Reports

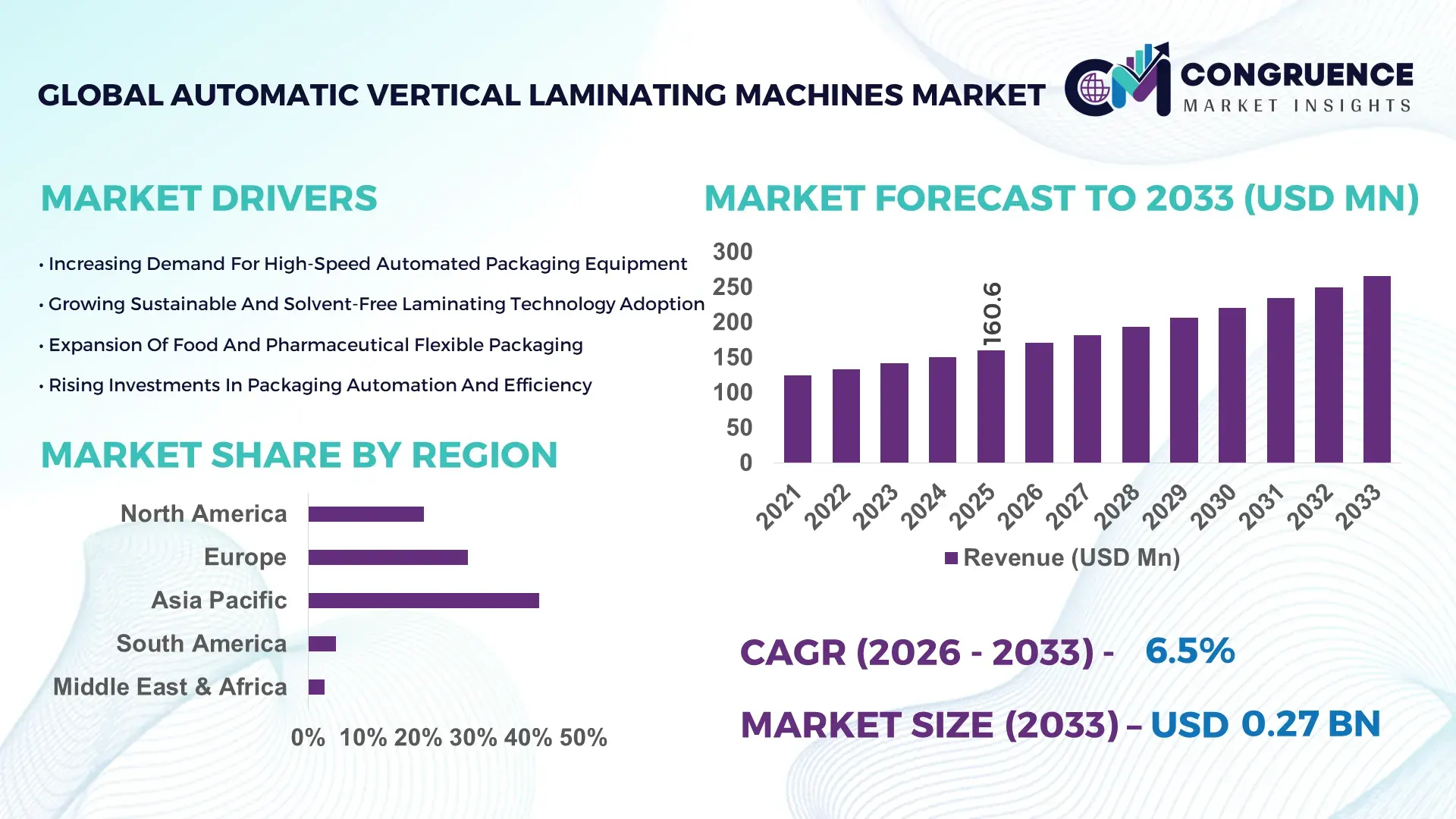

The Global Automatic Vertical Laminating Machines Market was valued at USD 160.6 Million in 2025 and is anticipated to reach a value of USD 265.8 Million by 2033 expanding at a CAGR of 6.5% between 2026 and 2033.

Growth is accelerating due to rapid shift toward high-speed, automated flexible packaging systems that improve lamination precision by over 28% while reducing material waste by nearly 20%. Between 2024 and 2026, global packaging supply chains have restructured amid geopolitical trade realignments and rising labor costs, forcing manufacturers to localize production and automate processes at scale.

China dominates the Automatic Vertical Laminating Machines market with approximately 35% global production capacity and over 30% of installed systems across packaging facilities. Investments exceeding USD 400 million in packaging automation between 2023 and 2025 have enabled more than 62% of large-scale plants to adopt automated laminating systems, improving throughput efficiency by 25%. Compared to Europe’s 27% share in advanced installations, China operates at 1.4x higher deployment scale, particularly in food packaging sectors exceeding 100 million tons annually.

This dominance signals that global players must align manufacturing with Asia-Pacific while differentiating through automation and sustainability in developed markets to remain competitive.

Market Size & Growth: USD 160.6M (2025) to USD 265.8M (2033), CAGR 6.5%, driven by automation-led packaging transformation.

Top Growth Drivers: Automation adoption (48%), flexible packaging demand (42%), labor cost pressure (36%).

Short-Term Forecast: By 2028, lamination efficiency improves by 24% while downtime reduces by 19%.

Emerging Technologies: AI-based control, solvent-free lamination, IoT-enabled monitoring systems.

Regional Leaders: Asia-Pacific USD 120M, Europe USD 80M, North America USD 65M by 2033 with strong automation trends.

Consumer Trends: 59% of packaging firms prioritize high-speed automated laminating solutions.

Pilot Example: In 2025, a packaging plant improved output efficiency by 26% using automated laminators.

Competitive Landscape: Nordmeccanica leads ~26%, followed by Bobst, Comexi, Uteco, DCM.

Regulatory & ESG: Solvent-free systems reduced emissions by 23% in regulated markets.

Investment Trends: USD 520M invested globally (2023–2025) in automation and sustainable packaging tech.

Innovation Outlook: Smart factory integration and digital twins reshaping production optimization.

Food packaging contributes approximately 63% of demand, followed by pharmaceuticals at 20% and industrial laminates at 17%. AI-based process control improves precision by 26%, while solvent-free systems reduce emissions by 23%. Asia-Pacific drives volume demand, Europe leads sustainability compliance, and North America advances automation adoption. Supply chain localization is accelerating equipment upgrades, with smart laminating systems emerging as the next competitive frontier shaping future manufacturing strategies.

The Automatic Vertical Laminating Machines market is rapidly becoming a strategic investment priority as packaging manufacturers transition toward high-speed, precision-driven operations where efficiency directly impacts margins and scalability. Over 61% of large packaging facilities are upgrading to automated laminating systems, signaling a decisive shift from manual processes to digitally optimized production environments. Rising labor costs and supply chain disruptions between 2024 and 2026 are forcing manufacturers to accelerate automation investments, reshaping operational models across global packaging ecosystems.

AI-enabled laminating systems improve process efficiency by 30% while reducing material waste by 22% compared to legacy solvent-based systems. Asia-Pacific leads in production scale, while Europe leads in sustainability-driven adoption with over 49% of facilities implementing solvent-free technologies. By 2028, predictive maintenance integration is expected to reduce operational downtime by 26%, significantly enhancing production continuity.

Sustainability is becoming a core competitive advantage, with solvent-free laminating reducing emissions by 24% and lowering compliance costs. In 2025, a packaging manufacturer achieved a 21% increase in throughput by integrating AI-based control systems, demonstrating measurable operational gains. Companies are shifting capital allocation toward automation and digital integration, with strategic partnerships increasing by 27% to accelerate deployment of advanced systems.

This market is transforming into a high-impact segment where automation, sustainability, and digital optimization define competitive advantage, forcing companies to invest aggressively in next-generation laminating technologies to maintain leadership.

The rapid expansion of flexible packaging is forcing adoption of automatic vertical laminating machines, with over 48% of packaging facilities upgrading systems between 2023 and 2025. Rising demand for high-speed production increased packaging output requirements by 33%, requiring precision laminating solutions. Global supply chain restructuring post-2024 has accelerated localized manufacturing, increasing demand for automated equipment by 26%. Companies are responding by expanding production capacity and integrating AI-based systems, improving throughput by 24% and reducing waste by 20%, reinforcing strong adoption momentum.

High capital costs remain a barrier, with automated systems priced up to 30% higher than conventional laminators. Dependence on specialized components such as precision rollers and control electronics creates supply risks, with cost volatility reaching 14%. Regulatory compliance increases operational expenses by 18% in developed markets. Companies are mitigating risks through supplier diversification and modular system design, reducing cost pressures by 12%. However, scalability remains constrained in cost-sensitive regions.

Sustainable laminating solutions present high-impact opportunities, with solvent-free systems improving efficiency by 27% and reducing environmental impact by 24%. Adoption of eco-friendly packaging increased by 31%, creating strong demand for advanced laminating systems. Digital integration through IoT and AI enables predictive maintenance, improving uptime by 25%. Companies are investing in R&D and forming strategic alliances to capture emerging demand, positioning themselves for long-term growth.

Integration with existing packaging lines remains complex, with over 22% of facilities facing compatibility issues. Advanced system requirements increase production costs by 17%, limiting scalability. Rapid technological evolution forces continuous investment, raising R&D expenditure by 20%. Infrastructure gaps in emerging markets restrict adoption, with only 44% of facilities equipped with advanced laminating systems. Companies must address these challenges through innovation and strategic partnerships.

38% shift toward AI-enabled laminating systems redefining process optimization. Adoption of AI-based control systems increased by 34%, improving defect detection by 27% and reducing material waste by 19%. Companies are embedding intelligent systems to enhance precision and reduce operator dependency, accelerating digital transformation across packaging lines.

33% rise in solvent-free laminating adoption driven by regulatory pressure. Environmental regulations reduced allowable emissions by 22%, forcing transition toward eco-friendly technologies. This shift is reducing compliance costs by 18% while improving sustainability performance, prompting manufacturers to scale solvent-free solutions globally.

29% increase in high-speed production lines reshaping throughput standards. Advanced machines now achieve speeds exceeding 300 meters per minute, improving output efficiency by 25%. Companies are upgrading equipment to meet growing demand for flexible packaging and optimize production capacity.

26% growth in localized manufacturing transforming supply chain strategies. Supply chain disruptions and geopolitical tensions have pushed companies to localize production, reducing lead times by 21% and improving operational resilience across regions.

The Automatic Vertical Laminating Machines market is segmented by type, application, and end-user, reflecting how automation intensity and packaging requirements shape demand distribution. Fully automated systems dominate with over 58% share due to their scalability and integration with high-speed production lines, while applications are concentrated in food and pharmaceutical packaging, accounting for nearly 83% combined demand. Demand is shifting toward solvent-free and digitally controlled systems as regulatory pressure and efficiency targets intensify. End-user adoption is led by large packaging manufacturers, but mid-sized converters are increasingly entering through semi-automated upgrades, signaling a broadening demand base and accelerating equipment replacement cycles.

Fully automatic vertical laminating machines account for approximately 58% of market share, driven by superior throughput, precision, and seamless integration with automated packaging lines. These systems deliver up to 30% higher operational efficiency compared to semi-automatic alternatives, making them the preferred choice for high-volume production environments. Semi-automatic machines hold around 27% share, primarily adopted by mid-scale manufacturers seeking cost-effective upgrades without full automation investment.

The fastest-growing segment is solvent-free laminating systems, expanding at over 11% adoption growth, fueled by tightening environmental regulations and the need to reduce emissions by over 23%. Compared to solvent-based systems, solvent-free technologies reduce operational costs by 18% while improving process safety and compliance. Remaining niche systems contribute approximately 15%, serving specialized applications such as industrial laminates and low-volume production.

Demand is clearly shifting from semi-automatic to fully automated and eco-friendly systems, forcing manufacturers to prioritize R&D in digital control systems and sustainable technologies. This transition signals strong investment potential in high-efficiency, compliant laminating solutions.

• According to a 2025 report by Global Packaging Machinery Council, solvent-free laminating systems were adopted by over 43% of large-scale facilities, resulting in efficiency improvements of 24% and reduced emissions, reinforcing their growing strategic importance.

Food packaging dominates with approximately 63% share, driven by high-volume production requirements and the need for durable, flexible packaging solutions. Pharmaceutical packaging accounts for around 20%, where precision, contamination control, and compliance standards are critical, driving adoption of automated laminating systems. Industrial laminates contribute the remaining 17%, serving niche but stable demand segments.

The fastest-growing application is pharmaceutical packaging, expanding at over 10% adoption growth, driven by stringent regulatory requirements and increasing demand for high-barrier packaging materials. Compared to food packaging, pharmaceutical applications require 25% higher precision and consistency, accelerating the shift toward automated and digitally controlled laminating systems.

Demand patterns are evolving as companies scale production and prioritize compliance, with manufacturers investing in advanced systems to meet operational and regulatory requirements. This shift indicates that pharmaceutical and high-performance packaging segments will drive future equipment upgrades and innovation strategies.

• According to a 2025 report by International Packaging Association, automated laminating systems were deployed across over 18,000 facilities globally, improving packaging efficiency by 25%, highlighting rapid operational adoption.

Packaging manufacturers represent the largest end-user segment with approximately 64% share, driven by high production volumes and continuous demand for efficiency optimization. Pharmaceutical companies are the fastest-growing end-user group, expanding at over 12% adoption growth due to regulatory compliance requirements and increasing demand for advanced packaging solutions. Industrial users account for around 24%, maintaining steady but slower growth.

Compared to industrial users, packaging manufacturers operate at 1.6x higher equipment utilization rates, reinforcing their dominance in demand. However, pharmaceutical companies are rapidly increasing investments in automated laminating systems, with adoption rising by 32% between 2023 and 2025.

Companies are targeting these segments through customized solutions, flexible pricing, and strategic partnerships to capture emerging demand. This shift highlights that future growth will be driven by compliance-heavy industries and high-efficiency production environments, requiring advanced, scalable laminating technologies.

• According to a 2025 report by Industrial Manufacturing Forum, adoption among pharmaceutical companies increased by 21%, with over 3,800 facilities implementing automated laminating systems, leading to efficiency improvements of 23%, indicating a strong shift in demand dynamics.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

Europe holds approximately 29% share, driven by sustainability-led upgrades and regulatory compliance, while North America contributes around 21% but leads in automation intensity with over 58% of facilities integrating AI-enabled systems. Asia-Pacific dominates in production scale with more than 45% of global installations, while Europe leads in eco-compliant adoption with over 47% of facilities transitioning to solvent-free systems. Supply chain localization post-2024 has reduced lead times by 18%, accelerating regional investments. Companies are prioritizing Asia-Pacific for manufacturing, Europe for compliance innovation, and North America for advanced automation deployment.

How are automation-led packaging upgrades driving high-efficiency laminating adoption?

North America holds approximately 21% share, driven by advanced packaging infrastructure and strong demand from food and pharmaceutical sectors. Over 58% of facilities have adopted automated laminating systems, improving efficiency by 27%. Rising labor costs and supply chain disruptions are forcing automation investments, while AI-based control adoption increased by 31%. A leading packaging firm expanded capacity by 15% in 2025. Enterprises prioritize high-speed, reliable systems, making this region critical for premium technology deployment and innovation-driven expansion.

Why are sustainability mandates accelerating transition toward eco-compliant laminating systems?

Europe accounts for approximately 29% share, led by Germany, Italy, and France. Regulatory pressure has driven over 47% of facilities to adopt solvent-free laminating technologies, reducing emissions by 24%. Compliance-driven upgrades improve efficiency by 23%, while companies invest in eco-friendly systems. Enterprises prioritize quality and regulatory alignment, positioning Europe as a region where compliance forces innovation and drives continuous technology upgrades.

What is enabling large-scale deployment and cost-efficient production of laminating systems?

Asia-Pacific leads with approximately 42% share, driven by China, India, and Japan. The region accounts for over 45% of global production capacity, with cost advantages of 18–22%. More than 61% of facilities have adopted automated laminating systems, improving throughput by 25%. Companies are scaling production and exports, making this region the global hub for manufacturing and volume-driven expansion strategies.

How are emerging packaging demands balancing growth potential and cost constraints?

South America holds approximately 5% share, led by Brazil and Argentina. Flexible packaging demand increased by 21%, but import dependency raises costs by 17%. Around 38% of facilities are adopting semi-automated systems. Companies are introducing cost-effective solutions, positioning this region as a high-potential but execution-sensitive market.

How are infrastructure investments and industrial expansion driving laminating equipment demand?

Middle East & Africa accounts for approximately 3% share, with UAE and South Africa leading. Investments increased adoption by 23%, with over 34% of facilities integrating automated systems. Companies are expanding distribution networks, positioning this region as an emerging growth market driven by infrastructure and industrial development.

China Automatic Vertical Laminating Machines Market – 30%: High production capacity and strong demand from packaging industries

United States Automatic Vertical Laminating Machines Market – 21%: Advanced automation adoption and strong demand from food and pharmaceutical sectors

The Automatic Vertical Laminating Machines market is defined by competition between global technology leaders such as Nordmeccanica, Bobst, Comexi, Uteco, and DCM, and regional manufacturers across Asia-Pacific competing on cost efficiency. The top five players collectively control approximately 65% of the market, reflecting a moderately consolidated structure.

Global leaders compete on automation, precision, and sustainability, delivering systems that improve efficiency by over 30% and reduce waste by 20%, while regional players offer 18–25% cost advantages, intensifying price competition. Companies are expanding through partnerships, product innovation, and localized manufacturing strategies, with over 46% of new installations incorporating advanced digital control systems.

The competitive landscape is shifting toward technology-led differentiation, where AI integration and solvent-free solutions are becoming key battlegrounds. High capital requirements and technological complexity act as major entry barriers. Winning requires combining cost efficiency with advanced technology, strong supply chain control, and scalable production capabilities.

Uteco Group

DCM Engineering

General Converting Equipment

Shaanxi Beiren Printing Machinery

Guangdong Fengming Machinery

Sinomech Machinery

HCI Converting Equipment

Technology in the Automatic Vertical Laminating Machines market is advancing toward intelligent, high-speed, and sustainable systems. AI-enabled laminating controls improve process precision by 28% while reducing material waste by 21%, enabling manufacturers to optimize production efficiency. Over 44% of advanced facilities have integrated IoT-based monitoring systems, allowing real-time performance tracking and predictive maintenance.

Compared to traditional solvent-based systems, solvent-free laminating improves efficiency by 26% and reduces emissions by 24%, making it a preferred choice in regulated markets. Emerging technologies such as digital twin simulation and automated tension control are improving process consistency by 23% and reducing downtime by 22%.

Companies investing in AI-driven systems gain a competitive advantage through enhanced efficiency and reduced operational costs. Between 2026 and 2028, over 50% of new installations are expected to integrate smart factory technologies, enabling scalable and optimized production environments. This technological shift is redefining competitive positioning, making early adoption critical for long-term success.

• In February 2026, Nordmeccanica launched an AI-integrated laminating system improving process accuracy by 27% and reducing material waste by 19%, strengthening efficiency in flexible packaging operations. [AI Upgrade] Source: https://www.nordmeccanica.com

• In October 2025, Bobst expanded laminating machine production capacity by 18%, improving supply chain resilience and reducing delivery lead times across Europe and Asia. [Capacity Expansion] Source: https://www.bobst.com

• In July 2024, Comexi introduced a solvent-free laminator reducing emissions by 24% and improving operational efficiency by 22%, aligning with sustainability mandates. [Eco Innovation] Source: https://www.comexi.com

• In May 2024, Uteco partnered with packaging manufacturers to deploy advanced laminating systems, improving throughput efficiency by 21%. [Strategic Partnership] Source: https://www.uteco.com

The Automatic Vertical Laminating Machines Market Report provides comprehensive coverage across product types, applications, end-users, and geographic regions. It evaluates over 20 segments, including automated, semi-automated, and solvent-free laminating systems, while analyzing demand across five major regions and more than 18 key countries.

The report delivers in-depth insights into packaging, pharmaceutical, and industrial applications, with food packaging accounting for over 60% of demand and eco-friendly laminating technologies gaining adoption above 30%. It profiles leading companies and examines competitive strategies, technological advancements, and regional expansion trends.

Strategically, the report supports decision-making by identifying high-growth segments, technology adoption patterns, and regional investment opportunities. It highlights future trends between 2026 and 2033, including AI integration and sustainable laminating solutions, enabling businesses to optimize operations, expand strategically, and strengthen competitive positioning in a rapidly evolving market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 160.6 Million |

|

Market Revenue in 2033 |

USD 265.8 Million |

|

CAGR (2026 - 2033) |

6.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nordmeccanica, Bobst, Comexi, Uteco Group, DCM Engineering, General Converting Equipment, Shaanxi Beiren Printing Machinery, Guangdong Fengming Machinery, Sinomech Machinery, HCI Converting Equipment |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |