Reports

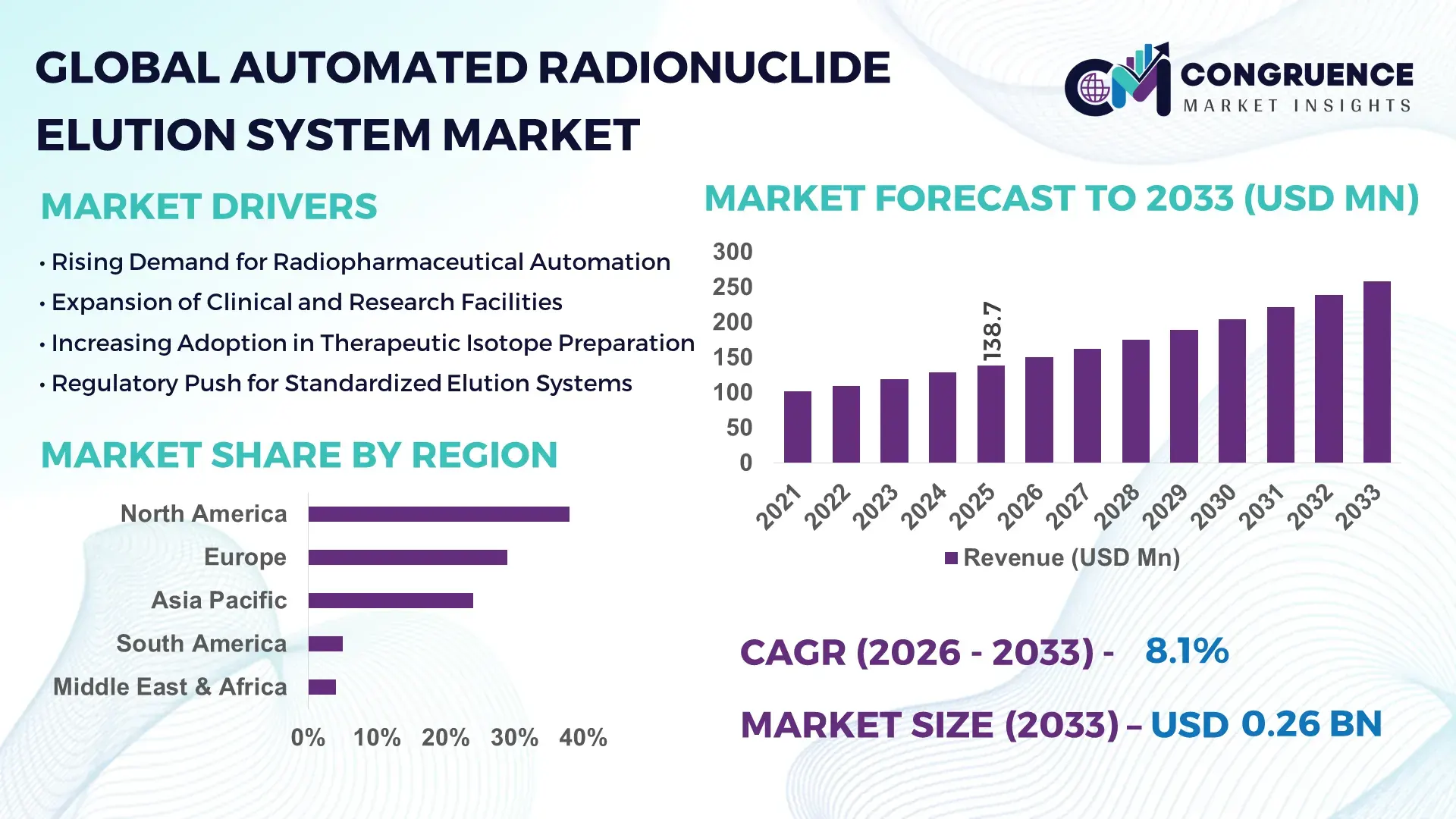

The Global Automated Radionuclide Elution System Market was valued at USD 138.7 Million in 2025 and is anticipated to reach a value of USD 258.6 Million by 2033 expanding at a CAGR of 8.1% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily supported by the rising procedural volume in nuclear medicine and the shift toward automation to improve radiopharmaceutical preparation accuracy.

The United States remains the dominant country in the Automated Radionuclide Elution System Market, supported by the largest installed base of nuclear medicine facilities and isotope production centers. More than 1,200 nuclear medicine departments operate across the country, performing over 18 million diagnostic procedures annually. The U.S. accounts for over 40 commercial cyclotrons, enabling high domestic production of Tc-99m generators and PET isotopes. Annual public and private investments in nuclear medicine infrastructure exceed USD 1.5 billion, with automation penetration in radiopharmacies crossing 65% in 2025. Advanced adoption of closed-system elution platforms and AI-assisted dose calibration systems has improved workflow efficiency by 30–35% across leading hospital networks.

Market Size & Growth: Valued at USD 138.7 Million in 2025, projected to reach USD 258.6 Million by 2033, expanding at 8.1% CAGR, driven by rising nuclear imaging volumes and automation mandates.

Top Growth Drivers: Automation adoption +42%, procedural throughput improvement +28%, contamination risk reduction +35%.

Short-Term Forecast: By 2028, automated elution systems are expected to reduce radiopharmacy preparation time by 25% per batch.

Emerging Technologies: AI-guided dose calibration, closed-system sterile elution modules, and remote monitoring platforms.

Regional Leaders: North America USD 104 Million by 2033 (hospital automation), Europe USD 72 Million (regulatory-driven upgrades), Asia Pacific USD 61 Million (new cyclotron installations).

Consumer/End-User Trends: Hospital radiopharmacies account for 62% of system installations, with centralized labs growing at 18% annually.

Pilot or Case Example: In 2024, a U.S. hospital network achieved 32% workflow efficiency gain using fully automated elution units.

Competitive Landscape: Market leader holds ~28% share, followed by 4 major players controlling ~52% combined.

Regulatory & ESG Impact: Automation adoption linked to 40% reduction in radioactive handling incidents under updated GMP norms.

Investment & Funding Patterns: Over USD 620 Million invested globally in nuclear medicine automation projects since 2022.

Innovation & Future Outlook: Integration of robotics and AI-based contamination detection is shaping next-generation systems.

The Automated Radionuclide Elution System Market is driven by hospital radiopharmacies contributing 45%, diagnostic imaging centers 35%, and research institutes 20% of total demand. Closed-system sterile elution technologies and AI-based calibration modules are accelerating product innovation. Regulatory tightening on radiation safety, growing PET-CT installation density in Asia Pacific, and rising oncology imaging volumes are strengthening long-term adoption, while compact modular systems are emerging as the preferred configuration.

The Automated Radionuclide Elution System Market holds strong strategic relevance as nuclear medicine transitions from manual preparation toward fully automated, compliance-driven radiopharmacy workflows. Automation now directly influences diagnostic accuracy, radiation safety compliance, and hospital throughput efficiency. Advanced closed-system elution platforms deliver 35% contamination risk reduction compared to open manual elution standards, significantly lowering occupational exposure and batch rejection rates.

North America dominates in procedural volume, while Europe leads in adoption with nearly 68% of radiopharmacies using automated systems as of 2025. By 2028, AI-assisted activity calibration and predictive maintenance platforms are expected to improve batch yield consistency by 22% and cut system downtime by 30%. Firms are committing to ESG metrics such as 45% reduction in radioactive waste handling incidents by 2030, supported by automated containment and monitoring protocols.

In 2024, a German radiopharmacy network achieved 27% dose accuracy improvement through robotic-assisted elution and digital verification systems. Comparative benchmarks show next-generation robotic elution delivers 40% workflow improvement compared to semi-automated legacy platforms. As nuclear imaging volumes grow and compliance thresholds tighten, the Automated Radionuclide Elution System Market is positioned as a pillar of operational resilience, regulatory alignment, and sustainable diagnostic infrastructure.

The Automated Radionuclide Elution System Market is shaped by rising nuclear imaging demand, tightening radiation safety regulations, and growing centralization of radiopharmacy operations. Over 75% of new nuclear medicine labs commissioned since 2022 are designed around automated preparation workflows. Increased adoption of PET-CT and SPECT systems, which exceeded 65,000 active installations globally, continues to drive consistent system demand. At the same time, workforce shortages in nuclear pharmacy and stricter GMP compliance standards are accelerating the shift from manual to closed automated elution platforms across hospitals and commercial radiopharmacies.

Global nuclear medicine procedures surpassed 50 million annually by 2025, with oncology imaging accounting for over 60% of total scans. Automated elution systems now support 2–3x higher daily batch throughput compared to manual preparation. In high-volume radiopharmacies, automation has reduced technician exposure time by 38% and preparation errors by 41%, directly improving clinical safety and operational scalability.

The average cost of a fully automated elution workstation ranges between USD 180,000–320,000, limiting adoption in small and mid-sized hospitals. Maintenance contracts add 8–12% annually to operating expenses. In emerging markets, only 35% of nuclear medicine centers can justify full automation due to limited procedural volumes and constrained capital budgets, slowing penetration.

Centralized radiopharmacies now supply over 48% of urban imaging centers in developed regions. Automation enables centralized facilities to scale output by 45–55% without proportional labor expansion. Growth of hub-and-spoke radiopharmacy models across Asia Pacific and the Middle East is creating sustained demand for multi-generator, high-throughput automated elution platforms.

Radiopharmaceutical preparation is governed by over 120 distinct national and regional compliance requirements. Validation cycles for new automated systems can exceed 12–18 months, delaying deployments. Inconsistent harmonization between FDA, EMA, and regional regulators increases certification costs by 20–25%, creating barriers for rapid product rollout.

Rapid shift toward fully closed sterile systems: Over 72% of new installations in 2025 adopted fully enclosed elution chambers, reducing airborne contamination by 44% and improving batch sterility pass rates to 99.6%.

Integration of AI-assisted calibration platforms: AI-based dose verification is now deployed in 38% of advanced radiopharmacies, improving activity measurement accuracy by 26% and reducing reprocessing rates by 31%.

Growth of compact modular systems: Compact automated units represent 41% of new sales, cutting floor space usage by 35% and enabling deployment in outpatient imaging centers with limited infrastructure.

Rise in remote monitoring and predictive maintenance: Remote diagnostics reduced unplanned downtime by 29% and extended system uptime to >97% availability across large hospital networks.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Automated Radionuclide Elution System Market. Research suggests that 55% of new projects achieved cost benefits using prefabricated installation modules. Pre-assembled shielding and automated fluid paths reduced on-site commissioning time by 42%, particularly in Europe and North America, where construction efficiency is critical.

The Automated Radionuclide Elution System Market is segmented by type, application, and end-user, each reflecting distinct operational needs and compliance requirements within nuclear medicine workflows. By type, fully automated closed systems dominate installations due to their superior sterility control and reduced radiation exposure risk, while semi-automated and manual-assisted systems remain relevant in low-volume facilities and emerging markets. By application, radiopharmaceutical preparation represents the core demand driver, supported by increasing diagnostic imaging volumes and tighter GMP compliance mandates. Therapeutic isotope preparation and research-based elution workflows are expanding as nuclear oncology and theranostics gain clinical traction. By end-user, hospital radiopharmacies account for the majority of system deployments, followed by centralized commercial radiopharmacies and academic or government research institutes. Across all segments, adoption is shaped by procedural throughput requirements, workforce safety standards, and national regulatory frameworks governing radioactive material handling and sterile drug preparation.

Fully automated closed-system elution units represent the leading product category, accounting for approximately 56% of global installations in 2025. Their dominance is supported by the ability to reduce technician radiation exposure by 35–45%, achieve sterility assurance levels above 99.5%, and enable batch-to-batch reproducibility within ±2% activity variance. Semi-automated systems hold nearly 24% of adoption, favored by mid-sized hospitals seeking partial workflow automation without full capital investment. Manual-assisted and compact hybrid systems collectively contribute the remaining 20%, maintaining niche relevance in low-throughput centers, academic labs, and emerging markets with budget constraints.

While fully automated platforms lead in installed base, compact modular systems are the fastest-growing type, expanding at an estimated 10.2% CAGR, driven by outpatient imaging center growth, space constraints, and rapid deployment needs. These systems reduce footprint requirements by 30–40% and cut on-site commissioning time by 45%.

Radiopharmaceutical preparation remains the leading application, accounting for approximately 61% of system utilization, supported by high-volume Tc-99m and PET isotope workflows for oncology and cardiology diagnostics. Therapeutic isotope preparation currently represents 23% of adoption, reflecting growing demand for lutetium-177 and actinium-225–based therapies. Research and clinical trial isotope preparation contributes the remaining 16%, driven by university hospitals and biotech firms developing novel radiotracers.

Therapeutic isotope preparation is the fastest-growing application, expanding at an estimated 11.4% CAGR, fueled by rapid expansion in nuclear oncology programs and increased approvals of radioligand therapies. In 2025, more than 41% of tertiary hospitals globally reported upgrading elution workflows to support therapeutic isotope production. Additionally, 38% of nuclear medicine departments in developed markets are now piloting dual-use systems capable of both diagnostic and therapeutic isotope elution.

Hospital radiopharmacies constitute the largest end-user segment, representing approximately 62% of total system deployments. Their leadership is supported by rising diagnostic imaging volumes, internal isotope preparation mandates, and workforce radiation safety regulations. Centralized commercial radiopharmacies account for 26% of installations, driven by hub-and-spoke distribution models supplying urban imaging centers within 200–300 km radii. Academic and government research institutes collectively contribute the remaining 12%, maintaining stable demand for experimental isotope workflows and tracer development programs.

Centralized commercial radiopharmacies are the fastest-growing end-user group, expanding at an estimated 12.1% CAGR, supported by urban population growth, next-day isotope delivery requirements, and outsourcing of radiopharmaceutical preparation by mid-sized hospitals. In 2025, 44% of hospitals in North America and Europe reported sourcing at least part of their isotope supply from centralized facilities, while 29% of new radiopharmacy facilities commissioned globally were commercial hubs.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2026 and 2033.

North America continues to lead due to more than 1,300 active nuclear medicine centers, over 18 million diagnostic procedures annually, and automation penetration exceeding 65% in radiopharmacies. Europe follows with 29% share, supported by over 6,500 SPECT and PET scanners and harmonized GMP enforcement across 27 countries. Asia-Pacific holds 24% share, driven by rapid infrastructure expansion, with China and India adding over 320 new nuclear imaging facilities between 2022 and 2025. South America represents 5%, while Middle East & Africa together account for 4%, supported by rising oncology programs and government-backed isotope production projects. Regional adoption patterns reflect regulatory stringency, healthcare spending per capita, cyclotron density, and the scale of centralized radiopharmacy networks.

North America holds approximately 38% of the global market share, supported by the highest concentration of nuclear medicine facilities and centralized radiopharmacies. The region operates more than 40 commercial cyclotrons and over 9,000 active PET and SPECT scanners, generating sustained demand for high-throughput automated elution systems. Key demand originates from hospital radiopharmacies, oncology imaging centers, and commercial isotope distributors. Regulatory reinforcement of USP <825> and radiation safety standards has accelerated closed-system adoption, with over 68% of new installations now fully automated. Digital transformation trends include remote monitoring, AI-assisted dose calibration, and predictive maintenance platforms. A leading U.S.-based manufacturer expanded domestic production capacity by 25% in 2024 to meet rising hospital procurement. Regional consumer behavior reflects higher enterprise adoption in healthcare systems, with over 72% of tertiary hospitals preferring in-house automated isotope preparation.

Europe accounts for nearly 29% of global installations, with Germany, France, and the UK representing over 62% of regional demand. More than 6,500 nuclear imaging systems operate across the region, supported by strong public healthcare funding and centralized radiopharmacy networks. Regulatory bodies enforce harmonized GMP and radiation protection directives, driving replacement of semi-automated systems with fully enclosed platforms. Sustainability initiatives targeting 30% reduction in radioactive handling incidents by 2030 are influencing procurement strategies. Adoption of digital batch verification and traceability systems now exceeds 55% in Western Europe. A German equipment supplier deployed standardized automated systems across 14 university hospitals in 2024. Regional behavior reflects regulatory pressure leading to strong demand for explainable, auditable automation platforms.

Asia-Pacific ranks as the second-largest volume market, holding approximately 24% share, with China, Japan, and India contributing over 70% of regional installations. Between 2022 and 2025, more than 320 new nuclear medicine departments were commissioned across the region. Japan operates over 1,200 PET scanners, while China added 140 cyclotron facilities in five years. Manufacturing localization and modular system adoption are accelerating, with compact systems representing 46% of new deployments. Regional innovation hubs in Shanghai, Tokyo, and Seoul are integrating robotics and digital QA platforms. A Japanese technology firm expanded automated elution exports by 31% in 2024. Consumer behavior reflects growth driven by expanding hospital networks and rapid modernization of public healthcare systems.

South America accounts for approximately 5% of global demand, led by Brazil and Argentina, which together represent over 68% of regional installations. Brazil operates more than 420 nuclear medicine centers, supported by national isotope production programs and public oncology initiatives. Infrastructure upgrades in urban hospitals and new PET-CT deployments are increasing demand for automated preparation. Government incentives for domestic radiopharmaceutical production are improving equipment procurement cycles. A Brazilian public-sector radiopharmacy commissioned six new automated elution units in 2024 to support national imaging programs. Regional behavior shows demand tied to public healthcare expansion and localization of diagnostic services.

Middle East & Africa together hold approximately 4% market share, with the UAE, Saudi Arabia, and South Africa leading regional adoption. Over 110 new nuclear imaging centers were added between 2021 and 2025 across Gulf states. Technological modernization programs emphasize automation, radiation safety, and centralized isotope preparation. Trade partnerships with European equipment suppliers support system imports and training. A UAE-based healthcare group deployed fully automated systems across five oncology hospitals in 2024. Consumer behavior reflects preference for turnkey automated solutions in large government-funded hospitals, with rising adoption in tertiary care centers.

United States – 31% Market Share: Dominates due to the largest installed base of nuclear medicine facilities and centralized radiopharmacy networks.

Germany – 14% Market Share: Leads through high regulatory enforcement, strong public healthcare funding, and advanced automation adoption in university hospitals.

The Automated Radionuclide Elution System Market exhibits a moderately concentrated but competitive structure, characterized by 10–12 active manufacturers operating across clinical, research, and radiopharmacy settings globally. The combined share of the top five companies—including market leaders and innovation-driven challengers—accounts for approximately 55–60% of total market activity, reflecting substantial influence among established players, while the remainder is segmented among niche and regional OEMs. Competitive positioning focuses heavily on automation reliability, radiation safety features, workflow integration capabilities, and system modularity, rather than price pressure alone, making performance and compliance differentiators.

Comecer (ATS Group) leads the market with around 25% share, supported by its integrated hot-cell and workflow solutions, while Eckert & Ziegler and Trasis remain strong through modular, high-reliability platforms. Companies such as IBA Radiopharma Solutions and Bracco Diagnostics are gaining traction with specialized modules and system compatibility across diverse isotope types. Challenger companies like Mirion Technologies and LemerPax emphasize shielding, ergonomic design, and service support as competitive advantages.

Strategic initiatives across the market in recent years include product launches of compact multi-isotope systems, partnerships for digital monitoring capabilities, and enhanced software for compliance tracking. Innovation trends center on remote process monitoring, predictive maintenance, and enhanced automation of sterility and yield optimization. Mergers and collaborations between equipment manufacturers and major hospital networks are expanding install bases, while partnerships with radiopharmaceutical research institutions are stimulating advanced system validation and adoption.

TemaSinergie

IBA Radiopharma Solutions

Bracco Diagnostics

Mirion Technologies

Trasis

Lemer Pax

Nordion

Tritec Radiopharma

Rotem Industries

Advanced Cyclotron Systems

Radiopharma Solutions

Technology within the Automated Radionuclide Elution System Market is evolving rapidly to meet the exacting demands of clinical safety, workflow efficiency, and regulatory compliance. Core technologies focus on closed-system automation, real-time process monitoring, and integrated shielding and radiation safety features. Several systems now incorporate advanced software modules that automate flow control, elution timing, and pressure regulation to precisely deliver radiopharmaceutical eluates with minimal human intervention. This reduces operator exposure and improves sterility assurance, thereby enhancing operational reliability in high-throughput nuclear medicine departments.

Modern elution platforms increasingly integrate imaging workflow software, enabling synchronization with hospital PACS and radiopharmacy information systems for automated dose tracking and batch documentation. Digital monitoring capabilities include remote status dashboards, automated error detection alerts, and predictive maintenance scheduling, which improve uptime and support large-scale radiopharmacy operations. Some configurations support multi-isotope elution, allowing seamless preparation of 99mTc, Ga-68 and other radionuclides within the same platform, enhancing versatility for mixed clinical workflows and theranostics.

Emerging technological trends include AI-assisted yield optimization algorithms that dynamically adjust flow parameters to maximize radionuclide recovery efficiency and sensor fusion technology for concurrent measurement of radiation dose, fluid dynamics, and system health metrics. These advances strengthen quality control processes while minimizing variability between batches.

Another area of innovation is compact, modular system design that reduces footprint and supports rapid installation in outpatient imaging centers or satellite facilities. Enhanced human–machine interfaces with touchscreen controllers, automated sterilization cycles, and integrated shielding reduce training barriers and improve operator confidence. Collectively, these technologies are enabling safer, more efficient, and more compliant radiopharmaceutical preparation workflows for hospital radiopharmacies, centralized production facilities, and research institutions globally.

• In December 2025, IBA (Ion Beam Applications S.A.) acquired ORA, a Belgian radiochemistry specialist to expand its capabilities in advanced isotope labelling and radiopharmaceutical production technology, reinforcing its integrated solutions for hospitals and global radiopharmacy networks. The deal was valued at €15–20 million and aims to accelerate access to innovative isotope labelling technologies. Source: www.biospace.com

• In March 2025, Actinium Pharmaceuticals announced a supply agreement with Eckert & Ziegler for a reliable supply of Actinium-225 (Ac-225), supporting clinical development of Actimab-A and additional therapeutic programs. The agreement underpins expanded access to high-quality Ac-225 for U.S. and international clinical trials. Source: www.prnewswire.com

• In December 2024, Eckert & Ziegler Radiopharma GmbH commenced production of Actinium-225 (Ac-225) using cyclotron-based methods in collaboration with the Nuclear Physics Institute of the Czech Academy of Sciences. Validation towards GMP-grade Ac-225 is underway to support broader clinical and commercial supply starting in 2025. Source: www.outsourcedpharma.com

• In April 2025, RLS Radiopharmacies partnered with Eckert & Ziegler to expand the production of Ga-68-based radiopharmaceuticals across its U.S. network — equipping all 31 radiopharmacies with advanced GalliaPharm® generators to enhance PET imaging isotope preparation capacity. Source: www.businesswire.com

The scope of an Automated Radionuclide Elution System Market Report encompasses a comprehensive examination of equipment used to automate the elution of radionuclides from generator systems for diagnostic and therapeutic applications. This includes detailed segmentation by isotope/generator type such as 99Mo/99mTc, 68Ge/68Ga, and 82Sr/82Rb systems, as well as system configuration types like standalone automated eluters, integrated hot cell modules, shielded mobile elution carts, and multi-isotope controllers. Geographic coverage spans major regions including North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level insights that profile adoption and infrastructure trends across over 40 national markets.

The report focuses on key industries such as hospital radiopharmacies, centralized commercial radiopharmacies, diagnostic imaging centers, and research institutions, evaluating how workflow automation, regulatory requirements, and safety standards drive system selection and deployment. Technology insights provide analysis of software integration, monitoring systems, and safety enhancements, while competitive landscapes align market positioning of leading and emerging players.

The document also examines current and near-term innovations affecting system design, including digital control platforms, remote operation capabilities, multi-isotope compatibility, and predictive maintenance features. It highlights operational challenges such as capital investment thresholds and technical complexity, alongside emerging opportunities created by nuclear medicine infrastructure expansion and workflow standardization initiatives. The positioned scope supports decision-makers seeking strategic insights into segmentation, competitive dynamics, technology evolution, and regional adoption patterns within automated radionuclide elution systems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 138.7 Million |

| Market Revenue (2033) | USD 258.6 Million |

| CAGR (2026–2033) | 8.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Comecer (ATS Group), Eckert & Ziegler, Trasis, TemaSinergie, IBA Radiopharma Solutions, Bracco Diagnostics, Mirion Technologies, LemerPax, Siemens Healthineers, Nordion, Rotem Industries, Tritec Radiopharma, Advanced Cyclotron Systems, Radiopharma Solutions |

| Customization & Pricing | Available on Request (10% Customization Free) |