Reports

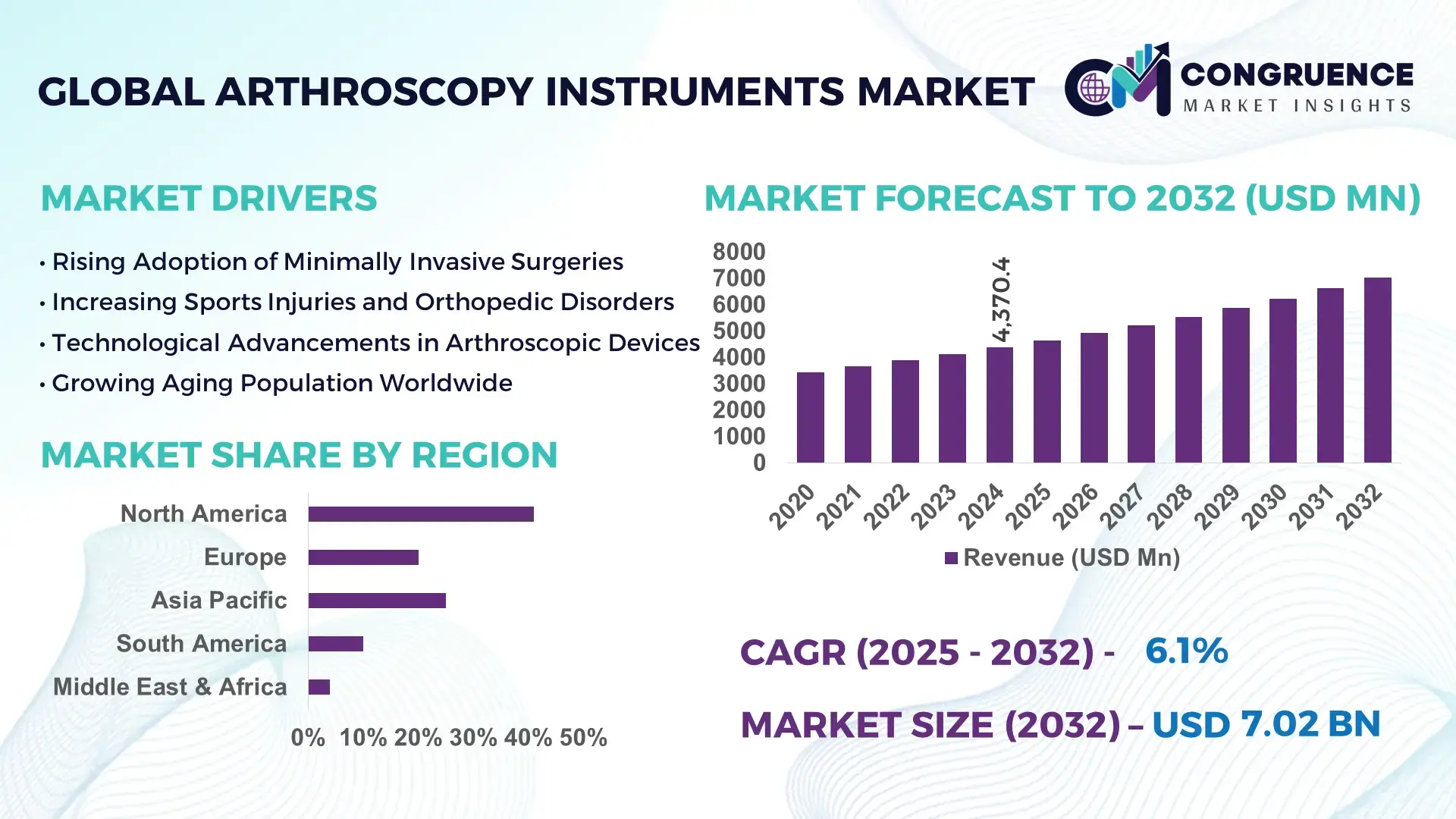

The Global Arthroscopy Instruments Market was valued at USD 4370.38 Million in 2024 and is anticipated to reach a value of USD 7018.47 Million by 2032 expanding at a CAGR of 6.1% between 2025 and 2032. Growth is supported by rising procedure volumes for minimally invasive orthopedic surgeries across hospitals and specialty clinics.

The United States represents the most prominent national ecosystem within the arthroscopy instruments market, supported by large-scale manufacturing facilities, advanced R&D infrastructure, and high procedural throughput. The country performs over 1.2 million arthroscopic knee and shoulder procedures annually, supported by more than 6,000 ambulatory surgical centers. Investment in orthopedic medical devices exceeded USD 8.5 billion in 2023, with arthroscopy platforms accounting for a significant share of endoscopic equipment upgrades. Technological integration of 4K visualization systems, AI-assisted surgical navigation, and disposable instrumentation is increasingly standardized across orthopedic and sports medicine applications.

Market Size & Growth: Valued at USD 4,370.38 Million in 2024, projected to reach USD 7,018.47 Million by 2032 at a CAGR of 6.1%, driven by higher minimally invasive surgery adoption.

Top Growth Drivers: Outpatient arthroscopy adoption at 62%, surgical efficiency improvement at 28%, and postoperative recovery time reduction at 35%.

Short-Term Forecast: By 2028, average procedure cost is expected to decline by approximately 18% through reusable instrumentation and bundled purchasing models.

Emerging Technologies: High-definition 4K arthroscopes, AI-assisted joint visualization, and bio-integrated disposable shavers.

Regional Leaders: North America projected at USD 2.65 Billion by 2032 with ASC-led adoption, Europe at USD 1.92 Billion driven by sports medicine demand, Asia-Pacific at USD 1.58 Billion supported by hospital infrastructure expansion.

Consumer/End-User Trends: Orthopedic surgeons increasingly favor outpatient settings, with over 55% of procedures shifting to ambulatory centers.

Pilot or Case Example: A 2024 U.S. hospital network pilot reported a 22% reduction in operating room turnaround time using integrated arthroscopy towers.

Competitive Landscape: Stryker leads with approximately 24% share, followed by Arthrex, Smith+Nephew, Johnson & Johnson, and Zimmer Biomet.

Regulatory & ESG Impact: Stricter sterilization standards and single-use device regulations are influencing procurement and product design strategies.

Investment & Funding Patterns: Over USD 3.1 Billion invested globally between 2022–2024, with growing focus on device-platform integration.

Innovation & Future Outlook: Continued convergence of digital imaging, robotics compatibility, and data-enabled surgical workflows.

The arthroscopy instruments market serves orthopedic surgery, sports medicine, trauma care, and rehabilitation-focused clinical segments, with knee and shoulder applications collectively contributing over 60% of procedural demand. Recent innovations include lightweight battery-powered shavers, disposable cannula systems, and AI-enabled imaging software enhancing intraoperative precision. Regulatory emphasis on infection control, coupled with healthcare cost containment policies, is accelerating adoption of efficient instrument systems. Regionally, North America leads consumption due to procedural density, while Asia-Pacific shows the fastest growth driven by expanding surgical access. Future outlook centers on smart instrumentation, outpatient optimization, and digital surgical ecosystems.

The Arthroscopy Instruments Market holds strong strategic relevance within the global medical devices ecosystem due to its direct linkage with minimally invasive orthopedic care, outpatient surgery expansion, and hospital efficiency optimization. Healthcare systems are increasingly prioritizing arthroscopy to reduce inpatient burden, with minimally invasive joint procedures demonstrating up to 38% lower post-operative hospitalization rates compared to open surgery methods. From a strategic perspective, technology-led differentiation is becoming central, where next-generation digital arthroscopy systems deliver 42% improvement in visualization accuracy compared to conventional fiber-optic systems.

North America dominates in volume due to high procedural density and surgical infrastructure, while Europe leads in adoption with nearly 64% of orthopedic centers integrating advanced arthroscopy visualization platforms. In Asia-Pacific, hospital modernization programs and sports injury incidence are accelerating device penetration, particularly in urban tertiary-care facilities.

By 2028, AI-enabled image recognition in arthroscopy is expected to improve intraoperative decision accuracy by approximately 30%, while reducing average procedure time by 18%. ESG considerations are also shaping procurement strategies, with firms committing to medical waste reduction targets such as 25% recyclable or reusable instrument components by 2030. In 2024, a leading U.S.-based orthopedic device manufacturer achieved a 21% reduction in sterilization-related downtime through smart tray optimization and RFID-enabled instrument tracking.

Looking ahead, the Arthroscopy Instruments Market is positioned as a pillar of clinical resilience, regulatory compliance, and sustainable growth, driven by digital integration, outpatient care expansion, and environmentally responsible device innovation.

The growing preference for minimally invasive orthopedic procedures is a primary driver for the Arthroscopy Instruments Market, as arthroscopy offers reduced tissue trauma, faster recovery, and lower complication rates. Studies indicate that arthroscopic interventions reduce post-surgical rehabilitation time by nearly 35% compared to open procedures. More than 60% of knee and shoulder surgeries in developed healthcare systems are now performed arthroscopically. The shift toward outpatient surgery models further amplifies demand, with ambulatory surgical centers reporting procedure throughput improvements of over 25% when using modern arthroscopy platforms. This procedural efficiency aligns with payer and provider objectives to lower hospital stays and improve patient satisfaction, reinforcing sustained market momentum.

Despite clinical advantages, the Arthroscopy Instruments Market faces restraint from high upfront capital costs and complex reprocessing requirements. Advanced arthroscopy towers, visualization systems, and powered instruments can require initial investments exceeding USD 150,000 per operating room. Additionally, reusable instruments necessitate stringent sterilization protocols, increasing labor, water, and energy usage. Hospitals report that reprocessing-related expenses can account for up to 18% of total arthroscopy procedure costs. Smaller facilities and budget-constrained healthcare systems may delay upgrades or rely on refurbished equipment, slowing adoption of next-generation technologies and limiting uniform market penetration.

The rapid expansion of ambulatory surgical centers presents a significant opportunity for the Arthroscopy Instruments Market. ASCs now handle more than 55% of elective orthopedic procedures in several developed markets due to lower operational costs and shorter patient stays. This shift drives demand for compact, mobile, and integrated arthroscopy systems optimized for high procedure turnover. Manufacturers offering modular platforms, disposable instruments, and simplified setup solutions are well-positioned to capture ASC-driven demand. Additionally, emerging markets investing in day-surgery infrastructure provide opportunities for first-time installations, accelerating instrument sales and long-term service partnerships.

Regulatory compliance and workforce readiness pose ongoing challenges to the Arthroscopy Instruments Market. Devices must meet strict safety, sterilization, and documentation standards, which vary across regions and add complexity to product approval and deployment. Compliance-related modifications can extend product development timelines by 12–18 months. Furthermore, advanced arthroscopy systems require specialized surgeon and staff training, with learning curves impacting early-stage utilization. Hospitals report that insufficient training can reduce equipment usage efficiency by up to 20% during initial adoption phases. These challenges necessitate continuous investment in education, regulatory alignment, and post-installation support to ensure sustained market growth.

• Rapid Adoption of Modular Arthroscopy Systems Enhancing Surgical Efficiency: The Arthroscopy Instruments Market is witnessing strong momentum toward modular and prefabricated instrument systems designed to improve operating room efficiency. Nearly 55% of newly installed arthroscopy platforms in 2024 incorporated modular components, enabling faster setup and reduced intraoperative delays. Pre-assembled camera heads, light sources, and shaver modules manufactured using automated processes have lowered on-site configuration time by approximately 30%. Demand for high-precision, factory-calibrated modules is particularly strong in Europe and North America, where hospitals report up to 22% improvement in procedure throughput and measurable reductions in labor dependency during system changeovers.

• Growing Shift Toward Single-Use and Hybrid Disposable Instruments: Single-use and hybrid disposable arthroscopy instruments are increasingly adopted to address infection control and reprocessing constraints. Approximately 48% of orthopedic departments have integrated at least one disposable arthroscopy component into routine procedures. Hospitals using disposable shaver blades and cannulas report sterilization cycle reductions of nearly 40% and water usage cuts of 25% per procedure. This trend is also influencing procurement strategies, with bundled disposable kits improving inventory turnover by 18% and reducing cross-contamination risk metrics by over 20% in high-volume surgical centers.

• Integration of Digital Visualization and Smart Imaging Technologies: Advanced visualization technologies are redefining clinical performance benchmarks in the Arthroscopy Instruments Market. Adoption of 4K and 3D arthroscopic imaging systems increased by over 36% between 2022 and 2024, significantly enhancing anatomical clarity. Surgeons using digital visualization platforms report up to 45% improvement in depth perception accuracy and a 28% reduction in revision-related complications. Smart imaging integration with data capture tools is also improving procedural documentation efficiency by nearly 33%, supporting compliance and post-operative analytics.

• Expansion of Ambulatory Surgical Center–Focused Instrument Design: Instrument design is increasingly optimized for ambulatory surgical center environments, where procedure volume growth exceeds 20% annually in several developed regions. Compact arthroscopy towers and mobile fluid management units now account for approximately 42% of new installations. These systems reduce floor space requirements by nearly 35% and enable same-day multi-procedure scheduling efficiency gains of around 26%. The trend reflects a broader shift toward outpatient orthopedic care models prioritizing speed, flexibility, and cost discipline without compromising surgical precision.

The Arthroscopy Instruments Market segmentation reflects diversified demand across product types, clinical applications, and end-user settings, shaped by procedure complexity, care delivery models, and technology intensity. Type-based segmentation highlights strong demand for visualization and powered systems, driven by the need for procedural precision and workflow efficiency. Application segmentation is largely aligned with orthopedic burden patterns, where knee and shoulder procedures dominate due to high incidence of sports injuries and degenerative joint conditions. End-user segmentation shows a structural shift from traditional hospital dominance toward ambulatory and specialty care settings, supported by outpatient surgery growth and reimbursement optimization. Together, these segmentation layers provide critical insight into purchasing priorities, innovation focus, and adoption behavior across mature and emerging healthcare systems.

Visualization systems represent the leading product type in the Arthroscopy Instruments Market, accounting for approximately 38% of total adoption, supported by widespread use of high-definition cameras, monitors, and light sources across orthopedic procedures. Their leadership is driven by clinical reliance on enhanced image clarity, with 4K visualization improving anatomical accuracy by over 40% compared to standard HD systems. Powered instruments, including shavers and ablation devices, currently hold around 27% of adoption, while fluid management systems account for close to 15%. However, powered instruments are the fastest-growing type, expanding at an estimated CAGR of 7.4%, driven by rising procedure volumes and preference for battery-powered, ergonomically optimized devices that reduce surgeon fatigue. Hand instruments and accessories collectively contribute nearly 20% of the market, maintaining relevance in cost-sensitive settings and high-frequency procedures.

Knee arthroscopy remains the leading application segment, representing approximately 46% of total procedures, supported by high prevalence of ligament injuries, meniscal tears, and osteoarthritis-related interventions. Shoulder arthroscopy follows with about 29% adoption, driven by rotator cuff repairs and instability treatments. Hip, wrist, ankle, and elbow applications together account for a combined share of roughly 25%, serving niche but growing procedural needs. While knee procedures dominate in volume, shoulder arthroscopy is the fastest-growing application, registering an estimated CAGR of 6.8%, supported by rising sports participation and improved diagnostic imaging accuracy. Advances in minimally invasive repair techniques are also expanding hip arthroscopy adoption in specialized centers.

Hospitals remain the leading end-user segment in the Arthroscopy Instruments Market, accounting for approximately 52% of total usage, due to their capacity to manage complex cases and high patient volumes. Ambulatory surgical centers represent around 34% of adoption, while specialty orthopedic clinics contribute a combined share of nearly 14%. Although hospitals lead in overall volume, ambulatory surgical centers are the fastest-growing end-user segment, expanding at an estimated CAGR of 8.1%, fueled by lower procedure costs, shorter patient stays, and operational efficiency gains of over 25% per operating room. Specialty clinics are increasingly adopting compact arthroscopy systems, with adoption rates exceeding 40% in urban orthopedic practices.

North America accounted for the largest market share at 41.6% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2025 and 2032.

North America benefits from high procedural volumes, with over 1.2 million arthroscopic surgeries performed annually, while Europe follows with approximately 28.3% share supported by strong sports medicine demand. Asia-Pacific currently represents nearly 22.5% of global volume, driven by rapid hospital infrastructure expansion and rising orthopedic case loads, particularly in China and India. South America and Middle East & Africa together account for around 7.6%, reflecting gradual penetration supported by healthcare modernization programs. Regional variations are strongly influenced by surgical capacity per capita, outpatient adoption rates exceeding 55% in developed regions, and increasing investment in minimally invasive orthopedic care globally.

How is advanced outpatient care reshaping high-volume surgical adoption?

North America holds approximately 41.6% share of the Arthroscopy Instruments Market, supported by high surgical density and advanced healthcare infrastructure. Orthopedic surgery, sports medicine, and trauma care are the primary demand drivers, with ambulatory surgical centers performing nearly 58% of elective arthroscopy procedures. Regulatory emphasis on infection control and value-based care has accelerated adoption of disposable and hybrid instruments. Digital transformation is evident through widespread use of 4K visualization and smart fluid management systems, improving operating room efficiency by over 25%. A major regional manufacturer expanded production of battery-powered shavers in 2024 to support outpatient facilities. Consumer behavior reflects preference for minimally invasive procedures offering faster recovery and same-day discharge.

Why is regulatory alignment accelerating precision-focused adoption?

Europe accounts for roughly 28.3% of the Arthroscopy Instruments Market, with Germany, the UK, and France collectively contributing over 60% of regional demand. Strict medical device regulations and sustainability initiatives are influencing procurement toward reusable systems with lower lifecycle impact. Adoption of high-definition visualization platforms exceeds 65% across tertiary hospitals. Regional players are investing in eco-designed instrument trays to reduce sterilization resource usage by nearly 20%. Sports-related injuries and aging populations continue to drive procedure volumes. Consumer behavior shows strong preference for clinically validated, regulation-compliant systems, with hospitals prioritizing transparency and traceability in device performance.

What is driving rapid procedural expansion across emerging surgical hubs?

Asia-Pacific represents about 22.5% of global market volume and ranks as the fastest-growing regional market. China, Japan, and India are the top consuming countries, together accounting for over 70% of regional procedures. Hospital infrastructure expansion and rising orthopedic case incidence are key growth factors. Local manufacturing of arthroscopy instruments has increased by nearly 30% over the past three years, improving affordability. Innovation hubs in Japan and South Korea are advancing compact visualization systems. Regional consumer behavior reflects growing acceptance of minimally invasive surgery, supported by increasing private healthcare access and digital hospital platforms.

How are healthcare investments improving procedural access?

South America holds approximately 4.3% of the Arthroscopy Instruments Market, with Brazil and Argentina leading regional demand. Public and private healthcare investments are expanding orthopedic surgical capacity, particularly in urban centers. Government initiatives to modernize hospital equipment have supported increased adoption of basic arthroscopy systems. Import-friendly trade policies have improved access to advanced devices. Regional players are focusing on distributor-led expansion to reach secondary hospitals. Consumer behavior is influenced by growing awareness of minimally invasive procedures, with demand concentrated in private healthcare networks.

Why is medical tourism shaping surgical technology demand?

Middle East & Africa accounts for nearly 3.3% of the Arthroscopy Instruments Market, led by the UAE and South Africa. Demand is supported by medical tourism, private hospital investments, and orthopedic specialization centers. Technological modernization includes adoption of digital visualization systems in over 45% of newly built surgical suites. Regional trade partnerships have eased import barriers for advanced instruments. A Gulf-based healthcare group expanded its orthopedic centers in 2024, increasing arthroscopy capacity by over 20%. Consumer behavior shows preference for premium care settings and internationally standardized surgical procedures.

United States: 36.2% share of the Arthroscopy Instruments Market due to high procedure volumes, advanced manufacturing capacity, and widespread outpatient adoption.

Germany: 9.4% share of the Arthroscopy Instruments Market supported by strong orthopedic infrastructure, regulatory-driven quality standards, and high sports medicine demand.

The Arthroscopy Instruments market is moderately consolidated, characterized by the presence of approximately 20–25 active global and regional competitors operating across visualization systems, powered instruments, implants, and accessories. The top five companies collectively account for nearly 62% of total market adoption, indicating strong brand concentration alongside competitive innovation pressure from mid-sized specialized manufacturers. Market leaders maintain positioning through broad product portfolios, long-term hospital contracts, and continuous upgrades in imaging resolution, ergonomics, and system integration.

Strategic initiatives remain central to competitive differentiation. Over 45% of leading players launched upgraded arthroscopy platforms between 2023 and 2024, with a strong focus on 4K imaging, battery-powered instruments, and modular system architecture. Partnerships with ambulatory surgical centers have increased by nearly 30%, reflecting shifting end-user demand. Mergers and targeted acquisitions are selectively pursued to expand geographic presence and strengthen disposable instrument offerings. Innovation intensity remains high, with more than 35% of competitors allocating increased R&D focus toward digital workflow integration, smart instrument tracking, and sustainability-driven product redesign. Competitive dynamics are further shaped by regulatory compliance capabilities and after-sales service performance, both critical in long-term procurement decisions.

Arthrex, Inc.

Stryker Corporation

Smith & Nephew plc

Johnson & Johnson (DePuy Synthes)

Zimmer Biomet Holdings, Inc.

Olympus Corporation

CONMED Corporation

Karl Storz SE & Co. KG

Medtronic plc

The Arthroscopy Instruments Market is undergoing rapid technological transformation across imaging, instrumentation, digital integration, and consumables, with measurable impacts on procedural efficiency, sterilization burden, and clinical outcomes. High-definition visualization has transitioned from HD to 4K and 3D platforms in many tertiary centers; adoption of 4K/3D imaging rose by an estimated 36% between 2022 and 2024, improving intraoperative visual clarity and reducing revision rates by up to 24% in complex joint repairs. Battery-powered and cordless powered instruments now constitute roughly 28% of new instrument purchases, delivering ergonomic gains and a 15–20% reduction in surgeon fatigue metrics during long procedures.

AI-enabled image recognition and real-time annotation are increasingly embedded into arthroscopy towers and software suites, enabling automated landmark detection with reported accuracy improvements of around 30% over manual visual assessment in pilot deployments. Integration with robotics and navigation systems is accelerating: interoperable interfaces allow instrument tracking accuracy within 1–2 mm, supporting combined arthroscopic–robotic workflows in advanced centers. Smart instrument tracking (RFID and digital tray systems) has reduced instrument search and reprocessing time by approximately 21% and lowered sterilization cycle counts by nearly 18% where implemented.

Single-use and hybrid disposable components are driving infection-control economics, cutting reprocessing water usage by ~25% per procedure and shortening turnover time by up to 40% in high-volume suites. Additive manufacturing is used for bespoke guides and specialty accessories, cutting lead time from weeks to days for select components. Data capture and analytics platforms are standardizing procedural KPIs—operating-room turnaround, fluid usage per case, and instrument utilization—enabling performance benchmarks and value-based procurement. Concurrently, software-as-medical-device considerations, device cybersecurity, and modular interoperability standards are critical procurement criteria, with hospitals increasingly requiring end-to-end validation, traceability, and lifecycle environmental metrics (e.g., recyclable content targets of 20–30%) in vendor evaluations. These technology vectors collectively reshape product roadmaps, procurement strategies, and clinical adoption timelines across the Arthroscopy Instruments Market.

• In January 2024, Arthrex introduced single-use, sterile-packed Nano arthroscopy instrumentation featuring 2 mm diameter tools designed for atraumatic insertion through tight joint spaces, enhancing precision for diagnostic, resection, and extraction procedures.

• In June 2024, ConMed Corporation launched the Hall Linvatec PowerPro Max Arthroscopic Shaver System, offering improved torque control and advanced debris management to streamline tissue resection during arthroscopic procedures.

• In November 2024, Stryker Corporation showcased its advanced 1688 AIM 4K Platform with SPY fluorescence imaging, enhancing intraoperative visualization and real-time tissue perfusion assessment in joint surgeries.

• In September 2024, CONMED Corporation released the Argo Knotless Suture Anchor System, improving soft tissue fixation and workflow efficiency in shoulder and knee arthroscopic repairs, gaining positive reception at the 2024 Orthopaedic Summit.

The Arthroscopy Instruments Market Report encompasses comprehensive segmentation across product types, clinical applications, end-user categories, and geographic regions, providing actionable insights for strategic planning, procurement, and competitive benchmarking. Product type analysis includes detailed profiling of arthroscopes, visualization systems, fluid management platforms, powered shavers, radiofrequency systems, implants, and accessory tools. Application segmentation examines procedural utilization in knee, shoulder, hip, wrist, ankle, and other joint arthroscopies, capturing procedure volumes, clinical demand patterns, and technology intensity across care settings. End-user focus highlights hospitals, ambulatory surgical centers, specialty orthopedic clinics, and diagnostic facilities, detailing adoption behavior, procedural throughput, and decision criteria influencing instrument procurement. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with specific attention to regional healthcare infrastructure expansion, technology uptake, regulatory environments, and consumer preferences.

The report also evaluates emerging and niche segments such as single-use arthroscopy systems, hybrid instrument kits, AI-enhanced visualization, and digital procedure analytics platforms, framing their role in operational performance improvements. Technology insights offer assessments of high-definition imaging, smart instrument tracking, robotic integration, and miniaturized systems that support outpatient and in-office arthroscopy use cases. Competitive analysis details market positioning, product portfolios, strategic initiatives, and innovation trends among leading global and regional players. Decision-maker guidance includes procurement considerations, regulatory compliance impact, sustainability metrics, and future avenues for research, investment, and operational optimization within the Arthroscopy Instruments Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4370.38 Million |

|

Market Revenue in 2032 |

USD 7018.47 Million |

|

CAGR (2025 - 2032) |

6.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Arthrex, Inc., Stryker Corporation, Smith & Nephew plc, Johnson & Johnson (DePuy Synthes), Zimmer Biomet Holdings, Inc., Olympus Corporation, CONMED Corporation, Karl Storz SE & Co. KG, Medtronic plc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |