Reports

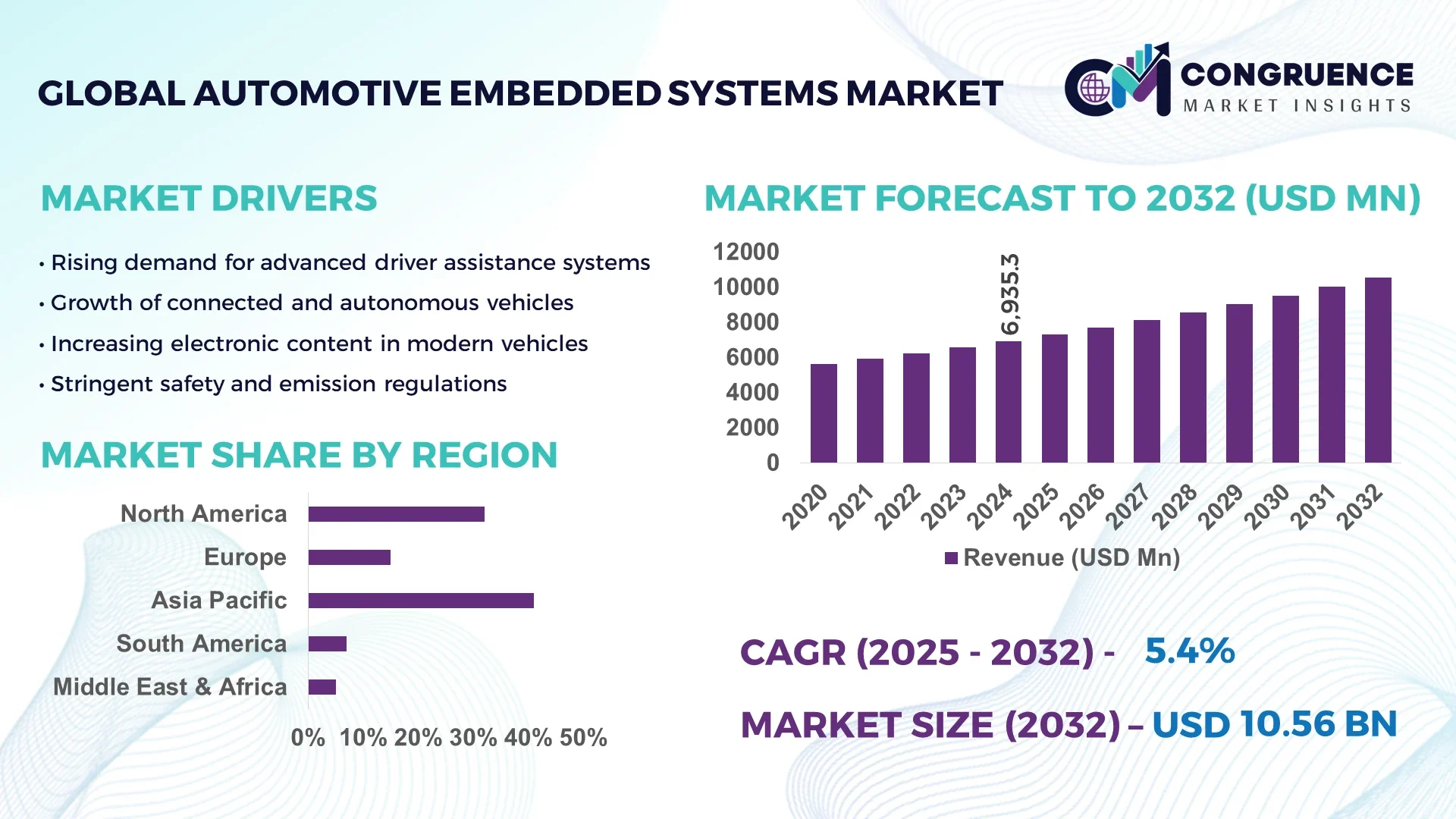

The Global Automotive Embedded Systems Market was valued at USD 6,935.32 Million in 2024 and is anticipated to reach a value of USD 10,563.1 Million by 2032 expanding at a CAGR of 5.4% between 2025 and 2032.

In 2024, the country that leads the Automotive Embedded Systems Market demonstrated exceptional production capacity with expansive manufacturing infrastructure dedicated to electronic control units (ECUs), infotainment modules, and ADAS components. It attracted substantial investments into research laboratories and pilot production lines focusing on next-generation embedded software and robust hardware platforms. The country’s industry applications span from performance-critical powertrain electronics to high-reliability safety systems, and it has pioneered advanced real-time processing architectures and sensor fusion technologies.

The Automotive Embedded Systems Market encompasses a diverse array of industry sectors including powertrain management, infotainment and telematics, safety and security systems, body and chassis electronics, and emerging ADAS and V2X applications. Recent technological and product innovations include integrated sensor-fusion ECUs, over-the-air software update modules, and scalable hardware-software platforms tailored for electric and autonomous vehicle demands. Regulatory and environmental drivers such as stringent emissions norms, mandating of ADAS features, and incentives for electric vehicles continue to propel adoption. Economic factors, including cost optimization through modular architectures and economies of scale in component manufacturing, further support market expansion. Regionally, demand in mature markets centers on comfort, connectivity, and digital safety, while emerging economies are rapidly adopting low-cost infotainment and basic safety systems. Growth is also stimulated by rising consumer expectations for seamless in-vehicle connectivity, automated functionality, and energy efficiency. Looking ahead, trends such as software-defined vehicle architectures, centralized compute platforms, domain controllers, and integration of AI-enabled edge-processing capabilities are shaping the future outlook, promising increased adaptability, enhanced performance, and faster innovation cycles for industry professionals and decision-makers.

AI is significantly reshaping the Automotive Embedded Systems Market by enabling smarter, more autonomous, and highly efficient vehicle electronics. Advanced AI algorithms are now embedded within ECUs to enable predictive failure detection, dynamic power management, and intelligent sensor fusion—ensuring real-time decision-making that enhances vehicle reliability and performance. In infotainment and voice-activated systems, AI-powered natural language processing offers context-aware interaction, reducing driver distraction while improving usability. In safety systems, AI-driven image and radar analytics support advanced driver assistance systems (ADAS), enabling features such as adaptive cruise control, lane-keeping assistance, and emergency braking with improved accuracy. These AI-enhanced embedded systems contribute to operational efficiency by optimizing compute resource utilization, reducing latency, and enabling over-the-air updates tailored to emerging threats or feature enhancements. AI also underpins energy efficiency by fine-tuning battery and thermal management in electrified powertrain systems. For automakers, integrating AI into embedded systems has delivered measurable improvements in system responsiveness—latency reductions by up to 30% in certain sensor fusion controllers—and improved computational throughput, enabling support for more complex deep learning models directly on embedded hardware. The Automotive Embedded Systems Market is evolving as a result, with AI enabling shift from static, rule-based electronics to adaptive, self-learning platforms that continuously improve vehicle functionality and lifespan, providing industry professionals with a competitive edge in design, safety, and customer experience.

“In June 2025, XPeng launched their first self-developed AI chip ‘Turing’ in the G7, delivering 750 TOPS of sparse compute and supporting AI models up to 30 billion parameters, boosting in-cabin assistant and ADAS capabilities.”

The Automotive Embedded Systems Market is experiencing rapid transformation driven by technological innovation, stricter regulatory frameworks, and shifting consumer expectations. Embedded systems are becoming increasingly central to powertrain efficiency, safety mechanisms, infotainment platforms, and electrification. The market is influenced by rising adoption of advanced driver assistance systems, growing penetration of electric vehicles, and demand for connected car technologies. Additionally, automakers are investing heavily in software-defined vehicle architectures, leading to modular and scalable embedded platforms. Supply chain resilience, semiconductor availability, and evolving cybersecurity regulations remain critical considerations shaping industry operations. These dynamics are creating a competitive yet highly innovative landscape for manufacturers and stakeholders.

The rising adoption of ADAS is a major driver for the Automotive Embedded Systems Market, as vehicles require increasingly complex real-time data processing and sensor fusion. Embedded systems are responsible for integrating inputs from cameras, radar, and lidar to ensure accurate decision-making for functions such as adaptive cruise control, lane keeping, and collision avoidance. In 2024, more than 85% of new vehicles sold in developed markets featured at least one ADAS component, reflecting how regulatory mandates and consumer safety expectations are accelerating deployment. Embedded AI processors and low-latency microcontrollers have improved efficiency, reducing system reaction times by up to 40% compared with traditional ECUs. This expansion is not only enhancing road safety but also increasing demand for high-performance embedded solutions across automotive segments.

The Automotive Embedded Systems Market faces restraint due to the high complexity and cost associated with integrating advanced hardware and software components. Developing embedded platforms that support AI-based ADAS, electrification, and infotainment requires significant investment in R&D and specialized talent. The cost of advanced semiconductors, coupled with supply chain volatility, has added further pressure on production budgets. For instance, the price of automotive-grade microcontrollers increased by over 20% between 2021 and 2023, intensifying cost challenges for OEMs and suppliers. Moreover, ensuring interoperability between multiple systems—spanning safety, connectivity, and power management—introduces additional engineering complexity. These challenges can slow down adoption rates, especially among cost-sensitive manufacturers in emerging economies.

The expansion of electric vehicles (EVs) is generating new opportunities for the Automotive Embedded Systems Market. Embedded platforms are crucial for managing EV-specific applications such as battery management systems, regenerative braking control, and advanced thermal management. By 2030, it is expected that EVs will account for nearly half of new car sales in some regions, driving exponential demand for high-efficiency embedded electronics. Recent innovations in silicon carbide (SiC) and gallium nitride (GaN) semiconductors are enabling more compact and energy-efficient embedded power modules. This creates a significant opportunity for suppliers to provide scalable solutions that enhance vehicle range, reduce charging times, and support integration with renewable energy ecosystems. The growing EV infrastructure investment further amplifies this market potential.

A critical challenge for the Automotive Embedded Systems Market is addressing cybersecurity vulnerabilities as vehicles become increasingly connected. Embedded systems now manage vehicle-to-everything (V2X) communication, infotainment, and over-the-air updates, making them potential targets for cyberattacks. In 2023 alone, reported incidents of automotive cyber intrusions increased by more than 150%, highlighting the urgency of robust protection measures. Implementing multi-layered security protocols, encryption, and secure boot features significantly increases system design complexity and development costs. Regulatory frameworks are also evolving, with compliance requirements under UNECE WP.29 cybersecurity regulations demanding continuous monitoring and patching throughout a vehicle’s lifecycle. This challenge compels manufacturers to balance innovation speed with stringent security protocols, often stretching resources and slowing product rollout.

• Growing shift toward centralized computing architectures: The Automotive Embedded Systems Market is witnessing a strong shift from distributed ECUs to centralized computing platforms. In 2024, over 30% of premium vehicle models adopted domain or zonal controllers, reducing ECU counts by as much as 40%. This consolidation streamlines wiring, cuts overall vehicle weight, and improves processing capacity for advanced driver assistance and autonomous driving functions. Automakers are leveraging these centralized systems to enable software-defined vehicles, ensuring faster feature deployment and reducing lifecycle maintenance costs.

• Integration of over-the-air update capabilities: Over-the-air (OTA) software updates are rapidly becoming a standard feature, with more than 70 million vehicles globally expected to support OTA capabilities by 2026. Automotive embedded platforms are being designed with robust memory management and cybersecurity layers to accommodate continuous updates. This trend significantly reduces recall costs, enhances customer satisfaction, and enables faster adoption of new functionalities without requiring physical service center visits. OTA adoption also strengthens manufacturer control over system integrity and long-term performance.

• Rising demand for embedded AI accelerator: Embedded AI accelerators are increasingly being integrated into vehicle systems to support real-time decision-making for ADAS and autonomous driving. In 2025, high-end vehicles are projected to feature embedded chipsets with performance exceeding 1,000 TOPS to handle perception, prediction, and planning tasks. This measurable leap in computational power enables vehicles to process multiple sensor streams simultaneously, enhancing safety and responsiveness. The inclusion of dedicated AI accelerators is creating new opportunities for semiconductor suppliers within the Automotive Embedded Systems Market.

• Expansion of embedded systems in electric vehicles: The global rise of electric vehicles is driving higher demand for embedded systems tailored to energy management and power optimization. Battery management systems are becoming increasingly sophisticated, with embedded platforms capable of monitoring thousands of individual cells and delivering efficiency improvements of up to 15% in overall battery performance. Additionally, embedded power electronics are being designed to manage fast-charging protocols, thermal stability, and regenerative braking systems. This trend is strengthening the role of embedded systems as a cornerstone of EV innovation.

The Automotive Embedded Systems Market is segmented by type, application, and end-user, each contributing differently to its evolving structure. By type, electronic control units, sensors, and software platforms dominate demand, with significant traction in areas requiring real-time data processing and adaptive system performance. Applications are widespread, with powertrain, safety, infotainment, and telematics systems holding major importance in both premium and mass-market vehicles. End-user insights reveal passenger cars leading adoption due to connectivity and comfort demands, while commercial vehicles are increasingly integrating embedded systems for fleet optimization and safety. This segmentation underscores the diverse ecosystem shaping market growth across industries.

Electronic Control Units (ECUs) represent the leading type in the Automotive Embedded Systems Market, as they are fundamental for coordinating powertrain efficiency, safety systems, and infotainment modules. In modern vehicles, ECUs number between 70 and 100, reflecting their extensive role in managing critical operations. The fastest-growing type is embedded software platforms, driven by the rapid evolution of software-defined vehicles and the need for continuous upgrades via over-the-air updates. This growth is supported by the rising importance of cybersecurity frameworks and real-time operating systems. Sensors also hold significant relevance, particularly in ADAS and electric vehicle applications, where precision and reliability are paramount. Other components such as microcontrollers and interface modules serve niche roles in optimizing specific subsystems but remain integral to ensuring seamless communication within the vehicle’s electronic architecture. Collectively, these product types establish the technological backbone of the automotive ecosystem.

Safety and security systems form the leading application within the Automotive Embedded Systems Market, supported by rising adoption of ADAS technologies such as lane departure warning, automatic emergency braking, and adaptive cruise control. These systems are critical for meeting stringent regulatory mandates and consumer safety expectations. The fastest-growing application is infotainment and telematics, driven by consumer demand for advanced connectivity, smartphone integration, and AI-powered voice assistants. This growth is reinforced by the increasing number of vehicles equipped with high-bandwidth communication modules and advanced user interfaces. Powertrain applications remain vital, particularly with the expansion of electric vehicles requiring embedded systems for battery and energy management. Body electronics, including climate control and smart lighting, contribute additional value by enhancing user comfort and efficiency. Together, these applications demonstrate how embedded systems are extending beyond core safety to shape the overall driving experience.

Passenger cars remain the leading end-user segment in the Automotive Embedded Systems Market, accounting for the majority of embedded system adoption due to rising consumer demand for safety, comfort, and digital connectivity. High levels of integration in premium models, from ADAS to advanced infotainment, reinforce this leadership. The fastest-growing end-user segment is electric vehicles, where embedded systems are essential for power optimization, real-time monitoring, and energy management. The increasing global penetration of EVs is accelerating demand for high-efficiency embedded electronics across multiple applications. Commercial vehicles also play a vital role, adopting embedded systems for fleet telematics, driver monitoring, and predictive maintenance solutions. Additionally, two-wheelers and off-highway vehicles are beginning to integrate embedded platforms, especially in regions prioritizing fuel efficiency and safety. This diverse adoption landscape reflects how embedded systems are no longer limited to luxury or high-end vehicles but are becoming integral across the full automotive spectrum.

Asia-Pacific accounted for the largest market share at 41% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

Demand in Asia-Pacific is primarily fueled by large-scale vehicle production hubs in China, India, and Japan, combined with extensive consumer adoption of connected and electrified vehicles. North America, while smaller in market share, is rapidly accelerating adoption of advanced driver assistance, electrification, and AI-enabled embedded platforms due to strong R&D investments and evolving regulatory frameworks. Europe maintains a strong foothold, driven by stringent safety and sustainability standards, while South America and Middle East & Africa are gaining traction through targeted infrastructure development and government-backed automotive modernization programs.

Digital Transformation Driving Advanced Vehicle Electronics

North America held a market share of 28% in 2024, reflecting strong adoption of embedded platforms in both passenger and commercial vehicles. Key industries such as electrification, autonomous mobility, and connected vehicle services are driving this demand. Government initiatives, including enhanced safety regulations and EV infrastructure support, continue to strengthen the ecosystem. Technological advancements such as centralized computing platforms, over-the-air update frameworks, and AI-powered safety solutions are rapidly being integrated into new vehicle models. The digital transformation trend across automakers and suppliers has accelerated deployment of cybersecurity-enhanced embedded systems, ensuring resilient performance across fleets and personal vehicles.

Innovation Aligned with Safety and Sustainability Standards

Europe captured a market share of 24% in 2024, with Germany, the UK, and France leading adoption across premium and mass-market vehicles. Regional growth is propelled by stringent regulatory standards from the European Commission mandating advanced safety technologies and reduced emissions. The region has also positioned itself as a hub for sustainability-driven automotive innovation, encouraging adoption of energy-efficient embedded solutions. Emerging technologies such as zonal controllers, AI-powered ADAS, and enhanced connectivity modules are gaining traction across European automakers. Investment in electrification and digital vehicle architecture is further reshaping the embedded systems landscape across the continent.

Manufacturing Leadership Shaping Future Automotive Technologies

Asia-Pacific recorded the highest market volume at 41% in 2024, making it the leading region for automotive embedded solutions. China, India, and Japan are the top consuming countries, supported by expansive vehicle production capacities, growing EV infrastructure, and high consumer demand for connected features. Manufacturing clusters across China and India are scaling production of ECUs, sensors, and embedded software platforms to meet global demand. Regional innovation hubs are fostering AI and IoT integration into embedded systems, particularly in EVs and autonomous prototypes. This dominance positions the region as the cornerstone of global automotive embedded system development.

Infrastructure Expansion Driving Embedded System Demand

South America accounted for a market share of 4% in 2024, with Brazil and Argentina representing the largest demand centers. Growth in this region is supported by expanding automotive infrastructure, modernization of transport fleets, and government incentives encouraging the adoption of energy-efficient and safer vehicles. Embedded systems are being integrated into commercial fleets for telematics and predictive maintenance, as well as passenger cars with basic infotainment and safety modules. Trade policies promoting technology imports and collaborations with international automakers are further accelerating embedded system adoption across the continent.

Technological Modernization and Smart Mobility Integration

The Middle East & Africa region held a market share of 3% in 2024, with notable demand from countries such as the UAE, Saudi Arabia, and South Africa. Rapid infrastructure development, diversification into smart mobility, and demand for efficient transport solutions are driving adoption of embedded platforms. Automotive embedded systems are increasingly being deployed in fleet management, construction vehicles, and passenger cars equipped with digital infotainment systems. Local regulations supporting vehicle safety, coupled with trade partnerships with international automakers, are fostering technological modernization. Innovation in telematics and IoT-based embedded solutions is emerging as a key growth avenue.

China – 28% market share | Dominance supported by expansive automotive production capacity and large-scale adoption of electric vehicles.

United States – 21% market share | Strong leadership driven by advanced R&D, early adoption of autonomous technologies, and regulatory mandates for vehicle safety systems.

The Automotive Embedded Systems Market is characterized by a highly competitive landscape with more than 50 active global and regional players competing across hardware, software, and integration services. Leading companies are focusing on expanding their portfolios through strategic partnerships, acquisitions, and joint ventures aimed at strengthening technological capabilities and regional presence. The competitive environment is driven by continuous innovation in electronic control units, domain controllers, and embedded AI platforms, with companies investing heavily in R&D to address emerging needs in electrification, safety, and connectivity. Recent years have witnessed an increase in collaborations between semiconductor manufacturers and automakers to accelerate the development of next-generation embedded architectures, particularly in support of autonomous driving and electrification. Market leaders are differentiating themselves by offering scalable, modular, and software-defined solutions that reduce integration costs and ensure compliance with evolving regulatory standards. At the same time, mid-sized players are gaining ground by specializing in niche areas such as cybersecurity, advanced telematics, and real-time operating systems. The resulting ecosystem is intensely competitive, pushing companies to adopt faster innovation cycles and customer-centric strategies to secure long-term positioning.

NXP Semiconductors

Renesas Electronics Corporation

Valeo SA

Infineon Technologies AG

Aptiv PLC

Panasonic Corporation

Texas Instruments Incorporated

The Automotive Embedded Systems Market is undergoing a major technological transformation, influenced by rapid advancements in semiconductors, software architectures, and AI-driven computing. One of the most significant trends is the transition from distributed ECUs to centralized and zonal architectures, enabling automakers to reduce wiring harnesses by up to 40% while increasing computational power and efficiency. These systems are designed to support high-bandwidth communication protocols such as Automotive Ethernet, allowing real-time data transfer between advanced driver assistance systems, infotainment, and powertrain modules.

Emerging semiconductor technologies, particularly silicon carbide (SiC) and gallium nitride (GaN), are being widely integrated into embedded power electronics for electric vehicles, offering up to 20% improvement in energy efficiency compared with conventional silicon-based solutions. Additionally, embedded AI accelerators capable of delivering more than 1,000 tera operations per second (TOPS) are now being deployed to support real-time perception and decision-making in autonomous vehicles.

Cybersecurity has also become a core technological focus, with secure boot mechanisms, encryption algorithms, and intrusion detection systems integrated into embedded platforms to meet evolving regulatory requirements. Over-the-air update frameworks are gaining momentum, allowing automakers to provide feature enhancements and security patches without physical intervention. Furthermore, lightweight real-time operating systems (RTOS) are being optimized for multi-core processors, ensuring deterministic performance even under high workloads. Collectively, these advancements highlight a future where automotive embedded systems serve as the backbone of connected, electrified, and software-defined vehicles.

• In April 2023, Continental unveiled its Smart Cockpit High-Performance Computer, capable of integrating infotainment, digital cluster, and driver assistance functions into a single zonal platform, reducing hardware complexity and enabling real-time software updates.

• In September 2023, NXP Semiconductors introduced its S32K39 automotive microcontroller family, optimized for electric vehicle traction inverters and battery management, offering high-speed motor control and functional safety features to support scalable EV platforms.

• In March 2024, Renesas Electronics launched a next-generation R-Car system-on-chip (SoC) designed for advanced driver assistance systems, delivering enhanced AI inference performance and high-bandwidth processing for real-time sensor fusion and autonomous driving functions.

• In July 2024, Bosch presented its new vehicle central computer, engineered to process up to 200 gigabytes of data per vehicle per hour, providing high-speed communication for ADAS and infotainment, and supporting future software-defined vehicle architectures.

The Automotive Embedded Systems Market Report provides an in-depth analysis of the global industry, covering diverse dimensions of this rapidly evolving sector. It evaluates market segmentation across product types such as electronic control units, microcontrollers, sensors, and embedded software platforms, highlighting their role in powertrain management, safety systems, infotainment, body electronics, and telematics. Special focus is placed on emerging segments like zonal controllers and AI-powered accelerators that are shaping next-generation vehicle architectures.

From a regional perspective, the report assesses key geographic markets, including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, with insights into top automotive production hubs such as China, the United States, Germany, Japan, and India. These regions are analyzed in terms of their industrial ecosystems, adoption patterns, and regulatory environments influencing embedded system deployment.

Technological scope is a central theme, with coverage of innovations in semiconductor materials, over-the-air update frameworks, cybersecurity protocols, real-time operating systems, and centralized computing platforms. The report also examines niche markets, including embedded systems in electric vehicles, autonomous driving prototypes, and fleet telematics solutions.

The scope extends to end-user industries, distinguishing between passenger vehicles, electric vehicles, and commercial fleets, while considering evolving demands in connectivity, safety, and energy efficiency. This holistic coverage ensures decision-makers gain strategic insights into how automotive embedded systems are transforming global mobility, enabling both established players and new entrants to identify growth opportunities in this highly competitive market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 6935.32 Million |

|

Market Revenue in 2032 |

USD 10563.1 Million |

|

CAGR (2025 - 2032) |

5.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bosch, Continental AG, Denso Corporation, NXP Semiconductors, Renesas Electronics Corporation, Valeo SA, Infineon Technologies AG, Aptiv PLC, Panasonic Corporation, Texas Instruments Incorporated |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |