Reports

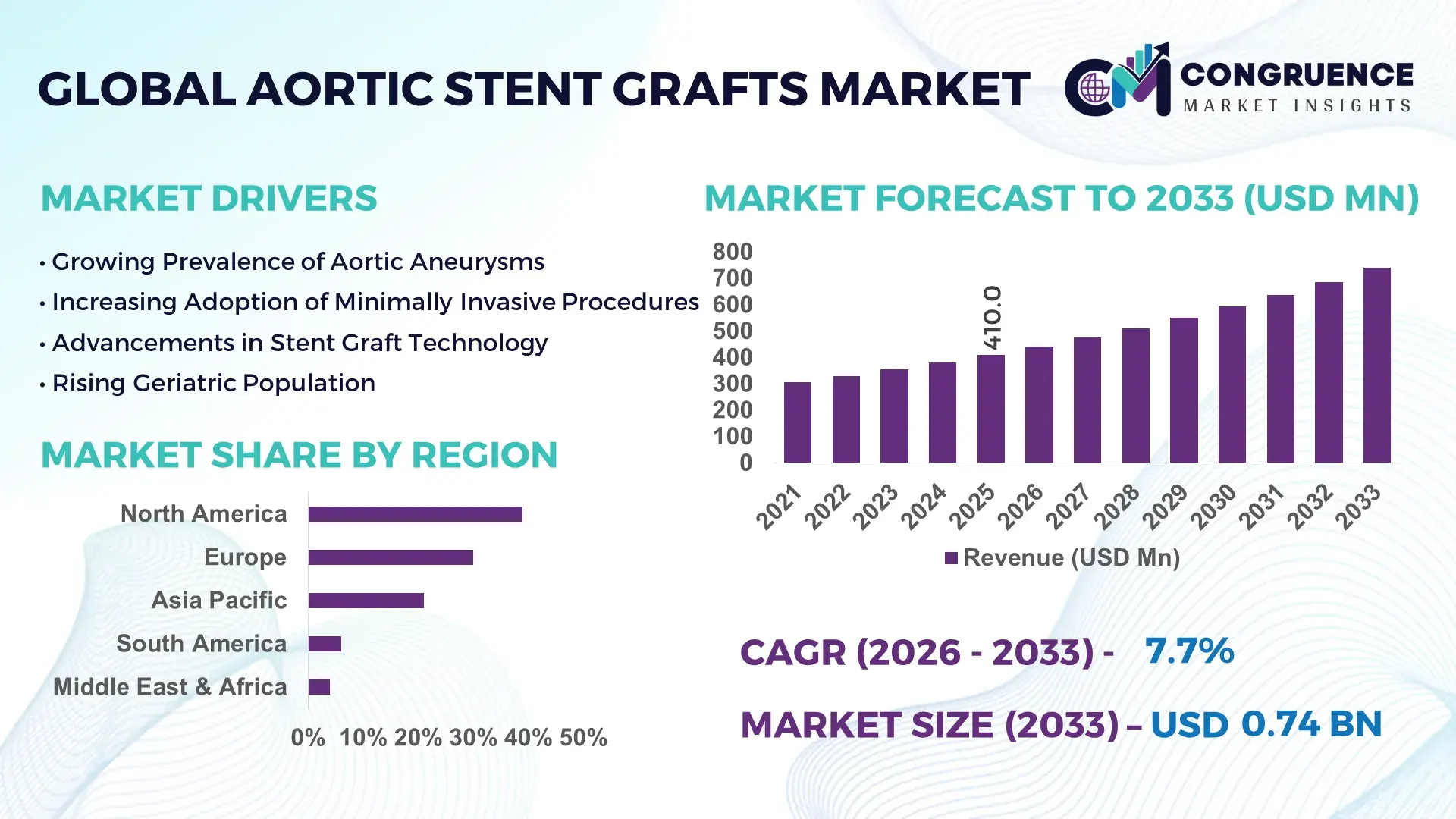

The Global Aortic Stent Grafts Market was valued at USD 410.0 Million in 2025 and is anticipated to reach a value of USD 739.4 Million by 2033 expanding at a CAGR of 7.65% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is expanding steadily due to the increasing prevalence of aortic aneurysms, rising geriatric population, and growing preference for minimally invasive endovascular repair procedures over open surgical interventions.

The United States remains the dominant country in the Aortic Stent Grafts Market, supported by advanced vascular surgery infrastructure and high procedural volumes. Over 200,000 abdominal aortic aneurysm (AAA) cases are diagnosed annually in the U.S., with nearly 45,000 endovascular aneurysm repair (EVAR) procedures performed each year. More than 75% of elective AAA repairs are conducted using endovascular stent graft systems. The country hosts multiple large-scale manufacturing and R&D facilities focused on next-generation fenestrated and branched stent grafts, with annual medical device R&D expenditure exceeding USD 15 billion across cardiovascular segments. Technological integration, including 3D imaging-guided deployment systems and low-profile delivery catheters below 16F, continues to enhance precision and patient outcomes.

Market Size & Growth: USD 410.0 Million (2025) projected to reach USD 739.4 Million by 2033 at 7.65% CAGR, driven by 70% shift toward minimally invasive EVAR procedures.

Top Growth Drivers: 75% adoption of endovascular repair in elective AAA cases; 40% increase in geriatric population (65+); 30% reduction in hospital stay duration versus open surgery.

Short-Term Forecast: By 2028, advanced imaging integration is expected to reduce procedure time by 20% and complication rates by 15%.

Emerging Technologies: AI-assisted surgical planning, 3D-printed patient-specific grafts, low-profile delivery systems under 16F.

Regional Leaders: North America projected at USD 290.0 Million by 2033 with high EVAR penetration; Europe at USD 210.0 Million driven by screening programs; Asia-Pacific at USD 165.0 Million with rising tertiary care capacity.

Consumer/End-User Trends: 80% of procedures concentrated in tertiary hospitals; growing adoption in specialty cardiac centers with 25% faster recovery protocols.

Pilot or Case Example: In 2024, a U.S. vascular center achieved 18% reduction in reintervention rates using image-fusion guided EVAR.

Competitive Landscape: Market leader holds approximately 35% share, followed by major players including Medtronic, Cook Medical, Gore Medical, Endologix, and Terumo.

Regulatory & ESG Impact: Increasing compliance with FDA Class III device standards; 25% reduction targets in manufacturing waste by 2030.

Investment & Funding Patterns: Over USD 2.5 Billion invested globally in cardiovascular device R&D over the past three years, with growth in strategic acquisitions.

Innovation & Future Outlook: Expansion of branched and fenestrated graft platforms, robotics-assisted EVAR integration, and bioresorbable graft material research shaping long-term advancement.

Key industry sectors include hospitals contributing nearly 60% of procedural demand, specialty cardiac centers at 25%, and ambulatory surgical centers at 15%. Fenestrated and branched stent graft innovations improved anatomical compatibility by 30%, while stricter device surveillance regulations enhanced post-market compliance by 20%. North America leads consumption, followed by Europe’s structured screening programs. Future growth is aligned with precision-based vascular intervention and digital surgical planning ecosystems.

The Aortic Stent Grafts Market holds strategic importance within the global cardiovascular device ecosystem due to its role in reducing mortality from abdominal and thoracic aortic aneurysms. Endovascular aneurysm repair (EVAR) has transformed vascular surgery by offering minimally invasive alternatives that reduce hospital stays by nearly 30% and perioperative mortality by approximately 50% compared to open repair. AI-guided imaging systems deliver 25% improvement in deployment accuracy compared to conventional fluoroscopy-based planning.

North America dominates in procedure volume, while Europe leads in structured aneurysm screening adoption with over 65% of eligible male populations above age 65 enrolled in national screening programs in select countries. By 2028, AI-driven preoperative planning and robotic catheter navigation are expected to reduce operative complications by 20% and shorten recovery times by 15%.

Firms are committing to ESG metrics such as 30% reduction in polymer waste and improved recyclability of delivery systems by 2030. In 2024, a leading U.S. device manufacturer achieved a 22% improvement in device deployment precision through AI-integrated imaging platforms.

Looking ahead, the Aortic Stent Grafts Market is positioned as a pillar of resilience, regulatory compliance, and sustainable growth, driven by technological innovation, aging demographics, and evolving minimally invasive treatment standards.

The Aortic Stent Grafts Market is influenced by demographic aging, rising aneurysm detection rates, technological evolution in graft materials, and expansion of tertiary vascular centers. Increasing screening initiatives have improved early-stage aneurysm diagnosis by nearly 35% in developed healthcare systems. Procedural migration from open repair to EVAR continues to reshape procurement and hospital investment strategies. Device miniaturization, improved flexibility, and enhanced sealing mechanisms are reducing post-procedural complications such as endoleaks. Emerging economies are investing in catheterization laboratories and hybrid operating rooms, expanding procedural capacity by over 20% in urban centers. However, regulatory scrutiny and high device development costs continue to shape competitive positioning.

Minimally invasive EVAR procedures account for more than 75% of elective AAA repairs in developed markets. Compared to open surgery, EVAR reduces blood loss by nearly 40%, ICU stay by 50%, and overall hospitalization time by approximately 30%. Clinical studies show perioperative mortality rates of 1–2% for EVAR versus 4–5% for open repair. As hospitals prioritize faster patient turnover and improved surgical outcomes, procurement of advanced stent graft systems continues to increase. Growing patient awareness and insurance reimbursement coverage exceeding 80% in major healthcare systems further accelerate adoption.

Aortic stent graft systems are classified as high-risk Class III medical devices, requiring extensive clinical validation. Development cycles often exceed 5–7 years with clinical trial participation involving more than 500 patients per pivotal study. Regulatory compliance costs can account for nearly 20% of total development expenditure. Additionally, device costs per procedure can exceed USD 10,000, limiting adoption in cost-sensitive markets. Strict post-market surveillance and reporting requirements further increase operational overhead for manufacturers and healthcare providers.

Approximately 30% of aneurysm patients present with complex anatomies unsuitable for standard grafts. Fenestrated and branched stent grafts offer customized solutions, improving anatomical compatibility by nearly 35%. Advances in 3D imaging and patient-specific modeling reduce sizing errors by 20%. Emerging markets are expanding vascular labs by 25%, creating new avenues for adoption. Increasing use of AI-powered simulation tools enhances procedural planning accuracy and supports expansion into complex thoracic and abdominal repair segments.

Advanced stent graft deployment requires specialized vascular training and proficiency in imaging-guided navigation. In several emerging economies, less than 40% of vascular surgeons are certified for complex EVAR procedures. Learning curves can extend over 20–30 supervised cases. Complications such as endoleaks occur in approximately 10–15% of cases, necessitating reintervention. Investment in hybrid operating rooms may exceed USD 2 Million per facility, limiting expansion in smaller hospitals. These barriers slow uniform market penetration.

Expansion of Fenestrated and Branched Grafts: Fenestrated and branched devices now account for nearly 28% of complex AAA repairs. Clinical adoption improved procedural success rates by 32% in anatomically challenging cases. Hospitals integrating 3D preoperative modeling reported 20% reduction in sizing errors and 18% fewer secondary interventions.

Integration of AI-Based Imaging and Navigation: AI-powered imaging platforms enhance deployment precision by 25% and reduce fluoroscopy exposure by 15%. Facilities implementing image-fusion technology recorded 22% shorter operative durations and 17% lower contrast usage, improving patient safety outcomes.

Miniaturization and Low-Profile Delivery Systems: Delivery systems below 16F have increased patient eligibility by 30%, particularly among individuals with smaller iliac arteries. Reduced access-site complications by 21% have improved recovery timelines and decreased readmission rates.

Growth of Hybrid Operating Rooms: Over 45% of tertiary hospitals in developed regions now operate hybrid OR suites. These facilities improve surgical workflow efficiency by 27% and reduce emergency conversion to open surgery by 14%, strengthening procedural reliability and long-term patient outcomes.

The Aortic Stent Grafts Market is segmented by type, application, and end-user, reflecting clinical complexity, procedural settings, and patient demographics. By type, abdominal aortic stent grafts account for the majority of procedures due to higher incidence of abdominal aortic aneurysms (AAA), which represent nearly 70% of all diagnosed aortic aneurysms globally. Thoracic aortic stent grafts are increasingly utilized for thoracic aortic aneurysm (TAA) and dissections, particularly in aging populations above 65 years.

By application, endovascular aneurysm repair (EVAR) remains the dominant procedure, while thoracic endovascular aortic repair (TEVAR) is gaining traction in tertiary cardiac centers. Elective repair procedures account for more than 65% of total interventions, while emergency interventions form a critical yet smaller segment.

By end-user, hospitals dominate procedural volumes, followed by specialty cardiac centers and ambulatory surgical centers. Increasing investments in hybrid operating rooms and catheterization laboratories are reshaping procurement strategies and device adoption patterns across developed and emerging healthcare systems.

The market is categorized into Abdominal Aortic Stent Grafts, Thoracic Aortic Stent Grafts, Fenestrated Stent Grafts, and Branched Stent Grafts. Abdominal aortic stent grafts currently account for approximately 58% of total adoption, primarily due to the high prevalence of infrarenal abdominal aortic aneurysms, which represent nearly 70% of aneurysm diagnoses. In comparison, thoracic aortic stent grafts hold around 24% adoption, driven by increasing detection of thoracic aneurysms through advanced imaging. However, fenestrated and branched stent grafts are rising fastest and are expected to exceed 30% combined adoption by 2033, particularly for complex anatomies. Fenestrated stent grafts represent the fastest-growing segment, expanding at an estimated 9.2% CAGR, supported by demand for customized solutions in patients with short neck or juxtarenal aneurysms. These devices improve anatomical fit by nearly 35% compared to standard grafts. Branched graft systems also address multi-branch vascular reconstruction needs and are gaining usage in high-risk surgical cases. The remaining standard thoracic and hybrid graft systems collectively contribute nearly 18% of total procedures, serving niche but clinically critical applications.

In 2024, the U.S. Food and Drug Administration approved an advanced fenestrated abdominal aortic aneurysm device designed for complex anatomies, expanding patient eligibility by approximately 25% in specialized vascular centers.

The Aortic Stent Grafts Market is segmented into Endovascular Aneurysm Repair (EVAR), Thoracic Endovascular Aortic Repair (TEVAR), and Hybrid Aortic Repair Procedures. EVAR currently accounts for approximately 62% of total procedures, reflecting its status as the preferred treatment for elective abdominal aneurysms. TEVAR holds around 26% adoption, particularly in managing descending thoracic aneurysms and dissections. However, hybrid aortic repair procedures are growing fastest and are projected to expand at a 8.8% CAGR, supported by increasing use in complex arch and multi-segment pathologies. Elective interventions dominate application share at nearly 65%, while emergency procedures account for roughly 35%, reflecting acute rupture management needs. Growing screening programs in developed countries have increased early detection rates by nearly 30%, driving planned EVAR adoption. Consumer and institutional trends further support expansion. In 2025, nearly 42% of U.S. hospitals reported testing advanced imaging-assisted EVAR planning systems. Additionally, over 60% of tertiary vascular centers in Europe utilize image-fusion technology during TEVAR procedures to enhance deployment accuracy.

In 2024, the Centers for Disease Control and Prevention reported expanded AAA screening initiatives across multiple U.S. states, increasing early-stage aneurysm detection rates among men aged 65–75 by nearly 20%.

The market is segmented into Hospitals, Specialty Cardiac Centers, and Ambulatory Surgical Centers (ASCs). Hospitals dominate with approximately 68% of total procedural volume, supported by access to hybrid operating rooms and multidisciplinary vascular teams. Specialty cardiac centers account for nearly 22% adoption, offering focused expertise and advanced imaging-guided procedures. However, ambulatory surgical centers represent the fastest-growing end-user category, expanding at an estimated 8.5% CAGR, driven by shorter recovery protocols and cost-efficient care models. Hospitals maintain leadership due to capacity for high-risk and emergency interventions, while ASCs are increasingly handling elective EVAR cases, improving patient throughput by nearly 25%. Over 45% of tertiary hospitals in developed regions now operate dedicated hybrid OR suites to support complex aortic repairs. Adoption trends indicate that in 2025, approximately 38% of vascular centers globally piloted AI-integrated surgical navigation tools to enhance graft deployment precision. In the U.S., nearly 50% of large academic hospitals reported using 3D imaging software for preoperative aortic planning.

In 2024, the National Institutes of Health supported multi-center clinical studies across more than 100 U.S. hospitals to evaluate advanced endovascular devices, strengthening adoption among large tertiary care institutions.

North America accounted for the largest market share at 39% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2026 and 2033.

North America performed over 70,000 EVAR and TEVAR procedures annually, supported by more than 45% penetration of hybrid operating rooms in tertiary hospitals. Europe captured approximately 30% market share, driven by structured abdominal aortic aneurysm (AAA) screening programs covering nearly 65% of eligible male populations aged 65–75 in select countries. Asia-Pacific represented nearly 21% share, with China, Japan, and India collectively contributing over 60% of regional procedural volume. South America held around 6% share, while Middle East & Africa accounted for approximately 4%, reflecting improving but uneven access to advanced vascular care. Increasing investments in catheterization laboratories—up by nearly 25% in urban Asia-Pacific centers—and growing adoption of low-profile stent graft systems below 16F are reshaping global demand patterns.

North America holds approximately 39% of the global Aortic Stent Grafts Market, supported by high elective repair volumes and early adoption of advanced endovascular technologies. The region performs more than 75% of abdominal aneurysm repairs via EVAR, reflecting strong physician preference for minimally invasive interventions. Cardiovascular disease management programs and aging demographics—where nearly 17% of the population is aged 65+—sustain consistent demand. Regulatory oversight under Class III medical device pathways ensures rigorous safety validation, while reimbursement coverage for EVAR exceeds 80% across major payers, encouraging hospital procurement. Digital integration trends include AI-based imaging fusion systems used in nearly 50% of large tertiary hospitals to enhance deployment precision.

Europe accounts for nearly 30% of the global Aortic Stent Grafts Market, with Germany, the UK, and France collectively contributing over 55% of regional procedures. National AAA screening programs in several countries cover up to 65% of eligible men aged 65–75, significantly increasing early-stage diagnosis and elective EVAR volumes. The region operates under stringent medical device regulations aligned with enhanced post-market surveillance requirements, strengthening product quality and traceability standards. Approximately 48% of tertiary vascular centers use hybrid operating suites equipped with advanced fluoroscopic imaging. Adoption of fenestrated and branched grafts has increased by nearly 28% in complex anatomies.

Asia-Pacific represents approximately 21% of global market volume and ranks as the fastest-growing region. China, Japan, and India collectively account for more than 60% of regional consumption, supported by expanding tertiary hospital networks and increasing cardiovascular screening initiatives. Urban healthcare infrastructure investments have grown by nearly 30% in major metropolitan areas, including expansion of catheterization laboratories. Japan reports over 15,000 EVAR procedures annually, while China has increased endovascular intervention capacity by approximately 25% over five years. Manufacturing localization is rising, with domestic medical device production facilities expanding output to reduce import dependency.

South America accounts for approximately 6% of global market share, led by Brazil and Argentina, which together contribute over 70% of regional procedural volume. Public healthcare modernization initiatives have expanded tertiary hospital capacity by nearly 18% over the past five years. Brazil has increased access to hybrid surgical facilities in major cities, improving emergency aneurysm response times by nearly 15%. Trade policies facilitating medical device imports have reduced procurement lead times by approximately 12%. Growing private healthcare participation supports elective EVAR expansion in metropolitan regions. Regional demand is influenced by urban healthcare access disparities, with nearly 65% of advanced vascular procedures concentrated in capital cities. Increased training programs for vascular surgeons are gradually improving certification levels for complex EVAR deployment.

Middle East & Africa holds approximately 4% of global market share, with the UAE and South Africa representing nearly 50% of regional procedural activity. Government-backed healthcare expansion initiatives have increased specialized cardiac center capacity by approximately 22% in Gulf countries. Technological modernization trends include installation of advanced imaging suites in over 40% of new tertiary hospitals across leading Middle Eastern cities. Regional procurement strategies increasingly emphasize international device partnerships and compliance with stringent quality benchmarks. In the UAE, specialized cardiovascular centers report a 20% increase in minimally invasive aneurysm repairs over three years, reflecting patient preference for shorter recovery periods. Trade collaborations and public-private healthcare investments continue to support procedural capability expansion.

United States – 36% Market Share: Strong procedural volume exceeding 70,000 annual EVAR/TEVAR cases and advanced hybrid operating infrastructure drive leadership in the market.

Germany – 9% Market Share: Structured national screening programs and high concentration of specialized vascular centers sustain Germany’s leading position in the Market within Europe.

The Aortic Stent Grafts Market demonstrates a moderately consolidated structure, with the top five companies collectively accounting for approximately 68% of global market share. More than 20 active manufacturers operate across abdominal, thoracic, fenestrated, and branched stent graft segments; however, competitive intensity is highest among a core group of multinational cardiovascular device leaders. The market leader holds close to 35% share, supported by a broad endovascular portfolio and global distribution coverage spanning over 100 countries.

Competition is primarily driven by innovation in low-profile delivery systems below 16F, advanced conformable graft materials, and patient-specific fenestrated designs addressing nearly 30% of complex aneurysm anatomies. Over the past three years, the industry has recorded more than 15 regulatory approvals for next-generation graft systems targeting improved seal integrity and reduced endoleak incidence rates, currently observed in 10–15% of procedures.

Strategic initiatives include mergers to expand thoracic repair capabilities, partnerships with imaging technology providers to integrate AI-based preoperative planning, and clinical trial investments exceeding 500–1,000 patient enrollments per pivotal study. Companies are also strengthening physician training ecosystems, conducting over 200 annual hands-on workshops globally to address procedural complexity. Product differentiation increasingly centers on durability testing exceeding 400 million simulated cardiac cycles, reinforcing long-term device performance claims.

Terumo Aortic

Endologix LLC

MicroPort Endovascular MedTech

Lombard Medical Technologies

JOTEC GmbH

Braile Biomédica

Lifetech Scientific Corporation

Eucatech AG

Cordis Corporation

Bentley InnoMed GmbH

Endospan Ltd.

Artivion, Inc.

Technological innovation in the Aortic Stent Grafts Market is centered on device miniaturization, advanced biomaterials, digital surgical planning, and enhanced durability testing. Modern low-profile delivery systems under 16F have increased patient eligibility by nearly 30%, particularly among individuals with smaller iliac access vessels. Improvements in nitinol stent architecture provide radial force optimization while maintaining flexibility, reducing migration risk by approximately 18% compared to earlier-generation platforms.

Fenestrated and branched graft technologies now address nearly 30% of anatomically complex aneurysms, enabling treatment of short-neck and juxtarenal pathologies. Customization through 3D-printed patient-specific planning models has reduced sizing inaccuracies by 20%, improving first-time deployment success rates.

AI-integrated imaging fusion systems enhance intraoperative visualization, reducing fluoroscopy exposure by 15–20% and contrast media usage by nearly 17%, lowering renal complication risks. Robotics-assisted catheter navigation platforms are being evaluated in tertiary centers to improve deployment precision by over 20%.

Durability benchmarks now exceed 400 million fatigue cycles, simulating more than 10 years of cardiac pulsation. Polymer graft fabrics are engineered for reduced permeability, minimizing type IV endoleak incidence. Furthermore, ESG-driven manufacturing improvements target 25–30% reductions in production waste by 2030, aligning technological advancement with sustainability commitments.

• In October 2025, Medtronic received FDA labeling approval for its Endurant™ stent graft system to remove the warning against use in ruptured abdominal aortic aneurysm (rAAA), making it the first and only endovascular graft with this updated indication and empowering clinicians with confidence in emergency rAAA treatment. Source: www.news.medtronic.com

• In 2025, Endovastec™ announced multiple global clinical adoption milestones for its aortic stent graft portfolio, including first commercial implantations of the Minos™ Abdominal Aortic Stent Graft in Kazakhstan and Malaysia, and first use of its Talos™ Thoracic Stent Graft System in South America and Argentina, reflecting expanded international procedures. Source: www.endovastec.com

• In May 2025, Artivion reported its first-quarter 2025 financial results highlighting a 14% year-over-year growth in aortic stent graft sales, supported by progress in its NEXUS TRIOMPHE IDE trial showing a 63% reduction in major adverse event (MAE) rate versus the reference goal at the AATS Annual Meeting. Source: www.investors.artivion.com

• In April 2025, Gore & Associates announced expanded FDA approval for its TAG Conformable Thoracic Stent Graft with Active Control System featuring four new large-diameter tapered designs (34×28 mm to 45×37 mm) to broaden treatment options for complex thoracic aortic aneurysms. Source: www.evtoday.com

The Aortic Stent Grafts Market Report provides a comprehensive evaluation of product categories including abdominal, thoracic, fenestrated, branched, and hybrid graft systems. The report analyzes procedural segmentation such as EVAR, TEVAR, and hybrid aortic repair interventions, covering elective and emergency applications representing nearly 65% and 35% of procedures, respectively.

Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, incorporating regional infrastructure metrics such as hybrid operating room penetration exceeding 45% in developed markets and tertiary hospital expansion rates approaching 25% in urban Asia-Pacific regions.

Technology assessment includes low-profile delivery platforms below 16F, AI-powered imaging integration adopted in nearly 50% of large tertiary hospitals, durability testing beyond 400 million cycles, and patient-specific 3D modeling reducing deployment errors by 20%.

The report further evaluates end-user segments including hospitals (approximately 68% procedural volume), specialty cardiac centers, and ambulatory surgical centers. It incorporates regulatory frameworks, device validation pathways, physician training benchmarks, and ESG manufacturing targets such as 25–30% waste reduction goals.

Emerging focus areas include robotics-assisted catheter navigation, advanced polymer graft materials, and expansion of customized fenestrated solutions addressing nearly 30% of complex anatomical cases, positioning the report as a strategic tool for stakeholders assessing investment, innovation, and operational expansion opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 410.0 Million |

| Market Revenue (2033) | USD 739.4 Million |

| CAGR (2026–2033) | 7.65% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Medtronic plc; W. L. Gore & Associates; Cook Medical; Terumo Aortic; Endologix LLC; MicroPort Endovascular MedTech; Lombard Medical Technologies; JOTEC GmbH; Braile Biomédica; Lifetech Scientific Corporation; Eucatech AG; Cordis Corporation; Bentley InnoMed GmbH; Endospan Ltd.; Artivion, Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |