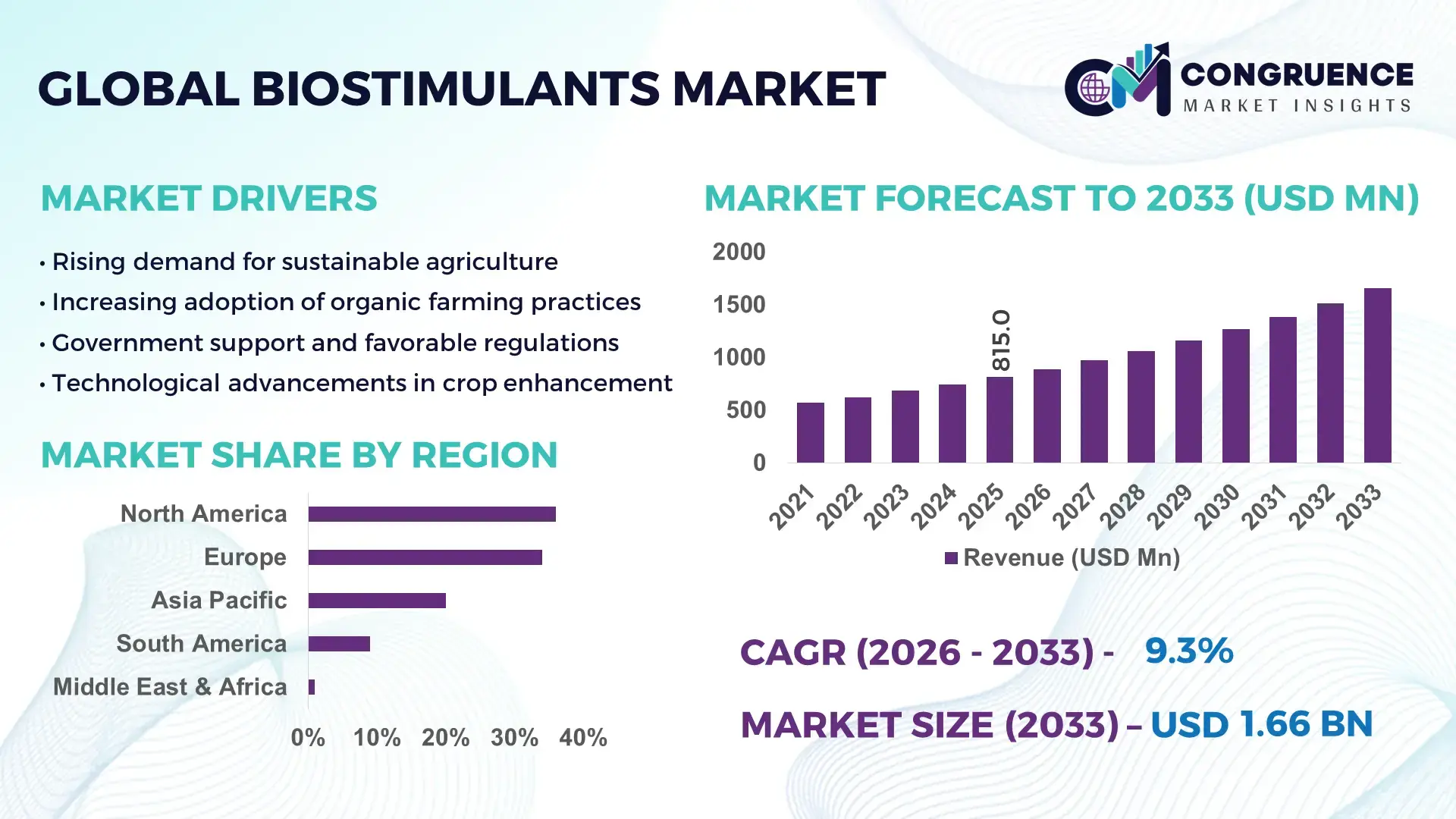

The Global Biostimulants Market was valued at USD 815.03 Million in 2025 and is anticipated to reach a value of USD 1656.46 Million by 2033 expanding at a CAGR of 9.27% between 2026 and 2033. The market is expanding steadily due to rising demand for sustainable crop productivity solutions and enhanced soil health management across commercial agriculture.

The United States leads in large-scale production and commercial deployment of advanced agricultural biostimulants, supported by over 370 registered manufacturers and formulators operating across specialty crop and row crop segments. The country records annual specialty crop production exceeding 125 million metric tons, with biostimulant adoption covering nearly 28% of high-value horticultural acreage. Investments in biological input R&D surpassed USD 1.2 billion in 2024, focusing on microbial consortia, seaweed extract formulations, and precision application technologies. Controlled-environment agriculture in states such as California and Florida integrates bio-based stimulants in more than 35% of greenhouse operations, demonstrating accelerated commercialization of eco-efficient nutrient optimization technologies.

Market Size & Growth: Valued at USD 815.03 Million in 2025 and projected to reach USD 1656.46 Million by 2033, registering a CAGR of 9.27%, driven by increasing adoption of sustainable crop enhancement solutions and regulatory support for bio-based agricultural inputs.

Top Growth Drivers: Organic farming expansion (18%), yield improvement efficiency (22%), reduction in synthetic fertilizer usage (15%).

Short-Term Forecast: By 2028, commercial farms are expected to achieve up to 12% improvement in nutrient-use efficiency and 9% reduction in input costs through precision-applied biostimulants.

Emerging Technologies: Microbial consortia engineering, seaweed-derived bioactive extraction, AI-driven precision agriculture integration.

Regional Leaders: Europe projected to reach USD 620 Million by 2033 with strong organic compliance adoption; North America expected at USD 480 Million driven by specialty crops; Asia-Pacific estimated at USD 410 Million supported by high-value horticulture expansion.

Consumer/End-User Trends: Large-scale growers and greenhouse operators increasingly integrate biostimulants into fertigation systems, with over 30% repeat purchase rates in intensive farming clusters.

Pilot or Case Example: In 2024, a commercial vineyard pilot reported 14% yield increase and 11% improved drought tolerance after microbial-based biostimulant application across 1,500 hectares.

Competitive Landscape: Leading companies hold approximately 16% combined share, including Valagro, BASF, UPL Limited, Syngenta, and Novozymes.

Regulatory & ESG Impact: Stringent EU fertilizer regulations and sustainability mandates are accelerating adoption of certified bio-based crop inputs, while carbon-reduction targets incentivize soil health technologies.

Investment & Funding Patterns: Over USD 2.4 billion invested globally since 2023 in biological crop input innovation, including venture-backed microbial startups and strategic acquisitions.

Innovation & Future Outlook: Integration with digital farming platforms, climate-resilient formulations, and multi-strain microbial products are shaping next-generation growth trajectories.

The biostimulants market demonstrates diversified demand across cereals and grains (approximately 38% of application volume), fruits and vegetables (32%), and turf and ornamentals (18%), with remaining usage in plantation crops and oilseeds. Recent advancements include bioactive peptide formulations, nano-encapsulated nutrient enhancers, and stress-mitigation microbial blends that improve crop resilience under drought and salinity conditions. Favorable environmental policies encouraging reduced chemical fertilizer dependency, combined with rising consumer preference for residue-free produce, are accelerating commercial adoption across Europe, North America, and Asia-Pacific. Strategic collaborations between agri-biotech firms and precision agriculture technology providers are expected to enhance product efficacy, traceability, and long-term soil regeneration outcomes in the coming years.

The strategic relevance of the Biostimulants Market lies in its capacity to enhance crop productivity while aligning with global sustainability mandates and food security objectives. As agricultural systems transition toward climate-resilient and low-carbon inputs, biostimulants are increasingly positioned as core components within integrated nutrient management strategies. Advanced microbial consortia technology delivers 18% improvement in nutrient-use efficiency compared to conventional synthetic fertilizer programs, while seaweed-based bioactive extracts demonstrate up to 14% higher stress tolerance under drought conditions relative to older foliar nutrient standards.

Asia-Pacific dominates in volume due to extensive cereal and horticulture cultivation, while Europe leads in adoption with over 35% of commercial farming enterprises integrating certified biological inputs into nutrient programs. By 2028, AI-enabled precision application platforms are expected to improve field-level nutrient optimization metrics by 16%, reducing input wastage and environmental runoff. Firms are committing to ESG metrics such as a 25% reduction in chemical fertilizer dependency by 2030, supported by regenerative agriculture frameworks and carbon footprint reporting mandates.

In 2024, Brazil achieved a 12% yield improvement in soybean cultivation through large-scale microbial inoculant integration supported by digital agronomy advisory systems. Strategic partnerships between agri-biotech developers and precision farming solution providers are accelerating commercialization pipelines. As regulatory clarity strengthens and climate volatility intensifies, the Biostimulants Market is emerging as a foundational pillar of agricultural resilience, compliance alignment, and sustainable long-term growth across global farming ecosystems.

The rapid expansion of sustainable agriculture practices is a primary growth driver for the Biostimulants Market. Organic farming areas have surpassed 75 million hectares globally, with double-digit annual increases in certified farmland across Europe and North America. Growers report up to 20% improved root biomass development when incorporating microbial-based biostimulants into soil programs. Additionally, 30% of large-scale greenhouse operators now integrate bio-based stimulants to enhance crop resilience against heat and salinity stress. Governments are implementing soil restoration initiatives targeting 100 million hectares of degraded land by 2030, directly increasing demand for biological soil enhancers. As food retailers strengthen residue limits and traceability standards, producers are adopting biostimulants to reduce synthetic input reliance while maintaining yield stability and crop quality benchmarks.

Regulatory fragmentation across regions presents a significant restraint for the Biostimulants Market. While Europe has implemented harmonized fertilizer product regulations, several emerging markets maintain varied classification systems, increasing approval timelines by up to 24 months. Product efficacy validation often requires multi-season field trials, raising compliance costs by 15–20% for manufacturers. Inconsistent labeling standards and lack of unified definitions for microbial strains or bioactive compounds further complicate cross-border trade. Smaller producers face elevated testing expenses and documentation requirements, limiting market entry. Additionally, limited awareness among smallholder farmers, who represent over 40% of global agricultural producers, slows adoption in developing economies. These structural inefficiencies create operational complexities and delay scalable commercialization.

Digital agriculture integration offers substantial growth opportunities for the Biostimulants Market. Precision farming tools now cover more than 25% of large commercial farms globally, enabling real-time soil health diagnostics and targeted nutrient application. AI-based crop modeling systems can optimize biostimulant dosage, resulting in up to 15% input efficiency improvement compared to blanket application methods. The expansion of climate-smart agriculture programs across Asia and Latin America supports adoption of stress-mitigation biological products in drought-prone regions. Increasing investment in controlled-environment agriculture, which has grown by over 10% annually in urban farming hubs, creates demand for high-performance bio-based formulations. Partnerships between agri-tech startups and biological input manufacturers are unlocking customized crop-specific solutions that enhance productivity under variable climatic conditions.

Rising research and formulation development costs present ongoing challenges for the Biostimulants Market. Developing stable multi-strain microbial products requires advanced fermentation infrastructure and quality control systems, increasing production costs by approximately 18% compared to conventional nutrient blends. Climate variability further complicates field performance consistency, as extreme weather events affect soil microbial activity and crop response rates. Field validation across diverse agro-climatic zones may require trials spanning three growing seasons, extending commercialization timelines. Storage and shelf-life limitations of certain biological formulations also pose logistical challenges in regions with limited cold-chain infrastructure. Addressing these operational constraints is critical to ensuring scalable adoption and maintaining performance reliability across global agricultural markets.

• 32% Increase in Microbial-Based Formulations Adoption: Microbial biostimulants, including multi-strain bacterial and fungal consortia, are witnessing accelerated integration across commercial agriculture. More than 32% of large-scale farms in North America and Europe have incorporated microbial seed treatments or soil-applied inoculants into nutrient programs. Field trials demonstrate up to 18% improvement in root biomass and 14% higher nutrient absorption efficiency compared to conventional nutrient-only approaches. Expansion of precision fermentation facilities has increased microbial production capacity by nearly 20% since 2023, enabling scalable supply to high-demand horticulture and cereal segments.

• 27% Growth in Seaweed and Botanical Extract Applications: Seaweed-derived and plant-based biostimulants are gaining traction due to their bioactive compounds that enhance stress tolerance. Approximately 27% of fruit and vegetable producers now utilize botanical extract formulations in foliar sprays to mitigate abiotic stress. Controlled trials report 12% yield enhancement under drought conditions and 15% improvement in chlorophyll content during heat stress exposure. Coastal processing hubs have expanded extraction capacity by 22%, strengthening global supply chains for algal-based crop enhancement products.

• 25% Integration Rate with Precision Agriculture Platforms: Digital agriculture convergence is transforming application efficiency in the Biostimulants Market. Around 25% of technologically advanced farms deploy AI-enabled soil sensors and satellite-guided fertigation systems to optimize biostimulant dosage. Precision mapping has reduced input overuse by nearly 16% and improved uniform crop growth across 1,000+ hectare operations. Adoption is particularly strong in Western Europe, where over 38% of commercial enterprises integrate biological inputs with digital agronomy advisory systems to enhance traceability and sustainability reporting.

• 30% Expansion in Climate-Resilient Crop Programs: Climate variability has driven a 30% rise in biostimulant usage within drought-prone and salinity-affected regions. In Latin America and parts of Asia-Pacific, more than 40 million hectares of farmland are exposed to water stress, prompting farmers to adopt stress-mitigation formulations. Application of osmoprotectant-enhanced biostimulants has demonstrated 13% improvement in water-use efficiency and 10% reduction in crop loss during extreme heat events. Agribusiness firms are scaling production facilities by 18% to meet increasing demand for climate-resilient biological crop solutions.

The Biostimulants Market demonstrates structured segmentation across product types, crop applications, and diversified end-user groups, reflecting varied agronomic requirements and adoption maturity. Product segmentation is primarily categorized into microbial, seaweed extract, humic substance, amino acid, and other bioactive formulations. Microbial and seaweed-based products together account for over 55% of total usage volume due to proven performance in nutrient uptake and stress mitigation. Application-wise, cereals and grains represent the largest segment, supported by large cultivation areas exceeding 700 million hectares globally, while fruits and vegetables exhibit strong penetration due to quality-focused farming. From an end-user standpoint, large commercial farms dominate adoption patterns, though greenhouse operators and contract farming enterprises are expanding usage. Segmentation patterns reveal increasing integration with precision agriculture systems, reflecting a transition from traditional input supplementation to data-driven biological crop enhancement strategies.

Product types in the Biostimulants Market include microbial biostimulants, seaweed extracts, humic substances, amino acids, and other botanical or synthetic bioactive compounds. Microbial biostimulants currently account for approximately 38% of total adoption, driven by their proven ability to enhance root development and improve nutrient-use efficiency by up to 18% under field conditions. Seaweed extracts hold nearly 24% share, particularly in high-value horticulture due to their 12–15% improvement in crop stress tolerance. However, amino acid-based formulations are rising fastest, projected to grow at a CAGR of 11.6%, supported by expanding foliar nutrition programs and rapid plant absorption characteristics.

Humic substances and other specialty bioactive blends collectively represent around 38% of the remaining segment, serving niche soil-conditioning and specialty crop applications.

Application segmentation includes cereals and grains, fruits and vegetables, turf and ornamentals, oilseeds and pulses, and plantation crops. Cereals and grains currently account for nearly 41% of total application volume, reflecting extensive cultivation areas and increasing integration of biological soil enhancers to improve nutrient efficiency across staple crops. Fruits and vegetables hold around 29% share, supported by quality-driven farming practices and export compliance standards requiring reduced chemical residues. However, turf and ornamentals represent the fastest-growing segment, expanding at a CAGR of 10.8% due to rising investments in sports infrastructure and landscaping projects requiring enhanced root vigor and aesthetic quality.

Oilseeds, pulses, and plantation crops collectively contribute approximately 30% of the application landscape, particularly in regions with high soybean, palm, and cotton cultivation.

End-user segmentation includes large commercial farms, greenhouse operators, contract farming enterprises, and smallholder farmers. Large commercial farms currently represent approximately 46% of total adoption due to scalable application systems and structured nutrient management programs. Greenhouse operators account for nearly 22% of the market, leveraging controlled-environment agriculture to achieve up to 16% yield optimization through targeted biostimulant integration. However, contract farming enterprises are emerging as the fastest-growing end-user segment, expanding at a CAGR of 12.3%, driven by vertically integrated supply chains and export-oriented crop production models.

Smallholder farmers and cooperative farming groups collectively contribute around 32% of the remaining adoption, particularly in Asia-Pacific and Latin America where government-backed soil restoration initiatives are expanding outreach.

Europe accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2026 and 2033.

Europe’s leadership is supported by over 16 million hectares of certified organic farmland and widespread integration of sustainable nutrient management frameworks across more than 35% of commercial farms. North America holds approximately 28% of the Biostimulants Market, driven by adoption across 125+ million metric tons of annual specialty crop output. Asia-Pacific represents nearly 24% share, supported by large-scale cereal cultivation exceeding 300 million hectares and rising horticulture exports. South America contributes around 9%, reflecting strong soybean and sugarcane cultivation across Brazil and Argentina. The Middle East & Africa collectively account for nearly 5%, with adoption increasing in water-stressed agricultural zones. Regional consumption patterns highlight stronger greenhouse and high-value crop penetration in developed markets, while emerging economies emphasize soil restoration and yield stabilization programs across staple crops.

How Are Advanced Agronomic Practices Accelerating Sustainable Crop Enhancement?

North America represents approximately 28% of the global Biostimulants Market, supported by large-scale commercial farming and advanced agronomic infrastructure. The United States accounts for nearly 70% of regional demand, driven by specialty crops, corn, and soybean cultivation. More than 30% of greenhouse vegetable operations integrate microbial and seaweed-based formulations into fertigation systems. Regulatory developments promoting soil health and carbon sequestration practices have expanded adoption across 20+ state-supported conservation programs. Precision agriculture tools now cover nearly 40% of large farms, enabling up to 15% improvement in nutrient-use optimization. Local players such as UPL Limited’s North American operations are expanding biological product portfolios and investing in fermentation facilities to enhance microbial supply capacity. Regional consumer behavior indicates higher enterprise-level adoption among large agribusinesses, with structured nutrient management planning and data-driven performance tracking becoming standard practice.

Why Is Regulatory Alignment Strengthening Bio-Based Agricultural Inputs?

Europe commands around 34% of the global Biostimulants Market, supported by strong organic farming penetration and harmonized fertilizer regulations. Germany, France, Italy, and Spain collectively contribute over 65% of regional demand due to high-value horticulture and cereal cultivation. More than 35% of certified organic farms incorporate biological crop enhancers into nutrient programs. The European Union’s sustainable agriculture initiatives target a 25% reduction in chemical fertilizer use by 2030, accelerating demand for validated biostimulant formulations. Technological adoption includes digital traceability platforms integrated across 38% of commercial farming enterprises to ensure compliance and sustainability reporting. Companies such as Valagro are advancing plant-based biostimulant innovation, expanding controlled-environment trial programs across Mediterranean horticulture zones. Regional buyer behavior is heavily influenced by regulatory pressure, resulting in demand for scientifically validated, compliant, and environmentally transparent biostimulant solutions.

What Factors Are Driving Rapid Agricultural Modernization and Biological Input Expansion?

Asia-Pacific accounts for approximately 24% of the global Biostimulants Market, ranking third in share but first in projected expansion momentum. China and India collectively represent over 60% of regional consumption due to extensive cereal, rice, and horticulture cultivation exceeding 300 million hectares combined. Japan contributes through high-tech greenhouse production and specialty crop exports. Manufacturing capacity in China has increased by nearly 18% since 2023 to meet growing domestic and export demand for microbial formulations. Innovation hubs in India and China are developing biofertilizer and microbial consortia technologies integrated with mobile-based farm advisory systems used by more than 20 million farmers. Regional consumer behavior reflects rapid digital adoption, with smallholder farmers increasingly relying on mobile agronomy apps for input recommendations and soil health monitoring, accelerating biological input integration across diverse crop systems.

How Is Large-Scale Commercial Farming Enhancing Soil Productivity Strategies?

South America represents close to 9% of the global Biostimulants Market, driven primarily by Brazil and Argentina. Brazil alone cultivates over 40 million hectares of soybean farmland, creating significant demand for microbial seed treatments and soil conditioners. Regional agricultural exports account for more than 45% of total crop output, reinforcing the need for yield optimization technologies. Government-backed soil recovery initiatives support adoption across degraded pastureland covering nearly 20 million hectares. Local producers are expanding fermentation capacity by approximately 15% to serve large-scale soybean and sugarcane operations. Consumer behavior in the region is strongly tied to export-oriented agribusiness, with large cooperatives adopting biological inputs to enhance productivity and maintain compliance with international residue standards.

How Are Water Scarcity and Agricultural Modernization Influencing Bio-Input Adoption?

The Middle East & Africa region accounts for nearly 5% of the Biostimulants Market, with rising adoption across water-scarce agricultural zones. The United Arab Emirates and Saudi Arabia are investing in controlled-environment agriculture projects, expanding greenhouse acreage by over 12% annually. South Africa leads sub-Saharan adoption, integrating biostimulants into fruit export programs covering more than 2 million hectares. Technological modernization includes hydroponic systems and precision irrigation technologies that improve water-use efficiency by up to 14% when combined with bioactive formulations. Regional regulations promoting food security and reduced import dependency are supporting biological crop enhancement programs. Consumer behavior emphasizes resource efficiency, with growers prioritizing stress-tolerance solutions to mitigate salinity and drought-related productivity risks.

United States – 22% market share: The Biostimulants Market in the United States leads due to high specialty crop production exceeding 125 million metric tons annually and strong integration of precision agriculture technologies across large commercial farms.

Germany – 11% market share: The Biostimulants Market in Germany is driven by extensive organic farmland coverage and strict fertilizer reduction policies encouraging adoption of certified biological crop enhancement products.

The Biostimulants Market is moderately fragmented, with more than 450 active manufacturers and formulators operating across microbial, botanical, and humic-based product segments. The top five companies collectively account for approximately 28% of total global share, indicating competitive intensity alongside strong regional specialization. Market leaders focus on vertically integrated production models, investing up to 15–20% of annual operating budgets into research, strain optimization, and field validation trials.

Strategic initiatives are accelerating consolidation, with over 25 mergers, acquisitions, and strategic alliances recorded globally since 2022 to strengthen microbial fermentation capacity and expand geographic reach. Product innovation cycles average 18–24 months, with more than 60 new formulations introduced in 2024 alone targeting climate-resilient crops and precision fertigation systems. Digital agronomy partnerships now support nearly 30% of commercial-scale deployments, enhancing traceability and performance analytics. Competitive positioning increasingly centers on validated efficacy data, ESG-aligned solutions, and integrated nutrient management portfolios rather than standalone biological products. Companies are also expanding production infrastructure by 12–18% annually to meet rising demand from specialty crops and high-value horticulture sectors.

Valagro

BASF

UPL Limited

Syngenta

Novozymes

Corteva Agriscience

Biolchim

Isagro

FMC Corporation

Haifa Group

Technological advancement in the Biostimulants Market is centered on microbial strain engineering, precision fermentation, advanced extraction processes, and digital integration with precision agriculture platforms. Microbial-based technologies now represent nearly 38% of total product adoption, with multi-strain consortia formulations improving nutrient-use efficiency by up to 18% and root biomass development by 20% under controlled trials. Advances in fermentation infrastructure have increased microbial production yields by approximately 22% since 2023, enabling scalable manufacturing of bacteria and fungi strains tailored for cereals, fruits, and oilseeds.

Seaweed extraction technology has evolved through cold-press and enzymatic hydrolysis methods, preserving up to 30% more bioactive compounds compared to traditional thermal processing. These refined extraction techniques enhance plant stress tolerance by 12–15% under drought and salinity conditions. Additionally, nano-encapsulation of amino acids and humic substances is emerging as a delivery optimization technology, improving nutrient absorption rates by nearly 14% while extending product shelf life by 10–12%.

Digital agriculture integration is reshaping application efficiency. Approximately 25% of technologically advanced farms now deploy AI-enabled soil sensors and satellite-based crop monitoring systems to determine optimal biostimulant dosage. Variable-rate application technologies have reduced input wastage by 16% and improved uniform crop growth metrics across farms exceeding 1,000 hectares.

Controlled-environment agriculture further accelerates technological demand, with over 35% of modern greenhouse facilities incorporating automated fertigation systems synchronized with biological input schedules. Blockchain-enabled traceability tools are being piloted in export-oriented farming clusters, ensuring compliance with sustainability standards and enabling real-time monitoring of soil health parameters. Collectively, these innovations position the Biostimulants Market at the intersection of biotechnology, digital agriculture, and climate-resilient farming systems, enhancing measurable productivity outcomes and operational efficiency for commercial growers worldwide.

• In March 2025, Syngenta Biologicals expanded its global footprint by opening a new biologicals production facility in Orangeburg, South Carolina, increasing microbial and natural-based product manufacturing capacity by over 20% to support growing North American demand for sustainable crop solutions. Source: www.syngenta.com

• In September 2024, Novozymes and Chr. Hansen completed their merger to form Novonesis, strengthening their combined biological solutions portfolio, including agricultural biostimulants and microbial technologies, serving more than 30 industry sectors with expanded R&D capabilities and integrated bioscience innovation platforms. Source: www.novonesis.com

• In May 2024, UPL Ltd launched a new range of natural plant biostimulants under its NPP (Natural Plant Protection) portfolio, targeting improved abiotic stress tolerance and nutrient efficiency across cereals and horticulture crops in over 20 countries. Source: www.upl-ltd.com

• In February 2024, BASF expanded its biological crop solutions portfolio with new inoculant technologies designed to enhance nitrogen fixation efficiency in soybean and corn production systems, supporting sustainable farming practices across key agricultural markets in the Americas and Europe. Source: www.basf.com

The Biostimulants Market Report provides a comprehensive evaluation of product types, application segments, end-user categories, and regional performance across developed and emerging agricultural economies. The report analyzes microbial-based formulations, seaweed extracts, humic substances, amino acid products, and specialty bioactive compounds, which collectively account for more than 90% of commercialized biological crop enhancement solutions. Application coverage spans cereals and grains cultivated across over 700 million hectares globally, fruits and vegetables representing nearly 30% of high-value crop demand, turf and ornamentals, oilseeds and pulses, and plantation crops such as sugarcane and coffee. The study assesses adoption across large commercial farms, greenhouse operators covering more than 500,000 hectares worldwide, contract farming enterprises, and smallholder cooperatives representing over 40% of global agricultural producers.

Geographically, the report evaluates performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating quantitative indicators such as cultivated acreage, organic farmland coverage exceeding 75 million hectares, and regional technology penetration rates surpassing 35% in digitally enabled farms. The scope further includes technological advancements such as precision fermentation, nano-encapsulation, AI-enabled nutrient management systems, and blockchain-based traceability tools. It also addresses regulatory frameworks, sustainability targets including fertilizer reduction programs aiming at 20–25% optimization, and ESG-aligned agricultural transformation strategies. Emerging niches such as controlled-environment agriculture, hydroponics, and climate-resilient cropping systems are incorporated to present a forward-looking, multidimensional view tailored for investors, agribusiness leaders, and strategic planners.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

9.27% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Valagro , BASF , UPL Limited , Syngenta, Novozymes, Corteva Agriscience, Biolchim, Isagro, FMC Corporation, Haifa Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |