Reports

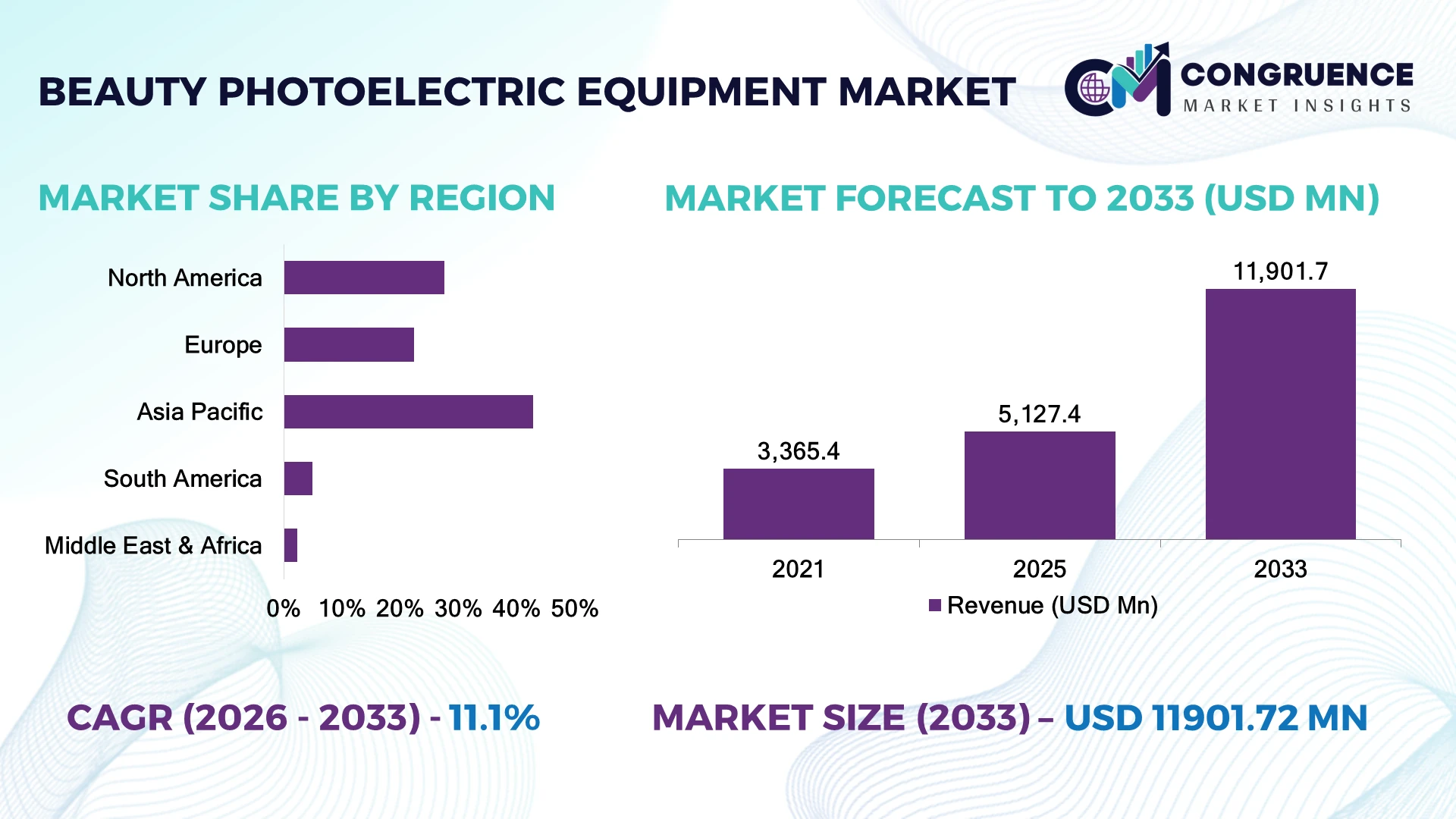

The Global Beauty Photoelectric Equipment Market was valued at USD 5,127.4 Million in 2025 and is anticipated to reach a value of USD 11,901.7 Million by 2033 expanding at a CAGR of 11.1% between 2026 and 2033. Rising adoption of AI-assisted skin diagnostics, multi-wavelength laser platforms, and non-invasive aesthetic procedures is accelerating equipment replacement across dermatology clinics, medical spas, and cosmetic hospitals.

China remains the dominant country, accounting for approximately 34% of global manufacturing capacity, supported by large-scale medical device production, expanding aesthetic clinic networks, and sustained investments in intelligent healthcare equipment. More than 68% of newly launched premium systems integrate AI-enabled treatment planning, while Japan maintains stronger penetration in high-end precision devices despite lower production volumes. The continued diversification of supply chains across Asia following post-pandemic manufacturing realignment has strengthened regional competitiveness.

Manufacturers prioritizing AI-enabled platforms, localized production, and regulatory-ready product portfolios are positioned to secure long-term competitive advantage.

Market Size & Growth: USD 5,127.4 Million in 2025 is projected to reach USD 11,901.7 Million by 2033, expanding at a CAGR of 11.1%, driven by advanced non-invasive aesthetic technologies.

Top Growth Drivers: AI-assisted diagnostics (+29%), multi-functional laser adoption (+24%), and medical aesthetics expansion (+21%) accelerate equipment deployment.

Short-Term Forecast: By 2028, treatment efficiency improves nearly 18%, while average maintenance costs decline around 12% through predictive servicing.

Emerging Technologies: AI imaging, picosecond laser systems, automated energy calibration, and cloud-connected platforms improve treatment precision and workflow efficiency.

Regional Leaders: Asia-Pacific is projected to exceed USD 4.8 Billion, North America approaches USD 3.6 Billion, and Europe surpasses USD 2.5 Billion, supported by expanding premium clinic networks and regional manufacturing shifts.

Consumer/End-User Trends: More than 62% of premium aesthetic clinics prioritize multifunctional photoelectric platforms over single-purpose devices.

Pilot/Case Example: In 2026, integrated AI-based treatment planning reduced consultation time by approximately 25% while improving treatment consistency across multi-clinic operations.

Competitive Landscape: Leading manufacturers collectively control nearly 48% of the global market, with Candela, Cynosure, Lumenis, Alma Lasers, and Lutronic competing through innovation and platform integration.

Regulatory & ESG Impact: Energy-efficient platforms reduce electricity consumption by nearly 15%, supporting evolving medical device sustainability requirements and operational efficiency.

Investment & Funding: More than USD 1.2 Billion supports manufacturing expansion, strategic partnerships, and next-generation aesthetic device development amid regional supply-chain diversification.

Innovation & Future Outlook: Smart connected systems, cloud-based treatment analytics, and AI-guided personalization strengthen competitive differentiation and premium equipment adoption.

Beauty Photoelectric Equipment demand continues expanding across dermatology clinics, medical spas, and cosmetic surgery centers as providers prioritize multifunctional platforms delivering faster treatment cycles and higher patient throughput. AI-assisted skin analysis and intelligent energy calibration are becoming standard features, with integrated systems improving procedural accuracy by nearly 22%. Regional manufacturing diversification and stricter medical device compliance frameworks are accelerating product upgrades, reinforcing the market's strategic evolution before the broader strategic discussion.

The Beauty Photoelectric Equipment Market has become strategically important as healthcare providers compete through advanced aesthetic services, shorter treatment cycles, and premium patient experiences. Digital treatment planning, AI-enabled diagnostics, and supply-chain restructuring are reshaping purchasing priorities, while manufacturers increasingly establish regional assembly and service capabilities to reduce delivery lead times and strengthen operational resilience. These changes are accelerating equipment standardization across dermatology clinics and medical aesthetics networks.

Modern AI-assisted photoelectric platforms complete skin analysis and parameter selection approximately 30% faster than conventional standalone systems while reducing operator-dependent variability and improving treatment consistency. Asia-Pacific leads high-volume manufacturing and rapid clinic deployment, whereas North America remains ahead in premium technology integration and software-enabled treatment workflows. Over the next two to three years, connected device adoption across advanced aesthetic facilities is expected to exceed 55%, supported by digital workflow integration and predictive maintenance capabilities.

A multi-location aesthetic clinic deploying integrated laser and IPL systems can improve patient throughput while simplifying maintenance through centralized equipment monitoring. Manufacturers are expanding strategic partnerships with distributors, software developers, and clinical training providers to strengthen market presence. Companies combining intelligent automation, regulatory-ready product development, and scalable service infrastructure will secure stronger competitive positioning, operational efficiency, and long-term market relevance.

AI-enabled treatment planning and multifunctional photoelectric systems are transforming clinical workflows by improving treatment precision and increasing equipment utilization. More than 64% of newly installed premium aesthetic devices now combine laser, IPL, and RF technologies on a single platform, while AI-assisted skin analysis reduces treatment planning time by nearly 30%. China continues expanding domestic medical device manufacturing under healthcare modernization initiatives, strengthening component availability and shortening production cycles. This operational shift enables clinics to standardize procedures and increase patient throughput. Manufacturers are responding through integrated software development, localized production, strategic distributor partnerships, and expanded clinical training programs, creating stronger product ecosystems while improving recurring service revenues and long-term customer retention.

High capital expenditure and evolving medical device compliance requirements continue limiting deployment among independent aesthetic clinics. Advanced photoelectric systems typically represent 35–45% higher acquisition costs than conventional standalone devices, while regulatory validation and certification activities extend commercialization timelines by nearly 20%. Japan and several European markets require increasingly stringent clinical documentation for advanced energy-based devices, increasing development costs for manufacturers. These structural pressures reduce purchasing flexibility and delay replacement cycles for smaller healthcare providers. Companies are mitigating risks by localizing component sourcing, introducing modular equipment configurations, expanding leasing programs, and securing long-term supply agreements to stabilize production costs while improving commercial accessibility across mid-sized clinics.

Cloud-connected treatment platforms, predictive maintenance, and AI-driven clinical analytics are creating new value beyond equipment sales. More than 58% of premium clinics are prioritizing digitally connected systems capable of centralized treatment monitoring, while predictive maintenance lowers unexpected equipment downtime by approximately 18%. South Korea is accelerating digital healthcare initiatives that encourage interoperability between aesthetic devices and electronic patient management systems. Manufacturers are expanding software partnerships, investing in remote diagnostics, and developing subscription-based digital service platforms that strengthen customer retention. A significant emerging opportunity lies in converting equipment data into personalized treatment optimization, enabling providers to improve operational efficiency while generating recurring digital service income alongside hardware sales.

The rapid evolution of photoelectric technologies is increasing implementation complexity across aesthetic practices. Approximately 42% of clinics report extended staff training requirements before deploying advanced AI-assisted treatment platforms, while integration with existing digital practice management systems increases installation timelines by nearly 22%. The United States continues experiencing shortages of experienced laser treatment professionals capable of operating multifunctional energy-based devices safely and efficiently. These operational challenges directly influence treatment consistency, equipment utilization, and long-term return on investment. Manufacturers must strengthen certified training programs, expand technical support networks, improve software interoperability, and invest in intuitive user interfaces to accelerate deployment while maintaining clinical performance and regulatory compliance.

AI-Driven Clinical Workflow Automation

AI-enabled treatment planning is becoming standard across premium aesthetic clinics, with automated skin assessment improving consultation efficiency by nearly 28% and reducing parameter selection errors by approximately 20%. Digital workflow integration shortens patient turnaround times while increasing equipment utilization. In response to growing software adoption and workforce shortages, manufacturers are expanding AI capabilities through software updates, cloud connectivity, and strategic collaborations with clinical technology providers to improve operational productivity.

Multifunction Platforms Replace Standalone Devices

Clinics are increasingly replacing single-function laser equipment with integrated laser, IPL, and RF platforms capable of performing multiple procedures. Nearly 60% of new equipment purchases now favor multifunction systems, reducing floor-space requirements by around 25% and lowering maintenance complexity. Equipment suppliers are redesigning product portfolios around modular platforms, enabling clinics to expand treatment offerings without significant infrastructure expansion or additional operator requirements.

Localized Manufacturing Gains Momentum

Medical device manufacturers are accelerating localized assembly and component sourcing to reduce logistics risks and improve delivery reliability. Average lead times have declined by approximately 18% following expanded manufacturing investments in China and South Korea, while localized procurement has lowered selected component dependency by nearly 15%. Companies are strengthening regional supplier ecosystems and restructuring procurement strategies to improve resilience against geopolitical trade disruptions and transportation bottlenecks.

Connected Service Models Expand Rapidly

Remote diagnostics, predictive maintenance, and software-enabled lifecycle management are becoming core differentiators in equipment purchasing decisions. Connected monitoring reduces unexpected service interruptions by nearly 16% while increasing equipment availability above 95% in high-volume aesthetic centers. Manufacturers are responding through subscription-based service packages, digital maintenance platforms, and long-term technology partnerships, creating recurring service revenue while strengthening customer retention beyond traditional hardware sales.

Laser Systems accounted for approximately 46% of the Beauty Photoelectric Equipment Market in 2025, maintaining leadership through superior treatment precision, broad clinical applicability, and seamless integration into advanced aesthetic platforms. Their ability to perform hair removal, skin resurfacing, pigmentation correction, and vascular treatments using configurable wavelengths makes them the preferred solution for high-volume clinics. Intense Pulsed Light (IPL) systems continue serving cost-sensitive facilities because of lower acquisition costs and versatile treatment coverage, while Ultrasound devices retain steady demand for non-invasive skin tightening procedures. Manufacturers continue improving laser cooling technologies, intelligent energy delivery, and AI-assisted treatment planning to strengthen clinical outcomes and equipment utilization.

Radiofrequency (RF) systems represent the fastest-growing equipment category as demand accelerates for collagen remodeling and minimally invasive facial rejuvenation procedures. Nearly 58% of newly introduced premium aesthetic platforms combine laser and RF technologies, reflecting increasing preference for multifunctional systems. Plasma devices and Photodynamic Therapy (PDT) equipment are gaining traction within specialized dermatology practices focused on scar revision and precision skin treatments. Companies are prioritizing integrated product portfolios, strategic technology partnerships, and modular platform development to strengthen competitive differentiation while supporting multi-procedure clinical environments.

According to the American Society for Dermatologic Surgery's 2025 procedural update, laser- and energy-based dermatologic treatments remained among the most frequently performed minimally invasive procedures, reinforcing continued clinical investment in advanced photoelectric equipment.

Hair Removal represented approximately 38% of total application demand in 2025, supported by consistent patient volumes, standardized treatment protocols, and recurring treatment schedules. Advanced diode laser and IPL technologies have improved treatment efficiency by nearly 20%, allowing clinics to increase daily patient throughput while maintaining treatment quality. Skin Rejuvenation remains another established application as providers increasingly combine laser, RF, and light-based therapies for anti-aging procedures. Acne Treatment, Pigmented Lesion Removal, Vascular Lesion Therapy, and Tattoo Removal continue expanding through improved device versatility and broader treatment customization.

Skin Rejuvenation is the fastest-growing application due to rising demand for minimally invasive aesthetic procedures and personalized treatment protocols. More than 61% of premium aesthetic providers now offer combination therapy packages utilizing multiple photoelectric technologies from a single platform. Tattoo Removal is also expanding as picosecond laser technology improves pigment clearance while reducing treatment sessions. Manufacturers are strengthening software integration, clinical education programs, and application-specific treatment protocols to maximize equipment utilization while supporting diversified procedural offerings across dermatology clinics and medical spas.

Industry findings released by the International Society of Aesthetic Plastic Surgery during 2026 highlighted continued expansion in minimally invasive aesthetic procedures, with energy-based skin treatments remaining among the fastest-growing procedural categories worldwide.

Dermatology Clinics accounted for approximately 44% of total equipment demand in 2025 due to specialized clinical infrastructure, experienced medical professionals, and consistently high utilization of advanced laser-based procedures. Their broad treatment portfolios and higher patient volumes justify investment in premium multifunctional photoelectric systems. Hospitals continue deploying advanced equipment for medically supervised dermatological care and reconstructive procedures, while Cosmetic Surgery Centers increasingly integrate photoelectric technologies into comprehensive aesthetic treatment programs. Manufacturers support these buyers through premium service contracts, customized software, and structured clinical training to strengthen long-term equipment utilization.

Medical Spas represent the fastest-growing end-user segment as consumers increasingly prefer minimally invasive cosmetic procedures delivered in outpatient environments. Nearly 57% of newly established premium medical spas prioritize multifunctional platforms capable of supporting multiple treatment applications while minimizing equipment footprint and operating costs. Beauty Centers continue adopting entry-level IPL and RF systems for selected cosmetic services, particularly across rapidly urbanizing markets. Companies are expanding flexible financing programs, localized distribution partnerships, tiered product portfolios, and subscription-based maintenance services to improve market penetration while strengthening long-term customer retention.

According to practice trend findings released by the American Med Spa Association during 2025, medical spas continued expanding investments in energy-based aesthetic technologies, with laser and light-based procedures remaining among the highest-utilized treatment categories across participating facilities.

Asia-Pacific accounted for the largest market share at 42.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 12.5% between 2026 and 2033.

Strong technology integration and premium clinic expansion reinforce market leadership

North America accounted for approximately 27.6% of the global Beauty Photoelectric Equipment Market in 2025, supported by widespread deployment of advanced laser platforms, AI-assisted diagnostic systems, and well-established dermatology clinic networks. The region maintains one of the highest concentrations of premium aesthetic practices, enabling faster adoption of multifunctional photoelectric equipment. More than 65% of newly installed premium systems incorporate AI-enabled treatment optimization and cloud-based software integration. Manufacturers continue expanding clinical education programs, strategic distribution partnerships, and after-sales service capabilities to improve equipment utilization and customer retention. Growing investments in digital healthcare infrastructure and predictive maintenance technologies further strengthen operational efficiency while supporting higher treatment throughput across medical aesthetics facilities.

United States Market Outlook: The United States leads the regional market through its advanced dermatology infrastructure, strong presence of global aesthetic device manufacturers, and rapid adoption of AI-enabled treatment technologies. More than 70% of premium dermatology practices have incorporated multifunctional laser platforms into their service portfolios, while continuous investment in physician training and digital workflow integration supports higher clinical productivity. Companies continue expanding domestic R&D activities, software development, and strategic partnerships to strengthen technological leadership and accelerate commercialization of next-generation photoelectric equipment.

Regulatory compliance and premium innovation strengthen equipment modernization

Europe represented approximately 22.4% of the global market in 2025, driven by high regulatory standards, established medical aesthetics infrastructure, and increasing replacement of legacy energy-based devices. Clinics across Germany, France, and Italy continue prioritizing multifunctional systems capable of supporting diverse aesthetic procedures while improving operational efficiency. Nearly 48% of newly procured premium equipment integrates intelligent treatment software and automated parameter optimization. Manufacturers are investing in localized technical support, product certification, and digital service capabilities to strengthen customer confidence while maintaining compliance with evolving medical device regulations.

Germany Market Outlook: Germany remains the largest market in Europe due to its strong medical device manufacturing base, advanced healthcare infrastructure, and extensive adoption of clinically validated aesthetic technologies. More than 55% of premium aesthetic centers continue replacing standalone systems with integrated laser and RF platforms. Domestic manufacturers and international suppliers are strengthening collaborative research, clinician training, and technology validation programs to enhance long-term equipment performance and regulatory readiness.

Manufacturing scale and expanding clinic networks accelerate global competitiveness

Asia-Pacific led the global Beauty Photoelectric Equipment Market with a 42.8% share in 2025, supported by extensive manufacturing capacity, expanding medical aesthetics infrastructure, and competitive production economics. China, South Korea, and Japan continue strengthening regional leadership through investments in intelligent medical device manufacturing and advanced aesthetic technologies. Nearly 34% of global production capacity is concentrated in China, while localized manufacturing has reduced average equipment delivery timelines by approximately 18%. Companies continue expanding regional assembly facilities, supplier ecosystems, and software integration capabilities to improve production flexibility and international competitiveness.

China Market Outlook: China represents the largest country-level market owing to its extensive manufacturing ecosystem, rapidly expanding dermatology clinic network, and strong domestic medical device industry. More than 68% of newly launched premium photoelectric platforms integrate AI-assisted treatment planning and intelligent energy management. Local manufacturers continue investing in export-oriented production, product innovation, and strategic international partnerships while strengthening quality certification to improve competitiveness across global aesthetic equipment markets.

Private aesthetic care expansion drives equipment modernization

South America accounted for approximately 4.9% of the global market in 2025, supported by expanding private aesthetic healthcare services and increasing consumer preference for minimally invasive cosmetic procedures. Premium dermatology clinics continue upgrading to multifunctional laser and RF systems to improve treatment efficiency and expand procedural offerings. Nearly 32% of recent equipment investments have focused on replacing older standalone technologies with integrated treatment platforms. Despite infrastructure and import dependency challenges, manufacturers continue strengthening distributor partnerships, clinical education initiatives, and localized service networks to improve deployment efficiency and customer support.

Brazil Market Outlook: Brazil dominates the regional market through its large cosmetic procedure volume, well-developed aesthetic medicine sector, and strong network of specialized dermatology clinics. High acceptance of non-invasive cosmetic treatments continues supporting demand for advanced photoelectric equipment. International manufacturers are expanding authorized distribution channels, clinician certification programs, and technical service infrastructure, enabling broader adoption of intelligent laser and energy-based treatment platforms across major metropolitan healthcare centers.

Healthcare modernization and premium investments accelerate technology adoption

The Middle East & Africa region is strengthening its market position through healthcare infrastructure modernization, premium private hospital expansion, and increasing investments in medical aesthetics. The region accounted for approximately 2.3% of global demand in 2025, with deployment concentrated in high-income healthcare markets. More than 40% of newly established premium aesthetic facilities are investing directly in integrated photoelectric treatment platforms rather than standalone devices. Equipment suppliers are strengthening regional partnerships, expanding technical service capabilities, and improving clinical training programs to support sustainable technology adoption while enhancing operational performance.

Saudi Arabia Market Outlook: Saudi Arabia leads regional development through large-scale healthcare transformation initiatives, expanding private specialty clinics, and growing investment in advanced medical technologies. Premium aesthetic centers continue integrating AI-enabled laser platforms to improve treatment precision and patient experience. National healthcare modernization programs and increasing private sector participation are encouraging manufacturers to strengthen local distribution partnerships, technical support infrastructure, and clinician training, positioning the country as the primary regional hub for advanced beauty photoelectric equipment deployment.

Global technology leaders including Candela, Cynosure Lutronic, Alma Lasers, Lumenis, and Cutera compete directly on premium multifunctional platforms, while regional manufacturers in China and South Korea challenge established brands through competitive pricing and localized production. The top five companies collectively account for approximately 48% of the global market, creating a moderately consolidated competitive structure. Competition centers on AI-enabled treatment planning, platform versatility, software integration, and clinical validation rather than hardware alone. Premium manufacturers deliver treatment efficiency improvements of nearly 25%, whereas localized manufacturing reduces delivery lead times by approximately 18% and production costs by 12–15%. Companies are strengthening market positions through product launches, strategic distributor partnerships, physician training, digital service platforms, and vertical integration across software and after-sales support. The competitive landscape is shifting toward intelligent connected ecosystems instead of standalone devices, while regulatory approvals and clinical evidence remain major entry barriers. Success increasingly depends on combining technological innovation, global service infrastructure, regulatory expertise, and recurring digital service capabilities.

Candela Corporation

Alma Lasers

Cynosure Lutronic

Lumenis

Cutera, Inc.

Fotona

Sciton, Inc.

El.En. S.p.A.

Aerolase Corporation

Venus Concept

Quanta System S.p.A.

DEKA M.E.L.A. S.r.l.

Artificial intelligence, advanced laser engineering, and connected digital platforms are redefining modern beauty photoelectric equipment. AI-assisted skin analysis, automated parameter selection, and real-time treatment optimization improve procedural consistency by approximately 28% while reducing consultation time by nearly 25%. More than 60% of premium aesthetic clinics now prioritize platforms integrating multiple treatment technologies with intelligent workflow software, enabling standardized clinical protocols and higher equipment utilization.

Multifunction platforms combining laser, radiofrequency, IPL, and diagnostic imaging are rapidly replacing conventional standalone devices. Compared with legacy single-application systems, integrated platforms improve treatment capacity by nearly 30% while reducing equipment footprint by approximately 20%. Cloud-enabled predictive maintenance further decreases unexpected downtime by around 18%, strengthening operational continuity. Premium manufacturers benefit most from this transition because integrated ecosystems create higher switching costs, recurring software revenue, and stronger long-term customer relationships than hardware-focused competitors.

Between 2026 and 2028, intelligent treatment personalization, digital twins for device calibration, and AI-supported clinical analytics will reshape competitive positioning. Adoption of connected equipment is expected to exceed 55% across premium aesthetic facilities as interoperability with patient management software becomes standard practice. Companies investing early in software ecosystems, cybersecurity, remote diagnostics, and modular hardware architectures will gain faster product scalability, stronger regulatory readiness, and sustainable differentiation as intelligent platforms become the industry's primary purchasing criterion.

May 2024 Candela launched the Vbeam Pro vascular laser platform featuring dual-wavelength capability, expanding treatment versatility for vascular and dermatologic procedures while strengthening its premium energy-based aesthetics portfolio. The platform combines 595 nm and 1064 nm wavelengths for broader clinical applications. Business impact: reinforces premium technology leadership. Source: PR Newswire

March 2025 Alma Lasers introduced the new Alma Harmony multifunction aesthetic platform integrating five treatment technologies into one system, including a platform delivering up to 45% higher energy output. Business impact: expands personalized treatment capabilities and strengthens platform-based competition. Source: Alma Lasers

January 2026 Candela unveiled the Glacē facial treatment platform during IMCAS Paris while showcasing Matrix and Vbeam Pro ahead of wider commercial availability. Business impact: accelerates expansion of integrated aesthetic treatment solutions across EMEA markets and strengthens premium product differentiation. Source: Business Wire

February 2026 Cynosure Lutronic received regulatory approvals for the Clarity II dual-wavelength laser platform in both China and Japan, expanding access to two major regulated aesthetic markets. Business impact: strengthens Asia-Pacific commercialization and enhances the company's competitive position in advanced laser technologies.

The report provides a comprehensive assessment of the global Beauty Photoelectric Equipment Market across Laser Systems, IPL Systems, Radiofrequency Systems, Ultrasound Systems, Plasma Devices, and Photodynamic Therapy equipment. It evaluates major applications including hair removal, skin rejuvenation, acne treatment, tattoo removal, pigmented lesion therapy, and vascular lesion treatment across dermatology clinics, hospitals, cosmetic surgery centers, medical spas, and beauty centers. Regional analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by operational, technology, and competitive intelligence.

The study analyzes adoption patterns, manufacturing concentration, deployment trends, and technology integration across leading equipment providers. It examines AI-enabled treatment systems, multifunction platforms, connected diagnostics, predictive maintenance, and digital workflow integration while profiling major industry participants. Strategic insights support investment prioritization, product positioning, expansion planning, partnership evaluation, competitive benchmarking, and identification of emerging opportunities expected to influence industry direction between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 5,127.4 Million |

|

Market Revenue in 2033 |

USD 11,901.7 Million |

|

CAGR (2026 - 2033) |

11.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Candela Corporation, Alma Lasers, Cynosure Lutronic, Lumenis, Cutera, Inc., Fotona, Sciton, Inc., El.En. S.p.A., Aerolase Corporation, Venus Concept, Quanta System S.p.A., DEKA M.E.L.A. S.r.l. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |