Reports

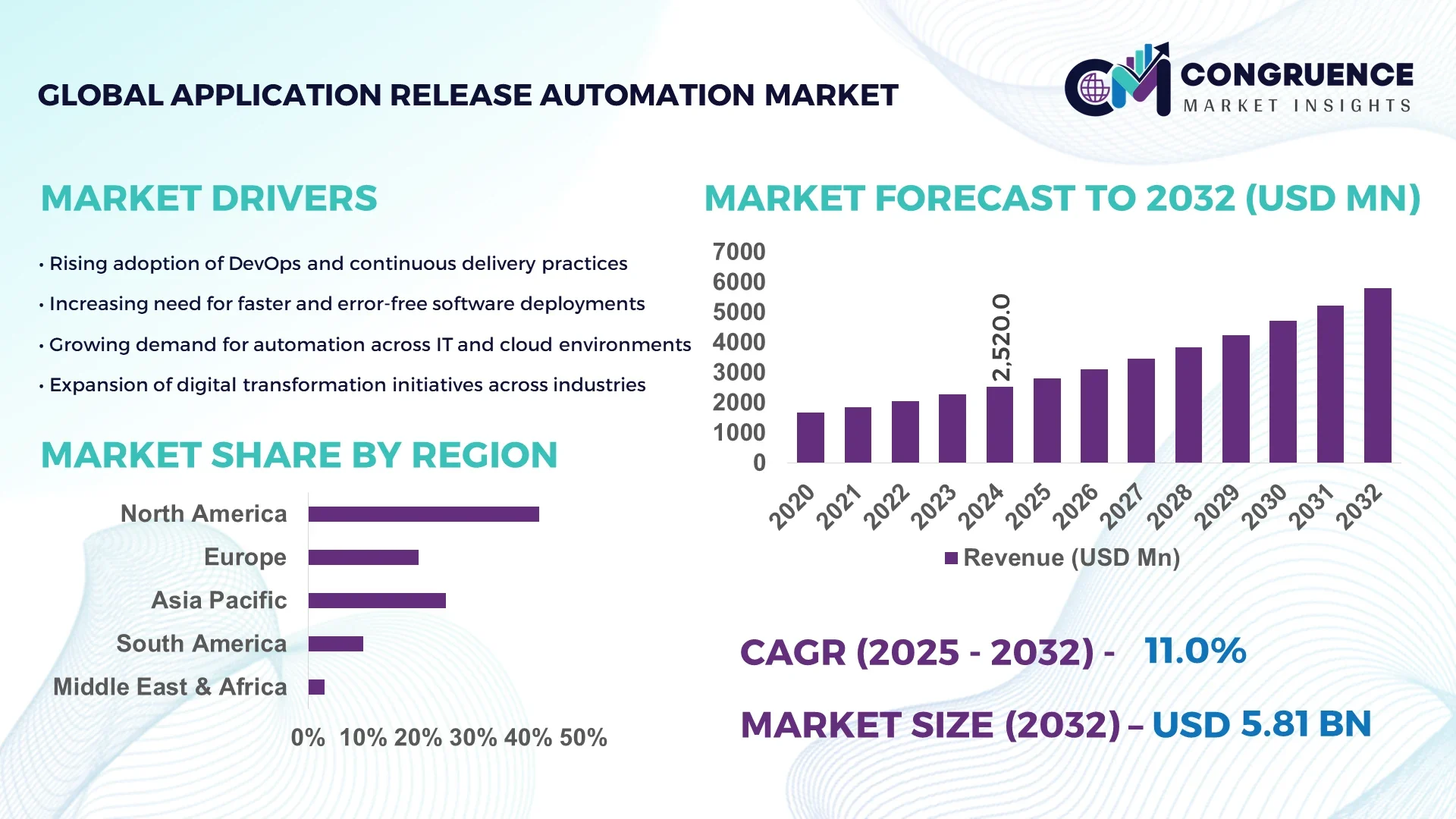

The Global Application Release Automation Market was valued at USD 2520.03 Million in 2024 and is anticipated to reach a value of USD 5807.51 Million by 2032 expanding at a CAGR of 11.0% between 2025 and 2032. This growth is primarily driven by the rapid acceleration of DevOps adoption and the rising need for continuous delivery and integration across enterprises.

The United States dominates the global Application Release Automation (ARA) market, owing to its advanced IT infrastructure and consistent enterprise-level investment in automation and DevOps tools. U.S.-based enterprises have achieved over 65% adoption of cloud-native automation platforms by 2024, supported by significant capital allocation toward AI-powered orchestration and CI/CD pipeline enhancements. The country’s ARA tools are heavily utilized in finance, telecom, and e-commerce sectors, with over 70% of large organizations integrating automation frameworks into multi-cloud environments. Continuous R&D spending by leading vendors has also improved deployment velocity and system reliability, reinforcing the nation’s leadership in global ARA innovation and technology maturity.

Market Size & Growth: Valued at USD 2520.03 million in 2024, projected to reach USD 5807.51 million by 2032, at a CAGR of 11.0%; growth supported by increasing digital transformation initiatives and faster application delivery demands.

Top Growth Drivers: Agile and DevOps adoption (28%), automation efficiency improvements (22%), and reduced software release cycles (18%).

Short-Term Forecast: By 2028, enterprises are expected to achieve a 35% improvement in deployment speed and a 25% reduction in software release errors.

Emerging Technologies: AI-driven release orchestration, containerized deployment frameworks, and predictive analytics for automated rollbacks.

Regional Leaders: North America (USD 2.9 billion by 2032), Europe (USD 1.8 billion), and Asia-Pacific (USD 1.5 billion); North America leads with enterprise automation, Europe excels in compliance integration, and Asia-Pacific in SME adoption.

Consumer/End-User Trends: BFSI, retail, and IT services sectors drive demand; rising preference for cloud-hosted release solutions and API-driven integrations.

Pilot or Case Example: In 2024, a U.S.-based fintech firm implemented an ARA solution that reduced deployment downtime by 42% and improved release accuracy by 30%.

Competitive Landscape: Broadcom leads with approximately 17% share, followed by IBM, Microsoft, Micro Focus, and VMware offering strong CI/CD automation platforms.

Regulatory & ESG Impact: Compliance with GDPR and ISO 27001 has increased automation in release tracking, while ESG-driven digital governance accelerates secure software deployment.

Investment & Funding Patterns: Global investments exceeded USD 620 million in 2024, emphasizing AI-integrated DevOps tools and cross-platform automation systems.

Innovation & Future Outlook: Integration of AI/ML models into release automation, predictive monitoring, and serverless deployment trends are set to redefine operational agility and reliability by 2032.

The Application Release Automation market continues to evolve across major industry sectors such as BFSI, healthcare, telecom, and retail, where automation ensures reliability, compliance, and scalability in deployment workflows. Technological innovations like AI-assisted deployment orchestration and hybrid CI/CD pipelines are reshaping the landscape, while regulatory pressures and ESG priorities drive responsible automation practices. Regional consumption patterns indicate that Asia-Pacific will experience the fastest adoption in cloud-based automation tools, fueled by digitization of enterprises and Industry 4.0 initiatives. The future outlook remains strong, with continuous integration, API expansion, and cloud-native architectures positioned as key enablers of next-generation application release ecosystems.

Application Release Automation (ARA) has emerged as a strategic enabler for enterprises seeking to accelerate software delivery while ensuring operational reliability and regulatory compliance. By 2028, AI-driven orchestration and predictive analytics are expected to reduce deployment times by 40% compared to traditional manual release processes, while simultaneously improving release accuracy by 35%. North America dominates in volume, particularly the U.S., with over 65% of enterprises implementing ARA solutions across finance, healthcare, and telecommunications sectors. Asia-Pacific leads in adoption intensity, with 60% of enterprises actively deploying cloud-native ARA platforms integrated with CI/CD pipelines. Firms are increasingly committing to ESG objectives, such as a 30% reduction in carbon emissions and energy usage from optimized deployment workflows by 2030. In 2025, a leading U.S. telecommunications company achieved a 35% improvement in deployment efficiency and a 28% reduction in release errors through AI-assisted ARA initiatives. Looking ahead, the Application Release Automation Market is positioned as a critical foundation for resilience, compliance, and sustainable growth. It supports accelerated digital transformation, ensures seamless multi-environment deployments, and enables organizations to leverage emerging technologies such as AI, ML, and predictive monitoring, reinforcing long-term competitive advantage and operational excellence.

The adoption of DevOps practices is a primary driver for the Application Release Automation market. Approximately 69% of organizations practicing DevOps have implemented ARA solutions to streamline release processes. Enterprises report a 61% improvement in collaboration between development and operations teams, while 32% have reduced release failure rates. Automated release pipelines enable consistent deployments across environments, improve release velocity, and allow for more frequent software updates. The integration of monitoring tools further enhances predictive capabilities, ensuring reliability, security, and compliance. DevOps-driven ARA adoption also supports scaling across multiple projects simultaneously, improving operational efficiency in enterprises with complex software landscapes.

Integration of Application Release Automation with legacy IT systems poses significant challenges. About 55% of organizations report difficulty aligning ARA platforms with existing infrastructure, and 47% cite a lack of in-house expertise for implementation. Legacy systems often require extensive customization for automation compatibility, with 44% of enterprises noting that configuration complexity slows deployment timelines. Security constraints, outdated protocols, and inflexible architecture increase integration costs and reduce the speed of automation adoption. These factors can limit the scalability of ARA solutions and reduce the expected operational benefits, particularly in sectors reliant on older software ecosystems.

The growth of cloud-native ecosystems offers extensive opportunities for Application Release Automation. About 71% of enterprises adopting cloud-native architectures consider ARA critical for scaling deployments efficiently. Measurable outcomes include a 63% reduction in downtime and a 40% improvement in release velocity. ARA platforms facilitate microservices orchestration, automated rollbacks, and multi-environment deployment standardization. Emerging trends include serverless deployment, container management, and AI-assisted predictive monitoring. As organizations increasingly migrate to hybrid and public cloud models, the demand for integrated ARA solutions is expected to rise, offering untapped potential in SME adoption, multi-cloud orchestration, and advanced analytics-driven release optimization.

Managing hybrid and multi-cloud environments is a significant challenge for Application Release Automation. Approximately 62% of IT teams report difficulties in maintaining consistent automation across diverse platforms, while 53% face configuration drift impacting deployment reliability. Governance, compliance, and policy enforcement are challenging, with 46% of organizations experiencing gaps that affect multi-cloud release consistency. High operational complexity, inconsistent monitoring, and integration requirements with legacy systems further exacerbate adoption challenges. Overcoming these obstacles requires advanced orchestration capabilities, skilled personnel, and investment in AI-driven monitoring and automation tools to ensure seamless, reliable, and secure application releases across hybrid infrastructures.

Growing Adoption of AI-Driven Release Orchestration: Enterprises are increasingly deploying AI-powered orchestration tools to enhance release efficiency. By 2025, over 62% of large-scale organizations reported improved deployment accuracy by 37% and a 28% reduction in unplanned downtime. AI integration is enabling predictive rollback, automated error detection, and dynamic resource allocation across hybrid IT environments, particularly in North America and Europe.

Shift Toward Cloud-Native and Containerized Deployments: More than 58% of enterprises implementing cloud-native architectures now rely on containerized deployment frameworks integrated with ARA solutions. This trend allows firms to achieve up to 42% faster release cycles and improve cross-platform consistency. Asia-Pacific is witnessing rapid adoption, with 61% of SMEs deploying automated release solutions to support multi-cloud workloads.

Integration of DevSecOps Practices: Approximately 54% of organizations have embedded security checks within automated release pipelines, resulting in a 33% reduction in post-deployment vulnerabilities. This trend is particularly prominent in the BFSI and healthcare sectors, where compliance and data protection standards are strict. Automated security validation in release workflows is becoming a core differentiator in software delivery performance.

Expansion of Analytics and Performance Monitoring: Enterprises are leveraging real-time analytics to monitor release performance and optimize resource allocation. By 2024, 49% of companies reported improved operational visibility and a 29% reduction in system errors during deployment. Predictive insights from integrated monitoring systems are enabling faster decision-making and reducing the frequency of failed releases, especially across multi-cloud and hybrid environments.

The Application Release Automation market is comprehensively segmented by type, application, and end-user to provide actionable insights for decision-makers and industry analysts. By type, the market includes cloud-based, on-premises, and hybrid solutions, each offering distinct operational benefits and integration capabilities. Application segments cover software deployment, continuous integration/continuous delivery (CI/CD), automated testing, and release orchestration, highlighting differing functional priorities across industries. End-user segmentation spans BFSI, IT & telecom, healthcare, retail, and manufacturing, reflecting the varied adoption patterns and deployment scale. North America and Europe show advanced adoption in enterprise IT operations, while Asia-Pacific SMEs are increasingly integrating ARA solutions to enhance operational efficiency. Adoption statistics indicate that approximately 68% of organizations prioritize cloud-based solutions, with software deployment and CI/CD applications dominating usage patterns. Overall, this segmentation provides a nuanced understanding of the market, guiding strategic investments and technology deployment decisions.

Cloud-based ARA solutions lead the market, accounting for 46% of total adoption due to their scalability, flexibility, and reduced infrastructure requirements. On-premises systems hold a 29% share, primarily in highly regulated sectors requiring strict data control. Hybrid solutions currently make up 25% of the market, offering a balance between on-premises security and cloud scalability. The fastest-growing segment is hybrid ARA, driven by enterprises seeking multi-cloud deployment capabilities and flexible release pipelines, expected to surpass 30% adoption by 2032. Other niche types include container-focused automation and AI-integrated orchestrators, together representing 15% of the market, catering to specialized operational needs.

Software deployment dominates the Application Release Automation market with a 44% share, primarily due to its role in accelerating development cycles and improving operational reliability. CI/CD pipelines are the fastest-growing application, with adoption expected to rise above 35% by 2032, supported by the growing need for automated testing and continuous monitoring. Automated testing and release orchestration collectively account for 21% of the application market, serving enterprises seeking precision and risk mitigation.

The BFSI sector leads end-user adoption of Application Release Automation, accounting for 42% of total implementation, driven by the need for secure, rapid, and reliable software updates. IT and telecom firms are the fastest-growing end-users, with adoption projected to exceed 38% by 2032, fueled by multi-cloud deployments and increased DevOps integration. Healthcare and retail segments collectively represent 31% of the market, utilizing ARA solutions to enhance operational efficiency and compliance. Manufacturing accounts for a smaller 12% share but is expanding due to Industry 4.0 automation initiatives.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12% between 2025 and 2032.

North America’s dominance is driven by extensive enterprise adoption across BFSI, healthcare, and IT sectors, with over 65% of large enterprises implementing cloud-based ARA solutions. Europe follows with a 28% share, emphasizing compliance-driven deployments. Asia-Pacific already holds 18% market volume but is rapidly scaling due to digital transformation initiatives in China, India, and Japan. Latin America represents 7% of the market, with government-backed infrastructure projects fueling automation uptake. Middle East & Africa collectively contribute 5%, driven by oil, gas, and construction sector modernization. Adoption statistics indicate over 60% of enterprises across North America and Europe now prioritize hybrid or cloud-native ARA solutions, while Asia-Pacific shows 58% adoption in SME and e-commerce sectors, highlighting regional variations in deployment scale and technology use.

How are enterprise adoption patterns shaping software release automation efficiency?

North America holds 42% of the global Application Release Automation market, with higher adoption in healthcare and finance sectors. Regulatory initiatives, such as enhanced cybersecurity frameworks, are driving compliance-focused automation. Technological advancements include AI-driven release orchestration and predictive monitoring. Local players like Broadcom and VMware are enhancing multi-cloud ARA platforms, reducing deployment downtime by over 35% across enterprise IT operations. Regional consumer behavior indicates preference for cloud-based solutions and integration with DevOps pipelines, with 68% of enterprises adopting hybrid deployment models to balance security and scalability. Continuous digital transformation and the push for faster software delivery are fueling the expansion of ARA in this region.

What are the key factors influencing automation adoption in regulated enterprise environments?

Europe accounts for 28% of the Application Release Automation market, with Germany, the UK, and France being the top contributors. Regulatory pressures and sustainability initiatives, such as GDPR compliance and ESG mandates, drive explainable and secure release automation adoption. Organizations are integrating AI-assisted pipelines and containerized deployment solutions to improve release quality. Local players, including Micro Focus, have implemented automated orchestration tools in financial institutions, achieving a 32% reduction in deployment errors. Enterprises in Europe prioritize compliance and reliability, with 60% favoring cloud-based hybrid ARA models, particularly in banking, healthcare, and manufacturing sectors.

How is the surge in digital transformation driving enterprise automation in emerging economies?

Asia-Pacific holds 18% of the Application Release Automation market, with China, India, and Japan leading consumption. Rapid growth in IT services, e-commerce, and manufacturing sectors fuels adoption. Infrastructure modernization, particularly in smart factories, supports automated release pipelines, while tech innovation hubs in Singapore and South Korea focus on cloud-native and AI-integrated ARA solutions. Local players, such as Infosys and Tata Consultancy Services, have deployed hybrid ARA systems, improving deployment efficiency by 37% across regional clients. Regional behavior shows SMEs embracing mobile AI apps and multi-cloud automation, with 58% actively integrating ARA for operational scalability.

What drives automation adoption in media, energy, and enterprise services sectors?

South America accounts for 7% of the global ARA market, with Brazil and Argentina as key contributors. Energy sector modernization and digital media localization drive demand, with 54% of enterprises adopting cloud-based release solutions. Government incentives for IT infrastructure upgrades and cross-border trade agreements encourage ARA adoption. Local players are increasingly deploying automated release pipelines to reduce downtime and enhance operational efficiency. Regional consumer behavior shows high engagement in media, retail, and language-based applications, with enterprises prioritizing multi-environment deployments and compliance tracking.

How is modernization of oil, gas, and construction sectors shaping software deployment trends?

Middle East & Africa represent 5% of the ARA market, with UAE and South Africa leading adoption. Growth is driven by modernization in oil, gas, and construction sectors, and digital transformation initiatives in government and financial institutions. Technological advancements include hybrid cloud deployments and AI-based orchestration tools. Local players are implementing predictive monitoring and automated rollback systems to ensure secure releases. Regional consumer behavior favors multi-cloud and on-premises hybrid solutions, with 52% of enterprises prioritizing operational reliability and compliance across diverse industrial and commercial applications.

United States: Market share 35%; high enterprise adoption across finance, healthcare, and IT sectors drives leadership in ARA deployment.

Germany: Market share 14%; strong regulatory compliance initiatives and advanced technological infrastructure position Germany as a top ARA market.

The Application Release Automation (ARA) market is moderately fragmented, with over 60 active global competitors operating across multiple regions and industry sectors. North America hosts the highest concentration of vendors, accounting for approximately 42% of market activity, while Europe contributes 28% and Asia-Pacific 18%. The top five companies collectively hold around 52% of the market, reflecting a competitive yet balanced landscape where mid-sized players maintain significant influence. Strategic initiatives such as AI-enabled orchestration, multi-cloud deployment solutions, and predictive monitoring are shaping competition, with 47% of vendors investing in integrated DevOps pipelines and automated testing frameworks. Partnerships and acquisitions are accelerating product innovation, with 33% of leading firms entering collaborations for enhanced cloud-native or hybrid automation solutions. Notable product launches in 2024–2025 include hybrid ARA platforms supporting automated rollback, error prediction, and performance analytics. The competitive environment is increasingly innovation-driven, emphasizing reduced deployment downtime, cross-environment orchestration, and improved operational reliability. Companies are also focusing on regulatory compliance, ESG-aligned practices, and regional customization to maintain a strong market presence.

Micro Focus International

CA Technologies

Electric Cloud

XebiaLabs

CloudBees

Atlassian Corporation

Digital.ai

The Application Release Automation (ARA) market is increasingly shaped by advanced technologies that enhance deployment speed, reliability, and scalability. AI and machine learning integration is driving predictive analytics in release pipelines, enabling enterprises to identify potential failures before deployment, which has improved error detection by approximately 34% in early adopter organizations. Cloud-native solutions and containerization are enabling seamless multi-environment deployments, with hybrid cloud architectures now adopted by 25% of global enterprises to manage distributed software releases. Automated rollback mechanisms and environment provisioning tools further reduce downtime, with firms reporting up to 38% faster recovery from release issues.

Emerging trends include the integration of DevSecOps principles directly into ARA workflows, embedding security validation within CI/CD pipelines to reduce vulnerabilities by 28% and ensure regulatory compliance in sectors like BFSI and healthcare. Low-code/no-code platforms are also being incorporated to streamline pipeline creation and modification, reducing manual configuration efforts by 30% and accelerating developer adoption. Predictive monitoring and observability tools are providing real-time insights into release performance across hybrid and multi-cloud environments, allowing IT teams to optimize resource allocation and system throughput.

Additionally, AI-driven chatbots and automated decision engines are being deployed to assist in release approvals and anomaly resolution, improving operational efficiency by 25% in enterprises with complex, multi-application landscapes. Quantum-inspired testing frameworks are beginning to influence early-stage ARA platforms, particularly in high-performance computing and financial trading systems, where release accuracy and speed are critical. Collectively, these technological advancements position ARA as a strategic tool for accelerating digital transformation, improving software delivery quality, and enabling scalable, resilient enterprise IT operations.

Broadcom Introduces VMware Tanzu Platform 10

In August 2024, Broadcom unveiled VMware Tanzu Platform 10, designed to accelerate intelligent application delivery in private cloud environments. This platform enhances automation capabilities, streamlining the application release process for enterprises. (Broadcom News and Stories)

IBM Launches watsonx Code Assistant for Z

IBM introduced the watsonx Code Assistant for Z in May 2024, aiming to accelerate the application lifecycle with generative AI and automation. This tool assists developers in modernizing mainframe applications, enhancing efficiency in the release process. (IBM Newsroom)

Broadcom Partners with NVIDIA for Private AI Solutions

In May 2024, Broadcom announced the general availability of VMware Private AI Foundation with NVIDIA, delivering a private and secure generative AI platform for enterprises. This collaboration aims to enhance application release automation through advanced AI capabilities.

IBM's Strategic Partnership with Anthropic

In October 2025, IBM and Anthropic formed a strategic partnership to integrate Anthropic's Claude large language model into IBM's AI-powered integrated development environment (IDE). This integration is expected to enhance enterprise software development, including application release automation processes. (TechRadar)

The Application Release Automation (ARA) market report offers a comprehensive analysis of the industry's current landscape and future directions. It covers various market segments, including product types, applications, and end-user industries, providing a detailed overview of each. The report delves into geographic regions, highlighting key markets such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, and examines regional adoption trends and growth drivers. In terms of applications, the report explores the utilization of ARA in sectors like healthcare, finance, retail, and manufacturing, emphasizing how automation enhances efficiency and reduces deployment risks in these industries. It also addresses the integration of emerging technologies, such as artificial intelligence, machine learning, and cloud computing, into ARA solutions, and their impact on the market.

The report also provides insights into the competitive landscape, profiling major players in the ARA market and discussing their strategic initiatives, including product innovations, partnerships, and acquisitions. It highlights the market's fragmented nature, with numerous vendors offering diverse solutions catering to various customer needs. Additionally, the report examines the regulatory environment affecting the ARA market, focusing on compliance requirements and standards that influence the adoption and implementation of automation solutions. It also considers the challenges and opportunities within the market, offering a balanced perspective for stakeholders. Overall, the Application Release Automation market report serves as a valuable resource for decision-makers, providing in-depth insights into the market's dynamics, trends, and future prospects.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2520.03 Million |

|

Market Revenue in 2032 |

USD 5807.51 Million |

|

CAGR (2025 - 2032) |

11% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Broadcom Inc., VMware, Inc., IBM Corporation, Micro Focus International, CA Technologies, Electric Cloud, XebiaLabs, CloudBees, Atlassian Corporation, Digital.ai |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |