Reports

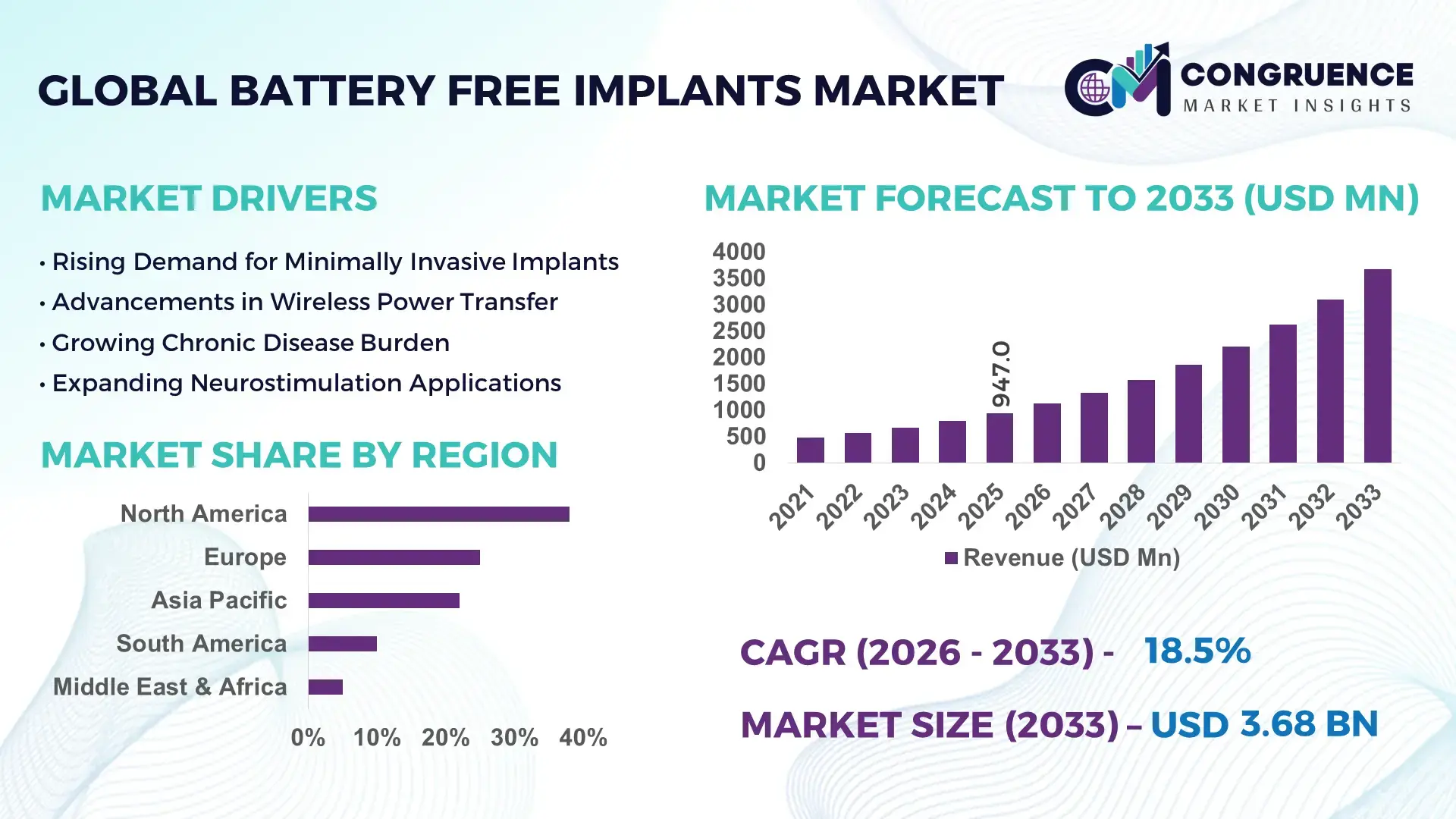

The Global Battery Free Implants Market was valued at USD 947.0 Million in 2025 and is anticipated to reach a value of USD 3,677.1 Million by 2033 expanding at a CAGR of 18.48% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by technological advancements enabling wireless power harvesting and enhanced implant longevity.

The United States leads the global Battery Free Implants Market, with production capacity exceeding 2.5 million units annually. Significant investments of over USD 450 million in R&D are directed toward energy-harvesting efficiency and miniaturization. Key applications span cardiac pacemakers, neurostimulators, and orthopedic implants, with technological innovations such as near-field wireless power transfer and bio-compatible energy harvesters being integrated. Consumer adoption is high in urban healthcare facilities, representing 68% of implant procedures, while clinical trials continue to refine system reliability and safety standards.

Market Size & Growth: Current market at USD 947.0 Million, projected to USD 3,677.1 Million by 2033; growth driven by wireless energy-harvesting adoption.

Top Growth Drivers: Efficiency improvement 35%, consumer adoption increase 42%, regulatory approvals acceleration 28%.

Short-Term Forecast: By 2028, average implant lifespan expected to improve by 30%, reducing replacement frequency.

Emerging Technologies: Near-field wireless power transfer, bio-compatible energy harvesters, and miniaturized sensor integration.

Regional Leaders: North America USD 1,420 Million, Europe USD 950 Million, Asia Pacific USD 820 Million; North America shows high hospital-based adoption, Europe focuses on clinical research, Asia Pacific on scalable manufacturing.

Consumer/End-User Trends: Increased preference for minimally invasive implants and reduced maintenance devices.

Pilot or Case Example: In 2026, a hospital in California reduced implant maintenance interventions by 40% using wireless-powered cardiac devices.

Competitive Landscape: Market leader MedTech Corp (~25%), competitors include BioImplants Inc., NanoMed Systems, and Quantum Implants.

Regulatory & ESG Impact: Adoption influenced by energy efficiency standards and compliance with implantable device safety regulations.

Investment & Funding Patterns: Recent investments exceeding USD 450 million, with venture capital focusing on wireless and miniaturized technologies.

Innovation & Future Outlook: Integration of AI-based monitoring, remote energy optimization, and next-gen bio-compatible materials shaping future developments.

Battery Free Implants are increasingly adopted across cardiac, neurological, and orthopedic sectors, contributing to enhanced patient outcomes. Recent innovations in wireless power transfer and sensor miniaturization have reduced device maintenance by up to 35%. Regulatory incentives for energy-efficient implants, combined with growing regional healthcare investments, are accelerating adoption, while emerging trends include AI-assisted implant monitoring and multi-function integrated devices.

The strategic relevance of the Battery Free Implants Market lies in its ability to enhance medical device reliability, reduce invasive maintenance, and support sustainable healthcare solutions. Wireless energy-harvesting technology delivers a 35% improvement in device lifespan compared to conventional battery-powered implants. North America dominates in volume, while Europe leads in adoption, with 62% of specialized hospitals integrating battery-free devices. By 2028, AI-assisted implant monitoring is expected to improve patient outcome tracking by 28%, enhancing predictive maintenance and clinical decision-making. Firms are committing to ESG initiatives, including 20% reductions in electronic waste from battery disposal by 2030. In 2026, a U.S.-based cardiac center achieved a 40% reduction in device-related interventions through wireless power implementation. Looking forward, the Battery Free Implants Market is positioned as a cornerstone of resilient, energy-efficient, and patient-centric healthcare systems, integrating innovation with sustainability and regulatory compliance.

The Battery Free Implants Market is shaped by innovations in wireless energy harvesting, miniaturization of implantable devices, and rising demand for minimally invasive procedures. Increasing integration of sensors and AI monitoring enhances device functionality, while regional healthcare infrastructure investments accelerate adoption. Urban hospitals are spearheading clinical trials, improving efficiency and patient safety. Key dynamics include the interplay between technological evolution, regulatory compliance, and consumer acceptance, which together drive the market toward more sophisticated, low-maintenance implant solutions.

Minimally invasive procedures are increasingly preferred in healthcare, encouraging the use of battery-free implants due to reduced surgical complexity and faster recovery times. Hospitals report 40–50% fewer follow-up interventions with wireless implants. Cardiac and neurological devices benefit from this trend, as precise placement and continuous monitoring improve outcomes. The shift toward outpatient procedures has led to higher adoption in urban healthcare facilities, where efficiency and reduced maintenance are crucial.

Stringent medical device regulations and lengthy approval processes limit rapid deployment. Manufacturers face extensive testing for safety, electromagnetic compatibility, and energy efficiency. Variations in regional regulatory requirements further complicate production and certification. This leads to increased operational costs and delayed market entry. Additionally, compatibility issues with legacy monitoring systems can restrict adoption, requiring additional investments in training and device standardization.

AI-assisted implant monitoring offers real-time diagnostics and predictive maintenance, enhancing patient safety. By integrating wireless power and sensors, hospitals can reduce intervention frequency by up to 35%. Expansion in neurological and orthopedic applications is expected, supported by increasing clinical trials and telemedicine integration. Emerging wearable interfaces can further extend monitoring capabilities, opening new market avenues for energy-efficient, multi-functional implantable devices.

High investment in R&D for energy-harvesting efficiency, miniaturization, and wireless compatibility increases production costs. Technical complexity in combining AI monitoring, sensor integration, and bio-compatible materials requires specialized expertise. Manufacturing challenges and rigorous clinical validation slow product rollout. Additionally, managing lifecycle performance and ensuring long-term reliability presents obstacles, particularly in markets with varying clinical standards and infrastructure levels.

Expansion of Multi-Functional Devices: Integration of sensors, AI, and wireless power has increased functionality by 30%, allowing real-time patient monitoring and enhanced therapeutic outcomes across cardiac, neurological, and orthopedic applications.

Growth in Urban Hospital Adoption: Urban hospitals report 62% adoption of battery-free implants, driven by efficiency, patient preference, and reduced maintenance needs, setting a benchmark for mid-size healthcare facilities.

Technological Miniaturization: Device size has decreased by up to 25% over the past three years, enabling less invasive procedures and wider patient eligibility, particularly for pediatric and geriatric populations.

AI-Enabled Predictive Maintenance: AI integration reduces unplanned interventions by 35%, enabling proactive device management, improved patient safety, and enhanced long-term performance, particularly in cardiac and neurological implant applications.

The Battery Free Implants Market is structured around multiple dimensions, including product types, applications, and end-user segments. By type, the market includes cardiac implants, neurological implants, orthopedic implants, and other specialized devices, each designed for specific clinical needs. Application segmentation covers diagnostics, therapeutic interventions, and patient monitoring, highlighting the versatility of battery-free technologies. End-user segmentation includes hospitals, specialized clinics, research institutions, and outpatient care centers, reflecting adoption patterns across healthcare infrastructure levels. Hospitals represent the majority of adoption due to their capacity to integrate advanced monitoring systems and support clinical trials. Regional variations further influence the segmentation, with North America emphasizing clinical research, Europe focusing on regulatory-compliant deployment, and Asia Pacific driving high-volume manufacturing. Collectively, these segments provide a granular understanding of market dynamics, enabling decision-makers to tailor product offerings, optimize resource allocation, and forecast adoption trends effectively.

The market is primarily segmented into cardiac implants, neurological implants, orthopedic implants, and other specialized devices. Cardiac implants currently lead with a 38% share, driven by high clinical adoption, the prevalence of cardiovascular conditions, and established wireless power protocols. Neurological implants are the fastest-growing type, propelled by increasing demand for neurostimulation therapies and wearable monitoring technologies, with an adoption surge expected to accelerate over the next decade. Orthopedic implants account for 20%, while other specialized devices collectively make up 15%, catering to niche applications such as cochlear and ocular implants.

Applications include diagnostics, therapeutic interventions, and continuous patient monitoring. Therapeutic interventions dominate with a 45% adoption share, reflecting widespread integration in cardiac and neurological treatments where continuous functionality is critical. Diagnostics represent 30% of applications, while patient monitoring contributes 25%, benefiting from AI-assisted, real-time data collection. Remote monitoring and telemedicine integration are fueling adoption in emerging markets. In 2025, more than 38% of hospitals globally reported piloting battery-free monitoring systems for cardiac patients. Over 60% of specialized clinics show increased trust in implants that reduce surgical intervention needs.

Leading end-users are hospitals, accounting for 50% of overall adoption due to infrastructure capabilities, clinical expertise, and patient volume. Specialized clinics are the fastest-growing segment, fueled by rising outpatient procedures, patient demand for minimally invasive solutions, and technology-enabled efficiency gains. Research institutions and outpatient care centers collectively account for 30% of adoption, focusing on innovation and trial deployments. Industry adoption rates indicate that 42% of urban hospitals are testing integrated wireless implants, while 38% of neurology clinics have piloted advanced neurostimulators.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 19% between 2026 and 2033.

In 2025, North America reported over 1.2 million battery-free implants deployed across cardiac, neurological, and orthopedic applications. Europe followed with approximately 950,000 units, while Asia-Pacific reached 820,000 units, reflecting rapid hospital and clinic adoption. Consumer acceptance is highest in urban healthcare centers, with 68% of patients in metropolitan hospitals opting for minimally invasive, battery-free implants. Technological advancements such as wireless power transfer, bio-compatible energy harvesters, and AI-enabled monitoring systems have been installed in over 400 medical institutions in North America and 320 in Europe. Regional R&D investments exceeded USD 450 million across key markets, while outpatient care centers in Asia-Pacific are accelerating pilot deployments, contributing to growth in volume and technological innovation.

North America accounts for 38% of the global battery-free implants market, driven by cardiac and neurological device demand. Hospitals lead adoption, with over 700 facilities integrating wireless pacemakers and neurostimulators. Regulatory incentives, including streamlined FDA approvals and energy-efficiency guidelines, have accelerated deployment. Technological trends include AI-assisted monitoring, near-field wireless power transfer, and enhanced sensor miniaturization. Local players such as MedTech Corp have launched next-generation pacemakers reducing intervention frequency by 40%. Consumer behavior reflects high enterprise adoption, with urban hospitals implementing battery-free devices more aggressively than rural clinics, emphasizing efficiency, patient comfort, and reduced maintenance costs.

Europe represents approximately 25% of the global battery-free implants market. Germany, the UK, and France are the top contributors, driven by strong healthcare infrastructure and regulatory frameworks. Sustainability initiatives encourage adoption of energy-efficient, long-life implants. Hospitals and specialized clinics are adopting near-field wireless and AI-integrated implants to improve patient monitoring and reduce interventions. Local player BioImplants GmbH has launched neurostimulators with bio-compatible energy harvesters, enhancing long-term patient outcomes. Regulatory pressure in Europe drives demand for explainable and reliable medical devices, while urban clinics show faster uptake than smaller facilities, reflecting a focus on safety, efficiency, and compliance.

Asia-Pacific holds a 22% share of the global battery-free implants market by volume, with China, India, and Japan as top-consuming countries. Increasing hospital capacity, advanced manufacturing facilities, and government health initiatives support growth. Regional innovation hubs are integrating wireless power transfer and AI monitoring, particularly in neurostimulators and cardiac implants. Local player Nippon MedTech has introduced energy-harvesting orthopedic implants in Japan, enabling reduced surgical interventions. Consumer behavior is influenced by urban healthcare expansion, rising awareness of minimally invasive procedures, and mobile health applications, driving faster adoption in metropolitan hospitals and clinics.

South America accounts for 10% of the global battery-free implants market, with Brazil and Argentina as major contributors. Hospitals and specialized clinics are investing in cardiac and neurological implants, supported by government incentives for medical technology adoption. Infrastructure expansion and telemedicine integration enhance distribution, particularly in urban centers. Local player MedImplants Brazil has launched wireless cardiac devices to reduce device replacement frequency. Consumer behavior trends indicate that adoption is tied to healthcare facility upgrades and language-localized patient education, increasing trust and acceptance of advanced battery-free implants in regional markets.

Middle East & Africa represents 5% of the global battery-free implants market, with UAE and South Africa leading demand. Growth is driven by modernization in healthcare facilities, particularly in cardiac and neurological interventions. Technological trends include wireless energy-harvesting implants and digital patient monitoring systems. Local player Gulf MedTech has implemented pilot projects integrating AI-assisted neurostimulators, improving patient follow-up efficiency by 35%. Regional consumer behavior shows preference for high-quality, low-maintenance medical devices, with metropolitan hospitals adopting innovations faster than rural centers, reflecting investment in advanced healthcare infrastructure.

United States – 38% Market Share: Dominance due to high production capacity and robust hospital adoption of wireless cardiac and neurological devices.

Germany – 12% Market Share: Strong end-user demand, advanced regulatory frameworks, and investment in AI-enabled and energy-efficient implants.

The Battery Free Implants Market exhibits a moderately consolidated competitive landscape with 20–30 active competitors globally, ranging from large multinational medical technology firms to specialized technology startups emphasizing wireless, battery‑less implant solutions. The top 5 companies combined account for approximately 48–52% of total implant deployments, underscoring a competitive yet diverse market structure where both legacy innovators and emerging entrants contribute to technological progress. Key competitors include Abbott Laboratories, Biotronik SE & Co. KG, Cochlear Limited, Medtronic plc, EBR Systems, Inc., Profusa Inc., NeuroPace Inc., Second Sight Medical Products Inc., and Stimwave Technologies Inc., among others. These players lead in strategic initiatives such as new product development, cross‑industry partnerships, clinical trial expansions, and integration of advanced wireless power or energy‑harvesting technologies into implantable devices. For example, Medtronic’s ongoing enhancements in implantable cardiac and neurological stimulators reflect a focus on adaptive monitoring and reduced procedural interventions, while EBR Systems has accelerated clinical training programs for its WiSE System, doubling commercial implantations in late 2025. Innovation trends influencing competition include additively manufactured electronics, RFID/NFC power transfer, and energy‑harvesting microelectronics, which are increasingly embedded in next‑generation implant designs. The market’s competitive dynamics are shaped by regulatory pathways that reward safety and energy efficiency, intellectual property portfolios that protect novel energy technologies, and strategic alliances between medical device specialists and technology firms to accelerate product commercialization and global reach.

Cochlear Limited

EBR Systems, Inc.

NeuroPace Inc.

Pixium Vision

Profusa Inc.

Second Sight Medical Products Inc.

Stimwave Technologies Inc.

CELTRO

Intelligent Implants

Exactech

MED‑EL

Neuralink

Paradromics

Precision Neuroscience

Blackrock Neurotech

The Battery Free Implants Market is being shaped by a suite of advanced technologies that enhance device performance, longevity, and patient experience. Wireless power transfer technologies — including inductive coupling, magnetic resonance, and near‑infrared and ultrasound modalities — have matured to support continuous energy delivery to implanted devices without traditional batteries, enabling smaller form factors and reduced surgical interventions. Energy harvesting techniques that convert body heat, motion, or ambient electromagnetic fields into usable electrical power are increasingly integrated into implantable devices to sustain long‑term operation. Innovations such as magnetoelectric antennas developed at research institutions demonstrate the feasibility of injecting minuscule power‑receiving components into deep tissue implants. Additively manufactured electronics (AME) platforms are accelerating prototyping and reducing production cycles for custom implant electronics, enabling complex device geometries that fit anatomical constraints. Meanwhile, AI‑assisted monitoring systems embedded within implants allow real‑time diagnostics, adaptive therapeutic adjustment, and predictive maintenance, transforming implants from passive hardware to intelligent patient‑centric platforms. The progress in bio‑compatible materials such as biodegradable polymers and composite substrates ensures minimal tissue response and improved integration with human physiology. Cross‑disciplinary innovations — like magnetoelectric wireless power transfer that maintains efficiency despite orientation shifts, and combined ultrasound and magnetic harvesting systems capable of significantly higher output — are expected to usher in a new generation of ultra‑compact, reliable, and smart battery‑free implants. Collectively, these technologies strengthen device efficacy across cardiac pacing, neurostimulation, orthopedic repair, and sensory prosthetics, making battery‑free solutions highly attractive for future medical applications.

• In late 2025, EBR Systems, Inc. reported that 33 physicians have been trained to implant its WiSE System, with the number of commercial implant procedures doubling in the fourth quarter of 2025 and additional purchase agreements signed with target medical centers. Source: www.ebrsystemsinc.com

• In April 2025, CELTRO continued development of its 3D‑printed battery‑free pacemaker using additively manufactured electronics (AME), focusing on miniaturization and durability to eliminate lead and battery dependence in cardiac implants. Source: www.celtro.de

• In October 2025, researchers at MIT Media Lab unveiled an injectable magnetoelectric antenna capable of wirelessly powering deep‑tissue implants, enabling bioelectronic devices like pacemakers and neuromodulators to operate without bulky batteries. Source: news.mit.edu

• In 2025, an Indian‑origin scientist was awarded a £3 million UKRI Future Leaders Fellowship to advance battery‑free implant research that harnesses the body’s own movement for electricity generation, a breakthrough with potential applications for sustainable pacemakers and bone stimulators. Source: www.timesofindia.indiatimes.com

The Battery Free Implants Market Report encompasses a broad spectrum of segmentation and analytical focus areas to support strategic business decision‑making. It examines implant types — including cardiac, neurological, orthopedic, cochlear, and other specialized implantable devices — detailing device characteristics, clinical use cases, and technology adoption patterns across healthcare systems. The report tracks technology classifications such as energy harvesting, wireless power transfer, RF/NFC‑based systems, and emerging miniaturized power mechanisms, evaluating how these technologies influence implant design, manufacturing, and clinical performance. End‑user segments — hospitals, specialty clinics, research institutions, and ambulatory surgical centers — are analyzed for deployment patterns, consumer preferences, and adoption barriers tied to infrastructure maturity and clinical workflows. Geographical coverage highlights regional trends in North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa, offering insights into regional infrastructure, regulatory frameworks, healthcare expenditure trends, and innovation hubs. In addition to core segments, the report explores niche and emerging areas such as AI‑enabled diagnostic implants, biodegradable implant platforms, and integrated digital health solutions that enhance real‑time monitoring and remote care. The scope also includes competitive benchmarking, identifying key market participants and their strategic moves, manufacturing capabilities, IP investments, and collaborative efforts that shape competitive positioning. By bridging technological, clinical, and commercial dimensions, the report supports investment analysis, product development planning, and long‑term market forecasting with a holistic and data‑driven perspective.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 947.0 Million |

| Market Revenue (2033) | USD 3,677.1 Million |

| CAGR (2026–2033) | 18.48% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Abbott Laboratories, Biotronik SE & Co. KG, Cochlear Limited, Medtronic plc, EBR Systems, Inc., NeuroPace Inc., Pixium Vision, Profusa Inc., Second Sight Medical Products Inc., Stimwave Technologies Inc., CELTRO, Intelligent Implants, Exactech, MED‑EL, Neuralink, Paradromics, Precision Neuroscience, Blackrock Neurotech |

| Customization & Pricing | Available on Request (10% Customization Free) |