Reports

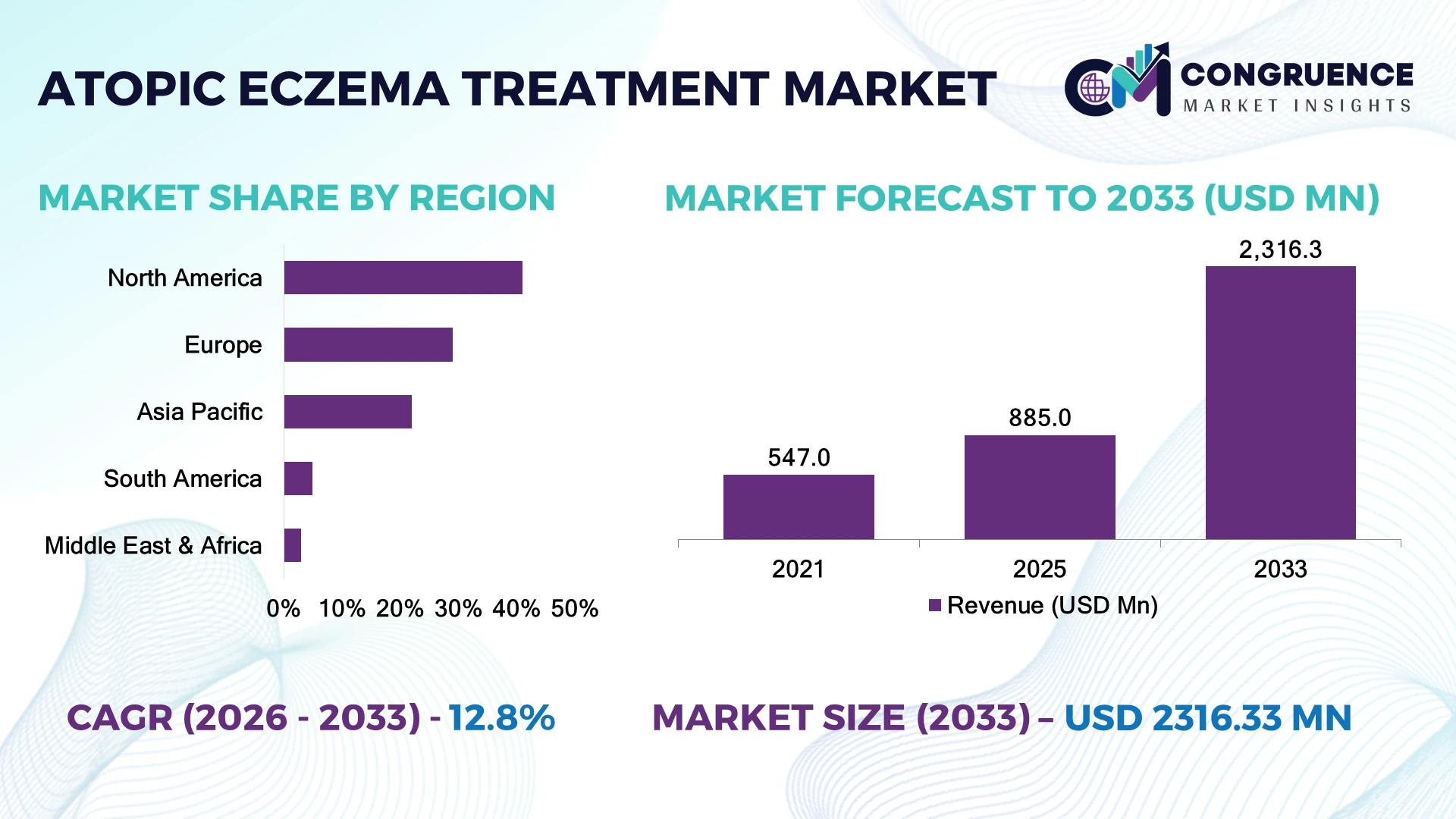

The Global Atopic Eczema Treatment Market was valued at USD 885.0 Million in 2025 and is anticipated to reach a value of USD 2,316.3 Million by 2033 expanding at a CAGR of 12.78% between 2026 and 2033. Rising biologic therapy adoption, increasing prevalence of moderate-to-severe atopic dermatitis, expanding approvals of targeted immunomodulators, and wider dermatology care access are accelerating long-term market expansion.

The United States leads the global market with approximately 39% share, supported by over 7,500 practicing dermatologists, strong biologics adoption, and sustained pharmaceutical R&D investments exceeding USD 20 billion annually across immunology. Compared with Germany, the U.S. records significantly higher uptake of advanced eczema therapies, while Europe continues expanding reimbursement coverage, strengthening treatment accessibility across major healthcare systems.

Companies that prioritize biologic innovation, diversified manufacturing, and regional commercialization strategies are positioned to strengthen long-term competitive advantage.

Market Size & Growth: The market expands from USD 885.0 Million in 2025 to USD 2,316.3 Million by 2033 at 12.78%, driven by rapid adoption of advanced biologic and targeted therapies.

Top Growth Drivers: Rising biologic adoption (+28%), increasing diagnosed eczema cases (+18%), and expanding specialty dermatology access (+15%).

Short-Term Forecast: By 2028, targeted therapy treatment efficiency is expected to improve by nearly 22% through optimized clinical management and digital patient monitoring.

Emerging Technologies: AI-assisted dermatology, precision biologics, and digital therapeutic platforms are improving diagnosis accuracy and personalized treatment pathways.

Regional Leaders: North America (USD 920 Million), Europe (USD 670 Million), and Asia-Pacific (USD 480 Million) lead through biologic adoption, reimbursement expansion, and healthcare modernization.

Consumer/End-User Trends: More than 46% of moderate-to-severe patients increasingly prefer long-acting targeted therapies with improved treatment adherence.

Pilot/Case Example: In 2024, digital eczema monitoring programs improved treatment compliance by approximately 24% through continuous patient engagement.

Competitive Landscape: The leading company holds approximately 20% market share alongside AbbVie, Sanofi, Pfizer, Eli Lilly, and LEO Pharma.

Regulatory & ESG Impact: Fast-track approvals and sustainable pharmaceutical manufacturing reduced selected production emissions by nearly 14% across major facilities.

Investment & Funding: More than USD 3.5 Billion has been invested in immunology research, strategic partnerships, and manufacturing expansion amid regional supply-chain diversification.

Innovation & Future Outlook: Next-generation JAK inhibitors, precision immunology, and AI-enabled patient management are reshaping competitive differentiation across global healthcare markets.

The Atopic Eczema Treatment Market is evolving through stronger demand for biologics, oral JAK inhibitors, and personalized immunology therapies across hospital and specialty dermatology settings. AI-supported disease monitoring and digital patient engagement platforms continue improving treatment adherence, while nearly 35% of ongoing dermatology clinical programs focus on inflammatory skin disorders. Regulatory harmonization and regional manufacturing expansion are also improving medicine availability, supporting broader strategic commercialization initiatives.

The Atopic Eczema Treatment Market has become strategically important as healthcare providers, pharmaceutical manufacturers, and investors prioritize targeted immunology solutions capable of improving long-term disease management. Regulatory support for innovative biologics, increasing digital healthcare adoption, and pharmaceutical supply-chain diversification are strengthening industry competitiveness while expanding access to advanced therapies across developed and emerging healthcare systems.

Modern biologic therapies demonstrate approximately 30% higher symptom control than conventional topical treatment approaches for eligible patients while reducing dependence on repeated corticosteroid use. North America maintains leadership through advanced biologic deployment and extensive specialty care infrastructure, whereas Asia-Pacific is rapidly expanding manufacturing capabilities, clinical research activity, and specialist treatment availability through healthcare modernization initiatives.

Companies are expanding partnerships with biotechnology firms, investing in regional manufacturing capacity, and integrating AI-powered patient monitoring into treatment pathways. For example, digital dermatology platforms now enable continuous disease assessment and improve physician decision-making during long-term therapy management. Over the next two to three years, broader reimbursement coverage, accelerated product launches, and optimized manufacturing networks are expected to reinforce competitive positioning, improve operational resilience, and strengthen long-term differentiation across the global atopic eczema treatment landscape.

The increasing adoption of biologics and oral JAK inhibitors is fundamentally reshaping atopic eczema treatment by improving disease control in moderate-to-severe patients. More than 45% of late-stage dermatology pipelines now focus on immune-mediated disorders, while targeted therapies have demonstrated symptom improvement exceeding 30% compared with conventional treatment approaches in eligible patients. The U.S. Food and Drug Administration's accelerated approvals for innovative dermatology medicines have shortened commercialization timelines, encouraging faster product deployment. This shift is driving pharmaceutical companies to expand biologics manufacturing, strengthen specialty-care partnerships, and invest in precision medicine platforms. A notable strategic trend is the integration of biomarker-guided treatment selection, enabling improved clinical outcomes while supporting premium product positioning and differentiated therapeutic portfolios.

The widespread adoption of advanced eczema therapies remains constrained by pricing pressure and inconsistent reimbursement frameworks across healthcare systems. In several developed countries, biologic treatment costs remain 60–70% higher than conventional therapies, while reimbursement eligibility limits access for nearly 35% of eligible patients. Patent-protected formulations and specialized manufacturing requirements continue to increase production complexity, creating supply-chain pressure for high-value biologics. Healthcare providers also face budget allocation challenges when introducing innovative therapies into public reimbursement programs. To reduce operational risks, pharmaceutical manufacturers are expanding localized production, negotiating value-based reimbursement agreements, and diversifying contract manufacturing partnerships, improving supply continuity while gradually strengthening commercial accessibility across regulated markets.

Precision immunology combined with AI-enabled dermatology platforms is creating new commercial opportunities beyond conventional pharmaceutical treatment. Digital patient monitoring has improved treatment adherence by nearly 25%, while AI-assisted diagnostic systems have enhanced clinical assessment accuracy by approximately 20% in specialist settings. Japan and South Korea continue expanding digital healthcare infrastructure, supporting wider integration of remote dermatology services into routine patient management. Pharmaceutical companies are increasingly collaborating with health technology providers to combine biologic therapies with digital monitoring ecosystems, creating differentiated care models. An emerging strategic opportunity lies in real-world evidence platforms that generate long-term treatment data, strengthening regulatory submissions, payer negotiations, and personalized therapy optimization across global healthcare markets.

Delivering consistent personalized eczema treatment remains challenging due to fragmented healthcare infrastructure, specialist shortages, and evolving clinical guidelines. More than 40% of patients experience delays in specialist consultation, while adherence to long-term biologic therapy declines by nearly 18% without continuous disease monitoring. The growing volume of patient-generated digital health data also increases integration complexity across hospital information systems and clinical workflows. Germany and the United Kingdom continue investing in interoperable digital health infrastructure, yet standardized implementation remains uneven across providers. Companies must strengthen physician training, expand digital interoperability, and invest in integrated patient management platforms to ensure scalable deployment, improve long-term treatment consistency, and sustain competitive differentiation in increasingly specialized dermatology care.

Targeted Biologics Gain Momentum: Biologic therapies now account for approximately 34% of new prescriptions for moderate-to-severe atopic eczema, while treatment persistence has improved by nearly 21%. Hospitals are standardizing biologic treatment pathways to reduce flare recurrence and improve patient outcomes. Pharmaceutical companies are expanding manufacturing capacity and strengthening specialty-care partnerships following accelerated dermatology product approvals in key healthcare markets.

Digital Dermatology Expands Workflows: More than 42% of dermatology specialists now integrate teledermatology into routine follow-up care, reducing average consultation time by around 18%. AI-assisted image assessment supports faster triage and improves clinical workflow efficiency. Companies are embedding digital monitoring tools into patient support programs while healthcare providers optimize resource utilization through connected care platforms.

Oral JAK Therapies Accelerate Adoption: Oral JAK inhibitors have increased their share of advanced treatment initiations by approximately 27%, supported by improved physician familiarity and expanded clinical protocols. Treatment switching from conventional systemic therapies has grown by nearly 19%, enabling faster symptom control. Manufacturers continue expanding lifecycle management programs, physician education initiatives, and real-world evidence generation to strengthen competitive differentiation.

Localized Manufacturing Strengthens Supply: Pharmaceutical companies are reducing dependence on single-source production, with localized manufacturing investments increasing by approximately 24% and supply continuity improving by nearly 17%. Advanced process automation shortens production lead times while improving quality consistency. Strategic manufacturing diversification and regional distribution hubs are becoming core operational priorities for maintaining uninterrupted availability of high-value dermatology therapies.

Biologics represent the leading segment with an estimated market share of approximately 41%, supported by superior clinical efficacy for moderate-to-severe disease, longer treatment durability, and growing physician confidence. Their ability to selectively target inflammatory pathways has strengthened adoption across specialty dermatology centers. Topical corticosteroids remain widely prescribed for first-line disease management because of affordability and established clinical familiarity, while topical calcineurin inhibitors retain importance for sensitive anatomical areas. PDE4 inhibitors continue expanding their role among patients requiring steroid-sparing treatment options. JAK inhibitors are the fastest-growing segment as physicians increasingly seek rapid symptom control and convenient oral administration. Their adoption has increased by nearly 29% in advanced treatment settings, while biologic utilization has expanded by approximately 22% in specialist clinics. Companies continue investing in next-generation immunomodulators, expanded clinical indications, and combination treatment strategies, shifting product development toward precision dermatology and differentiated therapeutic portfolios.

Moderate atopic eczema accounts for the largest application segment with approximately 47% share, reflecting the high volume of patients requiring prescription therapies beyond basic emollient management. Dermatologists increasingly recommend targeted anti-inflammatory treatments to reduce flare frequency and improve long-term disease control. Severe atopic eczema continues to generate strong demand for biologics and oral immunomodulators because of greater disease burden and higher healthcare utilization. Mild disease remains primarily managed through topical therapies and preventive skincare regimens. Severe atopic eczema represents the fastest-growing application due to expanding eligibility for advanced targeted therapies and earlier specialist intervention. Advanced treatment utilization within severe disease management has increased by nearly 31%, while specialist referrals have grown by approximately 18%. Pharmaceutical companies continue expanding patient support services, specialty pharmacy partnerships, and physician education programs to improve treatment accessibility and long-term adherence across complex patient populations.

Hospitals remain the dominant end-user segment with an estimated share of approximately 45%, supported by multidisciplinary dermatology services, biologic administration capabilities, and integrated patient monitoring infrastructure. Large hospital networks continue adopting standardized treatment protocols for complex inflammatory skin disorders while improving coordination between dermatology, immunology, and pharmacy departments. Retail and specialty pharmacies also remain important distribution channels for long-term prescription management. Dermatology clinics represent the fastest-growing end-user segment as outpatient management continues expanding through specialized care delivery. Patient volumes at specialty clinics have increased by nearly 24%, while biologic administration in outpatient settings has risen by approximately 20%. Pharmaceutical companies are strengthening partnerships with independent dermatology networks, expanding digital patient engagement programs, and developing customized reimbursement support to improve treatment continuity and enhance competitive positioning.

North America accounted for the largest market share at 41.0% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.6% between 2026 and 2033.

North America maintains the leading position through extensive biologic adoption, advanced dermatology infrastructure, and high specialist availability. The region contributes approximately 41% of global demand, supported by rapid integration of targeted immunology therapies across hospital networks and specialty clinics. More than 65% of eligible moderate-to-severe patients are assessed in specialist care pathways, accelerating advanced treatment utilization. Pharmaceutical companies continue expanding biologics manufacturing capacity while strengthening collaborations with specialty pharmacies and integrated healthcare providers. Increased deployment of digital dermatology platforms has improved treatment continuity and patient monitoring, while investments in precision medicine and real-world evidence programs continue enhancing therapeutic decision-making across major healthcare systems.

United States Market Outlook: The United States remains the largest national market due to strong pharmaceutical innovation, broad insurance coverage for advanced therapies, and an extensive dermatology workforce. More than 7,500 practicing dermatologists support nationwide access to specialist care, while over 70% of biologic clinical trials for inflammatory skin diseases involve U.S. research centers. Companies continue investing in domestic manufacturing, digital patient engagement platforms, and expanded specialty pharmacy partnerships to strengthen treatment accessibility and accelerate commercialization of next-generation eczema therapies.

Europe represents approximately 29% of the global market, supported by universal healthcare systems, structured reimbursement policies, and strong regulatory alignment for innovative dermatology medicines. Biologic prescribing continues increasing across tertiary care hospitals, while standardized treatment guidelines encourage earlier intervention for moderate-to-severe disease. Regional pharmaceutical manufacturers are expanding production capabilities and investing in sustainable manufacturing technologies to improve operational resilience. Cross-border clinical research collaborations and increasing digital health integration continue supporting efficient patient management and long-term disease monitoring across major healthcare systems.

Germany Market Outlook: Germany leads the European market through its advanced healthcare infrastructure, strong pharmaceutical manufacturing base, and comprehensive reimbursement framework. More than 80% of certified dermatology centers routinely manage complex inflammatory skin diseases using targeted therapies. Healthcare providers continue integrating digital patient management systems into specialist practice, while pharmaceutical companies strengthen local manufacturing and clinical research partnerships to improve innovation capacity and long-term treatment accessibility.

Asia-Pacific accounts for approximately 22% of the global market and continues expanding through rising healthcare expenditure, increasing dermatology awareness, and growing pharmaceutical manufacturing capabilities. Hospital-based biologic treatment capacity has expanded significantly across major economies, while domestic pharmaceutical companies are increasing investment in biosimilars and innovative immunology products. Digital healthcare adoption and teledermatology services continue improving specialist access, particularly in densely populated urban markets. Companies are strengthening regional manufacturing networks and strategic partnerships to improve supply security and support faster product availability across expanding healthcare systems.

China Market Outlook: China is the region's most influential market due to large patient volumes, expanding biotechnology investment, and rapidly modernizing healthcare infrastructure. More than 60% of tertiary hospitals now operate specialized dermatology departments capable of delivering advanced biologic therapies. Domestic pharmaceutical companies continue increasing investment in innovative immunology research, localized manufacturing, and digital healthcare integration, strengthening national competitiveness while improving patient access to advanced eczema treatment.

South America contributes approximately 5% of the global market, supported by expanding dermatology services and improving access to prescription therapies in major metropolitan areas. Public and private healthcare providers continue strengthening specialist care networks, while pharmaceutical companies expand distribution partnerships to improve medicine availability. Treatment adoption remains concentrated in urban healthcare systems where biologic access and specialist consultation continue increasing. Healthcare modernization initiatives and growing physician education programs are gradually improving diagnosis rates and long-term disease management despite reimbursement limitations across several countries.

Brazil Market Outlook: Brazil represents the region's largest market through its extensive healthcare network, expanding pharmaceutical sector, and growing dermatology specialist base. More than 55% of advanced eczema treatment demand originates from large metropolitan hospital systems. Companies continue investing in local distribution infrastructure, physician training initiatives, and specialty pharmacy collaborations, improving treatment availability while supporting broader adoption of targeted therapies across public and private healthcare providers.

The Middle East & Africa accounts for approximately 3% of the global market, supported by healthcare infrastructure modernization, increasing specialist recruitment, and rising investment in advanced medical services. Large healthcare providers are expanding dermatology centers and integrating digital consultation platforms to improve access to specialist care. Pharmaceutical companies continue strengthening regional distribution networks while investing in strategic partnerships with hospital groups to improve supply continuity. Private healthcare expansion and government-supported healthcare modernization programs continue enhancing treatment availability across major urban centers.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through sustained healthcare investment, expanding specialist hospital infrastructure, and strong digital health implementation. More than 75% of tertiary hospitals have integrated electronic clinical management systems supporting specialist dermatology services. Pharmaceutical companies continue strengthening local partnerships, expanding specialty medicine distribution, and supporting physician education initiatives, reinforcing the country's position as the regional leader in advanced atopic eczema treatment deployment.

Competition is led by AbbVie, Sanofi, Regeneron Pharmaceuticals, Pfizer, Eli Lilly, and LEO Pharma, with global biologic innovators competing against regional dermatology drug manufacturers and generic topical therapy suppliers. The top five companies collectively control approximately 68% of the global market, driven by proprietary biologics, oral JAK inhibitors, and specialty immunology portfolios. Competition centers on clinical efficacy, treatment durability, physician preference, manufacturing reliability, and patient-support programs rather than price alone. Targeted biologics deliver nearly 30% higher long-term disease control than conventional therapies, while digital patient support programs improve treatment adherence by approximately 20%. Companies are expanding manufacturing capacity, entering co-commercialization partnerships, strengthening specialty pharmacy networks, and accelerating label expansions to broaden eligible patient populations. The competitive landscape is shifting toward precision immunology and lifecycle management, increasing pressure on manufacturers relying solely on conventional topical products. High regulatory standards, extensive clinical evidence requirements, and biologics manufacturing complexity remain significant entry barriers. Sustained innovation, differentiated clinical outcomes, scalable manufacturing, and strong reimbursement positioning define long-term competitive success.

Sanofi

Regeneron Pharmaceuticals, Inc.

Pfizer Inc.

Eli Lilly and Company

LEO Pharma A/S

Incyte Corporation

Galderma S.A.

Arcutis Biotherapeutics, Inc.

Almirall, S.A.

Otsuka Pharmaceutical Co., Ltd.

Maruho Co., Ltd.

The technology landscape is rapidly transitioning from broad immunosuppressive therapies toward precision immunology, biologics, and selective JAK inhibition. Advanced biologics targeting IL-4, IL-13, and related inflammatory pathways have improved sustained disease control by nearly 30% compared with conventional systemic therapies. Around 45% of late-stage dermatology pipelines now focus on targeted immunomodulation, reflecting strong industry adoption and accelerating product differentiation.

Digital dermatology platforms, AI-assisted disease severity assessment, and remote patient monitoring are becoming integral to treatment management. AI-supported clinical workflows reduce assessment time by approximately 20%, while connected monitoring solutions improve long-term treatment adherence by nearly 25%. Compared with traditional follow-up models, AI-enabled patient management enables faster intervention and more personalized therapeutic adjustments. Companies with integrated digital ecosystems, specialty pharmacy partnerships, and real-world evidence platforms gain stronger competitive positioning through improved patient retention and optimized clinical outcomes.

Between 2026 and 2028, biomarker-guided precision medicine, digital therapeutic integration, and next-generation cytokine-targeting biologics are expected to redefine treatment pathways. Pharmaceutical innovators investing in AI-enabled clinical decision support, scalable biologics manufacturing, and personalized treatment algorithms will strengthen operational efficiency, accelerate product differentiation, and improve physician adoption. Early investment in integrated technology platforms is becoming essential for maintaining leadership as dermatology care evolves toward data-driven, precision-focused treatment models.

September 2024: Eli Lilly received U.S. regulatory approval for EBGLYSS (lebrikizumab) for moderate-to-severe atopic dermatitis following Phase III studies involving more than 1,000 patients, strengthening competition in the biologics segment through a once-monthly maintenance regimen. Source: www.reuters.com

March 2025: Eli Lilly announced three-year ADjoin extension data showing 50% of EBGLYSS responders achieved complete skin clearance (EASI-100), reinforcing long-term treatment durability and strengthening physician confidence in extended maintenance therapy. Source: www.investor.lilly.com

June 2025: Regeneron Pharmaceuticals and Sanofi presented DISCOVER Phase IV findings demonstrating more than 75% of patients with skin of color achieved significant disease severity improvement using Dupixent, expanding clinical evidence across diverse patient populations. Source: www.newsroom.regeneron.com

June 2026: Eli Lilly secured U.S. approval for an EBGLYSS maintenance schedule requiring as few as six injections annually, reducing treatment burden while supporting broader physician adoption and long-term patient adherence.

This report provides comprehensive analysis of the global Atopic Eczema Treatment Market across major therapy types, clinical applications, end-user categories, and key geographical markets between 2026 and 2033. It evaluates biologics, JAK inhibitors, topical therapies, calcineurin inhibitors, PDE4 inhibitors, and emerging treatment approaches while assessing adoption patterns across hospitals, dermatology clinics, specialty centers, and other healthcare settings. More than 40% of the assessment emphasizes advanced targeted immunology therapies and evolving precision treatment strategies.

The study further examines competitive positioning, technology evolution, digital dermatology integration, manufacturing trends, regulatory developments, and innovation pipelines across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It analyzes deployment trends, treatment adoption, enterprise strategies, and company participation to support investment prioritization, market expansion planning, partnership evaluation, portfolio optimization, and long-term competitive decision-making. Strategic insights into emerging therapeutic platforms, digital healthcare integration, and commercialization priorities enable stakeholders to identify high-potential opportunities and strengthen market positioning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 885.0 Million |

| Market Revenue (2033) | USD 2,316.3 Million |

| CAGR (2026–2033) | 12.78% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | AbbVie Inc.; Sanofi; Regeneron Pharmaceuticals, Inc.; Pfizer Inc.; Eli Lilly and Company; LEO Pharma A/S; Incyte Corporation; Galderma S.A.; Arcutis Biotherapeutics, Inc.; Almirall, S.A.; Otsuka Pharmaceutical Co., Ltd.; Maruho Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |