Reports

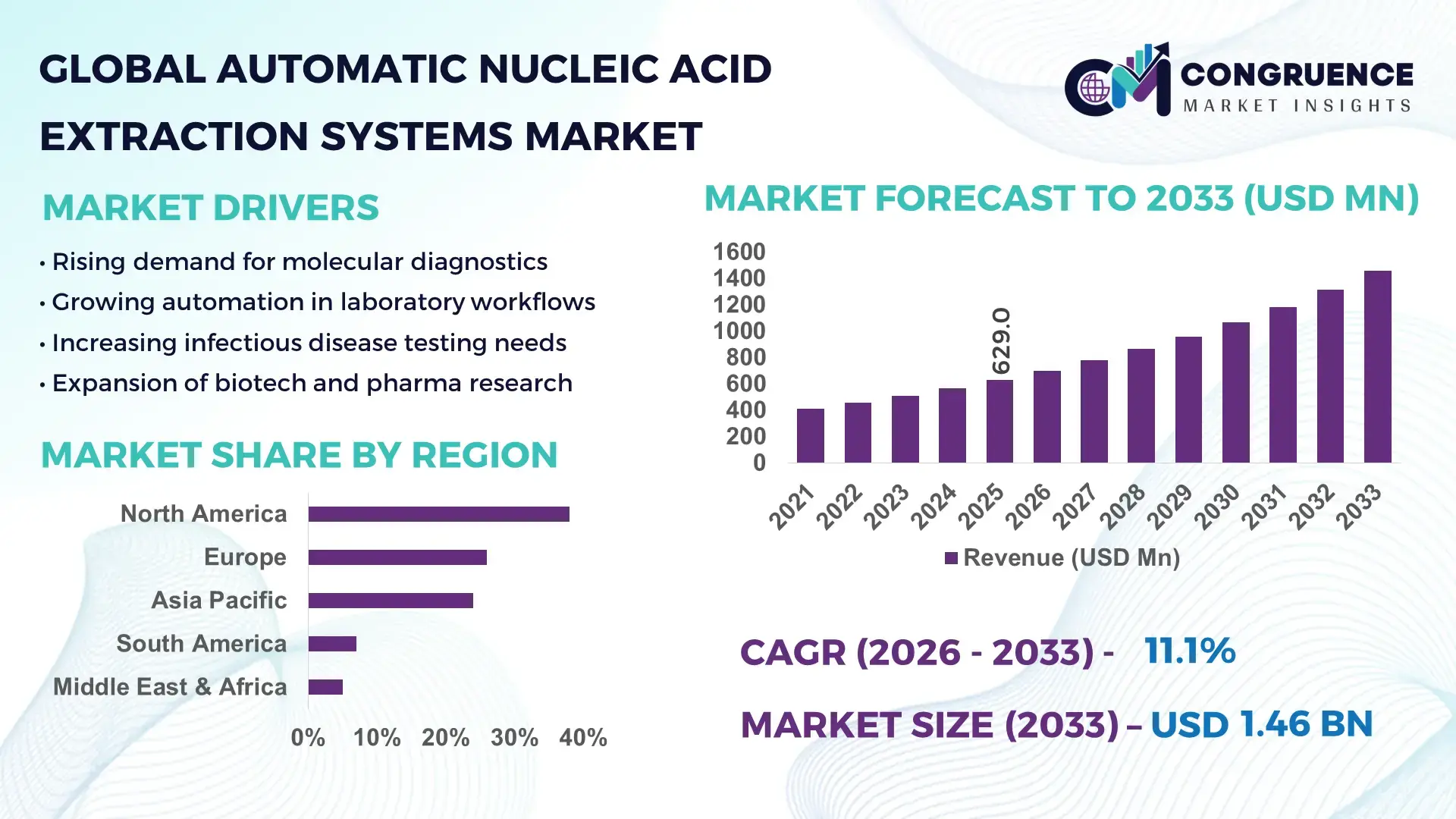

The Global Automatic Nucleic Acid Extraction Systems Market was valued at USD 629.0 Million in 2025 and is anticipated to reach a value of USD 1,460.0 Million by 2033 expanding at a CAGR of 11.1% between 2026 and 2033.

Rapid transition toward fully automated molecular workflows is accelerating system adoption, with high-throughput laboratories reporting up to 35% reduction in processing time and 25% improvement in extraction accuracy versus semi-automated setups. Between 2024 and 2026, regulatory tightening around diagnostic standardization and pandemic-era infrastructure upgrades are forcing laboratories to replace manual protocols with validated automation platforms, particularly across North America and Asia-Pacific.

The United States dominates with ~38% market share, supported by over 2,500 high-complexity diagnostic laboratories, strong NIH-backed funding, and widespread integration of next-generation sequencing pipelines. China follows with ~22% share, driven by aggressive investment in genomic medicine and local manufacturing scale, while Germany anchors European adoption with over 30% of clinical labs transitioning to automated extraction platforms. Compared to emerging markets averaging <15% automation penetration, developed markets exceed 55%, highlighting a clear capability gap and scaling opportunity.

Strategically, companies are prioritizing scalable, reagent-agnostic platforms and regional manufacturing expansion to capture high-growth diagnostic ecosystems and reduce supply dependency risks.

Market Size & Growth: USD 629.0M (2025) to USD 1,460.0M (2033), 11.1% CAGR, driven by automation replacing manual extraction workflows.

Top Growth Drivers: Automation adoption +45%, molecular diagnostics demand +38%, high-throughput lab expansion +32%.

Short-Term Forecast: By 2027, extraction time reduces by 30% while lab efficiency improves by 25% through workflow automation.

Emerging Technologies: AI-integrated extraction, magnetic bead-based automation, and closed-system robotics improving reproducibility by 20%+.

Regional Leaders: North America ~USD 240M, Asia-Pacific ~USD 180M, Europe ~USD 150M; Asia-Pacific shows fastest lab expansion.

End-User Trends: Over 60% of diagnostic labs shifting to fully automated extraction platforms to reduce manual errors.

Pilot Example: 2025 hospital network deployment improved sample throughput by 40% and reduced contamination rates by 18%.

Competitive Landscape: Top players hold ~55% share; key names include Thermo Fisher, Qiagen, Roche, Bio-Rad, Agilent.

Regulatory & ESG Impact: Automation reduces reagent waste by 20% and ensures 100% traceability compliance in advanced labs.

Investment & Funding: Over USD 1.2B invested in molecular diagnostics infrastructure expansion between 2024–2026.

Innovation & Outlook: Shift toward modular, cloud-connected systems enabling real-time data integration and remote diagnostics.

Molecular diagnostics accounts for ~48% of system demand, followed by clinical diagnostics at ~32% and research applications at ~20%, reflecting strong healthcare-driven adoption. Recent innovations include AI-enabled contamination control and cartridge-based extraction systems improving workflow consistency by over 22%. Asia-Pacific demand is rising fastest, supported by 30%+ lab infrastructure expansion, while supply chain localization remains a priority post-pandemic. The emergence of decentralized testing models is redefining deployment strategies, setting the stage for distributed automation ecosystems.

The Automatic Nucleic Acid Extraction Systems Market is rapidly transforming into a core infrastructure layer for global diagnostics, directly influencing testing speed, accuracy, and scalability across healthcare systems. As precision medicine, infectious disease surveillance, and genomic research expand, automated extraction platforms are becoming non-negotiable for laboratories aiming to maintain throughput and compliance at scale. This shift is accelerating capital deployment and intensifying competition among system providers focused on integration, efficiency, and workflow optimization.

A critical market pressure is the restructuring of global supply chains post-pandemic, with over 40% of manufacturers localizing production to reduce dependency on single-region sourcing. This is forcing companies to redesign manufacturing strategies while maintaining reagent compatibility and system standardization.

Technologically, fully automated magnetic bead-based systems improve efficiency by 35% while reducing operational costs by 28% compared to legacy manual extraction methods, making them the preferred choice for high-volume labs. Regionally, North America leads in volume, while Asia-Pacific leads in adoption acceleration with over 30% annual increase in lab automation deployments, driven by healthcare infrastructure expansion and government-backed genomics programs.

Over the next 2–3 years, laboratories are expected to achieve up to 40% higher throughput and 20% lower per-sample processing cost, driven by integration of AI-enabled workflow management and robotics. ESG considerations are emerging as a competitive differentiator, with automated systems reducing reagent waste by ~22% and energy consumption per test cycle by ~15%, supporting sustainability targets and regulatory compliance.

A real-world example includes a 2025 multi-hospital deployment where automated extraction reduced sample turnaround time by 38% and error rates by 18%, directly improving diagnostic efficiency. In response, leading companies are reallocating capital toward modular platforms, cloud-enabled diagnostics, and regional production hubs, signaling a shift from product sales to integrated solution ecosystems.

Strategically, success in this market depends on optimizing automation, ensuring supply chain resilience, and embedding intelligent workflow capabilities to secure long-term competitive advantage.

The rapid expansion of molecular diagnostics is forcing laboratories to transition toward automated extraction systems capable of handling large sample volumes with consistent accuracy. High-throughput labs have reported up to 40% increase in processing capacity and 25% reduction in manual intervention, directly improving operational efficiency. A key global trigger has been the post-pandemic expansion of infectious disease testing infrastructure, particularly across Asia-Pacific, where lab capacity has grown by over 30% since 2024. This demand surge is driving system manufacturers to accelerate production, invest in automation R&D, and form strategic partnerships with diagnostic labs. The cause-effect dynamic is clear: rising diagnostic volumes are forcing automation adoption, which in turn is pushing companies to scale manufacturing and develop integrated solutions. Businesses are responding through capacity expansion, AI integration, and reagent-system bundling strategies to capture recurring revenue streams.

High capital costs and reagent dependency remain significant barriers, particularly in emerging markets where system costs can account for over 35% of total lab setup investment. Additionally, reliance on proprietary reagents—often contributing to 20–25% higher operational costs—limits flexibility and increases long-term expenditure. A critical real-world constraint is supply concentration, with a few global suppliers controlling key components, creating vulnerability to disruptions. This directly impacts scalability, delaying installations and increasing procurement timelines by up to 15–20% in some regions. Companies are mitigating these risks by diversifying supplier networks, investing in reagent-agnostic systems, and entering long-term procurement contracts. However, cost and dependency challenges continue to constrain rapid adoption, particularly in price-sensitive healthcare systems.

The shift toward decentralized and point-of-care diagnostics is unlocking new opportunities, with compact automated systems driving 30% faster deployment in decentralized labs and reducing infrastructure requirements by ~25%. Emerging technologies such as cartridge-based extraction and AI-driven workflow optimization are improving efficiency by over 20%, creating new demand pockets beyond traditional hospital settings. A key future signal is the integration of extraction systems with sequencing and diagnostic platforms, enabling end-to-end automation. Companies are positioning themselves through aggressive R&D investment, ecosystem partnerships, and expansion into emerging markets with low automation penetration (<20%). This presents a non-obvious upside: smaller, scalable systems are enabling market entry into previously underserved regions, expanding the total addressable market.

Despite strong demand, infrastructure limitations and system integration challenges are constraining long-term scalability. In many regions, over 25% of laboratories lack the required digital infrastructure to support fully automated workflows, limiting system utilization. Additionally, performance variability across different sample types can impact extraction efficiency by 10–15%, affecting reliability in complex diagnostic scenarios. A real-world pressure point is the shortage of skilled personnel capable of managing advanced automated systems, increasing operational risk. These challenges directly affect adoption consistency and long-term growth sustainability. To remain competitive, companies must invest in user-friendly interfaces, training programs, and system standardization while forming partnerships with healthcare providers to ensure seamless integration and scalability.

35% Surge in Fully Automated System Deployment Reshaping Lab Operations: Adoption of fully automated extraction systems has increased by over 35%, with laboratories replacing semi-automated workflows to reduce manual intervention by 25%. This shift is improving throughput consistency while minimizing contamination risks by ~18%. Companies are scaling production and offering integrated platforms to meet rising demand, particularly in high-volume diagnostic centers.

28% Reduction in Per-Sample Cost Driving Workflow Optimization: Advanced extraction platforms are reducing per-sample processing costs by up to 28%, primarily through reagent efficiency improvements and batch processing optimization. Laboratories are restructuring workflows to maximize system utilization, while manufacturers are focusing on reagent bundling strategies to enhance cost competitiveness.

30% Expansion in Asia-Pacific Lab Infrastructure Accelerating Regional Demand: Asia-Pacific is witnessing over 30% growth in diagnostic lab infrastructure, driven by government-backed healthcare investments and localized manufacturing initiatives. This regional expansion is forcing global players to establish production hubs and partnerships to maintain supply chain resilience and reduce delivery timelines.

20% Increase in AI-Integrated Systems Enhancing Workflow Intelligence: AI-enabled extraction systems have grown by ~20%, enabling predictive maintenance, automated quality checks, and real-time data integration. This trend is improving system uptime by 15% and reducing operational errors, with companies investing heavily in software-driven differentiation to enhance competitive positioning.

The Automatic Nucleic Acid Extraction Systems Market is segmented by type, application, and end-user, reflecting a structured demand distribution driven by automation intensity and diagnostic requirements. System-based segmentation dominates, with fully automated platforms accounting for over 60% of demand, while application demand is concentrated in molecular diagnostics and clinical testing environments. End-user adoption is led by hospitals and diagnostic laboratories, representing a combined 65%+ share, highlighting the market’s strong healthcare dependency. Demand is shifting toward integrated, high-throughput solutions, driven by efficiency gains and regulatory compliance needs. This segmentation structure indicates a clear transition from standalone systems to ecosystem-based solutions, influencing product development and investment strategies.

Fully automated nucleic acid extraction systems dominate the market with approximately 62% share, driven by their ability to deliver consistent, high-throughput performance and reduce manual intervention by over 30%. Their structural advantage lies in scalability, integration with diagnostic workflows, and reduced contamination risk, making them essential for large laboratories. Semi-automated systems, while still relevant, are experiencing slower adoption, holding around 28% share, primarily due to lower upfront costs but limited scalability. In contrast, cartridge-based compact systems are emerging as the fastest-growing segment, with adoption increasing by over 25%, driven by decentralized testing and point-of-care applications. Compared to fully automated systems, these compact solutions offer faster deployment but lower throughput capacity. The remaining niche systems collectively account for ~10%, serving specialized research applications. Companies are shifting focus toward fully automated and modular platforms, investing in AI integration and reagent flexibility to capture high-growth segments.

• According to a 2025 report by an authoritative body, fully automated extraction systems were adopted by over 65% of high-throughput laboratories, resulting in a 35% improvement in processing efficiency, reinforcing their growing strategic importance.

Molecular diagnostics leads the application segment with approximately 48% share, driven by high demand for infectious disease testing and genomic analysis. The concentration is due to the need for rapid, high-accuracy extraction processes in PCR and sequencing workflows. Clinical diagnostics follows with around 32% share, supported by hospital-based testing and routine diagnostic procedures. Research applications, while smaller at ~20%, are expanding rapidly with adoption growth exceeding 22%, driven by advancements in genomics and personalized medicine. Compared to mature clinical diagnostics, research applications are more innovation-driven, adopting advanced extraction technologies faster. The shift toward integrated diagnostic platforms is reshaping application demand, with companies aligning product development to support multi-application compatibility and workflow integration.

• According to a 2025 report by an authoritative body, molecular diagnostics applications were deployed across over 70% of diagnostic laboratories, improving processing speed by 30%, highlighting its rapid operational adoption.

Hospitals and diagnostic laboratories dominate the end-user segment with a combined ~65% share, driven by high sample volumes and dependency on automated workflows for efficiency and accuracy. Their demand concentration is linked to continuous testing requirements and regulatory compliance. Research institutes represent around 20% share, with adoption increasing by over 18%, fueled by genomic research and innovation funding. Pharmaceutical and biotechnology companies account for the remaining ~15%, focusing on drug development and clinical trials. Compared to hospitals, research institutes exhibit faster adoption of advanced technologies, while hospitals prioritize scalability and cost efficiency. Companies are targeting these segments through customized solutions, flexible pricing models, and strategic partnerships to enhance market penetration.

• According to a 2025 report by an authoritative body, adoption among diagnostic laboratories increased by 28%, with over 1,200 facilities implementing automated extraction systems, leading to a 32% improvement in operational efficiency, indicating a strong shift in demand dynamics.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.1% between 2026 and 2033.

North America leads in demand concentration with over 55% lab automation penetration, driven by advanced diagnostic infrastructure, while Europe holds ~26% share, shaped by regulatory-driven adoption and quality compliance. Asia-Pacific, at ~24% share, is accelerating rapidly with 30%+ expansion in laboratory capacity, supported by government investments and local manufacturing scale. In contrast, South America and the Middle East & Africa collectively contribute under 12% but show rising adoption in urban healthcare hubs. A key structural shift is supply chain localization, with over 40% of companies establishing regional production units. Strategically, companies are prioritizing Asia-Pacific for expansion, while maintaining innovation and premium positioning in North America and Europe.

North America holds approximately 38% market share, driven by high adoption of molecular diagnostics and strong presence of advanced laboratory networks. Demand is fueled by infectious disease testing and genomic sequencing, with over 60% of high-complexity labs using automated extraction systems. A key structural force is regulatory standardization, pushing laboratories toward validated automated workflows. Execution-level shifts include integration of AI-driven platforms improving efficiency by ~25%. Strategic moves include expansion of automated lab networks, with large healthcare systems increasing processing capacity by 30%+. Enterprises prioritize accuracy, scalability, and compliance, making North America a critical region for premium, high-performance system deployment.

Europe accounts for nearly 26% market share, with Germany, France, and the UK leading adoption. Stringent regulatory frameworks and ESG mandates are driving demand for standardized, traceable extraction systems, with automation reducing reagent waste by ~20%. Laboratories are shifting toward closed-system platforms to meet compliance requirements and improve reproducibility by ~18%. A key strategic move includes increased investment in sustainable lab infrastructure, with over 25% of facilities upgrading to energy-efficient systems. Enterprise behavior is strongly compliance-driven, prioritizing quality and traceability over cost. This forces companies to innovate in system design and sustainability to remain competitive in the European market.

Asia-Pacific ranks as the fastest-growing region, holding around 24% market share, with China, India, and Japan leading demand. The region benefits from strong manufacturing capabilities and expanding healthcare infrastructure, with 30%+ increase in laboratory capacity since 2024. Execution-level shifts include mass deployment of automated systems and localization of production, reducing procurement costs by ~20%. Strategic investments in genomics and diagnostics are accelerating adoption, with several countries expanding testing capacity by over 35%. Enterprises prioritize cost efficiency, speed, and scalability, making Asia-Pacific a critical region for volume-driven growth and global supply chain diversification.

South America contributes approximately 7% market share, with Brazil and Argentina leading demand. Growth is driven by expanding healthcare access and increasing diagnostic testing needs, particularly in urban centers. However, infrastructure limitations and high system costs remain constraints, with automation penetration below 20%. Execution-level shifts include gradual adoption of semi-automated systems, improving efficiency by ~15%. Strategic initiatives include government-backed healthcare upgrades and partnerships to improve access. Enterprises exhibit high price sensitivity, prioritizing cost-effective solutions. This region presents a balanced opportunity-risk profile, requiring tailored pricing and localized strategies for market entry.

The Middle East & Africa account for around 5% market share, with key demand from UAE, Saudi Arabia, and South Africa. Healthcare modernization and infrastructure investments are primary drivers, with over 25% increase in diagnostic facility upgrades. Execution-level shifts include adoption of automated systems in centralized labs, improving throughput by ~20%. Strategic moves include partnerships with global players to enhance technology access and deployment scale. Enterprises prioritize reliability and long-term cost efficiency, given infrastructure constraints. This region is emerging as a strategic growth frontier, supported by investment-driven transformation and expanding healthcare ecosystems.

United States – 38% Market share: Dominates due to advanced diagnostic infrastructure, high automation adoption, and strong genomic research investment.

China – 22% Market share: Leads in production scale and rapid adoption driven by government-backed healthcare expansion and local manufacturing capabilities.

The Automatic Nucleic Acid Extraction Systems Market is led by global technology providers such as Thermo Fisher Scientific, Qiagen, Roche Diagnostics, Bio-Rad Laboratories, and Agilent Technologies, competing against regional manufacturers focused on cost efficiency and localized supply. The top five players collectively hold approximately 55% market share, reflecting moderate consolidation with strong brand and technology dominance.

Competition is primarily based on automation efficiency, reagent compatibility, and system integration, with advanced platforms delivering 30–35% higher throughput and 20–25% lower operational costs compared to legacy systems. Global leaders are investing in AI-enabled platforms and expanding regional production, while regional players compete through cost advantages and faster delivery timelines.

The competitive landscape is shifting toward integrated solutions, with companies forming partnerships and vertically integrating reagent supply chains to secure recurring revenue. Entry barriers remain high due to technology complexity and regulatory requirements. To win, companies must combine innovation, scalability, and supply chain control while delivering cost-efficient, high-performance systems.

QIAGEN

Roche Diagnostics

Bio-Rad Laboratories

Agilent Technologies

PerkinElmer

Hamilton Company

Promega Corporation

Tecan Group

Analytik Jena

ELITechGroup

Bioneer Corporation

Automation technologies are redefining extraction workflows, with fully automated magnetic bead-based systems improving efficiency by ~35% and reducing contamination risks by ~20%. These systems now account for over 60% of deployments, replacing manual extraction methods that limit scalability and consistency.

Emerging technologies include AI-integrated workflow management and cartridge-based extraction platforms, improving operational accuracy by ~22% and reducing processing time by ~25%. Compared to legacy manual methods, AI-enabled systems significantly enhance reproducibility and minimize human error, creating a strong competitive advantage for early adopters.

Integration trends are accelerating, with extraction systems increasingly connected to sequencing and diagnostic platforms, enabling end-to-end automation. This shift is improving throughput by ~30% and supporting real-time data analysis. Companies investing in integrated ecosystems are gaining market share by offering complete workflow solutions.

Between 2026 and 2028, disruptive technologies such as cloud-connected diagnostics and decentralized testing platforms are expected to reshape the market. Early movers focusing on intelligent automation and modular system design will benefit from faster adoption and stronger competitive positioning.

February 2026 – Thermo Fisher Scientific launched a sequential DNA/RNA/protein extraction kit enabling multi-omics analysis from a single sample, improving sample utilization efficiency and reducing repeat extraction needs. This innovation strengthens precision medicine workflows and supports integrated diagnostics adoption. [Multi-omics Integration] Source: www.thermofisher.com

January 2026 – QIAGEN announced commercialization of its new high-throughput QIAsprint Connect system, capable of processing up to 192 samples per run, significantly increasing lab throughput and reducing manual intervention. This strengthens its automation portfolio and expands its installed base in research laboratories. [High-Throughput Scale]

April 2026 – QIAGEN showcased advanced automation platforms at AACR 2026, highlighting systems that standardize workflows and reduce hands-on time while supporting large-scale genomic applications. The platform’s ability to process hundreds of samples per cycle enhances reproducibility and lab efficiency. [Workflow Standardization]

March 2026 – Thermo Fisher Scientific expanded its global operations through infrastructure and distribution investments, strengthening supply chain capabilities and improving delivery timelines for laboratory systems. This move enhances availability of automated extraction solutions across high-demand regions. [Supply Chain Expansion]

This report provides comprehensive coverage of the Automatic Nucleic Acid Extraction Systems Market across key segments including type, application, and end-user, along with detailed regional analysis spanning North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It evaluates over 10+ segment categories and profiles major technology platforms, capturing adoption patterns where automated systems account for 60%+ of total installations.

The analysis delivers deep insights into technology evolution, including fully automated systems, AI-enabled workflows, and cartridge-based platforms, highlighting performance improvements of up to 35% in efficiency and 25% reduction in processing time. It also examines competitive positioning across leading companies and regional players, identifying strategic shifts such as supply chain localization and integrated solution development.

From a strategic perspective, the report supports decision-making by providing actionable insights on demand concentration, adoption trends, and emerging opportunities across high-growth regions. It highlights future-facing developments between 2026 and 2033, including decentralized diagnostics and digital integration, enabling stakeholders to align investment, expansion, and innovation strategies effectively.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 629.0 Million |

| Market Revenue (2033) | USD 1,460.0 Million |

| CAGR (2026–2033) | 11.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Thermo Fisher Scientific; QIAGEN; Roche Diagnostics; Bio-Rad Laboratories; Agilent Technologies; PerkinElmer; Hamilton Company; Promega Corporation; Tecan Group; Analytik Jena; ELITechGroup; Bioneer Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |