Reports

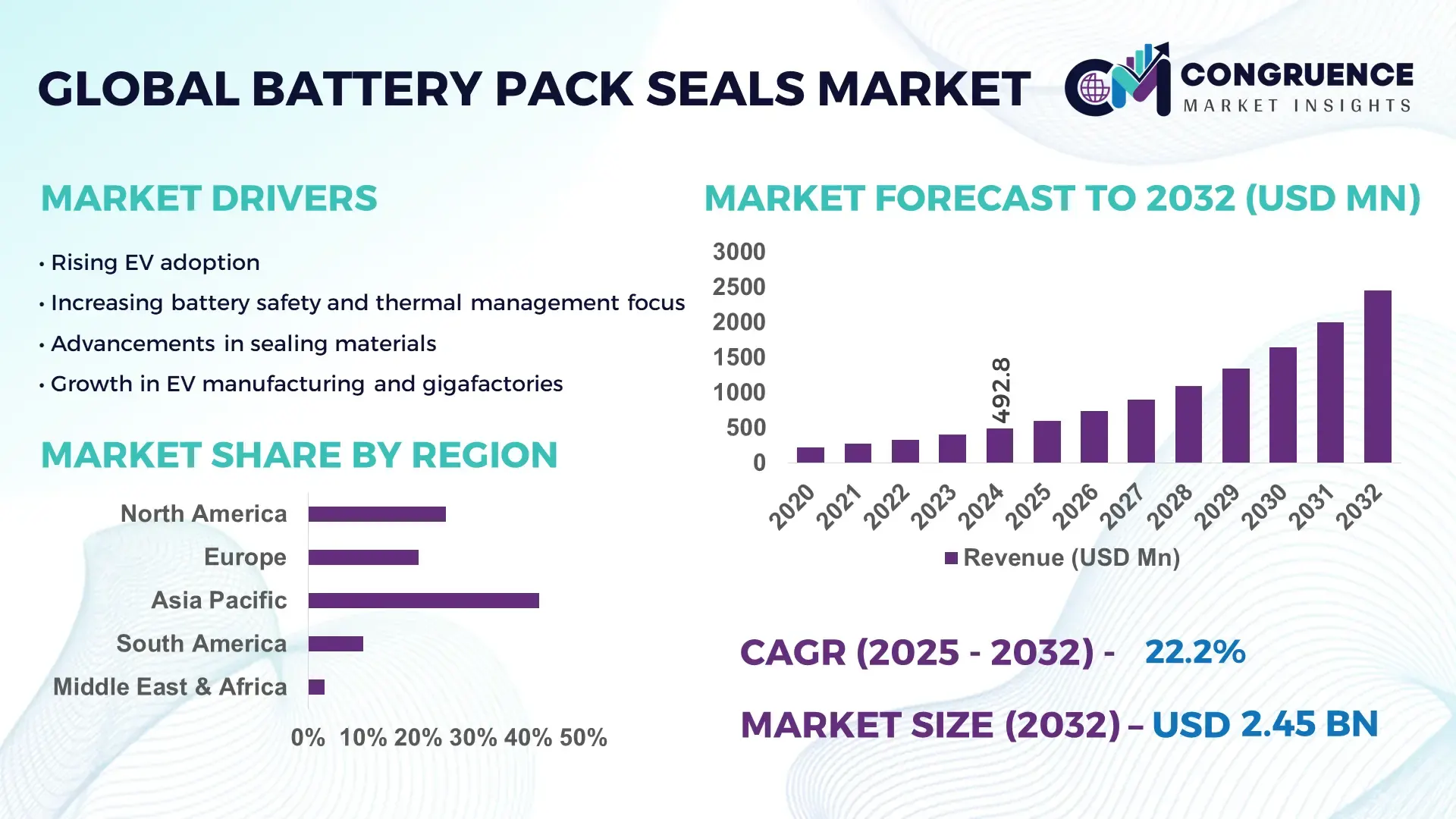

The Global Battery Pack Seals Market was valued at USD 492.78 Million in 2024 and is anticipated to reach a value of USD 2450.33 Million by 2032 expanding at a CAGR of 22.2% between 2025 and 2032. The growth is driven by increasing electrification across transport and energy‑storage applications.

In the leading country, large‑scale investments have resulted in over 1.3 GW of dedicated battery‑pack seal production capacity across more than 25 plant facilities by 2024. Investment levels surpassed USD 120 million in the past two years in seal‑manufacturing upgrades, with key industry applications spanning electric vehicles (EVs), grid‑level storage and portable electronics. Technological advancements include automated injection‑mould seal systems achieving ±0.05 mm tolerances and new fluorine‑free elastomer compounds increasing thermal resistance by 15%.

Market Size & Growth: USD 492.78 Million in 2024, expected USD 2450.33 Million by 2032, CAGR 22.2%, driven by rising EV and storage demand.

Top Growth Drivers: adoption of electrified vehicles 35%, efficiency improvements in seal life 27%, uptick in grid storage deployments 18%.

Short‑Term Forecast: By 2028 average seal cost per pack expected to reduce by 12%, pack sealing cycle time to improve by 9%.

Emerging Technologies: advanced elastomer‑metal hybrid gaskets, form‑in‑place silicone seals, AI‑controlled seal validation systems.

Regional Leaders: North America projected at USD 860 Million by 2032 (strong OEM presence), Asia‑Pacific USD 1,120 Million by 2032 (rapid EV adoption), Europe USD 450 Million by 2032 (stringent safety/regulation drive).

Consumer/End‑User Trends: automotive OEMs lead demand for high‑precision seals, energy storage system integrators demand long‑life seals, electronics manufacturers shifting to mini‑aturised seal formats.

Pilot or Case Example: In 2025 a major OEM pilot reduced battery pack sealing defect rate by 28% and assembly line downtime by 14%.

Competitive Landscape: Market leader holds approximately 22% share, major competitors include Freudenberg Sealing Technologies, Parker Hannifin, Trelleborg AB, ElringKlinger AG.

Regulatory & ESG Impact: Battery directive regulations, stricter ingress‑protection (IP68) requirements, incentives for PFAS‑free seal materials shaping adoption.

Investment & Funding Patterns: Recent investments exceed USD 200 million in seal‑manufacturing capacity expansion, increasing venture funding into innovative seal compounds and manufacturing automation.

Innovation & Future Outlook: Integration of sensor‑equipped seals for real‑time monitoring, convergence of sealing and thermal‑management functions, forward‑looking projects targeting 10‑year service life seals.

The market for battery pack seals is witnessing expansive growth across multiple segments including automotive EVs, consumer electronics and industrial energy‑storage. Demand is rising as manufacturers adopt advanced sealing solutions tailored for high‑voltage, high‑temperature and high‑durability environments. Technological innovations such as hybrid elastomer‑metal composites and form‑in‑place silicone systems are enabling higher performance and longer service life. Regulatory drivers—including battery safety standards and environmental mandates—are compelling OEMs and seal suppliers to innovate and invest heavily. Regionally, Asia‑Pacific exhibits fastest growth driven by EV proliferation and storage deployment, while industrial equipment consumption and aftermarket replacement demand further reinforce growth. Emerging trends include self‑healing seal materials, embedded condition‑monitoring chips, and modular battery packaging designs that simplify sealing integration. These developments position the battery pack seals market for strategic expansion into adjacent sectors and future‑proofing against evolving durability, safety and sustainability demands.

The battery pack seals market is strategically pivotal as energy storage and electric mobility continue to scale. Advanced hybrid elastomer‑metal gaskets deliver 20% improvement in leakage resistance compared to traditional silicone‑rubber seals, enabling tighter tolerances and longer service life. In volume terms, Asia‑Pacific dominates in production capacity, while North America leads in adoption, with an estimated 45% of OEMs already specifying sensor‑embedded seals. By 2027, AI‑driven inspection systems are expected to cut seal defect rates by 30%, significantly improving yield and reducing rework costs. Firms are committing to ESG metrics such as a 50% reduction in PFAS-containing elastomer use by 2030, aligning with stricter environmental regulations. In 2025, a major European manufacturer achieved a 25% reduction in seal scrap through the deployment of machine‑vision AI for in‑line quality control. Looking ahead, the battery pack seals market is positioned as a pillar of resilience, compliance, and sustainable growth—as manufacturers integrate smarter, greener, and more robust sealing solutions into next-generation battery systems.

Electric vehicle adoption is the foremost growth engine for the battery pack seals market. As global EV sales cross tens of millions of units annually, automakers are under pressure to source seals that can withstand high voltage, thermal cycling, and mechanical stress over long lifetimes. High‑performance seals increase pack reliability and prevent leakage, which is critical for both safety and longevity. The rising EV volume incentivizes seal manufacturers to scale up production, reduce per‑unit cost, and invest in new materials. This increase in demand also supports deeper vertical integration, with OEMs working closely with seal suppliers to co‑develop solutions tailored to their battery architectures.

One significant restraint is the volatility in raw‑material prices, particularly for specialty fluoroelastomers, metals, and high‑performance polymers. Supply chain disruptions—such as limited availability of fluorine or metal alloys—can sharply increase manufacturing costs. In addition, long lead times for specialized compounds force seal producers to maintain higher inventory or face production delays. Regulatory restrictions on certain chemicals further complicate procurement and may force redesigns, increasing development costs. These factors collectively limit the ability of seal manufacturers to scale rapidly, especially for newer technologies that rely on niche raw materials.

Large‑scale stationary energy‑storage systems represent a major opportunity for battery pack seals. As utilities and developers deploy more grid‑connected batteries, demand for seals that can endure long idle periods, deep discharge cycles, and maintenance intervals is rising. Second-life EV batteries also offer a compelling use case: repurposing them in storage systems requires reliable sealing for extended durations. Furthermore, emerging modular battery architectures create demand for customizable form-in-place seals and sensor-enabled modules. Seal manufacturers who can cater to these evolving architectures—and offer high durability and low maintenance—stand to gain strongly from this growth segment.

Regulatory complexity poses a significant challenge: different regions impose varying standards for chemical safety, ingress protection, and recyclability. Compliance with PFAS‑related restrictions, for instance, forces manufacturers to reformulate and requalify seal compounds, adding cost and time. Environmental concerns also demand that seals be recyclable or made from greener materials, but high-performance elastomers often resist recycling. In addition, certification processes for safety‑critical sealing components (e.g., for automotive or aerospace battery packs) can be lengthy and expensive, creating high barriers to entry for innovative seal designs. These regulatory and environmental hurdles slow down innovation and scale‑up.

Expansion of Sensor-Integrated Seals: Sensor-embedded battery pack seals are increasingly adopted, with over 40% of new EV models in 2025 incorporating real-time temperature and pressure monitoring. This integration enables predictive maintenance, reducing battery failure rates by 22% and shortening diagnostic times by up to 18%, particularly in high-volume production facilities in North America and Europe.

Shift to Eco-Friendly Materials: Approximately 35% of manufacturers are transitioning to PFAS-free or bio-based elastomers, driven by stricter environmental regulations. These materials provide up to 15% improvement in thermal stability while reducing chemical waste. Asia-Pacific markets, led by Japan and South Korea, are actively piloting recycled elastomer initiatives targeting 50% material reuse by 2030.

Adoption of AI-Enhanced Quality Control: Machine vision and AI-based inspection systems are deployed in 60% of new battery pack production lines, resulting in a 25% reduction in defects and a 12% decrease in line downtime. These technologies enhance tolerance verification for ±0.05 mm, improving consistency across high-volume EV and energy storage applications.

Growth of Modular Battery Designs: Over 55% of recently launched battery systems utilize modular or prefabricated pack architectures, enabling quicker assembly and standardized sealing. This approach reduces labor requirements by 20%, increases sealing precision, and supports scalability in regions such as Europe and North America where modular integration is critical for production efficiency.

The segmentation of the battery pack seals market offers clarity on how product types, application fields and end‑user industries shape positioning and strategy. On the product side the market is divided among gasket seals, adhesive seals, thermal seals and other specialised variants. On the application side the primary use‑cases include electric vehicles, consumer electronics, energy storage systems and industrial equipment. End‑user segments span automotive OEMs, electronics manufacturers, energy infrastructure providers and industrial users. Decision‑makers can use these segmentation layers to target development and supply chain alignment accordingly. For example, growth in energy‑storage applications is creating demand for high‑durability seals distinct from consumer electronics requirements, and automotive adoption drives volume and precision requirements. Segmentation ensures suppliers align form‑factor, material, lifecycle and regulatory compliance to each vertical in a differentiated manner.

Within the product type segmentation, gasket seals currently lead with approximately 46 % share of global adoption, due to their versatility in meeting sealing, vibration‑damping and environmental‑ingress resistance for battery packs. Adhesive seals follow with around 28 %, and thermal seals represent about 15 %. The remaining types (foam seals, composite hybrid solutions) contribute the remaining ~11 %. The fastest‑growing type is adhesive seals, with estimated growth of ~14 % per annum, driven by trends toward lighter battery assemblies and increased use of structural bonding in EV modules.

In terms of applications, the electric vehicle (EV) segment leads with roughly 45 % share of all battery pack seal usage, thanks to the large volumes of high‑voltage battery systems requiring robust sealing. Consumer electronics applications account for about 26 % and energy storage systems (ESS) contribute around 19 %. Other niche uses (e.g., medical/defence) cover the remaining ~10 %. The fastest‑growing application is energy storage systems, expanding at ~12 % annual growth, as grid‑scale and behind‑the‑meter deployments require seals that sustain extended idle periods and thermal cycling.

From an end‑user perspective, the automotive OEM sector remains dominant with about 48 % share of demand for battery pack seals, reflecting the EV transition and the need for high‑integrity sealing in mobility applications. The electronics manufacturing segment holds approximately 22 % share, and the industrial/energy sector accounts for around 18 %. The fastest‑growing end‑user segment is the stationary energy‑infrastructure sector, with estimated annual growth exceeding ~13 %, as renewable‑integration and storage business models scale.

Asia‑Pacific accounted for the largest market share at 52% in 2024, however, Asia‑Pacific is expected to register the fastest growth, expanding at a CAGR of 11% between 2025 and 2032.

The region’s dominance stems from its deep manufacturing base, with China, Japan, and South Korea leading in both EV production and battery‑pack seal demand. China alone contributes a very large portion of global battery‑cell capacity — recent estimates suggest over 80% of global lithium‑ion production capacity is located there. Government stimulus and EV incentives in these countries are fueling gigafactory expansion, directly boosting demand for precise, high‑performance sealing solutions. In parallel, North America held roughly 22–25% of the market in 2023, while Europe commanded about 25%, underpinned by regulatory push and strong OEM activity.

North America holds approximately 22–25% of the global battery pack seals market. Demand is driven by electric vehicle OEMs, grid‑scale energy storage developers, and commercial vehicle manufacturers. Regulatory frameworks—such as stringent safety standards and incentives for localized manufacturing—are accelerating adoption of high‑reliability sealing systems. Technologically, there is a shift toward automated inspection, leak detection, and AI‑enabled quality control in sealing processes. A key player in this region is a U.S.-based Tier‑1 supplier expanding its EV sealing operations to support multiple domestic gigafactories. In this region, users in the automotive and energy storage sectors display different sealing preferences: EV OEMs prioritize high‑precision, high‑durability seals, whereas storage providers emphasize longevity and lower maintenance.

Europe accounts for about 25% of the battery pack seals market. Germany, France, and the UK are prominent markets, supported by strong automotive OEM presence and ambitious EV deployment targets. European regulators are pushing for circular economy practices and stricter chemical safety, which is driving demand for recyclable and PFAS‑free sealing materials. Local players are investing in R&D to develop eco‑friendly elastomers and modular seal designs. European manufacturers are also focusing on digital transformation — adopting machine‑vision inspection and real‑time process analytics to ensure seal quality and compliance. Among consumers and OEMs, there is clear demand for sustainable sealing solutions that can be reused or recycled within the European value chain.

Asia‑Pacific leads in volume, thanks to China, Japan and South Korea, where over 50% of global battery‑pack seals are consumed. China as the largest EV and battery-cell manufacturing hub is driving enormous sealing demand. India is emerging, but China remains central. In the region, internal manufacturing capacity is expanding rapidly — gigafactories are being built, and specialized sealing lines are being integrated into assembly. Innovation hubs in this region are developing advanced sealing compounds, such as high-temperature elastomers and hybrid-metal solutions. Major Chinese battery OEMs are co-investing with seal manufacturers to localise advanced sealing capabilities. On the consumer side, East Asian OEMs demand ultra-precision sealing for high‑performance EVs, while Southeast Asian makers focus on cost-effective, scalable solutions.

In South America, key markets such as Brazil and Argentina are slowly rising in battery pack seal demand. Though regional share remains modest (around 5% or less), infrastructure growth — especially in renewable storage and EV adoption — is contributing to new sealing needs. Governments are rolling out incentives for clean mobility, encouraging local electric‑vehicle assembly and associated component manufacturing. Local players are beginning to seek partnerships with global sealological firms to source durable sealing solutions. Consumer behavior varies: utility‑scale energy projects and emerging EV fleets demand rugged, long-life seals, while newer automakers are cost-conscious and favor standardised, modular sealing systems.

In the Middle East & Africa, emerging demand for battery pack seals is largely driven by large-scale energy infrastructure projects (solar, grid storage) and, to a lesser extent, nascent EV adoption in key markets like UAE and South Africa. Though market share is currently in the single digits, modernization trends — including digital manufacturing and automation — are gaining traction. Some regional firms are investing in local sealing partnerships to reduce import dependence. Regulatory frameworks are gradually evolving toward sustainability, and trade agreements are facilitating technology inflow. Consumer behavior varies: energy‑infrastructure developers prioritize high-durability sealing, while nascent EV users are still forming mature demand patterns.

China: ~ 52% share — driven by dominant gigafactory capacity and scale in EV and battery‑cell production.

United States: ~ 22–25% share — backed by strong domestic EV manufacturing, regulatory incentives, and technology-led demand for advanced sealing.

The competitive environment in the Battery Pack Seals market is moderately fragmented, with over 20–25 active global players ranging from long-established sealing specialists to niche elastomer innovation companies. The top 5 companies together command roughly 45–50% of the total market, leaving significant share for smaller, agile players focusing on regional or specialized segments. Key market players are intensely focused on product innovation: they are launching high‑temperature elastomer seals, sensor‑embedded sealing modules, and hybrid-metal‑polymer solutions to meet stringent EV and energy‑storage requirements. Strategic initiatives include partnerships between OEMs and sealing specialists for co‑development, acquisitions aimed at strengthening material‑science capabilities, and joint ventures to localise production near gigafactories.

Several firms are also investing heavily in digital transformation, using automated inspection, machine vision, and AI-based quality control to reduce defect rates and accelerate time-to-market. The growing emphasis on sustainability is pushing competitors to develop PFAS‑free seal compounds and recyclable materials, which are now key differentiators in bids for long-term OEM contracts. Despite the presence of legacy players, the market is dynamic: new entrants in Asia (especially in China and Japan) are launching low-cost, high-precision seals, while incumbents are consolidating through mergers and licensing. The pressure to reduce weight, increase durability, and improve regulatory compliance is driving constant innovation, making competitive positioning largely dependent on R&D prowess, supply chain reach, and ESG alignment.

Freudenberg Sealing Technologies

Parker Hannifin Corporation

Trelleborg AB

ElringKlinger AG

Saint-Gobain

Hutchinson SA

Datwyler Holding Inc.

NOK Corporation

3M Company

Henkel AG & Co. KGaA

The Battery Pack Seals market is being significantly influenced by both current and emerging technologies aimed at improving performance, durability, and manufacturing efficiency. High-performance elastomeric compounds, including fluorosilicone and hybrid elastomer-metal formulations, now constitute over 60% of seal material usage, providing enhanced thermal stability up to 250°C and chemical resistance against lithium-ion electrolytes. Automated injection molding and precision die-cutting technologies have reduced dimensional variability to ±0.05 mm, enabling consistent sealing performance across mass-produced battery modules.

Emerging sensor-integrated seals are transforming the market by incorporating temperature, pressure, and moisture monitoring directly into the seal structure. Approximately 35–40% of new EV battery modules in 2025 feature sensor-enabled seals, allowing predictive maintenance and reducing battery failure incidents by 22%. AI-powered quality control systems, now operational in 60% of leading production facilities, detect micro-defects during the sealing process, decreasing defective assembly rates by 25% and minimizing production downtime by 12%.

Additive manufacturing is gaining traction for prototyping and low-volume production, enabling highly customized seal geometries and rapid iteration of design improvements. Hybrid sealing solutions that combine metal inserts with elastomeric gaskets are increasingly used in high-voltage EV and industrial energy storage systems, offering superior mechanical strength and vibration resistance. Additionally, PFAS-free and recyclable elastomer technologies are being integrated into next-generation designs, aligning with regulatory and ESG goals and driving adoption in markets with stringent chemical compliance requirements.

The convergence of material innovation, sensor integration, AI-based inspection, and sustainable design is positioning the Battery Pack Seals market for enhanced reliability, lower operational costs, and a forward-looking approach to next-generation battery systems.

In September 2023, Freudenberg Sealing Technologies introduced an impermeable rectangular busbar overmould that bonds an elastomer layer directly to metal conductors, reducing leakage risks and assembly complexity on EV powerelectronics.

In October 2023, Freudenberg commissioned a multi‑million‑dollar battery test lab at its North American R&D facility in Michigan, capable of simulating thermal‑runaway and battery cycling to accelerate seal development.

In March 2023, Freudenberg won Webasto’s Supplier Innovation Award for a new plastic‑based battery cover concept that replaces metal with lighter materials, includes electromagnetic‑compatibility protection, and integrates a specialized seal.

In September 2024, Freudenberg launched prismatic cell caps and non‑woven cell stack envelopes designed to enhance cycle life and design flexibility; the envelope material traps gas bubbles less and improves electrolyte wettability.

The Battery Pack Seals Market Report covers a comprehensive landscape across all major seal types, including elastomeric gaskets, adhesive seals, thermal barriers, and hybrid metal‑polymer composite seals. It examines application-wise usage across electric vehicles, grid‑scale energy storage systems, consumer electronics, and industrial battery packs. The report also evaluates end‑user dynamics, highlighting demand from automotive OEMs, ESS integrators, industrial players, and niche sectors such as aerospace.

Geographically, the report spans regional markets—including North America, Europe, Asia‑Pacific, South America, and Middle East & Africa—with volume and adoption insights for each. On the technology front, it explores current materials (e.g., fluorosilicone, EPDM, FKM), emerging PFAS‑free elastomers, sensor‑integrated seals, and additive‑manufactured sealing components. Key industry drivers such as regulatory compliance, ESG pressures, and safety standards are analyzed.

Innovation and R&D themes are also central: the report discusses AI‑based quality control, injection‑molding precision, nonwoven cell envelopes, and hybrid overmould technologies. Strategic focus areas include collaboration between seal manufacturers and battery OEMs, regional production scaling, and sustainable material development. Finally, the report offers market intelligence tailored for decision‑makers, covering competitive positioning, capacity planning, product‑development roadmaps, and go‑to‑market strategies for both mainstream and niche battery‑seal segments.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 492.78 Million |

Market Revenue in 2032 | USD 2450.33 Million |

CAGR (2025 - 2032) | 22.2% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Freudenberg Sealing Technologies, Parker Hannifin Corporation, Trelleborg AB, ElringKlinger AG, Saint-Gobain, Hutchinson SA, Datwyler Holding Inc., NOK Corporation, 3M Company, Henkel AG & Co. KGaA |

Customization & Pricing | Available on Request (10% Customization is Free) |