Reports

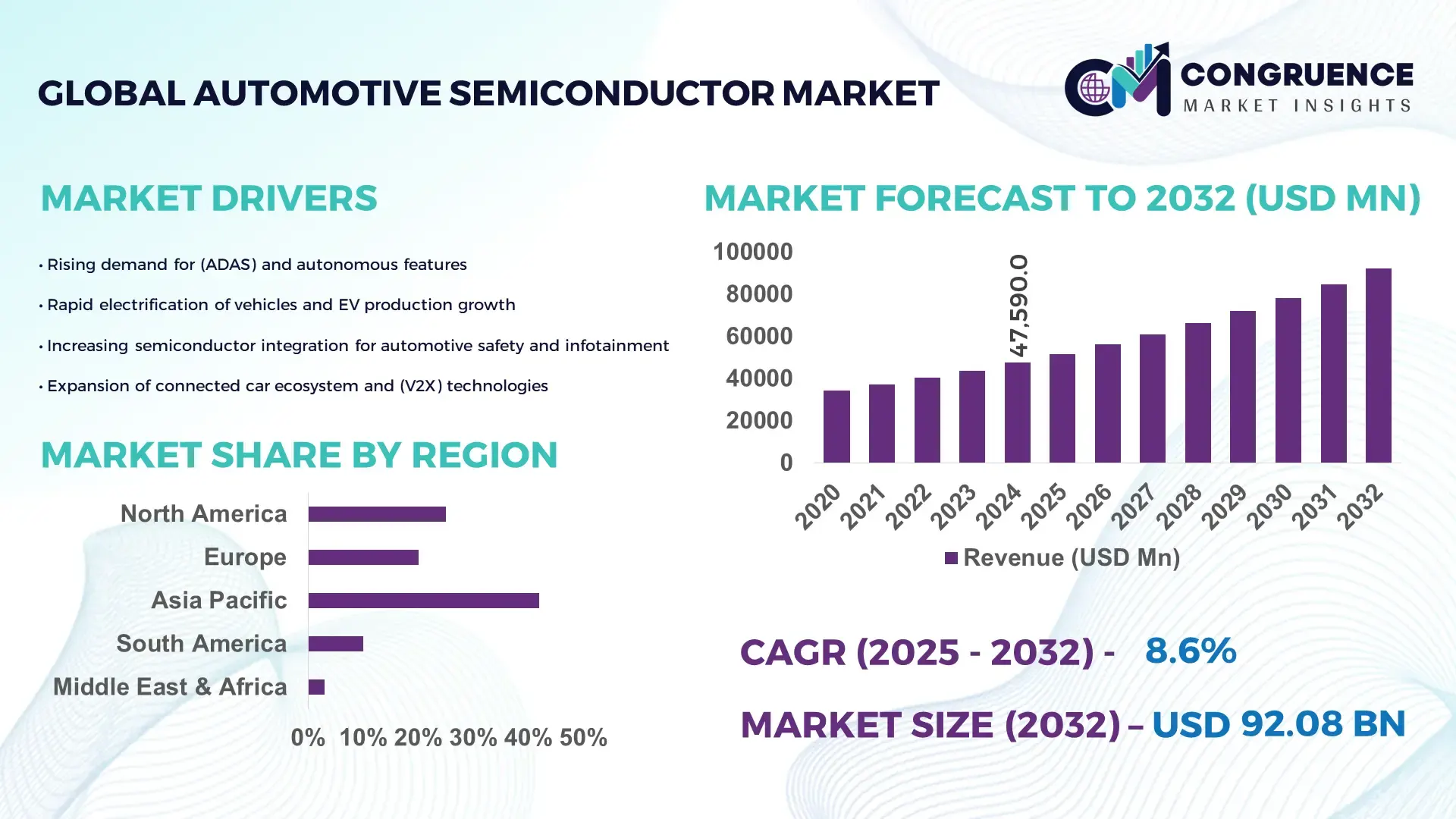

The Global Automotive Semiconductor Market was valued at USD 47,590 Million in 2024 and is anticipated to reach a value of USD 92,077 Million by 2032 expanding at a CAGR of 8.6% between 2025 and 2032. This growth is supported by rapid electrification, advanced driver-assistance deployment, and rising vehicle intelligence requirements.

Japan maintains a leading position in the automotive semiconductor landscape owing to its advanced production ecosystem, housing more than 30 high-capacity fabrication facilities dedicated to power electronics, microcontrollers, and sensor ICs. The country invested over USD 10 Billion in automotive chip R&D between 2022 and 2024, with manufacturers producing over 2.5 Billion automotive-grade chips annually used in ADAS, EV battery systems, and autonomous navigation modules. Japan’s automotive OEMs integrate semiconductors at an average rate of 27% higher than the global adoption benchmark, driven by expanded utilization in thermal management, safety control units, and next-generation EV platforms.

Automotive semiconductors are experiencing substantial growth across sectors such as driver assistance systems, EV powertrains, infotainment, and vehicle connectivity, each contributing between 18% and 30% to total semiconductor demand. Recent innovations include high-efficiency SiC MOSFETs, zonal architecture processors, and advanced sensing ICs that optimize data throughput and enhance system-level safety. Regulatory pressures on emissions and vehicle safety are accelerating adoption across Europe and Asia, while global consumption patterns show EV manufacturers increasing semiconductor utilization by over 40% per unit. Emerging trends such as vehicle central computing platforms, enhanced cybersecurity hardware, and energy-efficient semiconductor materials are shaping long-term market direction, supporting rapid adoption across developed and emerging economies.

The strategic relevance of the Automotive Semiconductor Market is anchored in its central role in electrification, advanced driver-assistance systems, connected mobility, and vehicle intelligence. The shift toward domain and zonal architecture is accelerating semiconductor density per vehicle, with next-generation processors enabling up to 38% faster data throughput than legacy distributed systems. Comparative benchmarks show silicon carbide (SiC) power modules delivering a 22% efficiency improvement compared to traditional silicon-based IGBTs, strengthening their adoption across EV inverters and fast-charging platforms. Regionally, Asia-Pacific dominates in volume, while Europe leads in adoption with 61% of enterprises integrating automotive-grade AI controllers for safety and emissions compliance.

By 2027, AI-enabled predictive control systems are expected to improve battery thermal management accuracy by 25%, cutting failure risks and extending EV operational lifespan. ESG commitments are also reshaping OEM strategies, with firms committing to 30% lifecycle emissions reduction through semiconductor energy-efficiency enhancements and materials recycling by 2030. In 2024, Japan achieved a 19% reduction in inverter switching losses through a nationwide SiC optimization initiative, demonstrating measurable gains from coordinated R&D investments.

Forward-looking strategies prioritize high-integration chips, autonomous-driving SoCs, cybersecurity hardware modules, and scalable power electronics, positioning the Automotive Semiconductor Market as a pillar of long-term resilience, regulatory alignment, and sustainable mobility expansion across global automotive supply chains.

The growing penetration of electrified and intelligent vehicles is significantly amplifying demand within the Automotive Semiconductor Market. Electrified powertrains require advanced power devices, microcontrollers, and thermal management ICs, with EVs using up to 70% more semiconductor content than internal combustion vehicles. The rapid acceleration of ADAS and autonomous functions also fuels the need for high-performance SoCs, image sensors, radar processors, and communication chipsets. Over 58% of new global vehicle models launched in 2023 integrated ADAS L2 or higher, directly increasing semiconductor consumption across safety and perception systems. The rising deployment of smart cockpits, vehicle-to-everything communication modules, and battery management systems further strengthens overall chip usage. These developments create a sustained uplift in semiconductor demand across EV, hybrid, and connected vehicle categories, reinforcing the market’s structural growth trajectory.

The Automotive Semiconductor Market faces limitations stemming from intricate global supply chains, high material dependencies, and extended lead times for critical components. Automotive-grade semiconductor fabrication often requires specialized production lines with qualification cycles extending up to 18 months, causing delays in capacity expansion. Material constraints in substrates such as SiC wafers, where global production remains limited to a few suppliers, create bottlenecks that slow broad-based adoption. Manufacturers encountered average lead times of 26–40 weeks for key microcontrollers and power modules during 2023–2024, impacting OEM production planning. Additionally, geopolitical disruptions, export controls, and regional manufacturing imbalances complicate logistics, raising procurement risks for automotive tiers. These structural challenges collectively restrain responsiveness and scalability across global automotive semiconductor supply chains.

Emerging technological advancements present significant opportunities for the Automotive Semiconductor Market, particularly across autonomous driving, connected mobility, and efficient power electronics. Growing adoption of L3–L4 automation is driving demand for high-performance compute platforms, with autonomous processors expected to increase computational density by 30% by 2028. Expansion of EV fleets fuels the need for SiC and GaN-based power devices, which enable faster charging and reduced thermal losses. Connected vehicle ecosystems also create opportunities, with 5G-enabled telematics units projected to exceed 280 million installations by 2027. Additional growth avenues include cybersecurity semiconductor modules, zonal vehicle architecture controllers, and advanced sensor fusion ICs. Together, these innovations open substantial pathways for suppliers and OEMs seeking long-term technological differentiation.

The Automotive Semiconductor Market faces significant challenges stemming from strict regulatory frameworks, rising R&D expenditures, and uncompromising quality standards for automotive-grade components. Safety and emissions regulations across Europe, North America, and Asia mandate rigorous compliance testing, often exceeding 1,000 hours of environmental and functional validation per chip type. These extended qualification demands increase both cost and time-to-market for suppliers. Furthermore, advanced fabrication for materials like SiC and GaN requires high-capital equipment and specialized engineering expertise, elevating R&D spending for next-generation devices. Cybersecurity mandates introduced for connected vehicles also necessitate hardware-based security modules, adding complexity to design cycles. Collectively, these pressures challenge cost efficiency, development timelines, and operational flexibility across global semiconductor producers.

• Acceleration of SiC and GaN Power Device Adoption: The Automotive Semiconductor market is witnessing rapid integration of silicon carbide and gallium nitride devices, driven by their superior efficiency metrics. SiC inverters now deliver up to 28% lower switching losses compared to silicon components, while GaN-based onboard chargers achieve nearly 22% faster charging performance. Over 6 million EVs produced in 2024 incorporated at least one SiC module, marking a 41% year-on-year adoption increase. This shift is boosting high-voltage platform efficiency and enabling compact, thermally optimized architectures across next-generation EV designs.

• Growth of Zonal and Centralized Vehicle Computing Platforms: Automotive OEMs are accelerating the move from distributed ECUs to zonal computing, resulting in a measurable reduction in hardware complexity. Zonal architectures cut wiring length by up to 35% and reduce component count by nearly 18%, improving reliability and lowering integration costs. In 2024, more than 27% of newly launched global vehicle models incorporated a partial or full zonal framework. This transition increases demand for high-throughput processors, advanced memory modules, and integrated communication ICs capable of supporting software-defined mobility ecosystems.

• Surge in ADAS Sensor Fusion and Edge AI Processing: Advanced driver-assistance systems are creating a sharp rise in semiconductor density per vehicle. Vehicles with L2+ capabilities use an average of 14–20 sensing units, representing a 52% increase compared to vehicles equipped with basic L1 systems. Edge AI accelerators embedded in sensor fusion processors enhance real-time decision-making by 30–40%, reducing latency to under 10 ms for perception and prediction tasks. The expanding deployment of radar-on-chip and vision SoCs is reinforcing demand for high-precision, power-efficient semiconductor solutions.

• Expansion of Semiconductor Content in Electrified Powertrains: Electrified vehicle platforms continue to increase semiconductor consumption, with EVs integrating up to 3,000 chips—nearly 65% more than traditional combustion vehicles. Battery management systems alone require between 120 and 150 dedicated semiconductor components per vehicle, reflecting growing emphasis on safety, thermal regulation, and energy optimization. In 2024, global production of intelligent power modules rose by 29%, supporting higher energy density and improved drivetrain efficiency. This trend underscores the critical role of advanced power electronics in enabling long-range, high-performance electric mobility.

The Automotive Semiconductor Market is segmented across types, applications, and end-user groups, each reflecting specific technology needs and adoption patterns. Types include microcontrollers, power semiconductors, sensors, memory devices, and integrated circuits that collectively support electrification, automation, and connectivity. Application segmentation spans ADAS, powertrain electronics, body electronics, infotainment, and vehicle networking systems. End-user insights highlight strong demand from OEMs, tier-1 suppliers, EV manufacturers, and aftermarket integrators, each relying on semiconductors to enhance efficiency, safety, and digital capabilities. Across segments, adoption continues to rise due to increasing semiconductor content per vehicle, which now exceeds 1,000 units for ICE platforms and up to 3,000 units for EVs, strengthening the structural demand base.

Microcontrollers (MCUs) represent the leading type in the Automotive Semiconductor Market, accounting for approximately 37% of total adoption driven by their essential role in ADAS, battery management, braking systems, and infotainment controls. Their dominance is supported by the growing integration of multi-core architectures and enhanced processing capabilities. Power semiconductors follow closely, capturing around 28% due to increased use of SiC and GaN devices in EV inverters, onboard chargers, and high-voltage components. In contrast, sensors hold a 25% share, with rapid growth in radar, camera, ultrasonic, and LiDAR sensing units supporting autonomous and safety functionalities.

The fastest-growing category is power semiconductors, expanding at an estimated 11% CAGR, accelerated by a shift toward vehicle electrification and high-efficiency power conversion systems. Sensors and memory devices contribute the remaining 10% combined share, serving niche but critical applications in data logging, thermal monitoring, and connectivity.

ADAS (Advanced Driver-Assistance Systems) represents the leading application segment, accounting for approximately 40% of total adoption due to rising deployment of L2–L3 autonomous features and increased sensor fusion requirements. Powertrain electronics follow with 27% share, supported by expanded electrification and high-voltage energy management needs. Infotainment and connectivity systems represent 22%, driven by growth in digital cockpits, real-time OS, and in-vehicle entertainment platforms. Body electronics and vehicle networking collectively contribute the remaining 11%, covering HVAC control modules, smart lighting, and gateway communication systems.

The fastest-growing application is powertrain electronics, advancing at an estimated 10% CAGR, supported by rising EV production, high-efficiency inverter designs, and thermal management optimization. ADAS adoption continues to accelerate as vehicles integrate an average of 15–20 sensing components, representing a 55% increase over earlier-generation systems.

OEMs (Original Equipment Manufacturers) are the leading end-user group, holding approximately 46% market share due to their high-volume production requirements and integration of semiconductors across safety, powertrain, and connectivity systems. Tier-1 suppliers follow with 32%, driven by their role in delivering subsystem-level electronics such as ADAS modules, infotainment platforms, and power electronics assemblies. EV manufacturers account for 18%, representing the fastest-growing end-user segment, expanding at an estimated 12% CAGR, fueled by high semiconductor density in electrified vehicle platforms. The remaining 4% consists of aftermarket players, fleet operators, and mobility service providers adopting semiconductor-based enhancements for operational efficiency.

Industry adoption rates show that more than 62% of global OEM platforms launched in 2024 integrated upgraded ADAS controllers, while 48% of EV manufacturers adopted high-performance SiC drive modules for enhanced efficiency. Tier-1 suppliers continue to influence technology innovation through integrated computing modules that reduce wiring complexity by up to 35%.

Asia-Pacific accounted for the largest market share at 46% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

The Asia-Pacific region maintained dominance due to its large EV production volume, exceeding 14 million units, supported by high semiconductor consumption across China, Japan, and South Korea. Europe contributed 28% of total demand, driven by stringent safety and emissions compliance requiring advanced semiconductor integration. North America accounted for 20%, with growing adoption in ADAS, connected mobility, and digital cockpit platforms. South America and Middle East & Africa collectively contributed 6%, supported by infrastructure modernization and increasing demand for vehicle electrification systems.

North America holds approximately 20% of the global Automotive Semiconductor Market, with strong demand originating from EV manufacturers, autonomous vehicle developers, and integrated fleet management platforms. Key industries driving semiconductor consumption include automotive OEMs, mobility service providers, and digital infrastructure operators. Regulatory frameworks such as advanced safety mandates and incentives for EV adoption continue to accelerate semiconductor integration in ADAS, battery systems, and vehicle communication modules. Notable advancements include high-performance computing chips enabling 30% faster autonomous processing within testing fleets. A key regional player recently expanded its semiconductor testing facility in the U.S., increasing validation capacity by 25%. Consumer behavior trends show higher enterprise adoption in finance and healthcare for connected fleet solutions, reinforcing rising semiconductor use in specialized mobility services.

Europe accounts for approximately 28% of the Automotive Semiconductor Market, driven by Germany, the UK, France, and Italy. The region exhibits strong demand due to strict Euro NCAP safety standards and environmental sustainability initiatives promoting electrified and low-emission vehicles. Adoption of emerging technologies such as SiC power modules and centralized vehicle computing continues to accelerate, with European OEMs integrating up to 20% more advanced processors in new EV platforms. A notable regional semiconductor manufacturer recently upgraded its production line to support 18% higher wafer output for automotive customers. Consumer behavior emphasizes regulatory compliance and demand for explainable and transparent semiconductor-enabled vehicle systems, strengthening uptake across autonomous, safety, and energy-efficient applications.

Asia-Pacific leads the Automotive Semiconductor Market with the highest volume output, contributing 46% of global consumption. China, Japan, and South Korea remain the top-consuming countries, collectively producing over 14 million EVs and integrating high semiconductor density across powertrain, sensing, and connectivity systems. Rapid advancements in fabrication infrastructure, including new 300mm wafer facilities, support scaling of SiC and GaN production. Regional innovation hubs in Japan and South Korea are accelerating adoption of autonomous processors and energy-optimized power modules, with integration rates increasing 35% year-on-year. A leading regional automotive electronics manufacturer introduced a next-generation ADAS sensor platform delivering 22% higher detection accuracy. Consumer behavior in Asia-Pacific is heavily influenced by mobile-first ecosystems, with growth driven by e-commerce-linked mobility apps and demand for connected vehicle features.

South America contributes roughly 4% to the global Automotive Semiconductor Market, with Brazil and Argentina representing the largest automotive production bases. Regional market share is supported by modernization of manufacturing facilities, increasing electrification efforts, and digital transformation across logistics and mobility services. Infrastructure developments, particularly in renewable energy and smart transportation, are driving the need for high-efficiency power semiconductors and robust communication chips. A local automaker introduced an EV pilot project integrating semiconductors that improved energy efficiency by 17% under regional conditions. Consumer behavior shows strong demand for media-rich infotainment and language-localized vehicle interfaces, reinforcing semiconductor usage in connectivity and display architectures.

The Middle East & Africa holds approximately 2% of the Automotive Semiconductor Market, with growth influenced by demand from oil & gas fleets, construction logistics, and emerging smart mobility programs. Countries such as the UAE, Saudi Arabia, and South Africa are accelerating digital transformation, prompting increased adoption of ADAS modules, vehicle telematics, and energy-efficient power devices. Regional modernization trends include investment in EV charging infrastructure and autonomous mobility pilots. A technology integrator in the UAE deployed connected vehicle control units that enhanced fleet monitoring accuracy by 23%. Consumer behavior reflects growing preference for digitally enabled automotive services, mobile-based vehicle tracking, and safety-enhancing semiconductor technologies.

China – 32% Market Share

Dominance driven by large EV production capacity and accelerated integration of power semiconductors and ADAS processors in domestic automotive platforms.

Japan – 18% Market Share

Leadership supported by advanced semiconductor fabrication infrastructure and strong OEM demand for high-reliability microcontrollers, sensors, and intelligent power modules.

The Automotive Semiconductor market is moderately consolidated, with more than 45 globally active competitors operating across power devices, MCUs, ADAS processors, sensor ICs, and memory components. The top five players collectively command an estimated 48–52% share, highlighting strong dominance by established semiconductor leaders. Competitive pressure intensified through 2023–2024 as companies expanded 200mm and 300mm automotive-grade wafer capacity, resulting in a 17% increase in output aimed at alleviating prior supply constraints.

Strategic partnerships continued to shape market positioning, with over 30 long-term supply and co-development agreements signed between semiconductor manufacturers and major OEMs/Tier-1 suppliers in 2024. Competition has also strengthened through technology-led differentiation, supported by more than 120 new automotive-grade product launches in the last 18 months, covering areas such as SiC MOSFETs, next-generation MCUs, integrated radar SoCs, and zonal controllers. M&A activity rose by nearly 22% during the same period as companies pursued portfolio expansion in electrification, autonomous systems, and cybersecurity modules.

Innovation intensity remains high, with nearly 60% of competitors increasing R&D allocations in 2024, reflecting average spending growth of 12–15%. Companies with vertically integrated supply chains, advanced packaging capabilities, and leadership in SiC/GaN platforms continue to strengthen their market positions. Overall, the competitive landscape is defined by rapid technology upgrades, expanded manufacturing footprints, and increased collaboration with automotive ecosystem partners.

Infineon Technologies

NXP Semiconductors

Renesas Electronics

STMicroelectronics

Texas Instruments

Robert Bosch GmbH (Semiconductor Division)

onsemi (ON Semiconductor)

Analog Devices

Rohm Semiconductor

Toshiba Electronic Devices & Storage Corporation

The Automotive Semiconductor market is undergoing a significant technology transformation driven by electrification, autonomous systems, and connected vehicle architectures. Power electronics remain one of the most critical domains, with a sharp rise in the adoption of silicon carbide (SiC) and gallium nitride (GaN) devices. SiC MOSFET penetration in electric vehicle inverters increased to nearly 38% in 2024, compared to just 22% in 2021, reflecting accelerated OEM demand for higher efficiency and thermal stability. GaN-based power switches are also gaining traction in onboard chargers and DC-DC converters, with shipments increasing by more than 28% year-over-year due to compact form factors and high switching frequencies. Microcontrollers (MCUs) and domain/zonal controllers are experiencing rapid upgrades as vehicles transition from distributed ECUs to consolidated architectures. In 2024, more than 55% of new vehicles integrated advanced 32-bit MCUs with enhanced cybersecurity modules, while the adoption of zonal controllers grew by 40% across premium vehicle platforms. This shift is reducing wiring harness weight by 70–90 kg per vehicle and enabling faster OTA software deployment cycles.

Sensor technologies, particularly radar, LiDAR, and camera-based systems, are also evolving quickly. Automotive radar chip shipments surpassed 210 million units in 2024, driven by increased ADAS installations and higher NCAP safety requirements. Camera sensors with AI-enabled ISP modules grew by 32%, supporting real-time object recognition, driver monitoring, and low-light imaging improvements. Memory and connectivity components are expanding in line with software-defined vehicle trends. Automotive-grade DRAM demand increased by more than 25% in 2024, while vehicle-to-everything (V2X) chipset installations rose by 18% as governments strengthened mandates for connected mobility. Collectively, these advancements position next-generation semiconductors as the core enablers of future automotive innovation and competitive differentiation.

In November 2024, Infineon and Stellantis signed supply and capacity reservations for PROFET™ smart power switches and CoolSiC™ silicon-carbide semiconductors, laying the foundation for next-generation 800 V EV power architectures.

In April 2024, NXP announced its first “super-integration” 5-nm automotive SoC, the S32N55, consolidating dozens of ECU functions into a single processor while supporting ISO 26262 safety levels up to ASIL D.

In November 2024, Renesas introduced its 3-nm R-Car X5H multi-domain SoC for software-defined vehicles, delivering up to 400 TOPS of AI performance and hardware isolation across ADAS, IVI, and gateway domains.

In December 2024, STMicroelectronics invested in Innoscience’s IPO to accelerate GaN semiconductor development, positioning itself strategically in energy-efficient power device supply for automotive applications.

The report on the Automotive Semiconductor Market encompasses a comprehensive evaluation of semiconductor types, including power devices (such as SiC and GaN MOSFETs), microcontrollers (MCUs), sensing ICs (radar, camera, LiDAR), memory components, and high-integration SoCs. It details application segments such as ADAS, powertrain electronics, infotainment, body electronics, and central compute platforms, offering insight into how chip demand is distributed across these use cases. The geographic scope covers major regions — Asia-Pacific, Europe, North America, South America, and Middle East & Africa — with country-level analyses of production capacity, consumption trends, and technology adoption.

On the technology front, the report explores innovations such as high-efficiency power semiconductors, 3-nanometer super-integration SoCs, zonal architecture controllers, and AI-enabled sensor fusion. It also maps out end users by OEMs, tier-1 suppliers, EV manufacturers, and mobility services, highlighting how different segments drive semiconductor consumption. Emerging or niche areas, including software-defined vehicle (SDV) architectures, central compute ECUs, domain controllers, and secure on-chip communication, are given special coverage. The report also considers supply-chain dynamics, capacity expansion, and strategic partnerships, offering decision-makers detailed insights into future investment needs, technology risk, and competitive positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 47590 Million |

|

Market Revenue in 2032 |

USD 92077 Million |

|

CAGR (2025 - 2032) |

8.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Infineon Technologies, NXP Semiconductors, Renesas Electronics, STMicroelectronics, Texas Instruments, Robert Bosch GmbH (Semiconductor Division), onsemi (ON Semiconductor), Analog Devices, Rohm Semiconductor, Toshiba Electronic Devices & Storage Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |