Reports

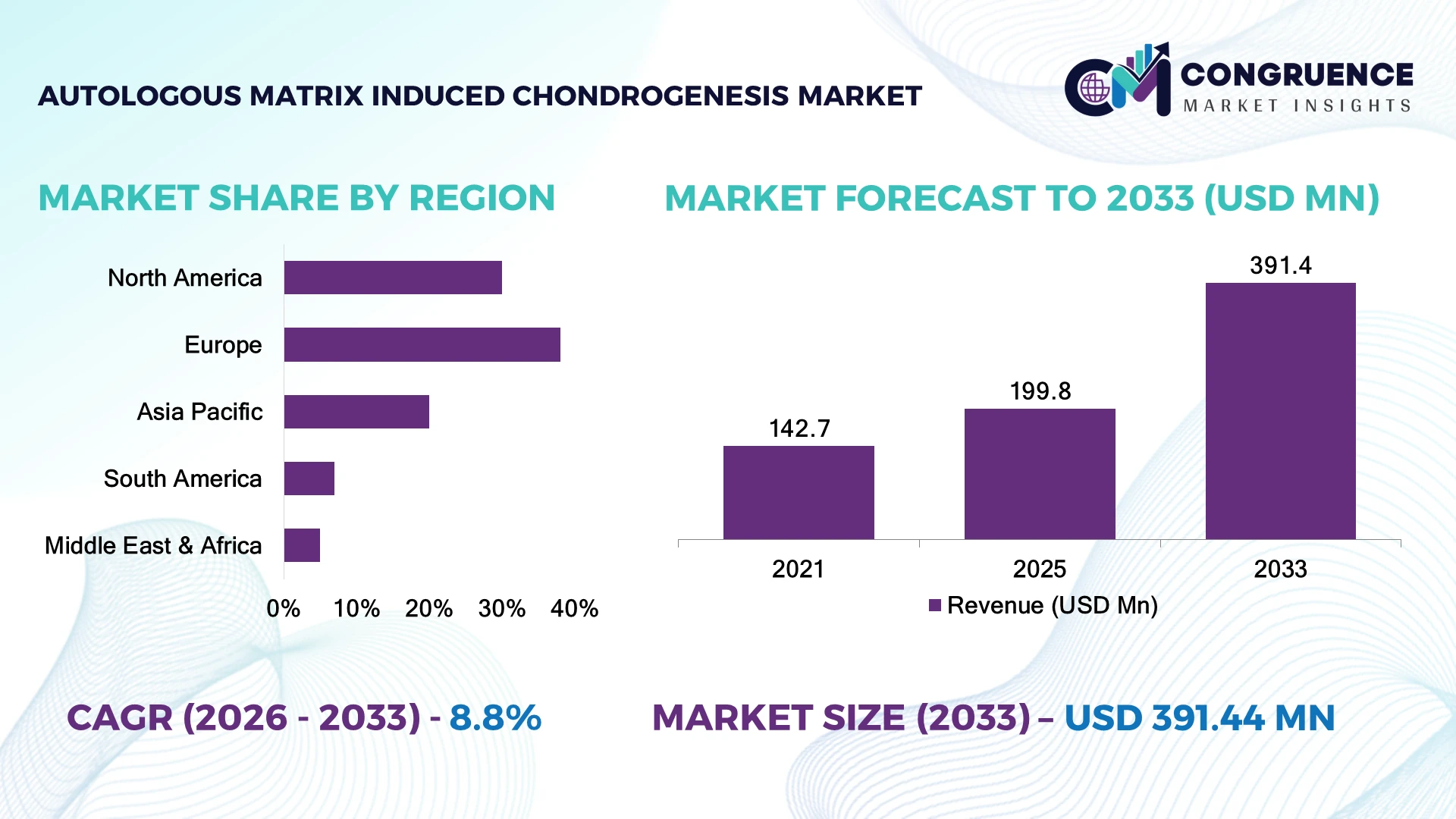

The Global Autologous Matrix-induced Chondrogenesis Market was valued at USD 199.8 Million in 2025 and is anticipated to reach a value of USD 391.4 Million by 2033 expanding at a CAGR of 8.77% between 2026 and 2033. Growth is driven by rising adoption of minimally invasive cartilage repair procedures, increasing sports-related knee injuries, and advancements in biomaterial scaffolds that improve tissue regeneration outcomes.

Germany leads AMIC adoption with over 30% European procedure share, supported by advanced orthopedic infrastructure, regenerative medicine investments, and more than 70% hospital utilization of collagen-based cartilage repair matrices in specialized centers. The United States follows with strong clinical adoption, while Asia-Pacific expands through healthcare modernization initiatives, including China’s regenerative medicine investments. Germany demonstrates higher penetration than emerging Asian markets, where adoption remains below 20%.

Strategic implication says Companies strengthening biomaterial innovation, surgeon partnerships, and regional clinical networks will secure long-term competitive positioning in cartilage regeneration.

Market Size & Growth: USD 199.8 Million (2025) to USD 391.4 Million (2033), driven by advanced cartilage repair technologies and increasing orthopedic procedures.

Top Growth Drivers: Sports injuries (+35%), osteoarthritis cases (+25%), and regenerative medicine adoption (+20%) are key demand catalysts.

Short-Term Forecast: By 2028, clinical adoption of AMIC procedures is expected to improve treatment efficiency by 15% through optimized scaffold designs.

Emerging Technologies: AI-assisted surgical planning, 3D biomaterial scaffolds, and next-generation collagen matrices are reshaping cartilage restoration.

Regional Leaders: North America projected at USD 120 Million, Europe at USD 150 Million, and Asia-Pacific at USD 90 Million, with rising regenerative medicine adoption.

Consumer/End-User Trends: Over 60% of orthopedic specialists prioritize biological repair approaches for younger active patients requiring cartilage restoration.

Pilot/Case Example: A 2023 European orthopedic program using AMIC techniques reported approximately 20% improvement in rehabilitation efficiency through enhanced postoperative protocols.

Competitive Landscape: Geistlich Pharma leads the market with an estimated 25% share, alongside Smith & Nephew, Arthrex, Anika Therapeutics, and Matricel.

Regulatory & ESG Impact: Increased approval pathways for regenerative implants are reducing development timelines by nearly 15% while supporting sustainable biomaterial usage.

Investment & Funding: Over USD 500 Million invested globally in regenerative medicine partnerships, focusing on biomaterials, clinical trials, and orthopedic innovation.

Innovation & Future Outlook: Next-generation scaffolds, personalized cartilage therapies, and digital orthopedic platforms are driving strategic transformation across the market.

Autologous Matrix-induced Chondrogenesis is gaining importance as a high-value regenerative orthopedic solution, particularly in sports medicine, trauma care, and early-stage cartilage degeneration treatment. Innovations in collagen membranes and cell-free regeneration approaches are expanding clinical applications, with approximately 40% of orthopedic research programs now focusing on biological repair alternatives. Operational improvements in medical device supply chains and stricter European regulatory frameworks are accelerating adoption across specialized healthcare systems, creating a transition toward more personalized cartilage restoration strategies.

The Autologous Matrix-induced Chondrogenesis Market is becoming strategically important as orthopedic companies shift from traditional joint replacement approaches toward regenerative solutions that preserve natural tissue function. Increasing healthcare focus on mobility preservation, rising sports injury treatment requirements, and advancements in biomaterial engineering are reshaping investment priorities across orthopedic care.

Supply-chain restructuring in medical device manufacturing is improving access to specialized collagen scaffolds, while regulatory modernization in Europe and North America is accelerating commercialization pathways. Compared with conventional microfracture procedures, AMIC technology provides enhanced structural support through biomaterial membranes, improving cartilage repair consistency and reducing revision risks by approximately 10–15% in selected clinical applications.

Europe remains the leading innovation hub due to established regenerative medicine infrastructure, while North America shows faster commercialization through advanced orthopedic networks and private healthcare investment. Asia-Pacific is expanding through hospital modernization and increasing adoption of minimally invasive procedures.

Over the next 2–3 years, companies are prioritizing surgeon training programs, regional partnerships, and localized manufacturing capabilities. Strategic investments in advanced scaffolds and digital-assisted orthopedic workflows will determine competitive advantage, positioning AMIC as a critical platform within the future regenerative medicine ecosystem.

The increasing preference for biological cartilage restoration procedures is accelerating AMIC adoption, supported by rising sports injuries and osteoarthritis cases. Germany, Switzerland, and the United States are expanding orthopedic regenerative medicine programs, with AMIC procedures accounting for nearly 30% of advanced cartilage repair interventions in selected European centers. Over 60% of orthopedic specialists now prioritize tissue-preserving approaches for younger patients. Advances in collagen scaffolds and minimally invasive techniques are improving clinical outcomes, encouraging companies to expand manufacturing capacity, develop surgeon training partnerships, and invest in next-generation biomaterial platforms. The strategic shift toward outpatient orthopedic care is creating stronger demand for scalable regenerative solutions.

AMIC market scalability remains constrained by elevated procedure costs, specialized surgeon requirements, and dependency on advanced biomaterial availability. Treatment expenses can be 20–30% higher than conventional cartilage repair approaches, limiting adoption in price-sensitive healthcare systems such as emerging markets. Germany and Japan face increasing pressure to optimize reimbursement frameworks as approximately 40% of orthopedic facilities still operate under cost-controlled procurement models. Supply dependency for collagen membranes and specialized scaffolds creates operational challenges, particularly during medical device manufacturing disruptions. Companies are reducing exposure through localized production, multi-year supplier contracts, and diversified biomaterial sourcing strategies to improve cost control and supply continuity.

Emerging opportunities are developing through AI-assisted surgical planning, personalized implants, and improved scaffold technologies that enhance cartilage regeneration accuracy. The United States and South Korea are increasing investments in digital orthopedic platforms, with more than 25% of new orthopedic technology programs incorporating data-driven treatment planning. Advanced collagen matrices and hybrid biomaterials are targeting improved recovery outcomes while reducing rehabilitation requirements by nearly 15% in selected clinical applications. Companies are strengthening market positions through research collaborations, hospital partnerships, and localized innovation centers. A key opportunity lies in integrating AMIC with outpatient surgery models, enabling broader access and improving healthcare system efficiency.

Long-term AMIC market expansion faces challenges related to procedure standardization, surgeon expertise gaps, and inconsistent clinical adoption across healthcare systems. Nearly 35% of orthopedic facilities outside major medical hubs lack dedicated regenerative medicine capabilities, creating uneven deployment patterns. Countries such as India and Brazil experience infrastructure limitations due to limited specialist training networks and restricted access to advanced cartilage repair technologies. Variations in rehabilitation protocols and regulatory requirements also affect treatment consistency and international scalability. Companies must address these barriers through surgeon certification programs, clinical evidence development, technology partnerships, and stronger healthcare infrastructure investments to maintain competitive differentiation.

Biomaterial Innovation Accelerates Advanced collagen membranes and hybrid scaffolds are becoming central to AMIC procedures, with approximately 25% of orthopedic device development programs incorporating next-generation biomaterials. Germany and Switzerland are leading clinical refinement through improved scaffold engineering and manufacturing precision. Companies are expanding R&D partnerships to enhance tissue integration, reduce recovery variability, and improve production scalability amid increasing demand for regenerative orthopedic solutions.

Digital Surgery Integration Expands AI-assisted planning and imaging-supported cartilage repair workflows are gaining adoption, with nearly 20% of advanced orthopedic centers integrating digital tools into surgical preparation. Hospitals in the United States are deploying data-driven approaches to improve procedure accuracy and patient selection. Companies are responding through software partnerships, digital platform investments, and workflow integration strategies that reduce planning time and improve clinical efficiency.

Outpatient Care Models Shift Healthcare systems are moving toward outpatient orthopedic procedures, with ambulatory surgery adoption increasing by approximately 15% in developed markets. This transition is reducing hospital resource dependency and encouraging manufacturers to optimize AMIC product designs for faster clinical workflows. Regulatory changes supporting value-based care in countries such as Germany are accelerating provider partnerships and specialized training programs.

Supply Networks Become Localized Medical device supply-chain restructuring is driving localized biomaterial production, with manufacturers targeting 30% shorter logistics cycles through regional sourcing strategies. Recent global supply disruptions have encouraged companies to diversify suppliers and establish closer production hubs. A non-obvious shift is the growing focus on smaller-scale manufacturing flexibility, enabling faster customization of cartilage repair products for specialized orthopedic centers.

Collagen membranes represent the leading AMIC type, accounting for approximately 55% of market utilization due to strong clinical acceptance, biocompatibility, and established surgeon familiarity. Their scalability, predictable handling characteristics, and integration with microfracture procedures have positioned them as the preferred solution across major orthopedic centers in Germany, the United States, and Japan. Other scaffold-based approaches contribute nearly 30% of adoption, supporting specialized cartilage restoration requirements through improved structural support. Synthetic and hybrid biomaterials represent the fastest-growing type category, expanding as manufacturers focus on enhanced durability, customization, and next-generation regeneration capabilities. Adoption of advanced biomaterials has increased by nearly 20% among research-focused orthopedic institutions. Companies are increasing investments in hybrid scaffold development, clinical collaborations, and product portfolio expansion to capture demand from emerging regenerative medicine applications.

Knee cartilage repair remains the dominant AMIC application, representing approximately 70% of procedures due to high incidence of cartilage defects, sports injuries, and early-stage degenerative conditions. Demand is concentrated among active patients seeking joint-preserving treatments, particularly in Germany, the United States, and Italy. Companies are prioritizing knee-specific product optimization, surgeon education, and hospital partnerships to strengthen adoption. Ankle and other cartilage repair applications represent faster-growing segments, supported by expanding clinical research and improved treatment protocols. These applications account for nearly 25% of procedures and are gaining traction as physicians seek alternatives for complex cartilage defects. Companies are broadening indications, improving rehabilitation pathways, and investing in evidence-based clinical programs to expand utilization beyond traditional knee procedures.

Hospitals represent the leading end-user segment, accounting for approximately 65% of AMIC utilization due to specialized surgical infrastructure, trained orthopedic teams, and access to advanced regenerative medicine facilities. Large hospitals in the United States, Germany, and Japan remain the primary adoption centers, supporting complex cartilage repair procedures and clinical research activities. Companies are strengthening hospital partnerships through training programs, product support services, and institutional agreements. Specialty orthopedic clinics are the fastest-growing end-user group, expanding at nearly 20% adoption growth as outpatient treatment models gain acceptance. These facilities benefit from streamlined workflows, lower operational complexity, and increasing demand for minimally invasive procedures. Companies are targeting specialty clinics through customized support programs, distributor networks, and simplified product delivery models. Research institutes and ambulatory centers continue contributing to innovation through clinical trials and technology validation.

Europe accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2026 and 2033.

North America holds a significant position in the AMIC market, supported by strong orthopedic healthcare systems, advanced surgical facilities, and increasing adoption of cartilage preservation procedures. The region contributes approximately 30% of global demand, with the United States accounting for the majority of procedure volumes due to extensive sports medicine networks and specialized orthopedic centers. More than 60% of leading orthopedic hospitals in the country have incorporated advanced cartilage repair techniques into treatment pathways. Partnerships between medical device companies and healthcare providers are expanding surgeon training programs, improving clinical adoption. Increasing investment in outpatient orthopedic infrastructure is also supporting faster deployment of regenerative procedures.

United States Market Outlook: The United States remains the key North American market due to its large orthopedic patient base, advanced clinical research ecosystem, and strong medical device industry. Over 40% of specialized cartilage repair procedures in major healthcare networks involve biological restoration approaches. Leading hospitals are expanding regenerative medicine capabilities through technology integration, clinical collaborations, and specialized treatment centers.

Europe represents the leading AMIC market due to established regenerative medicine expertise, strong orthopedic research capabilities, and early adoption of collagen-based cartilage repair solutions. Countries including Germany, Switzerland, and Italy demonstrate high procedure concentration, supported by advanced hospital infrastructure and experienced orthopedic specialists. The region accounts for nearly 38% of global market activity, with Germany serving as a major hub for cartilage repair innovation. More than 70% of specialized orthopedic centers in leading European healthcare systems utilize advanced biomaterial-based repair techniques. Regulatory support for innovative medical devices and increasing focus on joint-preserving treatments are encouraging manufacturers to strengthen regional partnerships and expand product portfolios.

Germany Market Outlook: Germany is the most influential European market due to its advanced healthcare infrastructure, medical technology expertise, and strong adoption of regenerative orthopedic procedures. Approximately one-third of European AMIC procedures are performed within German clinical networks. The country’s established medical device manufacturing base supports innovation in collagen membranes, scaffold technologies, and surgeon-focused training initiatives.

Asia-Pacific is emerging as the fastest-expanding AMIC market, supported by healthcare modernization, rising orthopedic treatment demand, and increasing investment in advanced surgical technologies. China, Japan, South Korea, and India are improving hospital infrastructure and expanding access to regenerative medicine procedures. The region currently contributes around 20% of global demand, with adoption concentrated in urban tertiary hospitals. Japan and South Korea are integrating advanced orthopedic technologies into specialized care facilities, while China is increasing investment in medical innovation programs. Companies are strengthening local distribution networks and forming hospital partnerships to improve accessibility. Rising demand for minimally invasive procedures and improved healthcare coverage is creating new opportunities for technology providers.

China Market Outlook: China is positioned as a major growth market due to expanding healthcare infrastructure, increasing orthopedic procedure volumes, and government support for advanced medical technologies. More than 50% of major urban hospitals have upgraded specialized surgical capabilities, creating stronger adoption potential for regenerative cartilage solutions. Domestic partnerships and localized manufacturing initiatives are improving market accessibility.

South America is developing as an emerging AMIC market, supported by improving orthopedic care infrastructure, increasing awareness of biological treatments, and expansion of private healthcare networks. Brazil and Argentina represent the primary adoption centers due to stronger medical facilities and specialist availability. The region contributes approximately 7% of global demand, with adoption concentrated in major metropolitan hospitals. Limited reimbursement coverage and uneven access to advanced surgical technologies continue to influence deployment patterns. Companies are addressing these barriers through distributor partnerships, localized education programs, and targeted product strategies. Increasing collaboration between orthopedic institutes and medical device suppliers is improving clinical familiarity with regenerative procedures.

Brazil Market Outlook: Brazil is the leading South American market due to its large healthcare sector, growing orthopedic specialization, and expanding private hospital networks. Around 45% of advanced orthopedic procedures in major Brazilian cities are performed through specialized healthcare facilities with access to modern surgical technologies. Companies are focusing on training initiatives and regional partnerships to improve AMIC adoption.

Middle East & Africa is gradually adopting AMIC technologies through healthcare modernization projects, private hospital expansion, and investment in advanced orthopedic services. The United Arab Emirates, Saudi Arabia, and South Africa represent the strongest adoption markets due to better infrastructure and specialized medical facilities. The region contributes nearly 5% of global demand, with deployment concentrated in premium hospitals and orthopedic centers. Healthcare investment programs in Gulf countries are supporting modernization of surgical capabilities and partnerships with international medical technology providers. Companies are targeting these markets through specialized training, regional distribution agreements, and premium care collaborations to overcome limited specialist availability.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a strategic Middle Eastern market due to healthcare transformation programs, increasing investment in specialized hospitals, and adoption of advanced surgical technologies. Over 30% of major tertiary hospitals have expanded orthopedic service capabilities through modernization initiatives. International partnerships and medical technology investments are strengthening the country’s position in regenerative healthcare adoption.

The AMIC market features competition between global biomaterial specialists such as Geistlich Pharma, Smith & Nephew, and Anika Therapeutics against regional orthopedic suppliers and regenerative medicine innovators. The top five players collectively account for approximately 55% of market activity, reflecting moderate consolidation. Competition is based on scaffold technology, surgeon adoption, pricing flexibility, supply reliability, and clinical evidence, with premium manufacturers achieving 20–30% stronger hospital preference through established biomaterial performance. Companies are expanding through hospital partnerships, distributor networks, clinical collaborations, and next-generation scaffold innovation. The competitive landscape is shifting toward personalized regenerative solutions, localized manufacturing, and digital-assisted orthopedic workflows. High regulatory requirements, clinical validation needs, and specialized surgeon training remain major entry barriers. Winning companies will combine proven biomaterial platforms, scalable supply chains, strong clinical partnerships, and continuous product innovation to outperform established market participants.

Smith & Nephew plc

Anika Therapeutics, Inc.

Arthrex, Inc.

Matricel GmbH

B. Braun Melsungen AG

Stryker Corporation

Zimmer Biomet Holdings, Inc.

CONMED Corporation

Collagen Matrix, Inc.

RTI Surgical Holdings, Inc.

Orthofix Medical Inc.

Advanced biomaterial scaffolds are becoming central to AMIC innovation, with collagen-based membranes, hybrid matrices, and regenerative coatings improving tissue integration and handling efficiency. Next-generation scaffold designs deliver approximately 15–20% better structural support compared with traditional repair materials. Adoption is increasing across specialized orthopedic centers, where more than 50% of advanced cartilage procedures now incorporate improved biomaterial approaches.

Digital orthopedic technologies are transforming procedure planning through AI-assisted imaging, patient-specific analysis, and workflow optimization. These systems improve surgical preparation efficiency by nearly 20% compared with conventional planning methods. Hospitals and orthopedic networks adopting digital platforms gain better patient selection accuracy, reduced operational delays, and stronger clinical consistency.

Between 2026 and 2028, disruptive technologies including 3D-printed biomaterials, personalized scaffolds, and data-driven rehabilitation platforms will reshape competition. Technology leaders with integrated product ecosystems will benefit most, while traditional suppliers face pressure to modernize. Companies acting now through partnerships, R&D expansion, and digital integration will strengthen their position in regenerative cartilage treatment markets.

July 2025 Anika Therapeutics announced topline results from its U.S. pivotal FastTRACK Phase III study for Hyalofast® cartilage repair scaffold. The product demonstrated improvements over microfracture, with clinical use exceeding 35,000 patients across 35+ countries, supporting regulatory expansion efforts. Source: www.ir.anika.com

March 2025 Smith+Nephew showcased advanced sports medicine and cartilage repair technologies at AAOS 2025, including CARTIHEAL® AGILI-C® and Spatial Surgery solutions. The company highlighted clinical evidence showing improved functional outcomes and expanded treatment options for cartilage restoration procedures. Source: www.smith-nephew.com

October 2025 Arthrex expanded its AutoCart™ cartilage repair ecosystem by introducing additional clinical education resources and procedure-focused training materials. The company reported supporting multiple studies demonstrating meaningful improvements in cartilage repair outcomes, strengthening adoption among orthopedic specialists. Source: www.bio.arthrex.com

May 2025 Smith+Nephew reported new clinical findings for its CARTIHEAL® AGILI-C® implant, showing an 87% lower relative risk of total knee arthroplasty or osteotomy at four years compared with standard surgical care. The development strengthened the company’s position in advanced cartilage restoration solutions.

The Autologous Matrix-induced Chondrogenesis Market Report provides comprehensive coverage of market dynamics, segmentation, competitive positioning, and regional developments from 2026 to 2033. The study analyzes major types including collagen membranes, synthetic scaffolds, and hybrid biomaterials, along with applications such as knee cartilage repair, ankle restoration, and other orthopedic procedures.

The report evaluates adoption patterns across hospitals, specialty orthopedic clinics, research institutes, and ambulatory centers in North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It examines emerging technologies, biomaterial innovations, digital orthopedic integration, and strategic initiatives of key market participants. The analysis supports investment decisions, expansion planning, partnership development, and competitive positioning by identifying evolving demand areas and long-term industry transformation opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 199.8 Million |

| Market Revenue (2033) | USD 391.4 Million |

| CAGR (2026–2033) | 8.77% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Geistlich Pharma AG; Smith & Nephew plc; Anika Therapeutics, Inc.; Arthrex, Inc.; Matricel GmbH; B. Braun Melsungen AG; Stryker Corporation; Zimmer Biomet Holdings, Inc.; CONMED Corporation; Collagen Matrix, Inc.; RTI Surgical Holdings, Inc.; Orthofix Medical Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |