Reports

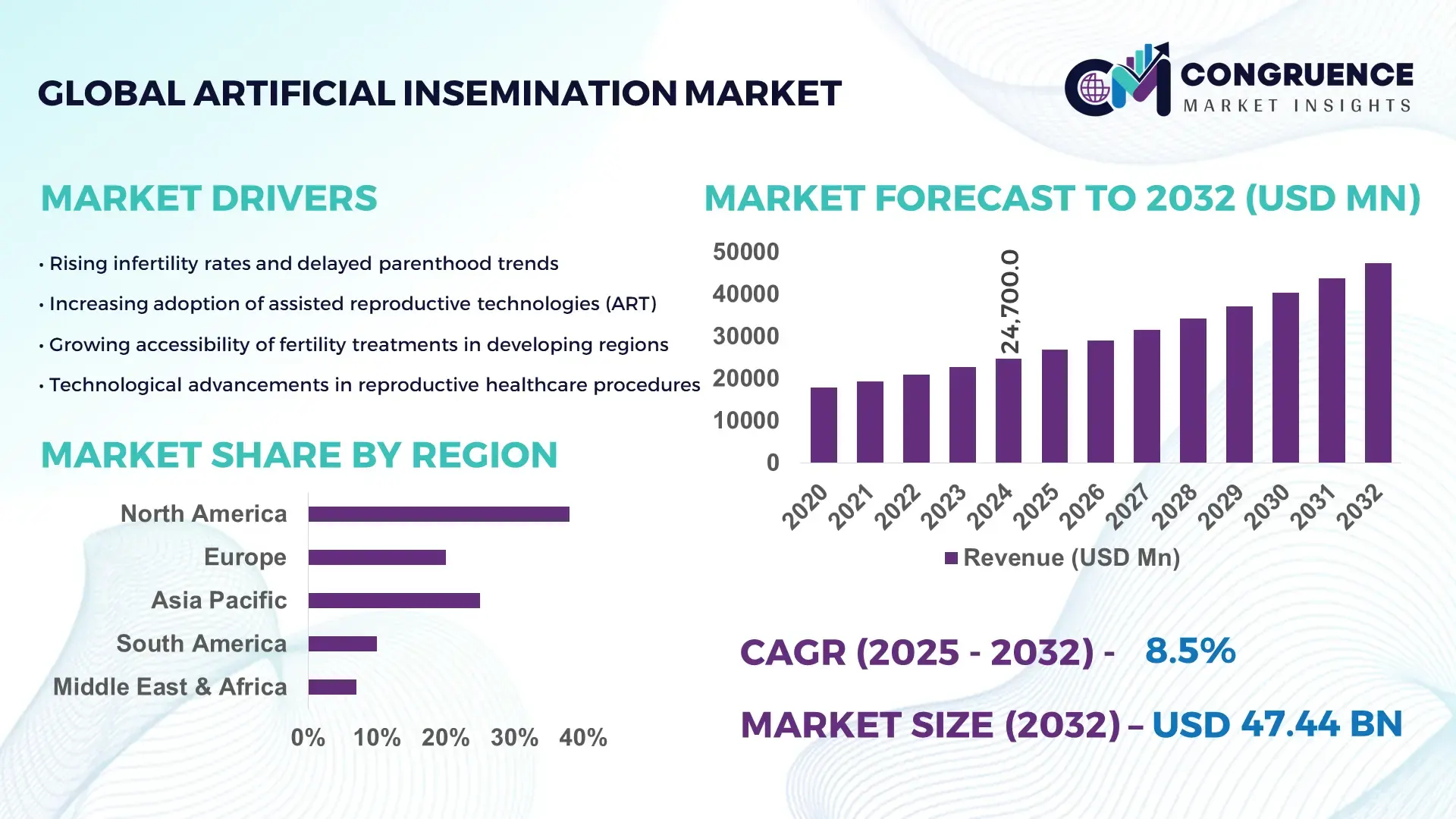

The Global Artificial Insemination Market was valued at USD 24,700 Million in 2024 and is anticipated to reach a value of USD 51,471 Million by 2032, expanding at a CAGR of 8.5% between 2025 and 2032. This growth is driven primarily by rising infertility rates, increased investment in fertility clinics, and rapid technological advancement in reproductive medicine.

In North America, the leading region in this market, there is a particularly high level of investment in fertility infrastructure combined with advanced sperm-preparation technologies. Over 1,500 clinics across the U.S. perform intrauterine insemination (IUI) procedures, and research centers are increasingly deploying microfluidic sperm-sorting platforms. Public and private funding for ART (Assisted Reproductive Technology) in Canada and the U.S. exceeds USD 1.2 billion annually, while peer-reviewed studies report success rate improvements of 10–15% due to next-generation sperm handling and cryopreservation techniques.

Market Size & Growth: Valued at USD 24,700 M in 2024, projected to hit USD 51,471 M by 2032 — CAGR of 8.5%, fueled by infertility prevalence and clinic expansion.

Top Growth Drivers: Rising infertility incidence (~40 %), increased adoption of donor sperm (~25 %), and surge in home-insemination kits (~20 %).

Short-Term Forecast: By 2028, AI procedure costs could decrease by ~12% due to process efficiencies and economies of scale.

Emerging Technologies: Microfluidic sperm-sorting, AI-driven sperm viability analysis, and novel cryopreservation media.

Regional Leaders: North America: Projected to exceed USD 18,000 M by 2032, driven by mature fertility markets. Asia-Pacific: Estimated at USD 10,500 M by 2032, with rapid adoption in China and India. Europe: Forecast to reach USD 7,800 M by 2032, supported by strong reimbursement policies and fertility tourism.

Consumer/End-User Trends: Growing use among single parents and LGBTQ+ individuals, and increased preference for minimally invasive home-insemination solutions.

Pilot or Case Example: In 2027, a fertility clinic in California reported a 14% increase in IUI success rates after integrating microfluidic sperm sorting.

Competitive Landscape: Leading player holds around 22–25% share; major competitors include Irvine Scientific, Cook Medical, FUJIFILM Irvine Scientific, Rinovum Women’s Health, and Rocket Medical.

Regulatory & ESG Impact: Regulatory frameworks such as FDA guidelines on donor-sperm screening and ethical donor use; sustainability focus on reducing disposable plastic use in insemination kits.

Investment & Funding Patterns: Recent funding of USD 350 M in fertility clinics and ART R&D; growing venture capital in at-home insemination platforms.

Innovation & Future Outlook: Integration of genomics for sperm quality prediction, development of portable AI-based IUI devices, and expansion into underserved regions through telemedicine-enabled fertility care.

The artificial insemination market spans human fertility treatment and animal breeding. In the human fertility segment, intrauterine insemination (IUI) remains dominant, supported by improvements in sperm-preparation protocols and home-conception kits. In animal husbandry, AI continues to be integral for genetic improvement in livestock, especially in cattle and swine, backed by cost-effective straws and cryo-storage innovations. Regulatory support—such as eased donor screening rules and tax benefits for fertility clinics—augments adoption, while economic factors such as delayed parenthood and rising infertility drive demand. Technologically, the market is shifting toward microfluidic systems, AI-assisted sperm viability analysis, and high-throughput cryopreservation. Regionally, North America leads in both clinic density and funding, Asia-Pacific is scaling rapidly with China and India investing heavily in fertility infrastructure, and Europe benefits from medical tourism and strong reimbursement policies. Looking ahead, emerging trends include decentralized fertility care, precision ART using genomics, and the commercialization of affordable at-home insemination platforms.

The strategic relevance of the Artificial Insemination market lies in its ability to align demographic changes, technological advancements, and clinical efficiency targets within both human fertility and animal breeding ecosystems. With global infertility affecting more than 15% of couples and livestock productivity goals rising sharply, the market is shifting toward precision-driven insemination processes supported by automated laboratory systems, microfluidic sperm-sorting, and AI-assisted viability analysis. A comparative benchmark shows that microfluidic sperm-selection technology delivers up to 22% improvement in motile sperm recovery compared to conventional density-gradient centrifugation, enhancing procedural success across high-volume clinics. Regionally, North America dominates in volume, while Europe leads in adoption with over 48% of fertility clinics integrating digital workflow systems to streamline insemination cycles. In the next short-term window, By 2028, AI-enabled sperm morphology scoring is expected to improve screening accuracy by 18%, reducing cycle failures and lowering per-patient treatment fatigue. Compliance also plays a critical role, with firms committing to ESG-centered laboratory operations through 30% reduction in consumable waste by 2030 via recyclable plastics and optimized cryo-storage. A recent micro-scenario demonstrates measurable impact: In 2024, a leading U.S. fertility network achieved a 16% increase in insemination efficiency after adopting automated sperm-prep robotics across seven facilities. Collectively, these advancements position the Artificial Insemination Market as a cornerstone for resilience, regulatory alignment, and long-term sustainable growth.

The rising focus on advanced reproductive technologies is significantly boosting growth in the Artificial Insemination market by elevating clinical accuracy, reducing procedural time, and increasing cycle success rates. Technologies such as microfluidic sperm-sorting improve viable sperm selection by up to 20%, enhancing overall treatment outcomes. Automated sperm-preparation systems reduce manual variability, enabling clinics to process up to 30% more samples per hour. In livestock applications, genomic selection tools and precision breeding kits are accelerating breeding cycles, allowing high-yield herds to expand genetic improvement programs. The rapid adoption of digital fertility monitoring, with usage increasing by more than 35% globally, further drives procedural planning and insemination timing accuracy. Collectively, these advancements strengthen operational efficiency across fertility centers and breeding facilities while improving patient and producer outcomes.

The Artificial Insemination market faces notable restraints stemming from procedural complexities, regulatory compliance demands, and variability in global clinical standards. Many fertility centers require highly trained embryologists and technicians, and shortages in skilled reproductive specialists have increased by over 18% in several regions. Strict donor-screening protocols, extended approval cycles for insemination products, and requirements for long-term sample traceability further elevate operational overheads. In animal breeding, cross-border regulations on semen transport, biosecurity protocols, and genetic material certification slow market expansion. Additionally, inconsistent availability of high-grade consumables and laboratory equipment contributes to procedural delays and reduced efficiency. These constraints collectively slow scalability and add to procedural burdens across clinical and agricultural environments.

The rapid expansion of digital fertility ecosystems is creating substantial opportunities for the Artificial Insemination market by integrating teleconsultation, remote cycle monitoring, and AI-driven diagnostics into mainstream fertility workflows. With more than 40% of fertility patients engaging with digital platforms for cycle tracking and consultation, clinics can expand reach without geographically intensive infrastructure. Remote insemination kits, paired with app-based timing algorithms, enable up to 15% improvement in insemination accuracy for home users. Livestock producers benefit from IoT-based heat detection systems, which achieve more than 90% estrus-detection accuracy, improving breeding efficiency. Additional opportunity lies in the development of personalized insemination protocols combining genomics and machine learning, enabling tailored sperm-selection pathways and optimized cycle outcomes. These innovations open new channels for revenue expansion while increasing accessibility and procedural success.

Rising laboratory operational costs and technical variability pose major challenges for the Artificial Insemination market, especially as fertility centers and breeding facilities expand their technology portfolios. High maintenance requirements for automated sperm-analysis systems and cryogenic storage units increase annual operational expenditure by an estimated 12–18%. Technical variability across labs, including differences in sperm-preparation techniques and insemination timing protocols, leads to inconsistent success outcomes, hindering standardization efforts. In livestock breeding, uneven access to high-quality semen storage infrastructure, climate-controlled transportation, and disease-free certification adds complexity and delay. Furthermore, increasing costs of disposable lab-grade consumables and specialized insemination media increase financial pressures on smaller clinics and producers. These challenges collectively impact service reliability, cost efficiency, and scalability across global markets.

• Expansion of AI-Integrated Fertility Technologies: AI-enabled sperm analysis platforms are increasingly being adopted, with more than 42% of fertility clinics incorporating automated morphology scoring tools to enhance evaluation accuracy. These systems deliver up to 18% improvement in identifying viable sperm compared to manual microscopic assessment. Additionally, deep-learning models used in ovulation prediction now support cycle-timing precision improvements of nearly 20%, enabling more efficient insemination planning across both clinical and home-use settings. The rise of AI-linked diagnostic algorithms continues to accelerate workflow standardization and procedural success rates.

• Growth in Home-Based Insemination Solutions: Home-insemination kits have witnessed notable adoption, with usage rising by approximately 27% over the last two years. Enhanced device ergonomics and improved sterile delivery mechanisms now offer up to 15% greater insemination accuracy for at-home users. Consumer demand is also influenced by expanding accessibility, as more than 30% of new fertility entrants prefer privacy-centric solutions. Manufacturers are responding by integrating app-enabled monitoring systems that deliver real-time guidance and cycle reminders, boosting compliance and usage consistency.

• Advanced Cryopreservation and Storage Innovations: Cryopreservation technologies have evolved rapidly, with new cryo-media formulations improving post-thaw motility by 12–16%. Facilities deploying digitally controlled cryogenic tanks report a 22% reduction in sample degradation incidents due to enhanced temperature monitoring. Automated inventory-tracking systems have achieved 25% improvement in logistical accuracy, minimizing handling errors and optimizing storage turnover. These advancements strengthen long-term genetic preservation for both human fertility programs and large-scale livestock breeding operations.

• Precision Breeding Technologies in Livestock AI Programs: Livestock-focused artificial insemination is experiencing strong technological upgrades, with genomic selection adoption now exceeding 48% in high-yield cattle operations. Precision estrus-detection sensors deliver up to 92% accuracy, improving insemination timing and boosting conception rates by nearly 14%. Automated semen-dosing and distribution systems have also reduced material wastage by 10–12% across commercial breeding sites. These innovations are significantly improving productivity, enabling producers to streamline genetic enhancement programs and meet rising protein-demand pressures in global agriculture.

The Artificial Insemination market is organized into clearly defined segments encompassing types, applications, and end-user groups, each contributing distinct operational and strategic value. Type-based segmentation reflects evolving procedural preferences driven by advancements in sperm-preparation, insemination delivery mechanisms, and cryogenic storage solutions. Application segments demonstrate strong traction across clinical fertility treatments and livestock breeding, each influenced by demographic, genetic, and productivity-driven imperatives. End-user segmentation highlights differentiated adoption patterns between fertility clinics, home users, livestock producers, and research institutions, each showing unique growth trajectories based on technology access, procedural expertise, and sustainability priorities. Collectively, the segmentation framework illustrates shifting technological uptake, rising digital integration, and more precise reproductive interventions, enabling stakeholders to align investments with measurable demand patterns across global markets.

Type segmentation in the Artificial Insemination market is defined by key categories including Intrauterine Insemination (IUI), Intracervical Insemination (ICI), Intratubal Insemination (ITI), and Home-Based Insemination Kits. Among these, IUI leads the segment with approximately 46% share, driven by higher success rates, standardized clinical protocols, and widespread availability across fertility centers. In comparison, ICI holds around 28%, while ITI techniques account for nearly 12% due to their more specialized procedural requirements. Home-based insemination solutions contribute a combined 14%, reflecting rising consumer-driven adoption. The fastest-growing segment is home-based insemination kits, expanding at an estimated 11% CAGR, supported by privacy preferences, digital monitoring tools, and rising demand from single-parent and LGBTQ+ consumers.

The application landscape of the Artificial Insemination market spans human fertility treatment, animal breeding, research laboratories, and genetic improvement programs. Human fertility treatment remains the leading application with an estimated 52% share, supported by rising infertility prevalence and rapid adoption of AI-led sperm analysis. In comparison, animal breeding holds 39% of application adoption, while research and genetic programs collectively represent 9%. The fastest-growing application is advanced livestock breeding, expanding at 9% CAGR, driven by genomic selection, productivity optimization, and estrus-detection technologies achieving more than 90% accuracy.

Other applications—such as reproductive research and cryobiology development—carry a combined share of 9%, offering niche but strategically relevant contributions to innovation pipelines.

End-user segmentation in the Artificial Insemination market includes fertility clinics, hospitals, home users, livestock producers, and research institutions. Fertility clinics remain the dominant end-user group with 48% share, supported by specialized infrastructure, skilled reproductive specialists, and adoption of automated lab systems enhancing procedure efficiency by over 20%. Hospitals hold around 18%, while home users represent approximately 15%, driven by rising comfort with guided insemination kits and digital cycle-tracking tools. Livestock producers form the fastest-growing end-user segment, expanding at 10% CAGR, as precision-breeding technologies and estrus-detection sensors improve reproductive outcomes by more than 12%. Research institutions and universities account for the remaining 19%, contributing significantly to product validation and innovation-driven experimentation.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2025 and 2032.

Europe followed with 27% share, supported by strong regulatory frameworks, while Asia-Pacific held 24%, driven by rapidly expanding fertility infrastructure. South America represented 7%, and the Middle East & Africa accounted for 4%, reflecting rising adoption but lower procedural capacity. Regional variations in clinical maturity, donor-bank availability, digital fertility tools, and livestock AI programs continue shaping operational priorities across global markets. Increasing investments in cryogenic storage, automated sperm-prep systems, and precision breeding technologies further widen regional performance gaps, with advanced economies demonstrating higher technology penetration rates exceeding 60% of fertility centers.

North America maintains a strong foothold in the Artificial Insemination market, capturing approximately 38% share in 2024, driven by highly advanced fertility networks and strong adoption of automated laboratory systems. Key industries strengthening demand include human fertility services, livestock genetics, and biomedical research. Regulatory support, such as improved donor-screening standards and state-level subsidy programs, continues to streamline clinical operations. Digital transformation remains central, with over 50% of fertility clinics adopting AI-enabled sperm-analysis tools and microfluidic sorting platforms. Leading regional providers are enhancing capabilities—one major U.S. fertility chain integrated robotics-assisted sperm preparation in 2024, improving cycle efficiency by 16%. Consumer behavior trends show higher adoption among LGBTQ+ users and single parents, along with strong enterprise-level investment in healthcare digitalization, aligning with regional expectations for accuracy, transparency, and procedural reliability.

Europe accounted for nearly 27% of the global Artificial Insemination market in 2024, supported by leading countries such as Germany, the UK, France, and Italy. The region’s advancement is influenced by strong medical governance frameworks, including bioethics committees and strict donor-regulation protocols. Sustainability initiatives encouraging reduced single-use plastics in fertility labs are further reshaping operational standards. Europe exhibits high adoption of emerging technologies, with more than 45% of clinics using automated cryogenic monitoring systems and digital consent workflows. A regional fertility technology provider in Germany launched a precision sperm-analysis platform in 2024, enhancing diagnostic accuracy by 14%. Consumer behavior highlights growing interest in transparent, explainable reproductive technologies, aligning with Europe’s emphasis on regulatory-compliant and ethically governed ART procedures.

Asia-Pacific represents one of the fastest-expanding regions, holding approximately 24% of market volume in 2024, driven by high consumption in China, India, Japan, and South Korea. China alone accounts for more than 11% of global usage due to extensive fertility-center networks and state-backed reproductive research. The region is witnessing major investments in laboratory automation, AI-linked fertility planning apps, and cost-efficient donor programs. Innovation hubs in Singapore, Shenzhen, and Bangalore are driving advancements in portable insemination kits and AI-led sperm viability software. A biotechnology firm in India introduced an enhanced cryopreservation medium in 2024, improving motility recovery by 13%. Regional consumer behavior reflects strong engagement with mobile fertility platforms and digital consultation services, aligning with rising tech adoption trends.

South America captured around 7% of the global Artificial Insemination market in 2024, with Brazil and Argentina as the primary contributors. Expanding reproductive-health infrastructure, combined with targeted government programs supporting fertility treatment accessibility, is strengthening demand across urban centers. Trends in livestock genetics are also notable, especially in Brazil, where large-scale cattle AI programs utilize advanced semen-dosing technologies, improving efficiency by 10–12%. One regional fertility group in Brazil launched a specialized donor-matching platform in 2024 to support rising patient volumes. Consumer behavior trends show increasing adoption of insemination services tied to personalized family planning, media-driven awareness, and language-specific fertility platforms.

The Middle East & Africa accounted for approximately 4% of the global Artificial Insemination market in 2024, with the UAE, Saudi Arabia, and South Africa emerging as key growth countries. Demand is influenced by national healthcare modernization programs and expanding reproductive-health initiatives. Technological integration is accelerating, with several fertility centers adopting digital sperm-tracking software and precision cryogenic storage solutions. Regulatory partnerships focused on donor safety and cross-border fertility services are improving procedural accessibility. A notable development in 2024 included a UAE-based clinic deploying AI-enabled sperm-morphology analysis, improving diagnostic consistency by 11%. Regional consumer behavior shows growing acceptance of ART services, especially among young urban populations seeking medically supervised reproductive options.

United States – 28% market share

Strong dominance due to advanced fertility infrastructure, high adoption of automated lab technologies, and significant consumer demand for medically assisted reproduction.

China – 11% market share

Leadership supported by large-scale fertility center networks, increasing ART utilization rates, and strong government backing for reproductive research and technological advancement.

The Artificial Insemination market is characterized by a moderately consolidated competitive structure, with more than 40 active manufacturers, service providers, and fertility technology companies operating globally. The top five players collectively account for approximately 38% of the overall market share, reflecting a competitive yet increasingly innovation-driven ecosystem. Market leaders maintain their positioning through strategic product enhancements, expanded fertility service networks, and continuous investment in reproductive biotechnology. Over the past three years, more than 25 notable strategic initiatives—including mergers among fertility clinics, cross-border service expansions, and the launch of streamlined insemination consumables—have reshaped competitive boundaries. Vendor differentiation is increasingly driven by procedural accuracy, automated insemination systems, and the integration of digital fertility tracking solutions adopted by over 60% of modern clinics. Partnerships between fertility centers and genetic testing companies have risen by nearly 30%, creating more comprehensive reproductive solutions. As demand for assisted reproductive technologies increases across both developed and emerging economies, competition intensifies around quality assurance, clinical success rates, and scalable service offerings, strengthening the market’s forward outlook.

Genea Biomedx

FUJIFILM Irvine Scientific

Rocket Medical

Rinovum Women’s Health

Coopersurgical, Inc.

MedGyn Products Inc.

Thermo Fisher Scientific

Technological evolution in the Artificial Insemination market is accelerating as fertility providers increasingly adopt automated, data-driven, and precision-focused solutions. Modern insemination procedures are now supported by advanced sperm preparation systems that enhance motility and viability, with over 55% of clinics globally using gradient-based purification technologies. Computer-Assisted Sperm Analysis (CASA) systems have become one of the most influential technologies, enabling objective assessment of sperm morphology and movement with accuracy rates exceeding 90%, significantly improving selection for intrauterine insemination (IUI) and intracervical insemination (ICI).

Digital fertility monitoring platforms are also transforming patient engagement, with more than 40% of fertility centers integrating ovulation tracking algorithms and AI-based prediction tools that optimize insemination timing. Automated insemination devices have gained strong commercial traction, reducing procedural inconsistencies and improving workflow efficiencies by up to 25%. Cryopreservation advancements—particularly vitrification-based freezing—have improved post-thaw sperm survival rates to nearly 80%, supporting long-term storage programs and cross-border donor distribution.

Emerging technologies are increasingly shaping next-generation capabilities. Microfluidic sperm sorting, which mimics physiological selection processes, is being adopted by an estimated 18% of advanced clinics due to its ability to isolate high-motility sperm while minimizing DNA fragmentation. Robotic-assisted reproductive systems are also gaining attention, offering precision-controlled insemination delivery in research and specialized clinical environments. Additionally, integration of genetic compatibility screening and digital lab management systems is expanding rapidly, enabling labs to streamline quality control and reduce operational errors by nearly 30%. Overall, the market is shifting toward automation, accuracy, and personalized treatment pathways, driven by sustained adoption of high-performance lab equipment, data-enhanced fertility planning tools, and next-generation sperm selection technologies.

In June 2024, CooperSurgical completed its acquisition of ZyMōt Fertility, integrating the ZyMōt sperm-separation device—known for isolating high-motility, low–DNA-fragmentation sperm—into its ART portfolio. (coopersurgical.com)

In October 2024, Hamilton Thorne announced a partnership with Alife Health, making Alife’s AI-driven Embryo Assist software available on Hamilton Thorne laser systems, enabling digital embryo imaging and data-driven ranking. (alifehealth.com)

Also in November 2024, Hamilton Thorne formed a collaboration with MIM Fertility to integrate MIM’s AI-powered embryo-assessment tool EMBRYOAID® into its LYKOS® laser systems, enhancing embryo selection accuracy. (Hamilton Thorne)

In February 2024, Alife Health partnered with Ovation Fertility, launching the world’s first embryo image-cataloguing system via Alife’s Embryo Assist platform to pilot AI-enabled embryo selection in a national lab network. (PR Newswire)

This Artificial Insemination Market Report provides a comprehensive analysis spanning multiple dimensions: type, application, technology, and geography. On the type axis, it covers IUI (intrauterine insemination), ICI (intracervical), ITI (intratubal), and intravaginal / home-insemination kits. In the applications segment, the report examines clinical fertility treatments, animal breeding programs, genetic-improvement research, and cryopreservation operations. On the technology front, it dives into microfluidic sperm selection, AI-enabled embryo scoring, digital ovulation and cycle-tracking platforms, and advanced cryogenic media.

Geographically, the report spans North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, dissecting regional adoption, infrastructure trends, and key country-level drivers. It also highlights end-user groups including fertility clinics, hospitals, home-users, livestock producers, and research institutions. For industry focus, the report addresses how established fertility centers, emerging femtech providers, and large-scale genetic / livestock breeding firms are shaping demand.

Emerging or niche segments are also covered: for instance, at-home insemination kits with integrated mobile-app tracking, AI-driven embryo decision-support systems in IVF labs, and cross-border donor-sperm logistics powered by improved cryo storage. The report evaluates market maturity, innovation pipelines, and investment flows, with detailed company profiles, competitive benchmarking, and strategic growth levers for decision-makers in reproductive health and animal genetics.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 24700 Million |

|

Market Revenue in 2032 |

USD 51471 Million |

|

CAGR (2025 - 2032) |

8.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Genea Biomedx, FUJIFILM Irvine Scientific, Rocket Medical, Rinovum Women’s Health, Coopersurgical, Inc., MedGyn Products Inc., Thermo Fisher Scientific, Hamilton Thorne Ltd., Vitrolife AB, INVO Bioscience |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |